Polyhydroxyalkanoates (PHA) Market Size

Ukhi Bioplastics Private Limited India

- A detailed examination of why 2025–2026 marks the critical transition of PHA from a high-cost medical niche to a scalable industrial material, including capacity forecasts through 2030.

- An accessible breakdown of Next-Generation Industrial Biotechnology (NGIB), explaining how salt-loving “extremophiles” and seawater-based fermentation are slashing production costs.

- Granular snapshots of 12 global powerhouses, including China’s massive scaling, Japan’s retail integration, Brazil’s energy-independent production, and India’s emerging ag-waste potential.

- Comprehensive profiles of the “Big Nine” global leaders and specialized innovators, covering their patented extraction methods, production capacities, and strategic alliances.

- Practical analysis of “White Spaces” in the market, focusing on PHA’s entry into the CO2-to-plastic and polyurethane-replacement sectors.

Publication Details

Publication Date: 20th February 2026

Publisher: Ukhi India Pvt. Ltd.

Location: New Delhi, India

Report Period Covered: 2018–2030

Data Last Updated: October 2025

Disclaimer

This report is based on data and information available from government publications, peer-reviewed research, and verified industry sources as of February 2026. While every effort has been made to ensure accuracy, Ukhi does not guarantee completeness in cases where official data is unavailable or incomplete. The report prioritizes factual integrity and transparency over speculative modelling.

EXECUTIVE SUMMARY

PHA at a Turning Point in 2026

The year 2026 marks a structural turning point for Polyhydroxyalkanoates (PHA).

For more than two decades, PHA has existed at the edges of the bioplastics industry. It has been technically impressive, environmentally superior, but commercially constrained.

In 2026, that balance begins to shift.

Three forces converge at this moment.

- First, regulatory pressure is in full force on the plastic producing and consuming industries. More than 50 countries have enacted bans or restrictions on conventional single-use plastics already. This has created an enforced demand for materials that can safely degrade outside controlled industrial systems, and PHA is an important one.

- Second, industrial technology relevant to PHA has matured. The bioplastics industry (particularly with reference to PHA value chains) is moving beyond early, expensive fermentation models.

- Third, market pull has become sector-specific. PHA IS gaining traction in applications where its unique properties are absolutely necessary.

As a result, PHA is transitioning from a future material to a polymer relevant today, especially in environmentally sensitive and high-value applications.

Five Things You Need to Know Now

- PHA is uniquely biodegradable in real world environments.

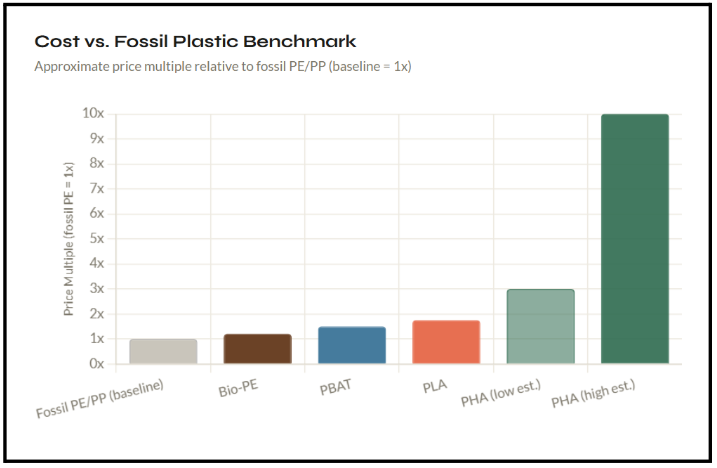

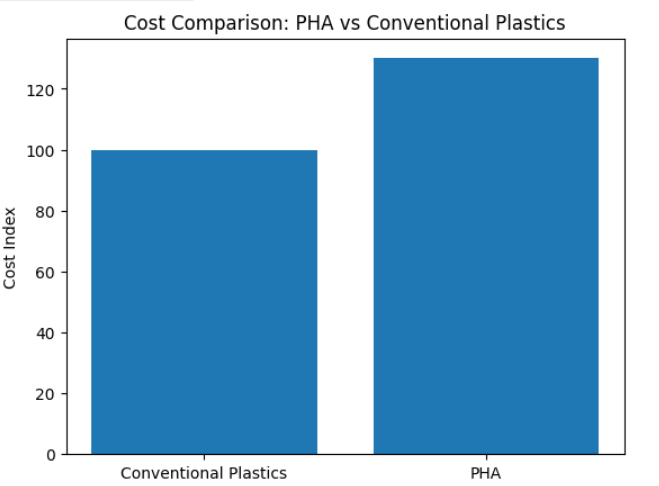

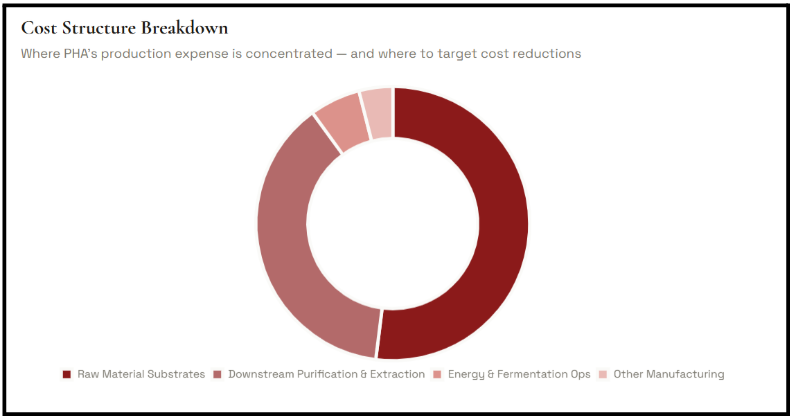

It is the only fully biosynthesized polymer certified to biodegrade in soil, freshwater, and marine conditions. Unlike materials such as PLA, which depend on industrial composting, PHA can break down under ambient conditions and reduce long-term microplastic risk. - Cost remains the single largest barrier.

Despite progress, PHA remains 3 to 10 times more expensive than traditional Polyethylene (PE), with raw materials alone making up 50% of the bill. Downstream recovery and purification account for up to another 50%. Cost reduction is therefore not incremental, it is more structural. - The industry is shifting to waste-based feedstocks.

Municipal food waste, sewage sludge, spent coffee grounds, and captured CO₂ are now central to PHA R&D strategies. PHA produced from urban biowaste has already demonstrated lower environmental impact and lower societal costs than fossil-based polyurethane in comparable applications. - Next-Generation Industrial Biotechnology (NGIB) is changing the economics of PHA.

The transition to Next-Generation Industrial Biotechnology (NGIB) is now active. The use of halophilic (salt-loving) bacteria allows for unsterile, continuous production in open tanks, which drastically lowers capital requirements. - PHA is not one material.

With over 150 different monomers, PHA can be engineered to be as rigid as a car bumper or as flexible as a rubber band.

Global Market Size Snapshot

The global PHA market remains small in absolute terms but is expanding rapidly.

As of 2023, market size estimates for PHA ranged widely (from USD 93.55 million to USD 650.7 million). This reflects differences in how analysts define scope and applications.

Despite this variance, all projections point towards PHA’s accelerated growth. By 2030, the market is expected to reach approximately USD 1.22 billion.

With a Compound Annual Growth Rate (CAGR) of between 14.2% and 29.4%, PHA is outstripping the growth of almost all fossil-fuel based polymers.

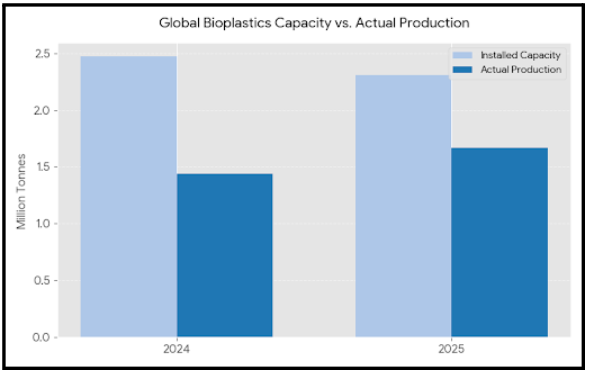

From a volume perspective, global PHA production capacity crossed 70,000 metric tons in 2024. This represented about 4.1% of total global bioplastics capacity.

Installed Capacity vs Demand Gap

Despite rising interest, the PHA market is constrained by a gap between installed capacity and effective demand.

1. Across all bioplastics (not merely PHA), capacity utilisation stood at around 58% in 2024. This meant a production of roughly 1.44 million tonnes against installed capacity of 2.47 million tonnes. This utilisation rate is expected to have risen to 72% by 2025.

2. In PHA specifically, more than 120 companies are engaged in research or early-stage production. Their aggregate capacity still trails the massive demand created by European and North American packaging mandates.

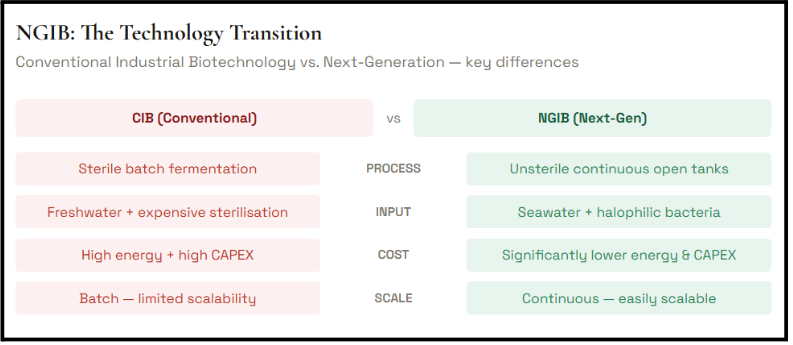

3. The “sterile batch” bottleneck remains. Until NGIB (Next-Gen) plants reach the 50,000-tonne individual scale, we will continue to see a deficit in available resin for multinational converters.

Ukhi explains: The “sterile batch” bottleneck refers to the intensive technical and financial burden of maintaining a 100% contaminant-free environment during the fermentation process.

Because PHA is produced by “feeding” specific bacteria, any foreign microbe that enters the tank can quickly outcompete the production strain, as it can eat the expensive feedstock without producing any plastic.

To prevent this, traditional factories must follow a “sterile batch” protocol:

- High Energy Costs: Large volumes of water and growth media must be pressurized and heated to over 121°C (autoclaving) to kill all existing microbes before every new batch begins.

- Downtime: After each batch is harvested, the entire bioreactor must be deep-cleaned and re-sterilized. This process can take hours or even days, during which no plastic is being made.

- Infrastructure Complexity: Maintaining “aseptic” (sterile) conditions requires expensive stainless-steel tanks, specialized air filtration, and complex piping to ensure no leakage of outside air occurs.

This creates a bottleneck because it makes scaling up to 50,000+ tonne facilities exponentially expensive. Every increase in tank size requires more energy to heat and more sophisticated engineering to keep sterile.

Next-Generation Industrial Biotechnology (NGIB) solves this by using “extremophile” bacteria that thrive in high-salt or high-pH environments where most common contaminants simply cannot survive. This allows for unsterile, continuous production in cheaper, open tanks.

On the demand side, PHA’s high prices restrict its adoption to premium segments such as medical devices, agriculture, and regulated packaging. However, policy-driven demand is beginning to pull PHA into larger volume applications despite the cost gap.

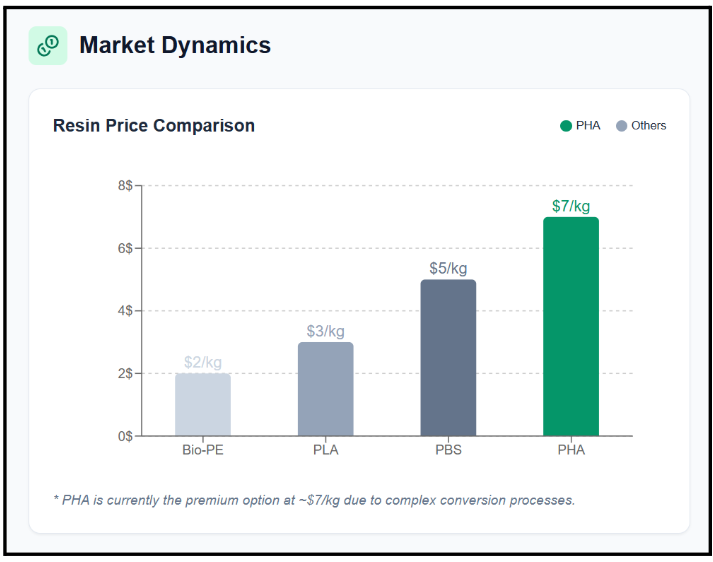

Price Comparison

Price is the most visible challenge for PHA.

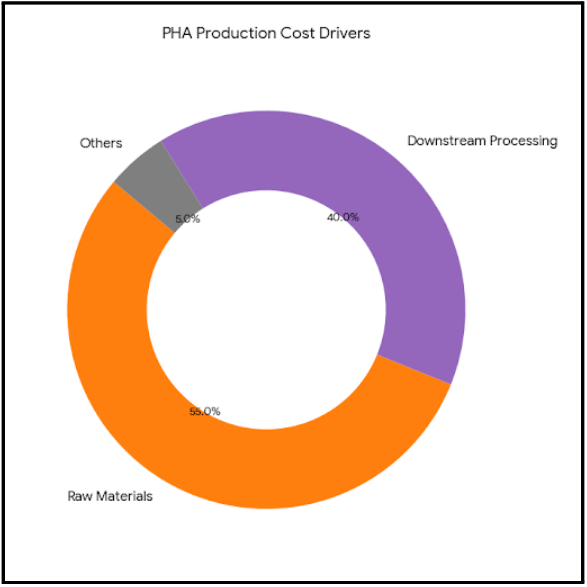

The key cost drivers are:

- Feedstocks, accounting for 50–60% of production cost

- Downstream recovery and purification, accounting for 30–50%

So, technologies that reduce feedstock cost and simplify recovery will determine whether PHA can compete beyond premium niches.

Ukhi explains: At Ukhi, we believe in radical transparency regarding cost. Parity with oil-based plastics is not yet here, but the gap is narrowing.

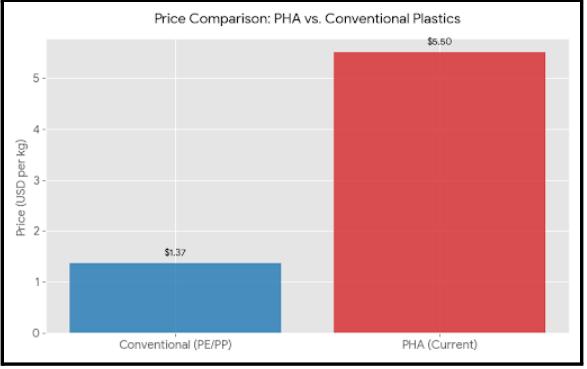

| Material Type | Price Range (USD/kg) | Relative Comparison |

|---|---|---|

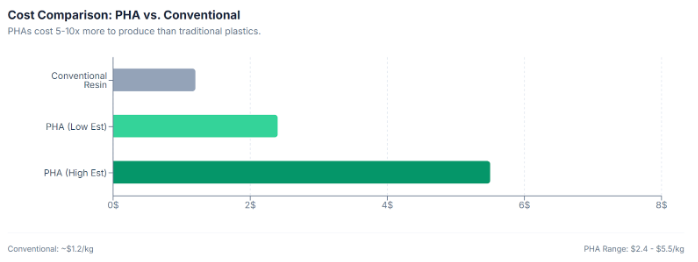

| Fossil Plastics (PE/PP) | $1.00 – $1.74 | The Global Benchmark |

| PLA (Polylactic Acid) | $2.00 – $3.00 | Mature Bioplastic |

| PHA (Current) | $4.00 – $7.00 | The Premium Tier |

| PHA (Historical – 2002) | $9.50 | Historical Reference |

What This Means for Stakeholders

- For Brand Owners: Incorporating PHA is currently a Brand Equity play. The higher cost must be offset by the marketing value of a truly marine-safe product.

- For Manufacturers: Focus on Copolymers (like PHBV). They are less brittle than pure PHB and provide a wider processing window, which means less machine downtime and wasted material.

- For Investors: The area of focus is Downstream Processing. Any technology that can reduce the 30–50% cost of extracting PHA from the bacteria is a high-value acquisition target.

The Bottom Line

PHA enters 2026 at a decisive moment.

Its environmental advantages are no longer debated.

Its technical limitations are understood and addressed.

What remains unresolved is scale and cost.

If next-generation production models deliver as expected, PHA will move from a niche sustainability material to a core polymer for regulated, high-impact applications.

If not, it will remain constrained to premium segments.

2. About This Report

This Ukhi PHA Market Research Report 2026–2030 is intended as a comprehensive and practical guide for decision-makers trying to make sense of the most complex and promising segment of the bioplastics industry — polyhydroxyalkanoates (PHA).

Our purpose is to provide a single source of truth that uses technical data and market analysis to deliver plain-language actionable insights for business leaders and policy architects.

2.1 Scope of the Report (PHA only)

This analysis focuses exclusively on the Polyhydroxyalkanoates (PHA) family of polymers. Unlike broader bioplastic reports, our analysis is focused on the PHA value chain, including:

- Global and regional market size and growth,

- Feedstocks, production methods, and technological advances,

- Application areas (e.g., packaging, agriculture, medical, consumer goods),

- Regulatory and policy landscape,

- Competitive dynamics and key players,

- Opportunities, risks, and major challenges facing the PHA industry.

2.2 Geographic Coverage (Global + 9 Countries)

The report provides a global outlook with deep-dive strategic profiles of9 key countries currently leading PHA innovation or adoption:

- Asia-Pacific: China, India, and Thailand.

- Europe: Germany, Italy, and United Kingdom.

- Americas: USA, Canada, and Brazil.

2.3 Time Horizon (2018–2030)

Our report analyses market trends and developments from 2018 through 2030, with:

- Historical (2018–2024): The ‘CIB’ (Conventional Industrial Biotechnology) era and early market

- Current State (2025–2026): The rise of Next-Gen fermentation

- Forecast (2027–2030): Capacity surges and the path toward cost parity with fossil-fuel plastics

2.4 Methodology & Sources

We base our findings on multiple independent data sources:

- Analysis of 2025/2026 investor filings and production reports from global bioplastics leaders

- Peer-reviewed scientific publications

- Industry whitepapers

- Policy documents and regulatory frameworks

- Expert interviews and presentations at global conferences

Where discrepancies or data gaps exist, we have chosen accuracy and transparency over completeness.

2.5 Limitations & Assumptions

- Market data on PHA is highly fragmented.

- Some figures are based on the most credible sources available as of publication (February 2026), but may be revised.

- Some “announced” industrial capacities may face delays due to downstream processing bottlenecks.

2.6 Note on Data Sources, Variations, and Our Approach

This report draws on multiple publicly available data sources, including industry associations, regional market studies, company disclosures, and policy documents.

Because the PHA and bioplastics sectors are still emerging, the data landscape is fragmented. Different analysts use different definitions, timeframes, and assumptions. As a result, market size and growth figures often vary — sometimes significantly.

Rather than hide these differences, we believe it is more responsible to explain them clearly.

1. Global Bioplastics Market – Data Variations

Production Capacity

One consistent reference point across sources is total global bioplastics production capacity:

- 2.47 million tonnes in 2024

This figure refers to installed production capacity across all bioplastics, not actual output.

Market Value

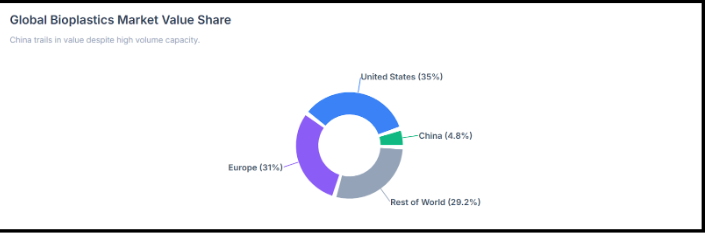

There is no single agreed global market value number across all sources. Instead, regional shares are often reported:

- United States: 35% of global value

- Europe: 31%

- China: 4.8%

These value shares are not contradictory, but they reflect different measurement bases — some include all bio-based plastics, while others focus only on biodegradable plastics.

Growth Rates

A single global CAGR for all bioplastics is rarely reported. Instead, growth is presented regionally:

- Europe: 11.46% (2025–2033)

- Australia: 7.6% (2025–2031)

These regional rates cannot be directly averaged into a global number because they cover different product mixes and baseline years.

2. Global PHA Market – Where Contradictions Are Most Visible

PHA data varies more sharply than overall bioplastics data. This is typical for smaller, early-stage markets.

A. Market Value – Wide Ranges

Reported estimates for global PHA market value differ substantially:

For 2023:

- Low estimate: USD 93.55 million

- High estimate: USD 650.7 million

For 2024:

- One estimate: USD 714.7 million

Future projections:

- USD 1.22 billion by 2030

- USD 1.5 billion by 2025 (aggressive scenario)

- USD 167–171 million between 2027–2034 (much lower projection)

These differences arise from:

- Whether medical applications are included

- Whether copolymers (e.g., PHBV) are included

- Whether forecasts assume rapid industrial scale-up

- Whether projections are volume-based or revenue-based

- Different baseline years

The smaller projection (USD 167–171 million) likely reflects a narrower product definition or conservative adoption assumptions.

B. Market Capacity / Volume – Conflicting Numbers

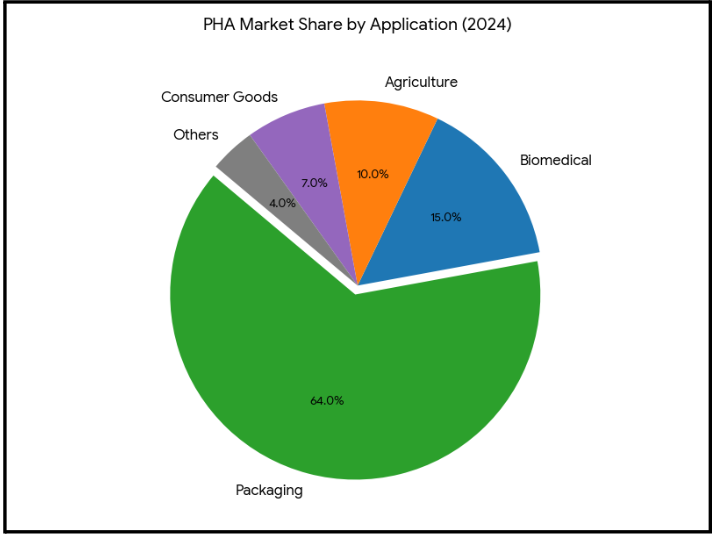

Installed capacity figures also vary:

- 70,000 tonnes in 2024

- 101,000 tonnes in 2024 (European Bioplastics estimate)

- A more conservative projection suggests global output will only surpass 50,000 tonnes by 2025

These are not necessarily contradictory. They may reflect:

- Installed capacity vs actual production

- Announced capacity vs operational plants

- Differences in reporting cut-off dates

The higher figure (101,000 tonnes) likely includes announced and partially commissioned facilities, while lower figures may refer to confirmed operational output.

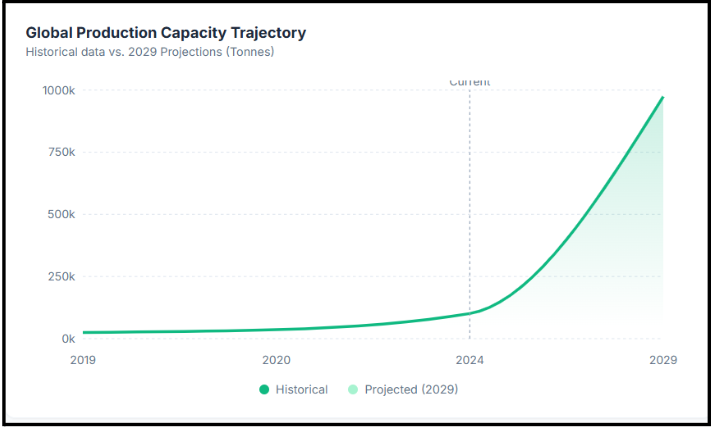

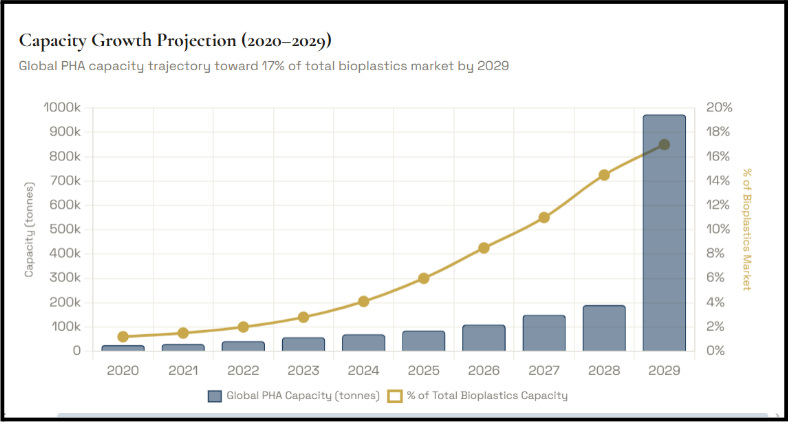

Future projections show much larger numbers:

- 974,000 tonnes by 2029

- Representing 17% of total bioplastics capacity

This projection assumes aggressive industrial scaling and successful cost reduction.

C. CAGR Projections – Why They Differ

PHA CAGR estimates range widely:

- 14.2% (2020–2025)

- 14.7% (2023–2030)

- 9.4% (2024–2030)

- 29.4% (2026–2034)

The variation comes from:

- Different starting years

- Different baseline market sizes

- Conservative vs optimistic scaling assumptions

- Inclusion or exclusion of certain applications

A high CAGR (such as 29.4%) often reflects a small starting base. Even modest volume increases can produce a large percentage growth rate.

Our Approach in This Report

Given these variations, we have taken a deliberate approach.

- Where credible estimates differ, we show the range rather than force a single number.

- Where installed capacity appears significantly higher than confirmed output, we lean toward the more conservative, operationally verified figure.

- We do not assume that all announced plants will run at full capacity on schedule.

We distinguish clearly between:

- Installed capacity

- Actual production

- Market value

- Forecast scenarios

For modelling and comparative analysis, we use mid-range, realistic estimates.

These reflect:

- Confirmed operational capacity

- Documented policy drivers

- Observable commercial adoption

Note on Country-Level Data Interpretation

In several countries, dedicated and reliable data specific to PHA (Polyhydroxyalkanoates) is not publicly available.

In such cases, reporting bodies often publish figures only for total bioplastics (which may include PLA, PBAT, starch blends, bio-PE, and other materials).

Where country-level PHA-specific data was unavailable, we have:

- Referenced the broader bioplastics market size or capacity

- Examined the country’s known positioning in biodegradable or fermentation-based polymers

- Applied proportional or directional estimates cautiously

- Clearly distinguished between confirmed PHA data and inferred positioning

3. PHA: Core Concepts & Market Relevance

3.1 What Is PHA?

At its core, Polyhydroxyalkanoate (PHA) is not a single material, but a vast family of naturally occurring biopolyesters.

While we think of plastic as a synthetic invention of the 20th century, PHA has been produced by nature for billions of years. It is synthesized by over 90 genera of bacteria, archaea, and even certain microalgae.

Of course, these microorganisms don’t “make plastic” for human use. They create PHA as a survival mechanism.

When a microbe finds itself in an environment with plenty of carbon (its food) but not enough of other essential nutrients like nitrogen or phosphorus, it stores that excess energy internally.

It converts the carbon into hydrophobic granules (tiny, insoluble droplets tucked inside the cell membrane).

When the “lean times” come and food is scarce, the bacteria consume these granules to survive. Because this material is designed by nature to be eaten by the very organisms that create it, it possesses a characteristic that sets it apart from almost every other plastic: biodegradability.

3.1.1 Chemical Structure of PHA

To understand how PHA performs in a factory or a kitchen, we have to look at its chemical structure.

PHAs are composed of (R)-hydroxy fatty acid monomers that are linked together by ester bonds (chemical bonds that allow for the eventual breakdown of the polymer).

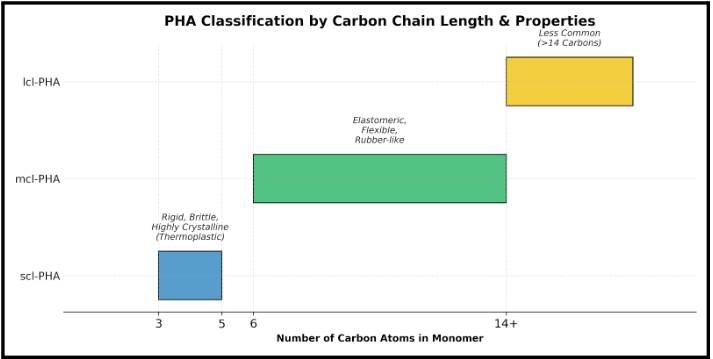

The industry classifies PHAs based on the number of carbon atoms in their monomeric building blocks. The carbon count determines whether the final plastic is stiff (for instance, as a soda bottle) or stretchy (for instance, as a rubber band).

| PHA Category | Carbon Atoms | Physical Properties | Common Examples |

|---|---|---|---|

| scl-PHA | 3–5 | Stiff, brittle, high melting point | PHB, PHBV |

| mcl-PHA | 6–14 | Elastomeric, flexible, low melting point | PHHx, PHO |

| lcl-PHA | >14 | Wax-like, specialized | Specialized copolymers |

3.1.2 How PHA is Produced

Bacteria like Cupriavidus necator are the workhorses of PHA production. However, to make PHA industrially means we need to scale these biological processes.

The Feedstock Evolution

The biggest cost in PHA production is the feed for the bacteria. Traditionally, this meant high-quality sugars like glucose or sucrose.

So, to make PHA a truly sustainable competitor to oil-based plastics, the industry is shifting toward circular feedstocks:

3.1.3 The Cost Reality

Currently, PHA is a lot more expensive than fossil-fuel plastics (sometimes up to 15 times higher). This price gap is driven by the energy required for downstream processing (breaking the bacteria open to get the plastic out) and the cost of the feedstock.

However, as the scale of production increases and we move toward waste-based feeds, these costs will decline.

3.1.4 The Superpowers of PHA

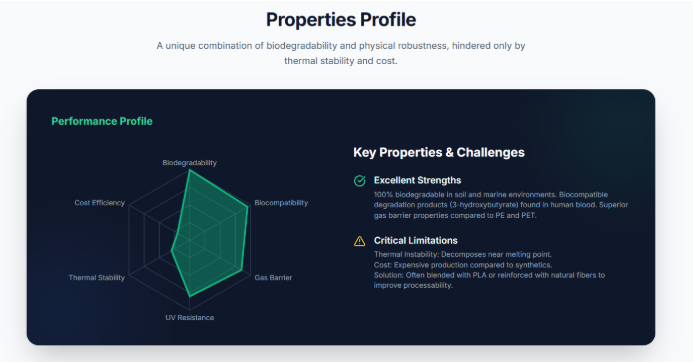

PHA offers a combination of properties that no other material can match.

True Biodegradability: Unlike degradable plastics that just break into microplastics, PHA is consumed by microbes. It disappears completely in soil, freshwater, and most importantly marine environments. If a PHA straw ends up in the ocean, it becomes fish food.

Biocompatibility: PHA is non-toxic to living tissue. In fact, when it breaks down in the human body, it produces 3-hydroxybutyrate, a substance naturally found in our blood.

High Barrier Performance: PHA is remarkably good at blocking gases. In many cases, it performs better than PE (Polyethylene) or PET (the plastic used in water bottles) at keeping oxygen out (which is vital for food shelf-life).

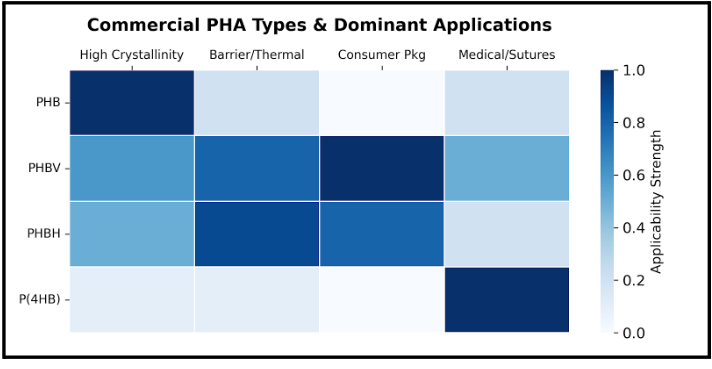

3.1.5 The Market Leaders (The Copolymers)

While pure PHB was the first PHA discovered, it is difficult to process because its melting point is very close to the temperature where it starts to burn. To fix this, the industry uses copolymers (means essentially mixing different types of PHA at a molecular level):

PHBV: Tougher and more flexible than pure PHB. Great for consumer goods.

PHBH: Offers superior heat resistance and is a strong candidate for replacing PET in bottles.

P(4HB): The gold standard for medical applications due to its high strength and slow, predictable breakdown in the body.

3.1.6 The Challenges of PHA Adoption

We believe in a grounded approach to bioplastics. PHA is not a magic bullet yet.

Aside from cost, its thermal processing window is a hurdle.

Because PHA is a biological product, it doesn’t like high heat. So if a factory worker leaves the machine running too hot for too long, the PHA can degrade inside the equipment.

To solve this, we see PHA blended with other materials or reinforced with natural fibers like wood or bamboo.

These blends make the material easier to work with while maintaining its eco-friendly credentials.

In the next section, we will break down the specific differences between PHA and other common biopolymers to see where each one wins the race for sustainability.

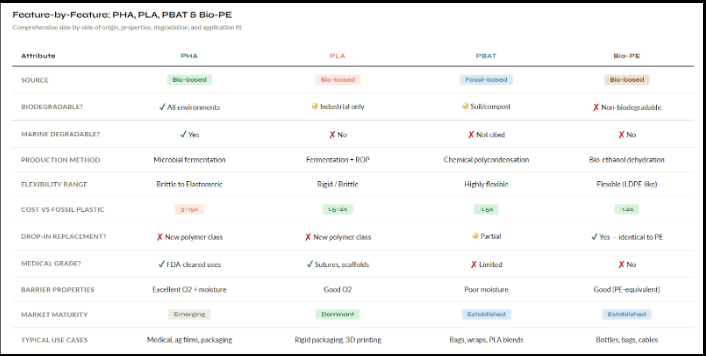

3.2 How PHA Differs from PLA, PBAT, and Bio-PE

The bioplastics market today is pillared on four leading materials: PHA, PLA, PBAT, and Bio-PE. Each of these materials has unique origins, chemistries, end-of-life outcomes, and market applications.

So it is essential to understand these differences to make informed choices for manufacturing, policy, and sustainability investments.

This section presents a clear, side-by-side comparison.

3.2.1 PHA vs. PLA (Polylactic Acid)

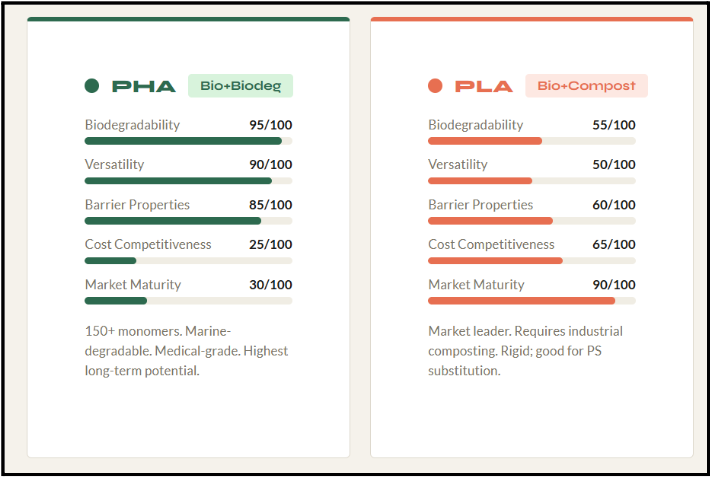

Polylactic Acid (PLA) is currently the most widely produced and commercially adopted bioplastic globally.

Origin and Feedstock:

PLA is bio-based, produced from renewable agricultural feedstocks such as corn starch, sugarcane, cassava, and sugar beets.

The raw material for PLA is fermented to produce lactic acid, which is then polymerised to form PLA.

Physical and Mechanical Properties:

PLA is known for its:

High rigidity

Transparency and gloss

Mechanical properties similar to polystyrene (PS) and, to some extent, polypropylene (PP)

However, PLA is naturally brittle, with a glass transition temperature between 45–60°C, and a relatively low heat resistance.

It is commonly used for:

Rigid packaging

Bottles

Thermoformed trays

3D printing filaments

Biodegradability and End-of-Life:

PLA is certified as compostable, but requires industrial composting conditions (specifically, temperatures above 58°C and regulated humidity) for effective breakdown. It does not readily degrade in soil, home compost, or marine environments. This can create confusion in end-of-life sorting and disposal.

Market Position and Cost:

PLA is the market leader in bioplastics due to its cost advantage, established manufacturing scale, and supply chain maturity.

In contrast, PHA, while also bio-based, is typically more expensive to produce(up to 15 times the cost of fossil plastics) because of complex fermentation and extraction processes.

| Feature | PHA | PLA |

|---|---|---|

| Source | Microbial fermentation | Fermentation, then polymerisation |

| Feedstock | Sugars, oils, wastes | Sugars (corn, cane, etc.) |

| Physical Form | Rigid (scl) to flexible (mcl) | Rigid, brittle |

| Heat Resistance | Moderate | Low |

| Compostability | Soil, marine, compost | Industrial compost only |

| Main Uses | Medical, packaging, agriculture | Rigid packaging, 3D printing |

| Cost | High | Moderate/low |

Key Distinctions:

PHA is structurally diverse (can be either rigid or elastomeric), while PLA is mainly rigid.

PHA biodegrades in a wide range of environments (soil, freshwater, marine, compost), while PLA requires industrial composting.

PLA dominates the market due to cost, but PHA is increasing its footprint in applications demanding true biodegradability.

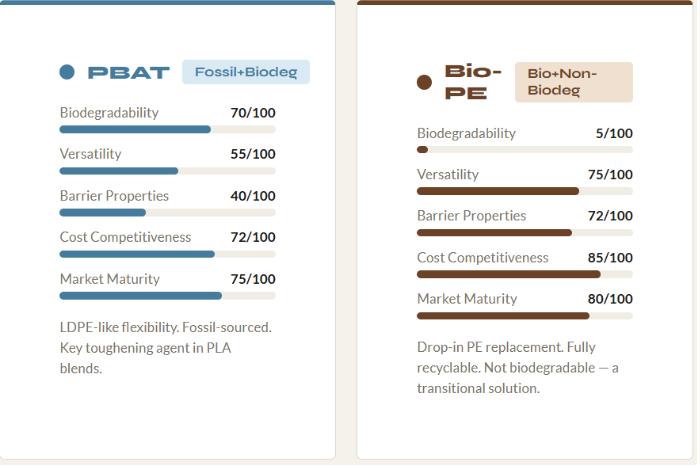

3.2.2 PHA vs. PBAT (Polybutylene Adipate Terephthalate)

Polybutylene Adipate Terephthalate (PBAT) is a fossil-based, biodegradable polyester commonly used as a flexible packaging material.

Origin and Feedstock:

PHA: Bio-based, synthesised by bacteria using renewable feedstocks.

PBAT: Synthesised from petroleum-derived monomers (1,4-butanediol, adipic acid, terephthalic acid) using standard polycondensation chemistry.

Physical and Mechanical Properties:

PHA: Highly tunable; short-chain-length types (e.g., PHB) are stiff and brittle, while medium-chain-length types are flexible, like rubber. Generally excellent oxygen and water barrier properties.

PBAT: Highly flexible and tough, with mechanical behaviour similar to low-density polyethylene (LDPE). PBAT offers good processability for films and bags but has higher water-vapour permeability and lower heat resistance than most PHAs.

Biodegradation:

PHA: Fully biodegradable in industrial compost, soil, freshwater, and marine environments. Degradation is both aerobic and anaerobic.

PBAT: Fully biodegradable in soil and industrial composting, but marine degradability is limited and not well documented.

Market Applications:

PHA: Medicine, specialty packaging (films, bottles), agriculture (mulch films).

PBAT: Rubbish bags, cling wraps, organic waste bags, disposable tableware, and as a toughening agent in PLA blends.

Comparative Table: PHA vs PBAT

| Feature | PHA | PBAT |

|---|---|---|

| Origin | Bio-based | Fossil-based |

| Synthesis | Microbial fermentation | Chemical polycondensation |

| Flexibility | Brittle to elastomeric | Highly flexible (LDPE-like) |

| Barrier | Excellent oxygen/water barrier | High water-vapour permeability |

| Degradation | Soil, marine, compost | Soil, compost |

| Uses | Medical, packaging, agriculture | Bags, wraps, blends |

Key Distinctions:

3.3.3 PHA vs. Bio-PE (Bio-polyethylene)

Bio-PE is a drop-in bioplastic—chemically identical to conventional polyethylene, but produced from renewable bio-ethanol instead of petroleum.

Origin and Feedstock:

Chemical Structure and Properties:

Biodegradability and End-of-Life:

Market Applications:

Comparative Table: PHA vs Bio-PE

| Feature | PHA | Bio-PE |

|---|---|---|

| Classification | Bio-based & biodegradable | Bio-based & non-biodegradable |

| Chemical Nature | Aliphatic polyester | Polyolefin (polyethylene) |

| Source | Microbial fermentation | Bio-ethanol from crops |

| Drop-in Solution | No (new class) | Yes (identical to fossil PE) |

| Environmental Fate | Sinks, degrades in water/soil | Persists, recycles like PE |

| Disposal | Composting, digestion | Mechanical recycling |

Key Distinctions:

| Attribute | PHA | PLA | PBAT | Bio-PE |

|---|---|---|---|---|

| Source | Bio-based (fermentation) | Bio-based (fermentation) | Fossil-based | Bio-based (bio-ethanol) |

| Biodegradability | Yes (soil, marine, compost) | Only industrial compost | Soil, compost | No |

| Key Properties | Rigid to flexible, barrier | Rigid, clear, brittle | Highly flexible | Durable, robust |

| End-of-Life | Compost, marine, soil | Industrial compost | Compost, soil | Mechanical recycling |

| Main Uses | Med, packaging, agri | Rigid packs, 3D print | Bags, wraps, blends | Bottles, bags, durable |

As regulatory and consumer demands change, these distinctions will play an increasingly significant role in the adoption of next-generation bioplastics.

3.3 Types of PHA

To understand the commercial potential of Polyhydroxyalkanoates (PHAs), we must first correct a common misconception: PHA is not a single material. It is a massive family of materials.

To date, scientists have discovered approximately 150 different monomers that can be combined to form PHA.

By mixing different monomers, manufacturers can create materials with a vast spectrum of characteristics, ranging from rigid, stiff plastics to flexible, rubber-like elastomers.

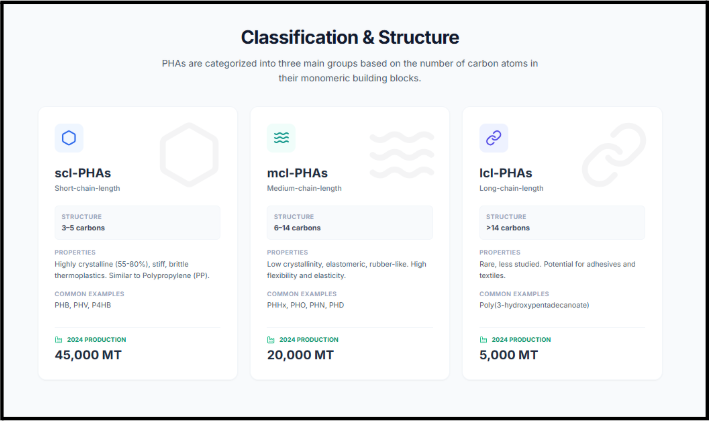

The industry classifies PHAs into three primary groups based on the number of carbon atoms in their monomeric building blocks: Short-Chain, Medium-Chain, and Long-Chain.

3.3.1 Short-Chain-Length PHAs (scl-PHAs)

The most mature segment of the market belongs to Short-Chain-Length PHAs. These are composed of monomers containing 3 to 5 carbon atoms.

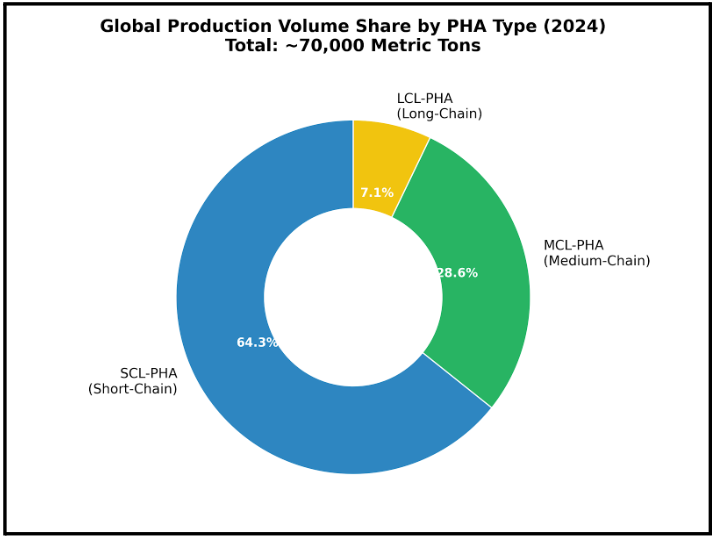

Scl-PHAs currently dominate the global production landscape.

In 2024, they accounted for approximately 45,000 metric tons of global production volume. Their dominance is due to their physical properties, which mimic some of the world’s most widely used fossil-based plastics.

Properties and Performance

Scl-PHAs are characterized by high crystallinity which ranges between 55% and 80%. In polymer science, high crystallinity translates to material stiffness. Consequently, these materials act as stiff, brittle thermoplastics.

If you are looking for a bioplastic replacement for Polypropylene (PP), scl-PHAs are the closest biological equivalent.

However, their stiffness is a limitation and leads to brittleness in certain applications unless modified.

Common Examples of scl-PHAs include:

Poly(3-hydroxybutyrate) (PHB): This is the most common and extensively studied homopolymer (a polymer made of identical monomer units). It is rigid and strong, and has a high melting temperature of approximately 175–180°C. This is technically impressive. However. pure PHB has a very narrow processing window, which means it is difficult to mold without degrading the material.

Poly(4-hydroxybutyrate) (P4HB): This ia specialized variant popular for high-value medical applications such as absorbable sutures (like TephaFLEX®). That’s because it is biologically compatible and reabsorbs into the body over time.

Poly(3-hydroxyvalerate) (PHV): Another typical short-chain variety used in copolymer blends to adjust material strength.

3.3.2 Medium-Chain-Length PHAs (mcl-PHAs)

Moving up the carbon count, we find Medium-Chain-Length PHAs, which consist of monomers with 6 to 14 carbon atoms.

While smaller in volume than short-chain types (reaching about 20,000 metric tons in global production in 2024) mcl-PHAs serve a vital role in the bioplastic ecosystem.

Properties and Performance

Structurally, these materials are the opposite of their short-chain cousins. They have lower crystallinity, which makes them act as flexible, semi-crystalline elastomers or even amorphous liquids.

If scl-PHAs are the “stiff plastic” of the family, mcl-PHAs are the “rubber.”

They possess high flexibility, elasticity, and a lower melting point with higher elongation at break. This makes them ideal for applications where the material needs to bend without snapping (examples of such applications are films, coatings, soft robotics, and specialized biomedical products).

Common Examples of mcl-PHAs include:

3.3.3 Long-Chain-Length PHAs (lcl-PHAs)

The final category is Long-Chain-Length PHAs. These contain monomer units with more than 14 carbon atoms (typically 15 to 20).

This is currently a niche market. These types are seldom produced by microbes in significant quantities, So, the global production of this type of PHA was roughly 5,000 metric tons in 2024. They are significantly less studied than SCL or MCL types.

However, their unique properties (that is, being elastic and durable) have potential uses in adhesives, textiles, and specialty high-performance goods.

3.3.4 The Power of Mixing: Copolymers and Terpolymers

The real commercial value of PHA lies in Copolymers.

A copolymer is created when two different monomers are chemically bonded in the same chain. By engineering these complex structures, manufacturers can effectively canceling out the weaknesses of one monomer with the strengths of another.

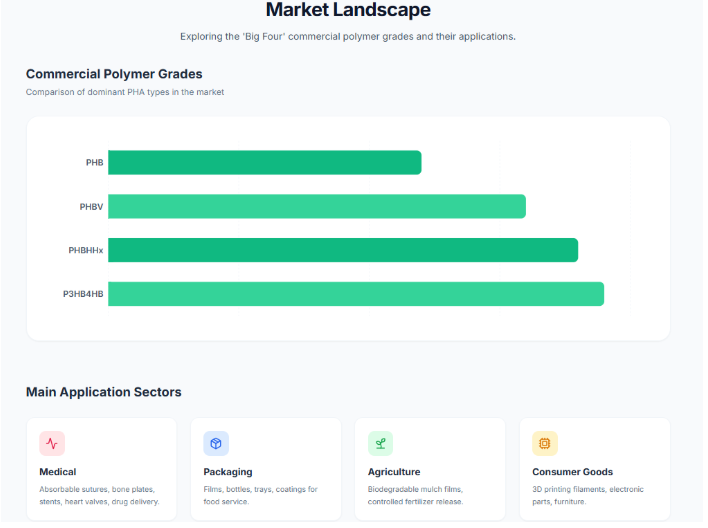

The “Big Four” Commercial Types

Based on current market activity, four specific types of PHA have emerged as the most commercialized varieties worldwide.

1. PHB (The Basic Unit)

This is the widespread stiff, brittle homopolymer. While it offers strength, its brittleness and difficulty in processing limit its standalone use. It is the base upon which better materials are built.

2. PHBV (The Tougher Alternative)

Full name: Poly(3-hydroxybutyrate-co-3-hydroxyvalerate).

This is a copolymer created by adding 3-hydroxyvalerate (HV) to the basic PHB backbone. The result is a material that is harder and stronger, yet significantly more flexible and durable than pure PHB.

Typical Application: Food containers and disposable cutlery where rigidity and impact resistance are required.

3. PHBHHx (The Flexible Solution)

Full name: Poly(3-hydroxybutyrate-co-3-hydroxyhexanoate).

This copolymer combines short-chain and medium-chain units. By introducing the hexanoate unit, the material becomes soft and flexible, improving toughness and processing capabilities.

Typical Application: Packaging films and plastic bags.

4. P3HB4HB (The Medical Grade)

Full name: Poly(3-hydroxybutyrate-co-4-hydroxybutyrate).

This is a soft, elastic copolymer. Its unique biocompatibility has made it a preferred material in the medical field.

Typical Application: Drug carriers, tissue engineering, and medical implants.

Beyond copolymers, the industry is also exploring Terpolymers, such as P(3HB-co-3HV-co-3HHx). These combine three different monomers to achieve highly specific material properties that a dual-mix cannot achieve.

Summary

The landscape of PHAs is not defined by a single material, but by the ability to tune the carbon chain length to suit the application.

From the rigid, polypropylene-like performance of scl-PHAs (perfect for a shampoo bottle) to the flexible, rubber-like nature of mcl-PHAs (perfect for a produce bag), the technology offers a spectrum of solutions.

3.4 Key Performance Properties

The commercial viability of any polymer rests on its ability to perform under stress while maintaining its structural integrity during its intended shelf life.

Polyhydroxyalkanoates (PHAs) are unique because they offer a “tunable” performance profile. Because they are a family of biopolyesters rather than a single material, their properties can be adjusted by altering the microbial strain, the feedstock, or the specific monomeric composition.

The key performance properties of PHAs are:

3.4.1 Comprehensive Biodegradability and Compostability

PHAs are currently the only class of polymers that are 100% biodegradable and exclusively synthesized by microorganisms.

Aerobic Composting (Home and Industrial):

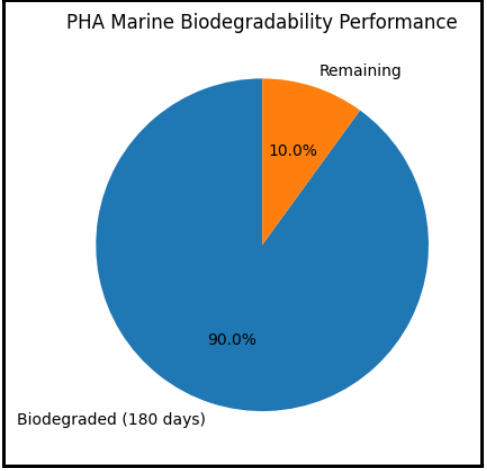

In standard composting environments, PHAs are consumed by bacteria and fungi. They convert the polymer into CO2, water, and mineral biomass. This process completes in less than four months. Unlike other bioplastics that require the aggressive heat of industrial facilities, many PHA grades are suitable for home composting.

Anaerobic Digestion (AD):

A standout feature of PHA is its ability to biodegrade in anaerobic conditions (which means environments without oxygen, such as landfill interiors or dedicated AD plants). In these settings, the degradation takes only two weeks. A strategic advantage of this pathway is that methane gas is generated in the process, which can be captured and repurposed as renewable energy.

3.4.2 Marine and Aquatic Degradation

One of the most significant environmental arguments for PHA is its “Marine-Degradable” certification. While most plastics fragment into microplastics when they enter the ocean, PHA serves as a carbon source for marine microbes.

Density and “The Sinking Effect”:

Most conventional plastics (like Polyethylene) have a lower density than water. This causes them to float on the surface and travel vast distances. PHAs possess a higher density than water. This means they sink to the bottom of aquatic ecosystems.

Ukhi explains: The “sinking” nature of PHA is a misunderstood benefit. In a circular economy, we want materials to stay within managed waste streams. However, if a leak occurs, a material that sinks and degrades in sediment is infinitely better than one that floats and enters the digestive systems of surface-feeding marine life.

Benthic Biodegradation:

By sinking into the sediment (the benthic zone), PHA enters an area rich in microbial activity. This means biodegradation can carry on even in the oxygen-poor environments of the sea floor.

Degradation Timeline:

Natural degradation in cold seawater can be a slow process taking several years. Still, it is significantly accelerated by exposure to Ultraviolet (UV) light near the surface. This dual-action (biological consumption and UV-assisted breakdown) ensures that PHA does not contribute to the permanent “Pacific Garbage Patch” phenomenon.

3.4.3 Barrier Properties

For the packaging industry, a material is only as good as its barrier performance. If it fails to block oxygen or moisture, the product it is supposed to protect, will get spoilt. PHA excels in this area and outperforms traditional fossil-fuel plastics.

Gas and Moisture Resistance

PHAs are naturally hydrophobic (water-repellent) and insoluble in water. This chemical nature means PHAs offer a superior moisture barrier compared to Polypropylene (PP). Furthermore, PHA’s oxygen barrier properties are superior to both Polyethylene (PE) and PET (the material used for soda bottles).

PHA is naturally resistant to UV radiation. This is a critical functional property for food and cosmetic packaging, as it prevents light from degrading the sensitive oils or nutrients inside the package.

Performance Enhancement (Nanofillers): For ultra-high-performance requirements, PHA can be compounded with nanofillers such as nanoclay or graphene oxide. These additives create what is known as a “tortuous pathway”. Think of it as a microscopic maze that makes it physically difficult for gas molecules to pass through the material. This extends the shelf life of the product.

| Property | PHA Performance | Comparison to Conventional Plastics |

|---|---|---|

| Oxygen Barrier | Excellent | Superior to PE and PET |

| Water Vapor Barrier | High | Better than PP |

| UV Stability | High | Superior to many untreated polyolefins |

| Water Solubility | Insoluble | Hydrophobic (water-repellent) |

3.4.4 Heat Resistance and Thermal Stability

The thermal profile of PHA determines how it can be manufactured and which “real world” temperatures it can withstand (such as being left in a hot car or holding hot coffee).

Temperature Tolerance:

PHAs generally exhibit good resistance to heat, with some forms remaining stable up to 120°C. Their melting points (Tm) typically fall between 160°C and 180°C, placing them in the same functional category as PVC and PET.

The Processing Window:

A significant hurdle for manufacturers is the narrow “thermal processing window.” For many PHAs (especially the homopolymer PHB), the temperature at which the plastic melts is dangerously close to the temperature at which it begins to thermally degrade (approximately 200°C). If the material is overheated during production, it loses its structural strength.

The Copolymer Solution:

To overcome this, manufacturers utilize copolymers like PHBV or 4-hydroxybutyrate. These additions lower the melting point, which widens the gap between “melt” and “degrade.” This broader thermomechanical range allows for easier processing on standard industrial machinery.

The combination of high barrier performance and universal biodegradability positions PHA as a premium material. However, these technical strengths must be weighed against its higher production cost.

3.5 Commercial Positioning of PHA

PHA stands out because it is both highly versatile and truly biodegradable. Unlike many “green” plastics that only break down in industrial composters, PHA will naturally biodegrade in regular soil and even in marine environments. It does this without leaving behind microplastics or toxic residues, which sets it apart from most alternatives.

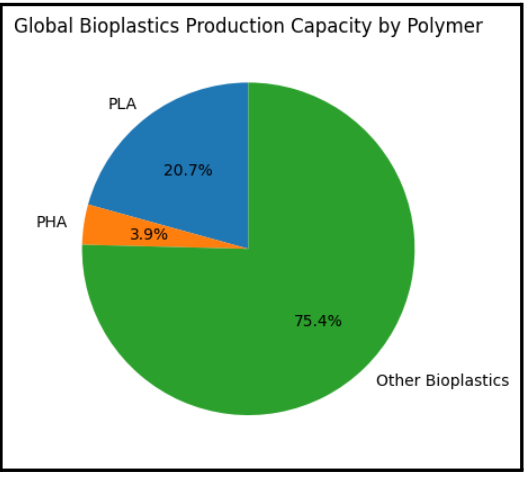

Today, PHAs make up a small part (about 3.9%)of the total bioplastics market. This is far less than more established materials like polylactic acid (PLA). But this share is expected to rise quickly. In fact, industry forecasts predict PHA production capacity will grow by 57% by 2028.

PHA is not yet a commodity, but it can soon be one.

3.5.1 Competitive Positioning vs. Fossil-Based Plastics

The ultimate goal for any bioplastic is to replace fossil-based plastics like polypropylene (PP) and low-density polyethylene (LDPE), which are found in everything from packaging to car parts.

PHA isn’t taking on these plastics everywhere at once. Instead, its entry point is in smaller, higher-value sectors where its unique strengths matter most.

While everyone looks at packaging films, research suggests that PHA’s most immediate strategic win lies in a different sector: Polyurethane (PUR) sealants and adhesives.

In these applications, the economics and environmental mathematics shift in favor of biology. PHA derived from urban biowaste can already outperform fossil-based PUR. The impact is measurable:

Environmental Impact: Four times lower than fossil PUR.

Societal Costs: Eight times lower.

This positions PHA not just as a “green alternative” but as a superior socioeconomic choice in the construction and automotive sealant markets.

Of course, the larger prize is the mass market of commodity films (LDPE) (the material used in everything from shrink wrap to grocery bags).

At the moment, high production costs mean PHA is not price-competitive for these uses.

The industry acknowledges this gap. However, the roadmap to closing this gap is clear.

The industry is positioning PHA to enter this space as biorefinery efficiencies improve, specifically, by reducing the reliance on expensive chemical extraction agents like sodium hypochlorite.

So, as these processing costs drop, PHA could move from a premium niche to a viable mass-market competitor.

3.5.2 How PHA Differs from Other Bioplastics

It’s not just fossil plastics that PHA is up against; it also needs to stand out among other bioplastics.

Most bioplastics, like PLA, need special industrial composting to break down. If a PLA item ends up in the ocean or in a ditch, it could last for decades. PHA, on the other hand, will break down in freshwater, saltwater, and soil. This is a big selling point for applications where there is a real risk of litter or environmental leakage.

Some bioplastics get soggy or fall apart when exposed to high humidity. PHA is much more stable in wet conditions. That makes it useful for packaging sensitive electronics, for example, where moisture would be a disaster.

PHA is not always a substitute; sometimes it’s an enhancer. Manufacturers sometimes blend PHA with PLA to make the resulting plastic stronger, tougher, or softer.

3.5.3 Main Market Segments for PHA

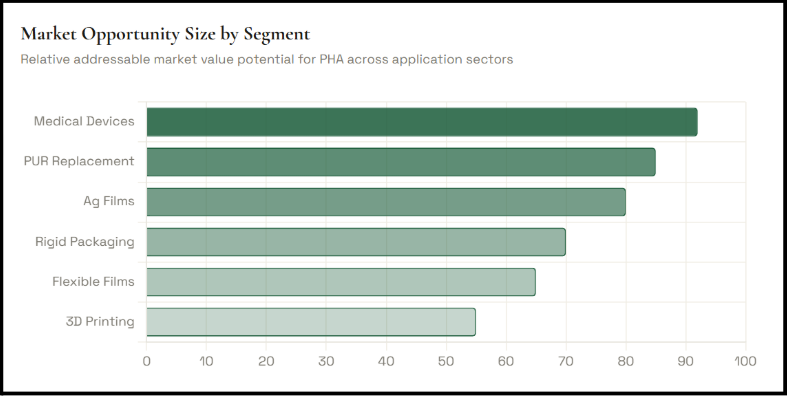

PHA’s physical properties are highly tunable, which means it can be made to be stiff and strong, or soft and flexible. That opens up different types of markets.

Packaging

This is currently the largest volume use for PHA. The application list is familiar to any consumer:

Food containers

Single-use cups

Compostable bags

Rigid packaging

Here, the “premium” positioning appeals to brands that want to make a sustainability statement beyond simple recycling.

Medical (The High-Value Niche)

This is where the high cost of PHA is less of a barrier. Due to its biocompatibility (the body accepts it without rejection), PHA is positioned for high-margin medical applications.

In this segment, the material is positioned as a life-science product.

Agriculture (The Functional Segment)

This is the most practical positioning of the material. PHA is used for mulch films and seed coatings.

The value proposition here is labor-saving. Because PHA can be left to degrade naturally in the soil, farmers eliminate the need for the retrieval and disposal of plastic films after the harvest. The plastic becomes part of the soil.

So, in this context, PHA is positioned as an operational efficiency tool as much as an environmental one.

3.5.4 Market Challenges and Restraints

Despite these strengths, there are important reasons why PHA hasn’t taken over the plastics world yet.

The number one barrier is price. PHA is much more expensive to make than regular plastics, mainly because the fermentation process is complex, the raw materials (like sugars and oils) are costly, and yields are lower.

Making PHA in the lab or in small pilot plants is one thing. Scaling up to big, efficient factories is much harder. It’s only when PHA is produced at industrial scale that costs will fall enough to take on mainstream markets.

Many buyers still don’t understand the difference between biodegradable, compostable, and bio-based plastics. This makes it harder for PHA to differentiate itself based on its real strengths.

For now, PHA mostly fits in markets where buyers are willing to pay extra for performance or for a clear sustainability benefit, such as in high-end packaging, the medical sector, or for agricultural films in places with strict environmental rules.

Summary

In summary, PHA is currently positioned as the “Gold Standard” of bioplastics. It is technically superior in its end-of-life profile and versatile in its application, but constrained by the economics of early-stage scaling.

4. Global PHA Market Size & Growth (2018–2030)

Polyhydroxyalkanoates (PHAs) are still a small part of the global plastics industry. However, they are growing quickly and attracting serious attention from investors, manufacturers, and policymakers.

As of 2024, PHAs account for roughly 1.2% to 4.1% of total global bioplastics production capacity. This is modest when compared to more established materials like PLA. But PHA is widely regarded as one of the most important long-term materials in the sector because of one key advantage: it can fully biodegrade in soil, freshwater, and marine environments.

This section outlines where the global PHA market stands today, how it has grown, and what the next five to ten years may look like.

4.1 Global Market Size and Capacity

Current Production Levels

The PHA industry has expanded steadily over the past five years.

This shows that PHA is moving beyond laboratory and pilot scale. It is now entering structured industrial production.

Market Value

Market value estimates vary widely depending on methodology and what products are included.

In 2023, reported market values ranged from USD 93.55 million to USD 650.7 million.

One 2024 estimate placed the global PHA market at USD 714.7 million.

This variation reflects the still-developing nature of the sector and differences in how analysts define the market.

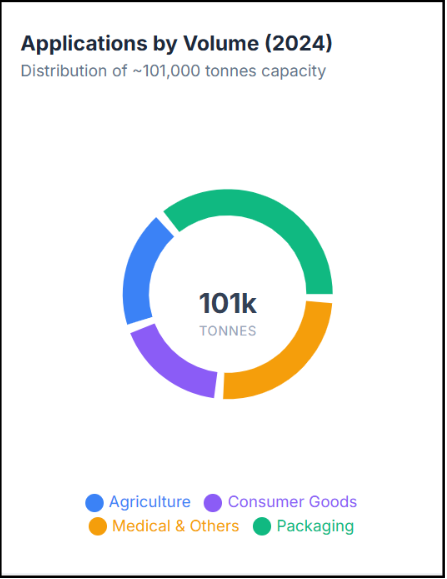

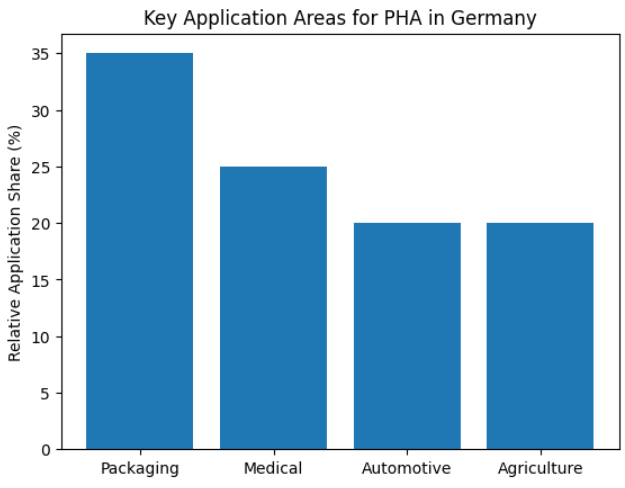

Where PHA Is Used (2024 Volume Split)

Based on available capacity data:

Packaging: ~38,000 tonnes

Agriculture: ~19,000 tonnes

Consumer goods: ~18,000 tonnes

Medical: ~5,000 tonnes

Packaging is clearly the largest segment by volume.

Growth Projections and Future Capacity

PHA is expected to grow faster than most other biopolymers over the coming years.

Capacity Expansion

Some projections suggest PHA could reach 17% of total bioplastics capacity by 2029, equivalent to roughly 974,000 tonnes.

Many sources forecast a 57% global capacity increase by 2028.

If these projections hold, PHA will move from a niche material to a major part of the bioplastics landscape.

CAGR Estimates

Reported compound annual growth rates (CAGR) vary but remain strong:

By 2030, the PHA market is projected to reach approximately USD 1.22 billion.

4.2 Regional Market Dynamics

Europe

North America

Asia-Pacific

4.3 Core Growth Drivers

Several factors are pushing PHA forward.

1. Environmental Regulation

More than 50 countries now have restrictions or bans on single-use plastics. Regulations increasingly favour certified biodegradable materials.

2. Feedstock Innovation

Producers are shifting toward lower-cost feedstocks such as urban food waste, sewage sludge, and even carbon dioxide. This reduces costs and aligns with circular economy goals.

3. High-Value Applications

Medical uses—such as absorbable sutures and implants—accounted for roughly 5,000 tonnes in 2024. These premium applications support industry profitability while scale builds elsewhere.

4. Marine and Soil Biodegradability

PHA’s ability to biodegrade in natural environments directly addresses concerns about ocean plastic and microplastic pollution.

4.4 Key Barriers

Despite strong growth, significant challenges remain.

1. Cost and Scale

In 2024, PHA was still 3–4 times more expensive than conventional plastics like polypropylene.

Only around 120 companies globally operate at commercial scale.

2. Downstream Processing

Extraction and purification steps account for 30–50% of total production costs.

Improving efficiency in this stage is critical for price reduction.

Technology Shifts

The industry is transitioning toward Next Generation Industrial Biotechnology (NGIB).

This includes:

If these technologies scale successfully, PHA could become cost-competitive with fossil plastics within the decade.

Key Takeaways

5. PHA Country-Level Market Profiles

5.1 China

China has firmly established itself as a global powerhouse in the bioplastics sector.

While the country produces a wide range of biodegradable materials like PLA and PBAT, Polyhydroxyalkanoates (PHA) occupy a special strategic position.

In China, PHA is widely regarded as the “bioplastic of the future.”

The industry here has successfully moved PHA from the laboratory to the factory floor. Manufacturers use agricultural crops (specifically corn starch) as the raw material for fermentation. This creates a strong link between China’s massive agricultural output and its industrial ambition for PHA.

However, the market presents a distinct paradox: China is a manufacturing giant with immense capacity, yet its domestic consumption of these high-value materials is not enough.

China – PHA Market at a Glance

| Metric | Status / Data Point |

|---|---|

| Share of global biodegradable plastics capacity | ~20% |

| Total plastics output (all plastics, 2022) | 128 million tonnes (32% of global output) |

| Biodegradable plastics volume | ~162,000 tonnes |

| Bioplastics market value | ~USD 1.6 billion (2024) |

| Share of global bioplastics value | ~4.8% |

| Forecast CAGR (2023–2026) | ~49% |

| Forecast CAGR (to 2030) | ~23.44% |

| Consumer sentiment | 93% seek fewer single-use plastics; 75% prioritize eco-friendly products |

| Core feedstock for PHA | Corn starch |

| R&D support allocation | >1.2 billion RMB |

| Key policy drivers | 2020 Plastic Ban; 14th Five-Year Plan (2021); Three-Year Action Plan (2023); Dual Carbon targets |

5.1.1 Current PHA Market Size and Global Share For China

When we analyze the production numbers, China’s dominance purely in terms of volume is undeniable.

The country accounts for approximately 20% of the global production capacity for biodegradable plastics.

To put the scale of the broader industry in perspective, here’s a fact: China’s total plastics output reached 128 million tonnes in 2022, which represents 32% of the global market.

Within this vast ecosystem, the biodegradable sector is scaling rapidly.

As of recent assessments:

Volume: The market volume for biodegradable plastics in China was recorded at 162,000 tons.

Value: The overall Chinese bioplastics market (aggregating PHA, PLA, and PBAT) was valued at approximately USD 1.6 billion in 2024.

Despite this manufacturing muscle, China’s capture of global value is lower than one might expect. The domestic bioplastics market represents only about 4.8% of the global market share by value. This significantly trails the United States (35%) and Europe (31%).

This indicates that while China is building the infrastructure to supply the world, its internal market for premium materials like PHA is still in the early stages of maturity compared to the West.

5.1.2 Growth Rate and Market Trajectory for PHA in China

The trajectory of the Chinese PHA market is aggressive.

Forecasts for the near future are incredibly bullish.

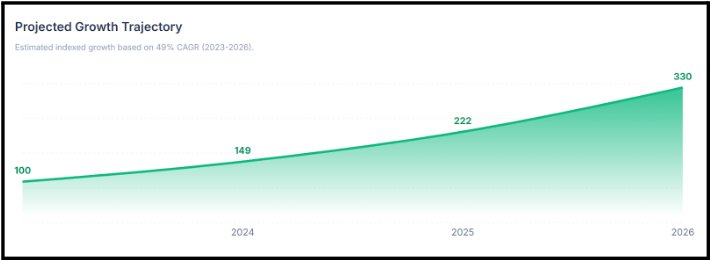

The sector is expected to grow at a Compound Annual Growth Rate (CAGR) of 49% between 2023 and 2026.

Even looking at the longer term, conservative estimates project a steady CAGR of 23.44% through 2030.

Two primary engines are driving this expansion:

The demand for flexible packaging in China’s massive logistics and delivery sector is immense.

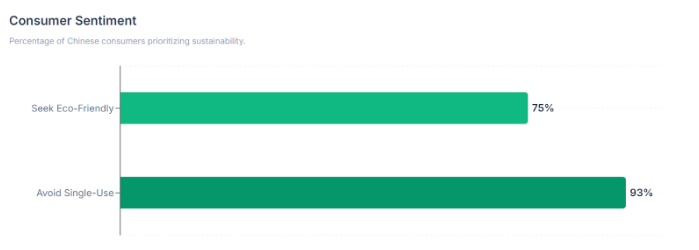

Public sentiment is turning against pollution. Recent surveys indicate that roughly 93% of Chinese consumers actively seek to buy fewer single-use plastics. Furthermore, 75% are expected to prioritize eco-friendly products in the future.

5.1.3 Market and Policy Evolution for PHA in China

The rise of PHA in China is the result of deliberate, long-term policy engineering.

While PHA was discovered globally in the 1970s, its industrialization in China began in earnest in the early 21st century. The state’s involvement has been the catalyst for this shift, anchored in the “Dual Carbon” framework, which is China’s commitment to peak carbon emissions by 2030 and achieve carbon neutrality by 2060.

Because 76% of China’s petrochemical feedstock is imported oil, developing a bio-based industry is a matter of national energy security as much as environmental protection.

The regulatory landscape has evolved through distinct phases:

2008: Early bans on ultra-thin plastic bags set the initial groundwork.

2020 Plastic Ban: This was a landmark policy phasing out non-biodegradable single-use plastics (cutlery, straws, bags) in the catering industry. Crucially, it created a specific regulatory “carve-out” that permits certified biodegradable alternatives. This effectively illegalized the competition (cheap plastic) and created a guaranteed market for materials like PHA.

14th Five-Year Plan for the Bioeconomy (2021): This elevated biotechnology to a national strategic force.

Three-Year Action Plan (2023): A roadmap aiming to make non-food bio-based products competitive with fossil-based counterparts by 2050.

To back these policies, the government has allocated over 1.2 billion RMB specifically to support bioplastics R&D.

5.1.4 Trends in Adoption and Consumer Preferences for PHA in China

Despite strong policy support, the PHA market faces a harsh reality: price.

In general, bioplastics in China are estimated to be 35% more expensive than conventional plastics. For PHA specifically, the cost premium is even higher due to the complexity of fermentation. This has left the market not fully ready for widespread adoption.

However, adoption of PHA is occurring in specific high-value niches where the costs can be justified:

The consensus is that as production scales and costs drop, the “willingness to pay” will align with the “ability to pay.”

5.1.5 Unique Trends, Real-World Examples, and Challenges for PHA in China

A unique characteristic of the Chinese PHA sector is the origin of its innovation. Unlike in the West, where innovation stems from corporate R&D, Chinese innovation is frequently driven by university spin-offs.

Key Market Players and Innovation

PhaBuilder: Founded in 2021 by Professor Chen Guoqiang of Tsinghua University, this company is a prime example of academic research scaling into commercial production.

Bluepha: A synthetic biotech firm operating a highly automated R&D lab in Shanghai. They specialize in molecular innovation to develop 100% biodegradable PHAs through fast iterations.

BBCA PHBV & Kingfa Science & Technology: These are major corporate players integrating PHA into broader biodegradable product lines.

Challenges and Risks

We must conclude the profile with a grounded look at the hurdles facing this market:

Scalability: Scaling from a lab beaker to a 10,000-liter tank without losing yield remains a difficult engineering challenge.

Feedstock Competition: Manufacturing currently relies heavily on agricultural crops (corn starch). This creates a tension between industrial growth and food security

The Innovation Gap: Although China is a volume leader, it still trails in intellectual property. The U.S. holds 36% of global bioplastic patents, compared to China’s 19.5%.

Lack of Standards: While bans on fossil plastics exist, there is a lack of specific regulations designed to create a dedicated market for biobased polymers. This makes it difficult for premium PHA to compete against cheaper, “technically biodegradable” alternatives like PLA that do not offer the same environmental benefits.

5.2 India

India is building its bioplastics industry on something it already has in abundance: agricultural by-products.

Materials such as sugarcane molasses and bagasse are being converted into higher-value polymers through fermentation. This approach supports a “waste-to-value” model. It addresses two challenges at once:

By linking agriculture, biotechnology, and manufacturing, India is shaping a bioplastics ecosystem that is both industrial and regenerative.

India – PHA Market at a Glance

| Metric | Status / Data Point |

|---|---|

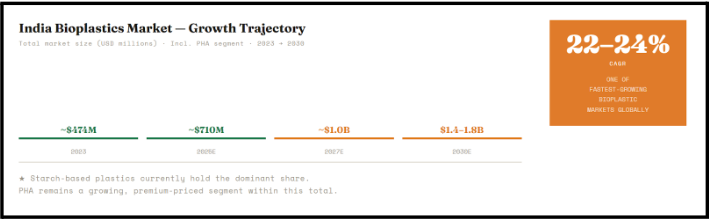

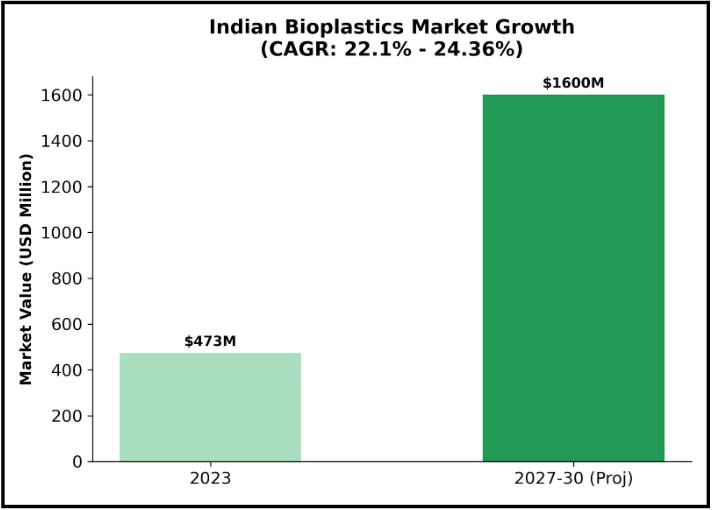

| Bioplastics market value (2023) | ~USD 447–500 million |

| Projected market value (2030) | ~USD 1.4–1.8 billion |

| Growth rate (CAGR) | 22.1%–24.4% |

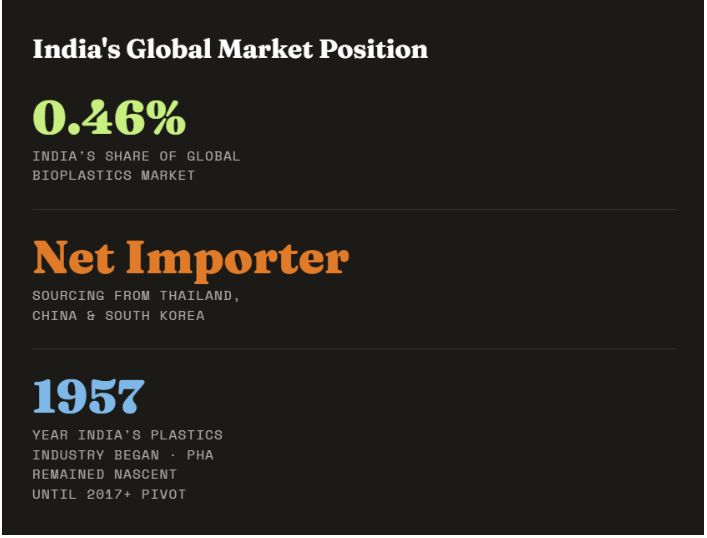

| Global market share | ~0.46% of global bioplastics industry |

| Import dependency | Historically high (Thailand, China, South Korea) |

| Key feedstocks | Sugarcane molasses, bagasse, agri side-streams |

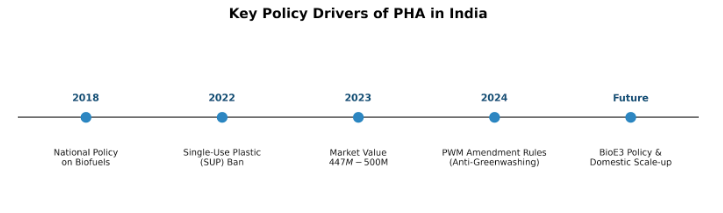

| Major policy drivers | 2022 SUP Ban; BioE3 Policy; PWM Rules 2024 |

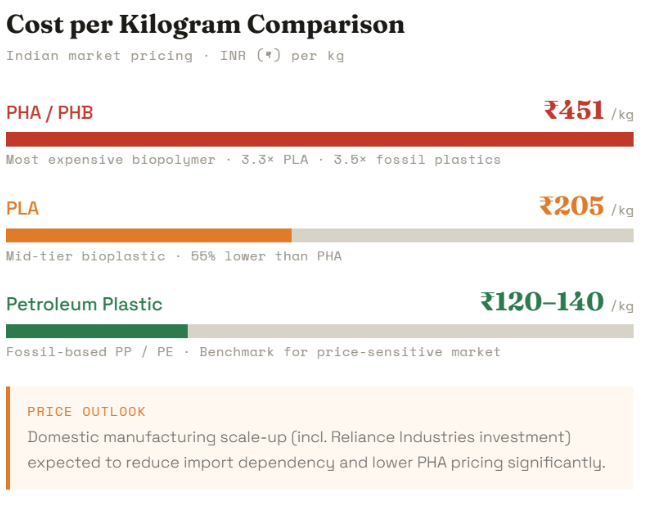

| PHA price vs alternatives | PHA: ~₹451/kg; PLA: ~₹205/kg; Fossil plastics: ~₹130/kg |

| Core application segments | Packaging, agriculture (mulch films), medical |

| Primary challenges | High cost; narrow processing window; scale-up complexity |

In India, Polyhydroxyalkanoates (PHA), and particularly the type known as Polyhydroxybutyrate (PHB), are moving from research to commercial value chains.

PHAs are produced through microbial fermentation of renewable biomass.

While lower-cost starch blends currently dominate India’s biodegradable plastics market, PHA is finding its role in applications where biodegradability must be reliable.

5.2.1 Current PHA Market Size and Global Share For India

However, this dynamic is changing.

New domestic manufacturing capacity is coming online. As India scales local production of PLA and PBAT, it strengthens the broader infrastructure needed for PHA fermentation as well.

5.2.2 Growth Rate and Market Trajectory for PHA in India

India’s projected growth rate for the PHA market (above 22% CAGR) is among the highest globally.

For PHA specifically, growth is tied to:

5.2.3 Market and Policy Evolution for PHA in India

Policy has played a decisive role in accelerating India’s biodegradable plastics sector.

1. The 2022 Single-Use Plastic (SUP) Ban

The nationwide ban on 21 low-utility plastic categories created immediate demand for alternatives. This policy created a real market opportunity for certified biodegradable materials.

2. BioE3 Policy

The Biotechnology for Economy, Environment and Employment (BioE3) policy identifies biopolymers as a strategic sector. It promotes the development of bio-manufacturing hubs to support industrial-scale fermentation.

3. Plastic Waste Management (Amendment) Rules, 2024

These rules tightened the definition of “biodegradable plastic.”

This regulatory shift benefits materials like PHA, which are naturally biodegradable across soil and water environments.

5.2.4 Trends in Adoption and Market Preference for PHA in India

Adoption in India are chosen where PHA provides functional value.

Packaging

PHA is being used in food containers and liquid-contact packaging because of its high hydrolysis resistance. This means it does not break down prematurely when exposed to moisture.

Agriculture

Farmers are beginning to adopt PHA mulch films and seedling trays. These can be ploughed back into the soil after use. This eliminates the labour and cost of collecting conventional plastic films from fields. This benefit is operational as much as environmental.

Medical

PHA’s biocompatibility makes it suitable for absorbable sutures and drug delivery systems. In this segment, performance outweighs price sensitivity.

Consumer Sentiment

Surveys indicate that approximately 93% of Indian consumers want to reduce single-use plastic consumption. This consumer preference pushes brands to consider certified biodegradable options.

5.2.5 Unique Trends, Real-World Examples, and Challenges for PHA in India

India’s strength in PHA lies in feedstock diversity and research depth.

Waste-Based Feedstocks

Indian research institutions are exploring non-traditional carbon sources, including:

This reduces reliance on food-grade sugars and improves long-term feedstock security.

Institutional Research

Challenges

Despite strong momentum, there are real barriers.

1. Price

PHA remains the most expensive commonly discussed biopolymer in India.

This cost gap limits PHA primarily to applications where environmental performance or functional benefit justifies the premium.

2. Processing Complexity

PHA has a narrow processing window. It melts at around 175°C but begins degrading near 185°C.

This requires precise temperature control and skilled manufacturing practices. Without technical discipline, yield losses increase.

Ukhi Perspective

From Ukhi’s standpoint, India’s long-term advantage lies in feedstock security and decentralised agricultural inputs.

Unlike countries dependent on imported biomass, India has large volumes of sugar residues and agricultural side-streams available domestically. This reduces supply chain risk.

For industrial players—including companies like Ukhi working at the intersection of material science and agricultural value chains—the opportunity is not limited to replacing plastic.

It is about building a domestic bio-materials ecosystem.

5.3 Thailand

Thailand has built a strong position in the global bioplastics industry. Polyhydroxyalkanoates (PHA) are seen as a key material for the country’s long-term strategy.

Thailand’s national development framework(the Bio-Circular-Green (BCG) Economy Model) treats biological resources as a strategic asset.

The country’s large agricultural base, particularly sugarcane and cassava, provides the raw materials needed for fermentation-based plastics.

This combination of policy direction and feedstock availability has created a foundation for growth.

| Metric | Status / Data Point |

|---|---|

| Total bioplastics capacity | ~95,000 tons/year |

| PHA share of global bioplastics | ~3.9% (2022) |

| Export share | ~90% of production exported |

| Export growth (2017–2022) | 25% CAGR (value); 23% CAGR (volume) |

| Capacity expansion plans | +75,000 tons/year planned |

| National target | Bio Hub of ASEAN by 2027 |

| Fiscal incentives | 125% tax deduction; up to 8-year BOI tax exemption |

| Main feedstocks | Sugarcane, cassava, palm oil mill effluent (POME) |

| PHA resin price | ~US$7/kg |

| Core challenges | High energy intensity; limited composting infrastructure; feedstock volatility; agricultural impacts |

5.3.1 Current PHA Market Size and Global Share For Thailand

- Thailand is currently the second-largest producer of bioplastics in Asia.

- Total bioplastics production capacity is approximately 95,000 tons per year.

This export orientation is significant. In fact, Thailand’s bioplastics industry has grown largely by serving international demand rather than domestic consumption.

For PHA specifically, Thailand is positioning itself not as a niche experimental producer, but as an industrial supplier.

5.3.2 Growth Rate and Market Trajectory for PHA in Thailand

Thailand’s bioplastics industry has grown steadily over the past decade, driven by both policy and global demand.

Between 2017 and 2022:

The government has set a clear goal: to become the Bio Hub of ASEAN by 2027.

PHA is expected to benefit from this push. Among bio-based resins, PHA is projected to experience one of the fastest increases in demand globally.

To support future growth:

These developments suggest that Thailand’s approach is capacity-driven and export-focused.

5.3.3 Market and Policy Evolution for PHA in Thailand

Thailand’s focus on bioplastics began formally in 2008 with the National Roadmap for the Development of the Bioplastics Industry. This roadmap allocated $60 million to establish early infrastructure and position Thailand as a regional leader.

Since then, policy support has remained consistent.

Bio-Circular-Green (BCG) Economy Model

The BCG model treats biological resources as economic drivers. Bioplastics, including PHA, are identified as priority sectors. The objective is to convert agricultural output into higher-value materials rather than exporting raw crops.

Fiscal Incentives

The government offers strong financial incentives to encourage production and adoption:

Waste Policy and Standards

Thailand’s Plastics Waste Management Roadmap (2018–2030) includes bans on single-use plastics and polystyrene foam. This creates demand for alternatives.

In 2024, the Thai Industrial Standards Institute (TISI) adopted ISO 22526-4, an international standard for life cycle assessment (LCA) of biobased plastics. This improves transparency around environmental impact and reduces greenwashing risks.

5.3.4 Trends in Adoption and Consumer Preferences for PHA in Thailand

Most PHA produced in Thailand is used to meet export demand, especially in regions with strict environmental regulations.

However, domestic adoption is gradually increasing.

Pricing remains a constraint.

Consumer surveys indicate:

5.3.5 Unique Trends, Real-World Examples, and Challenges for PHA in Thailand

Feedstock Advantage

Thailand’s agricultural base is central to its PHA strategy.

Key feedstocks include:

Glucose derived from sugarcane is particularly efficient because it requires minimal additional processing before fermentation. This reduces both cost and energy use.

Research has shown that converting cassava into bioplastics can increase its economic value by up to ten times. This creates direct rural economic impact.

Microbial Research

Thai scientists have identified effective PHA-producing bacterial strains, including:

A mutant strain of Bacillus licheniformis has shown strong yields when using POME as a substrate.

This demonstrates a practical approach: using industrial waste streams as carbon sources.

Industrial Partnerships

The partnership between RWDC Industries and Lummus Technology represents a move toward scaling PHA production at commercial levels.

Meanwhile, companies such as Total Energies Corbion (PLA) and PTT MCC Biochem (PBS) operate alongside newer entrants focusing on PHA.

Thailand’s ecosystem includes both established players and emerging fermentation specialists.

Biofuel Exploration

Beyond plastics, Thai researchers are exploring PHA derivatives such as 3HBME and 3HAME as gasoline additives. Early testing suggests performance similar to ethanol, with lower corrosiveness.

While still in development, this reflects the broader versatility of PHA chemistry.

Environmental and Infrastructure Challenges

Despite strong policy support, there are material challenges.

Energy and Emissions

Current PHA production in Thailand can result in higher cradle-to-gate greenhouse gas emissions than petrochemical plastics and even PLA. This is largely due to energy-intensive conversion processes.

Agricultural Impact

Large-scale cultivation of sugarcane and cassava carries environmental risks:

These trade-offs must be managed carefully.

Waste Management Infrastructure

Thailand lacks widespread industrial composting infrastructure.

If biodegradable plastics enter landfills, they may decompose anaerobically and release methane, which has a higher warming impact than CO₂.

Additionally:

Climate Risk

Feedstock crops are weather-dependent. Events such as droughts and El Niño can disrupt supply and increase raw material prices.

Conclusion

Thailand has built one of Asia’s most structured and policy-supported bioplastics industries. Its strategy combines:

At the same time, the country faces real environmental and infrastructure constraints. Energy use, agricultural impacts, and composting gaps must be addressed for PHA to scale sustainably.

5.4 USA

In the U.S., PHAs are valued as a biological technology.

Unlike conventional plastics, which are produced through petrochemical refining, PHAs are made through controlled fermentation processes using microorganisms.

The American market is currently defined by how these bacteria are fed, with the industry moving through three distinct “generations” of feedstock:

The market for bioplastics (and PHA) is characterized by high costs and a complex regulatory fight between federal and state-governments.

USA – PHA Market at a Glance

| Metric | Status / Data Point |

|---|---|

| North America share of global bioplastics capacity | ~19% (≈420,000 tonnes) |

| Share of bio-based resins in total U.S. plastics production | ~0.71% |

| U.S. bioplastics industry revenue | ~$96.75 million (2025 estimate) |

| Global PHA output benchmark | Expected to surpass 50,000 tonnes by 2025 (though reputed market research suggests the actual number may be much smaller) |

| Investment inflow | $500+ million (venture capital + government funding) |

| Projected CAGR (range) | 6.53% (conservative) to 15.3% (optimistic) |

| Projected market value | ~$167–171 million by 2027–2034 (varies by estimate) |

| Dominant application segment | Packaging (~64% of film revenues) |

| Fastest-growing segment | Biomedical and healthcare |

| Core challenges | High cost; fragmented regulation; composting infrastructure gaps; processing complexity |

5.4.1 Current PHA Market Size and Global Share For USA

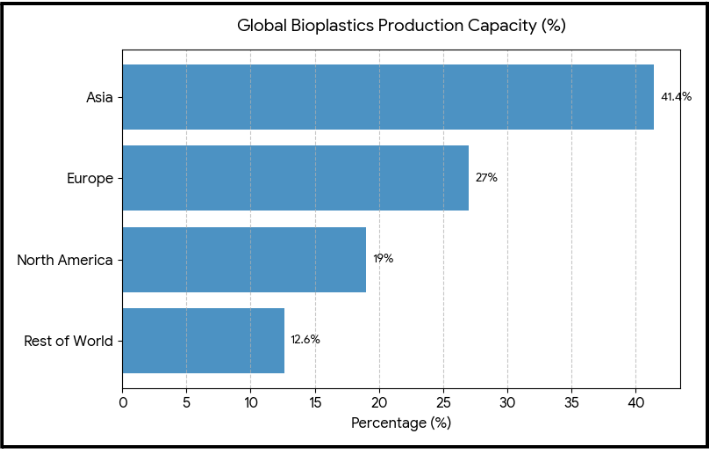

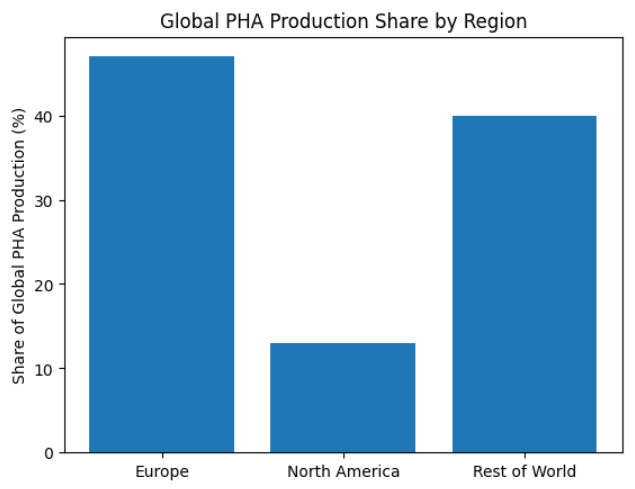

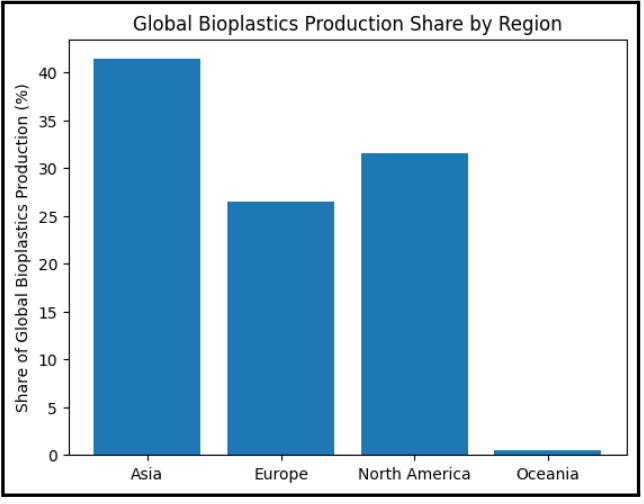

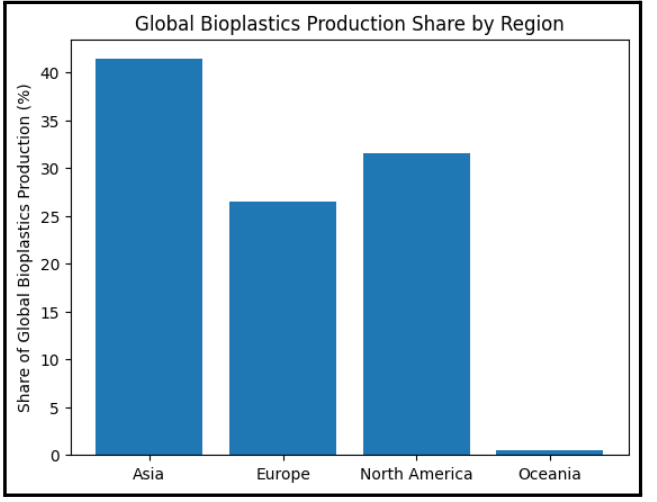

North America currently accounts for approximately 19% of total global production (about 420,000 tonnes), trailing Asia (41.4%) and Europe (~27%).

However, when we zoom in on bio-based resins specifically within the massive U.S. plastics sector, the share is minute.

Bio-based resin production represents an estimated 0.71% of overall U.S. plastic resin production.

Financially, the broader U.S. bioplastics manufacturing industry revenue was estimated at 96.75 million in 2025.

5.4.2 Growth Rate and Market Trajectory for PHA in USA

Despite the small current footprint, the trajectory of growth for PHA is aggressive. The U.S. market is capitalizing on a surge of investment, in the backdrop of the global PHA output being expected to have surpassed 50,000 tonnes by 2025 (expected to surpass 50,000 tonnes by 2025 (though reputed market research suggests the actual number may be much smaller).

This expansion is supported by over $500 million in venture capital and government funding flowing into the sector.

Growth projections vary, but all point upward:

The growth is not uniform across all sectors.

While packaging remains the dominant revenue stream (accounting for over 64% of film revenues), the biomedical and healthcare sectors are the fastest-growing.

Here, the high cost of PHA is less of a barrier compared to its value in tissue engineering and drug delivery.

5.4.3 Market and Policy Evolution for PHA in USA

In the U.S., PHA was first documented in 1925, and initial commercialization attempts in the 1970s and 90s were largely halted by economic factors. The last decade has seen a revival, driven largely by a shift in federal policy.

The “Whole-of-Government” Push

The current landscape is shaped by Executive Order 14081, signed in 2022. This ambitious order set a national goal to replace 90% of conventional plastics with bio-based alternatives within 20 years.

Ukhi explains:

The Executive Order 14081 has now been rescinded under the current administration:

This means EO 14081 is no longer in effect and its directives are no longer driving federal bioeconomy policy.

To support this, the USDA BioPreferred Program mandates that federal agencies give procurement preference to bio-based products. This creates a secure, guaranteed market for manufacturers, lowering the risk of scaling up.

The State-Level Complication

However, manufacturers face a fragmented landscape at the state level.

5.4.4 Trends in Adoption and Consumer Preferences for PHA in USA

In the U.S., adoption is driven by corporate sustainability targets and a specific consumer preference for home composting.

The Price Reality

We must be transparent about the cost barrier. PHAs in the U.S. are currently 5 to 10 times more expensive than petroleum-based plastics.

While consumers say they want sustainable options, the “green premium” they are willing to pay has a limit. Acceptance drops drastically when the cost increase exceeds 20%.

The Home Composting Shift

Interestingly, there is a growing preference for PHA over other bioplastics like PLA (Polylactic Acid) because many PHAs are home-compostable. This is a crucial distinction in the U.S., where access to industrial composting facilities is limited.

5.4.5 Unique Trends, Real-World Examples, and Challenges for PHA in USA

The U.S. market is characterized by high-tech innovation to solve biological problems.

Technological Innovation

Key Industry Players

Real-World Applications

We are seeing PHA appear in everyday items, though often in niche markets:

Structural Challenges

Despite the innovation, there are significant hurdles:

5.5 Canada

Canada is one of the world’s leading producers of bioplastics, and Polyhydroxyalkanoates (PHAs) form an important part of its transition toward a circular, bio-based economy.

The Canadian approach stands out in two ways.

First, many companies focus on using waste materials such as food waste or gases as feedstock.

Second, Canada has developed specialised forms of PHA, particularly medium-chain-length PHA (mcl-PHA), which are softer and more elastic than the more rigid versions of the polymer.

This combination of feedstock innovation and material specialisation gives Canada a distinct position within the global PHA landscape.

Canada – PHA Market at a Glance

| Metric | Status |

|---|---|

| Bioplastics market value | US$465.6 million (2021) |

| Global production rank | Top five globally |

| North America share | ~19% of global capacity |

| Unique PHA specialization | mcl-PHA (PolyFerm Canada) |

| Key feedstocks | Food waste, wood cellulose, C1 gases |

| Organics access | 71% curbside access |

| Compost acceptance | Limited; most facilities reject compostable plastics |

| Main challenges | High cost, brittleness, strict labeling, composting gaps |

5.5.1 Current PHA Market Size and Global Share For Canada

Canada is consistently ranked among the top five global producers of bioplastics, alongside China, the United States, Germany, and Brazil.

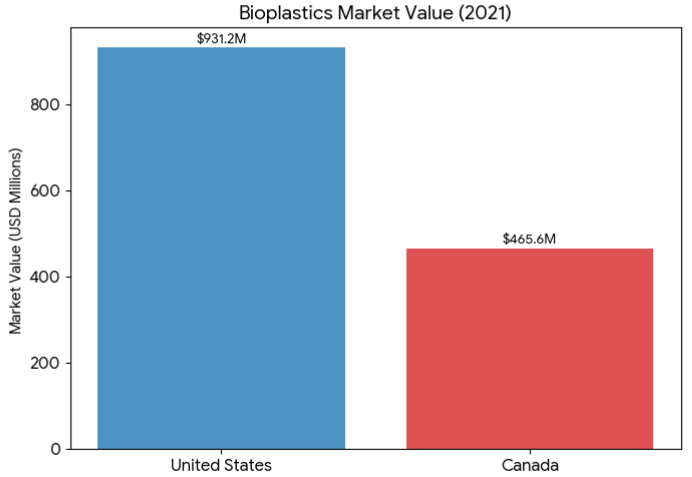

In 2021, Canada’s bioplastics market was valued at approximately US$465.6 million.

This places the Canadian market at roughly half the size of the US bioplastics market.

North America accounts for about 19% of global bioplastics production capacity, although Canada’s precise share of PHA alone is not publicly reported.