Prepared by

Ukhi Research Division

Ukhi Bioplastics Private Limited

India

Report Highlights

- Most published estimates for the compostable injection-moulding market include non-compostable bio-based resins — bio-PE, bio-PA, bio-PP — that have no business being in the same category. This report applies a strict EN 13432 scope throughout and shows why the real addressable market is meaningfully smaller than syndicated research suggests.

- This is a regulation-driven market, and the regulatory stack is now moving from proposal to enforcement. The EU PPWR entered into force in February 2025. Oregon’s EPR programme began collecting fees in July 2025. This report maps every significant regulatory event with specific dates, article numbers, and the product categories each affects.

- The material you should probably be paying more attention to is not PLA. PBS (polybutylene succinate) outperforms PLA on heat resistance, processing ease, and home-compost certification, and runs at PP-equivalent cycle times with no heated tooling requirement. Starch blends are the only other commercially available home-compostable injection material and run at near-PP throughput. Both receive a fraction of the investor attention directed at PLA. This report explains why, and whether that is about to change.

- The Danimer Scientific bankruptcy is the most important data point in this market, and most analyses have not drawn the right conclusions from it. Danimer built real production capacity for a technically superior material, raised $890 million, and was sold for $19 million. This report analyses what actually happened and draws specific, transferable lessons for how to underwrite any position in this sector.

- The investable opportunity is not where most capital has gone. Upstream resin manufacturing has absorbed the bulk of investment. The underserved positions are where durable margins are more likely to sit. This report maps each gap with enough specificity to support a genuine investment thesis.

Publication Details

Publication Date: May 2026

Publisher: Ukhi Bioplastics Private Limited

Location: New Delhi, India

Report Period Covered: Regulatory and market data current as of Q1 2026

This report is produced by Ukhi for information purposes only. It does not constitute investment advice, a solicitation to invest, or a recommendation to buy or sell any security or asset.

All market size estimates, pricing data, and capacity figures are drawn from the sources cited and reflect information available through April 2026. Where data is contested, uncertain, or based on announced-but-unbuilt capacity, this is flagged explicitly in the text. Readers should conduct their own due diligence before making any investment decision.

Forecasts are inherently uncertain. The scenarios presented in this report are analytical frameworks, not predictions.

Executive Summary

Compostable plastics for injection moulding represented a roughly $1.8 to $2.2 billion global market in 2025. It is growing at 6 to 10% annually toward $4.0 to $4.5 billion by 2035.

That makes this market approximately 0.7% of the total injection-moulding market and likely to stay a single-digit-percentage niche through the decade.

The investment thesis for investors is not that compostable resins will displace conventional plastics at scale. It is that:

- a specific, regulation-defined set of product categories is being legally mandated or commercially pulled toward certified-compostable formats, and

- that the producers, compounders, and converters supplying those formats operate in a policy-protected segment with pricing power, entry barriers, and a growing body of enforceable demand.

That demand floor is being hardened by a stack of regulations that are now moving from proposal to enforcement:

- The EU PPWR mandates certified-compostable formats for specific product categories from February 2028

- California’s SB 54 requires 100% of single-use packaging to be recyclable or compostable by 2032

- India’s Plastic Waste Management Rules exempt certified compostables from single-use plastic bans, creating an immediate route to market

- Spain’s plastic tax of €0.45/kg exempts compostable formats outright

- Rising EU carbon prices — at €75/tonne in April 2026 and forecast at €126 to €150/tonne by 2030 — progressively increase the effective cost of conventional plastic, narrowing the resin-price gap

The downside forces are equally real.

- Compostable resins still cost 2 to 6 times more than the polypropylene they replace,

- composting infrastructure is inadequate in most markets, and

- the capital demands of scaling new polymer production have already destroyed significant investor value.

Danimer Scientific, which entered the market with an $890 million SPAC valuation in 2020 and was the world’s leading PHA producer, filed for Chapter 11 bankruptcy in March 2025 and was sold for $19 million, approximately 2 cents on the funded-debt dollar.

Five Key Findings

1. The market is significant, but its size is consistently overstated in syndicated research.

The most frequently cited figures for the “compostable biopolymer injection moulding market” include non-compostable bio-based resins such as bio-PE and bio-PA. This is an error, and it inflated the addressable market for certified-compostable formats by 15 to 30%.

Applying a strict EN 13432 scope, the 2025 market is $1.5 to $2.6 billion.

The range reflects the uncertainty that must be acknowledged for what it is, as no single published dataset of analysis for “compostable biopolymer injection molding market” isolates certified-compostable and injection-molding-relevant materials with precision.

The growth rate of 6 to 10% CAGR is credible and consistent across multiple independent methodologies. Reaching the upper end of that range requires two things to happen simultaneously:

- EU PPWR implementation to proceed on schedule without dilution through delegated acts, and

- US state EPR programmes to generate enough fee pressure on conventional plastics that brand owners begin switching to compostable formats in volume by 2027.

The base case — 6 to 8% — requires only the EU regulatory pathway to hold.

2. Regulation is the real demand driver, and it is now moving from policy to enforcement.

The EU PPWR, entered into force February 2025, mandates industrial compostability for tea bags, coffee capsule single-serve units, and fruit-and-vegetable stickers from February 2028, with provisions for EU member-state to extend mandates to non-permeable coffee capsules.

Spain’s plastic tax exempts compostables outright.

The UK Plastic Packaging Tax rose to £228.82 per tonne in April 2026.

The carbon-price trajectory matters for cost comparisons. EU ETS carbon allowances stood at €75 per tonne in April 2026, with market consensus forecasting €126 to €150 by 2030. At those levels, the carbon cost embedded in a kilogram of polypropylene rises by roughly 12% at today’s prices and materially more by 2030, which mechanically reduces the effective price gap between PP and compostable resins each year.

For coffee capsules — a 3-gram rigid part produced at 100 million units per year — the nominal resin-price premium of PLA over PP is approximately 42%. Once Spain’s plastic-tax exemption for compostables, UK PPT savings, and reduced EU EPR fees are applied, that premium compresses to approximately 28% on a total-cost-of-ownership basis at 2026 policy levels. By 2030, at consensus carbon prices, it will compress further. The investment thesis in this market is not a bet on polymer chemistry getting cheaper. It is a bet on the policy cost of conventional plastic getting more expensive.

3. PLA leads the market today, but PBS and starch blends are being systematically overlooked.

PLA accounts for approximately 36 to 39% of the certified-compostable plastics market and is the default for injection-moulded cutlery, capsules, and food containers.

Its limitations are:

- a 20 to 50% cycle-time penalty versus PP in crystallised grades,

- a 55°C heat deflection temperature in standard grades that rules it out of hot-fill applications, and

- prices of $2.40 to $3.30/kg that may drift toward $1.80 to $2.20/kg by 2028 as Asian and Middle Eastern capacity comes online.

PBS (polybutylene succinate) receives far less attention but offers:

- a 95 to 108°C heat deflection temperature,

- home-compost certification,

- PP-equivalent cycle times, and

- a processing profile the industry describes as the easiest of all compostable polymers to run.

The reason it has not broken through is supply, not performance: global certified bio-PBS capacity sits at approximately 20,000 tonnes per year, almost entirely with PTT MCC Biochem in Thailand. That is a volume too small to serve large brand programmes. As Chinese producers expand petrochemical PBS capacity and prices fall toward $2.50 to $3.00/kg, the supply constraint will ease.

4. PHA offers unique environmental credentials and unique investment risk.

PHA is the only polymer family certified compostable in industrial, home, soil, and marine environments, which positions it uniquely as regulations tighten around marine litter and home-compostability claims.

The risk is equally distinctive.

- PHA is produced by bacterial fermentation, an inherently capital-intensive process with lower carbon yields and higher feedstock costs than petrochemical polymer production.

- Current PHA production costs sit at $4 to $6/kg (three to five times the cost of PP) and are unlikely to reach parity before 2030 to 2032 even in optimistic scenarios, because closing that gap requires both a step-change in fermentation yield and a shift to waste or non-food feedstocks (waste cooking oil, methane, municipal wastewater). Neither has been demonstrated at commercial scale.

Danimer Scientific’s trajectory illustrates this precisely.

- The company was valued at $890 million through a SPAC listing in 2020, built what was then the world’s first commercial-scale PHA fermentation facility, and attracted customers including Nestlé and PepsiCo.

- By 2024 it was running at approximately 15% of facility capacity, losing $72 million on $26 million of revenue in nine months.

- It filed for Chapter 11 in March 2025 and was sold to Teknor Apex in July 2025 for $19 million.

Today, the technology is intact; Teknor Apex acquired 480+ patents alongside the physical assets. But the capital structure that tried to finance PHA at scale before sufficient demand materialised did not survive. Investors should treat any PHA position as a long-dated, high-variance technology bet, sized accordingly.

5. Infrastructure is the ceiling on addressable market size, and composting capacity is the most under-capitalised gap in the value chain.

A compostable plastic that cannot reach an industrial composting facility is, in practice, a contamination risk to the recycling stream and a landfill input.

For context:

- fewer than 200 of approximately 4,700 US composting facilities accept certified compostable packaging, and

- EU biowaste collection, mandatory from January 2024, covers only approximately 26% of potential kitchen waste generation, with 74% still going to landfill or incineration.

Without collection and processing infrastructure, compostability certification is a necessary but insufficient condition for regulatory compliance, consumer claims, and brand credibility.

The most underserved investment opportunities in this value chain are in composting infrastructure, certified-compostable compounding capacity for specific applications, and end-of-life traceability technology, rather than in primary resin manufacturing, where Chinese overcapacity in PLA and PBAT is compressing margins.

About This Report

This report was researched and written by Ukhi for investors and venture capital practitioners evaluating positions in the compostable plastics value chain, with specific focus on the injection-moulding segment.

It is being published at a moment that makes the analysis both timely and somewhat perish, becauseable:

- the EU Packaging and Packaging Waste Regulation entered into force in February 2025;

- Danimer Scientific filed for Chapter 11 in March 2025 and was sold to Teknor Apex in July 2025;

- NatureWorks’ 75,000 tonne/year integrated PLA facility in Thailand and Emirates Biotech’s 160,000 tonne/year PLA plant in Abu Dhabi are both under active construction, with first production targeted for 2026/2027 and 2028 respectively.

The regulatory and commercial landscape is shifting fast, and any analysis of this market has a limited shelf life.

Specific regulatory timelines, pricing data, and company statuses in this report reflect information available through April 2026.

The report is written for an investor audience. That means it is focused on where the money is, where the risks are, and which facts matter for capital allocation.

Scope and Boundaries

In scope:

- Plastic polymers that are (a) certified, or certifiable, under EN 13432, ASTM D6400, or ISO 17088, and (b) commercially injection-mouldable on standard or modestly retrofitted equipment

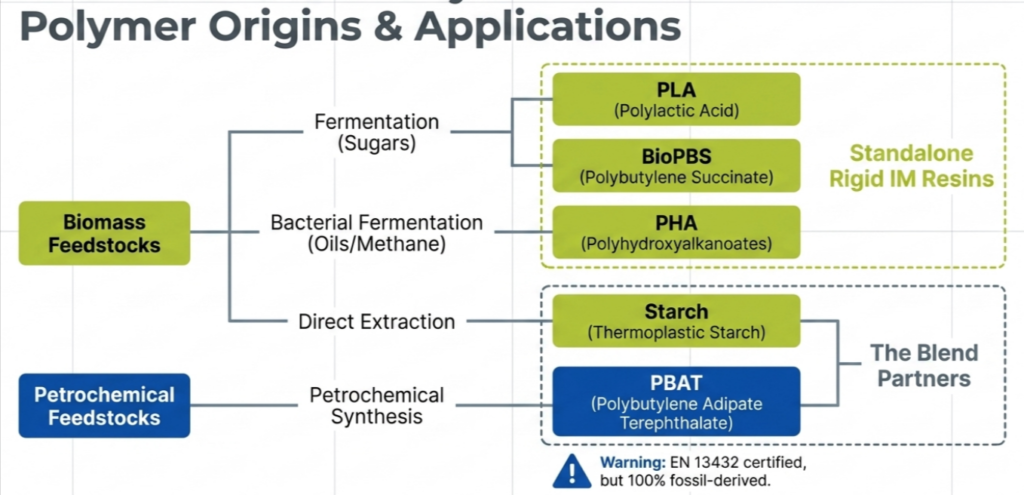

- Materials covered: PLA, PHA (all sub-types: PHB, PHBV, PHBH, PHACT, mcl-PHA), starch blends (TPS/PBAT, TPS/PCL, TPS/PLA), PBAT (as a blend component and in narrow standalone formats), and PBS

- Cellulose acetate is included as a watch-list boundary case only: it is bio-based and injection-mouldable but carries no EN 13432 certification and is not counted in any market-size figure

- Geographic scope: global, with detailed treatment of the EU, the United States, China, India, Southeast Asia, and the UAE

- Time horizon: 2025 to 2035, with primary emphasis on the 2025 to 2030 investment window

Out of scope:

- Bio-based but non-compostable resins: Braskem Bio-PE, Coca-Cola PlantBottle bio-PET, bio-PP, bio-PA. These use renewable feedstocks but do not biodegrade under EN 13432 conditions and are excluded from all volume and value estimates in this report.

- Recycled conventional plastics (rPET, rPP, rHDPE). These are referenced only as a competitive dynamic.

- Compostable films, flexible packaging, mulch films, and thermoformed sheet. These use some of the same resins and are referenced for context, but form factors outside injection moulding are not sized or profiled.

- Oxo-degradable plastics. These are banned under the EU Single-Use Plastics Directive and disqualified by EN 13432 and ASTM D6400.

Methodology

No single published dataset cleanly isolates certified-compostable injection moulding as a distinct category. We have addressed this by drawing on multiple independent source types and being explicit about where the data is solid and where it requires judgement.

Primary sources used directly:

- Manufacturer technical data sheets and processing guides (NatureWorks, TotalEnergies Corbion, Kaneka, CJ Biomaterials, PTT MCC Biochem, BASF, Novamont, Biotec, Eastman)

- Full regulatory texts (PPWR, SUPD, SB 54, India Plastic Waste Management Rules)

- Corporate disclosures and filings (Danimer Chapter 11 filing March 2025, Balrampur Chini board disclosures 2025, Versalis/Eni press releases, Emirates Biotech/Sulzer press releases)

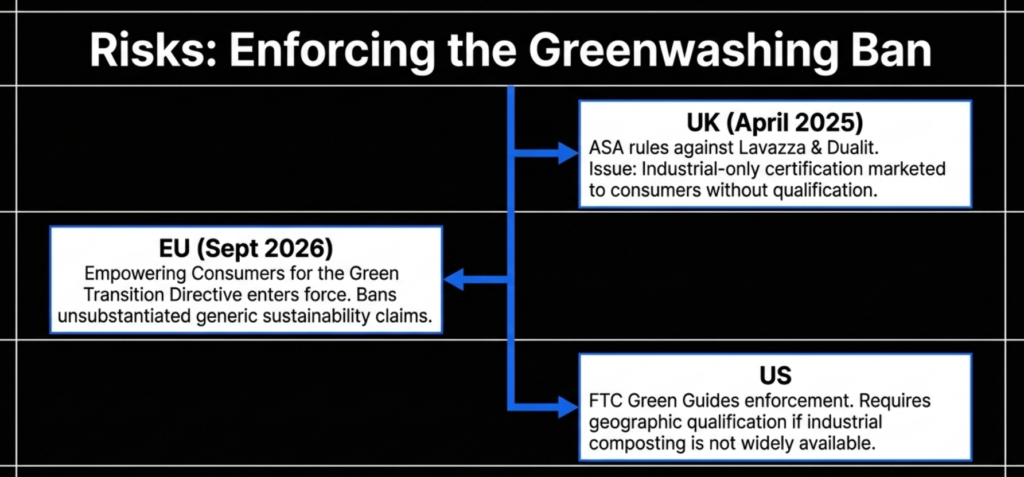

- Enforcement records including ASA rulings against Lavazza and Dualit (April 2025)

- European Bioplastics and nova-Institute annual market data reports (2024 and 2025 editions).

Secondary and market-intelligence sources:

- Spot pricing from ChemAnalyst, IMARC, Price-Watch.ai and Intratec, dated to Q1 and Q2 2025 unless stated.

- Synthetic market research from Grand View Research, Straits Research, Future Market Insights, and MarketsandMarkets is used for cross-referencing, not as primary inputs.

- Where their methodologies include non-compostable bio-resins in “biopolymer injection moulding” scopes, we apply explicit adjustments and note them.

Market sizing has been done using three independent methods:

- Top-down from the total compostable plastics market: We start with the published size of the overall compostable plastics market and apply the estimated share that flows into injection-moulded products.

- Application-segment build-up: We add up known end-use categories — cutlery, coffee capsules, food-container closures, agricultural components, medical disposables — and aggregate the revenue each represents.

- Resin-volume conversion: We start from known or estimated resin production volumes, apply the fraction converted through injection moulding, and multiply by average selling prices to derive a revenue figure.

Currency: All figures are in USD unless otherwise stated.

Uncertainty flags: Where data is sparse, contested, or dependent on announced-but-unbuilt capacity, we flag it explicitly.

What are Compostable Plastics for Injection Molding?

1.1 What Is Injection Moulding

Injection moulding is the dominant manufacturing process for producing rigid and semi-rigid plastic parts at scale. In this process, plastic resin pellets are fed into a heated barrel, melted, and then injected under high pressure into a precision-machined steel mould. Once cooled, the mould opens and the finished part is ejected. A single cycle typically takes between 5 and 60 seconds depending on part geometry, wall thickness, and resin type.

The process is used to make almost every rigid plastic object: cutlery, bottle caps, food containers, coffee capsules, cosmetic closures, medical devices, and thousands of industrial components.

Global injection moulding market size was approximately $370 to $385 billion in 2024 and is growing at a 4.3 to 4.7% CAGR, making it the largest single plastics processing sector by value.

What makes injection moulding relevant to the compostable plastics story is its reach into exactly the product categories that regulators are targeting: single-use food-service items, packaging closures, and disposable consumer goods.

Why it matters for investors: The mandated product categories in EU and US packaging regulation are almost entirely injection-moulded. Compostable resins that cannot run on standard injection-moulding equipment have no path into those mandated formats. The processing question and the commercial opportunity are the same question.

1.2 What Are Compostable Plastics

Compostable plastics are polymers that break down into CO2, water, and biomass under defined composting conditions, within a specified timeframe, without leaving toxic residues.

The word “compostable” is a technical certification category, not a general description. Plastics marketed as “biodegradable” without third-party certification do not automatically qualify as ‘compostable’.

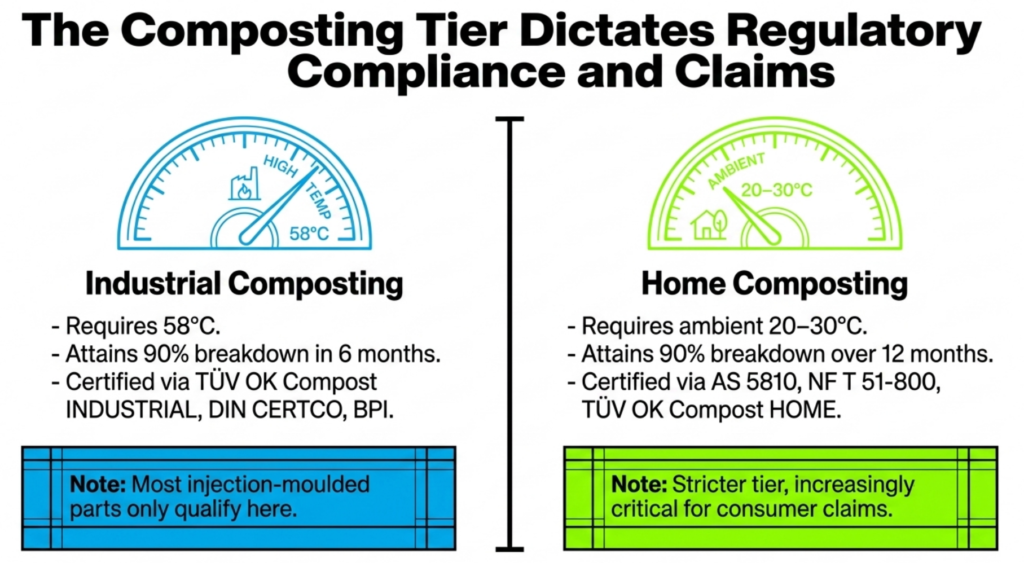

Definition: A plastic is certifiably compostable if it passes EN 13432 (Europe), ASTM D6400 (North America), or ISO 17088 (international). Each standard requires:

- at least 90% biodegradation to CO2 within six months at 58°C,

- full disintegration within 12 weeks, and

- no ecotoxicological harm to plants.

Products that pass are permitted to carry third-party certification marks: TÜV Austria’s OK Compost INDUSTRIAL mark, the European Bioplastics Seedling logo, DIN CERTCO’s DIN-Geprüft Industrial mark, or BPI certification (the Biodegradable Products Institute, US).

There is a further, stricter tier: home compostability, certified under AS 5810 (Australia), NF T 51-800 (France), or TÜV’s OK Compost HOME mark, which requires the same biodegradation threshold but at ambient temperatures of 20 to 30°C over 12 months.

Most injection-moulded compostable plastic parts only qualify for industrial composting, not home composting. This distinction matters increasingly for regulatory compliance and consumer claims.

1.3 Types of Compostable Plastics for Injection Moulding

Not all compostable polymers can be injection moulded. Processing temperatures, melt flow, and cooling behaviour all determine whether a material is suitable for injection molding.

The following families qualify commercially today.

Materials in scope:

-

PLA (polylactic acid)

- The dominant material, which accounts for approximately 36 to 39% of the compostable plastics market

- Bio-based (from corn or sugarcane), industrially compostable under EN 13432 and ASTM D6400

- Used in cutlery, coffee capsules, cold cups, food containers, and cosmetic packaging. Standard grades are not home-compostable

-

PHA (polyhydroxyalkanoates)

- A family that includes PHB, PHBV, PHBH (Kaneka Aonilex), and PHACT (CJ Biomaterials)

- The only polymer family certified for industrial, home, soil, and marine composting

- Used in straws, capsules, agricultural components, and medical disposables

- Currently priced at $4.50 to $8.00/kg, with global capacity of approximately 50 to 65 kt/year

-

Starch blends:

- Thermoplastic starch (TPS) compounded with PBAT, PCL, or PLA

- Leading brands include Novamont Mater-Bi and Biotec Bioplast

- Many grades carry home-compost certification

- Used in cutlery, plant pots, capsules, and agricultural clips. Closest to PP in processing behaviour

-

PBAT (polybutylene adipate terephthalate):

- Fossil-derived but EN 13432 certified

- Rarely injection moulded standalone due to very low stiffness

- Used primarily as a toughening agent in PLA and starch blends

- BASF’s ecovio IS grades are the main injection-moulding formulations

-

PBS (polybutylene succinate)

- Underutilised relative to its technical merits

- Heat deflection temperature of 95 to 108°C

- home-compostable, and the easiest of all compostable polymers to injection mold

- PTT MCC Biochem (BioPBS) is the leading bio-based producer

- Priced at $3.50 to $4.50/kg

Materials out of scope:

- Bio-based but non-compostable drop-ins such as Braskem’s Bio-PE, Bio-PET, bio-PP, and bio-PA. These use renewable feedstocks but do not biodegrade and carry no EN 13432 certification.

- Recycled conventional plastics (rPET, rPP, rHDPE) form a separate $40 billion market and are positioned as an alternative pathway to sustainability. They are not compostable.

- Oxo-degradable plastics are explicitly disqualified by EN 13432 and banned under the EU Single-Use Plastics Directive. They fragment into microplastics rather than fully biodegrading.

- Cellulose acetate (Eastman Treva, Daicel) is 42 to 45% bio-based and injection-mouldable but carries no EN 13432 certification. It is best understood as a bio-based engineering thermoplastic competing with ABS, not as a compostable material.

Insight: The boundary of this market is defined by certification, not by what a material is made from. A polymer produced entirely from plant-based feedstocks is not compostable for regulatory purposes unless it passes EN 13432 within the required timeframe. Several bio-based materials fail this test because their degradation rate at industrial-composting temperatures is too slow. Bio-content and compostability are related but distinct properties, and conflating them is one of the most common errors in market reporting on this sector.

2. Compostable Plastics for Injection Molding – Market Definition and Sizing

2.1 Approaches to Sizing the Compostable Plastics Injection Moulding Market

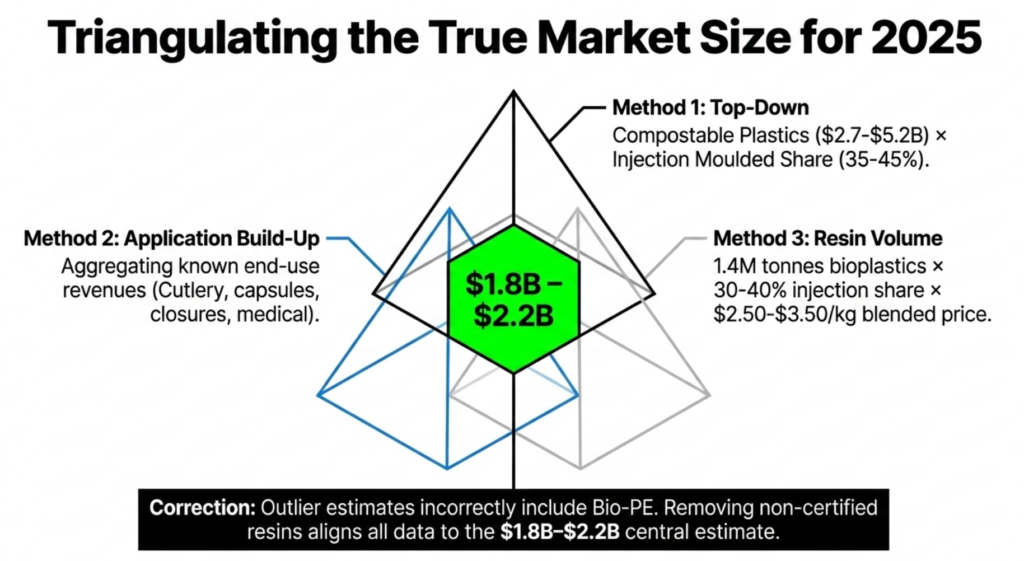

The compostable injection moulding market is a subset at the intersection of two larger markets: the global injection moulding industry and the global compostable plastics market. Both are well-documented individually but there is no single, standardised report isolating their overlap. Sizing the sub-market requires triangulation from three directions.

Method 1 — Top-down from compostable plastics: The global compostable plastics market size was estimated at $2.7 to $5.2 billion in 2024 and 2025 across Grand View Research, Straits Research, and Market Research Future.

Applying the injection-moulded share of compostable plastics consumption (typically 35 to 45% by value, given that injection moulding addresses higher-margin rigid formats) yields a sub-market of $1.0 to $2.3 billion for 2024.

Method 2 — Application-segment build-up: Using this approach, we add known end-use categories: food-service cutlery and plates, coffee capsules, food container closures, agricultural components, and medical disposables.

Adding these categories and applying the revenue bands reported by Future Market Insights for each end-use application produces an aggregate 2025 estimate of $1.5 to $2.2 billion for certified-compostable injection-moulded products. This method is useful as a cross-check because it starts from actual product volumes rather than resin capacity, but it depends on the accuracy of per-category revenue estimates that are themselves not always well-sourced.

Method 3 — Resin-volume conversion: The third method starts from resin supply. European Bioplastics and nova-Institute report total biodegradable bioplastics production at approximately 1.4 million tonnes in 2025. We estimate that 30 to 40% of that volume is processed through injection moulding rather than film extrusion, thermoforming, or fibre production, based on end-use application splits from industry data. Multiplying that volume by a blended average resin price of $2.50 to $3.50/kg gives a revenue estimate of $1.0 to $2.0 billion.

Clarification: All three methods produce overlapping ranges, which is reassuring. This convergence means that the general order of magnitude is consistent across different starting assumptions. The genuine uncertainty comes from two sources: different market reports use different definitions of what counts as “compostable” (some include non-certified bio-resins, inflating the figure), and there is unavoidable double-counting risk between the value of resin sold and the value of converted goods, since both appear in different published estimates. For these reasons, we present a range rather than a point estimate.

2.2 Compostable Plastics for Injection Molding – Market Size and Forecast

The compostable injection moulding market in 2025 was estimated at $1.5 to $2.6 billion, with a central estimate of approximately $1.8 to $2.2 billion. The most specific published study (Future Market Insights’ Biopolymer Injection Molders Market — October 2025) puts 2025 revenue at $2.6 billion, but its scope includes bio-PE, which is bio-based but not compostable and should not be counted. Removing bio-PE and equivalent non-certified resins reduces the figure by approximately 15 to 20%, which brings it into line with our central estimate.

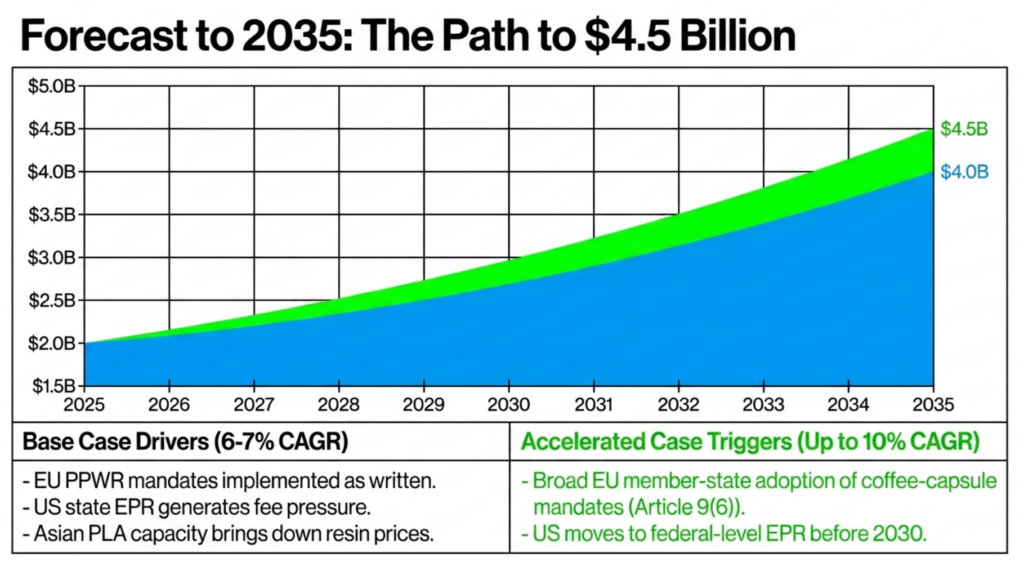

Compostable injection moulding market forecast to 2035

The market is forecast to reach $4.0 to $4.5 billion by 2035, at a CAGR of 6 to 10%.

-

The lower end of that range reflects the base case, which assumes:

- EU PPWR mandates are implemented broadly as written,

- US state EPR programmes generate meaningful fee pressure on conventional plastics, and

- Asian PLA capacity additions bring resin prices down gradually.

-

The upper end applies if:

- PPWR drives broader member-state adoption of compostable coffee-capsule mandates under Article 9(6), and

- if the US moves toward federal-level EPR before 2030.

The growth rate slows from 8 to 10% in the 2025 to 2030 period to 6 to 7% in 2030 to 2035 as the most directly mandated categories mature and the market for discretionary adoption faces more competition from recycled conventional plastics.

2.3 Compostable Plastics for Injection Molding – Regional Market Analysis

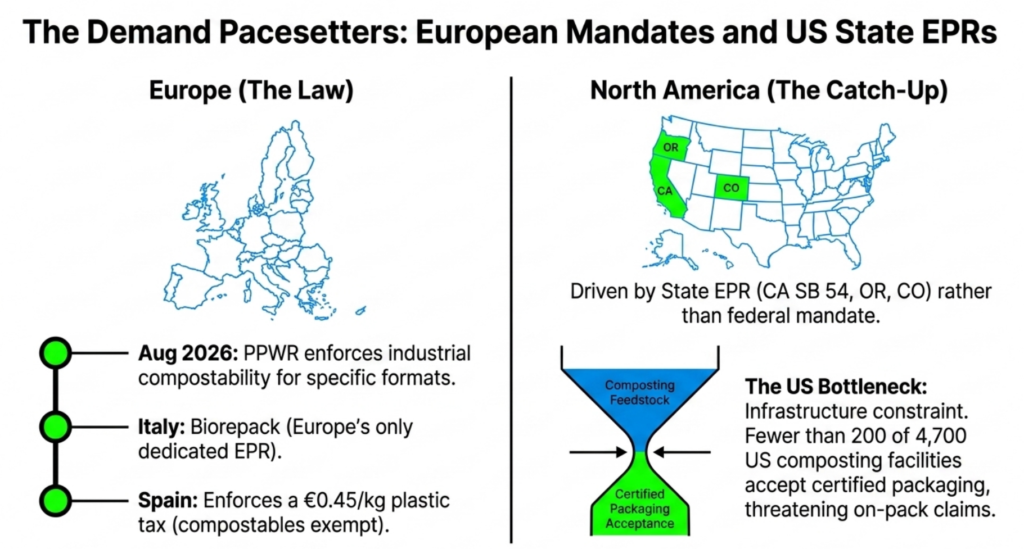

Europe

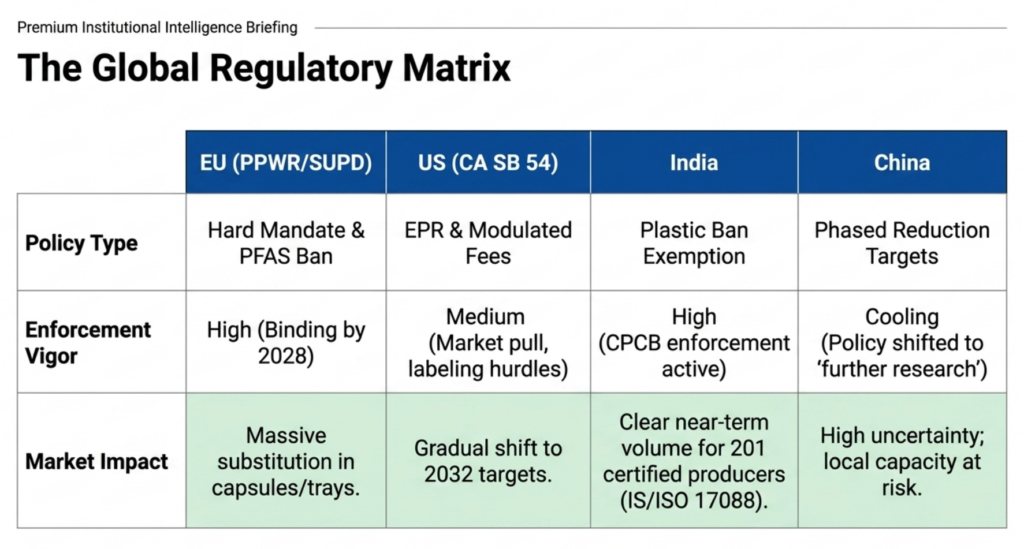

Europe’s compostable plastics market is the most developed in policy terms and among the highest in per-capita consumption. The EU Packaging and Packaging Waste Regulation (PPWR), which entered into force on 11 February 2025 and applies from 12 August 2026, mandates industrial compostability for tea and coffee bags, fruit stickers, and lightweight carrier bags. Member states may additionally mandate compostable coffee capsules, creating a legally protected and growing injection-moulding demand stream.

Italy operates the most advanced national infrastructure, with mandatory separate organic-waste collection across all municipalities. Italy’s Biorepack is Europe’s only EPR scheme dedicated to compostable packaging.

EU bioplastics demand is underpinned by further national plastic taxes in Spain (€0.45/kg, with compostables exempt), France, and an Italian levy targeting July 2026.

Europe accounts for approximately 13% of global bioplastics production capacity but a disproportionately higher share of premium compostable injection-moulded consumption, given consumer acceptance and regulatory pull.

Asia-Pacific

Asia-Pacific

Asia-Pacific compostable plastics market leads on volume, and is driven by Chinese capacity expansion and growing domestic regulation.

-

China’s PBAT market capacity has grown sharply:

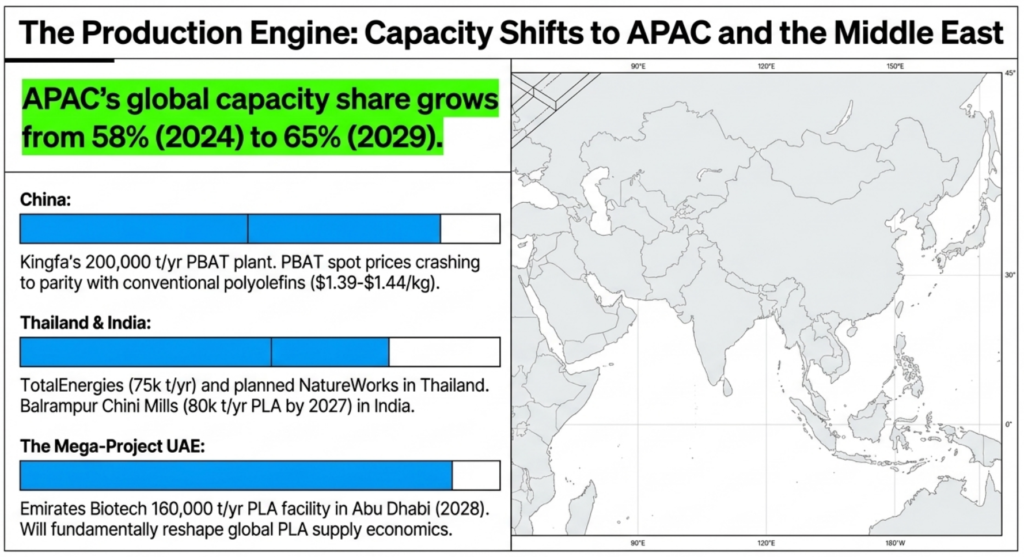

- Kingfa’s Zhuhai/Jiangmen plant alone exceeds 200,000 t/yr

- Chinese PBAT spot prices fell approximately 45 to 50% from 2022 peaks to around $1.39 to $1.44/kg by mid-2025, approaching parity with conventional polyolefins.

- Chinese domestic policy under the “white pollution” regulations mandates biodegradable substitutes in foodservice in Hainan Province and major cities, though national enforcement has been uneven.

- Japan mandates separate food-waste collection and subsidizes biodegradable mulch.

- South Korea bans single-use plastic cups and plastic straws in cafes and restaurants under rules enforced since 2022, with compostable alternatives permitted in certified categories.

- Thailand hosts TotalEnergies Corbion’s 75,000 t/yr PLA plant and the planned NatureWorks 75,000 t/yr integrated facility.

- India’s Plastic Waste Management Rules exempt certified compostable plastics from single-use bans, giving the country’s emerging converter base a route to market.

- The Balrampur Chini Mills’ 80,000 t/yr PLA plant in Uttar Pradesh, targeted for December 2027, signals India’s ambition to become a domestic compostable resin producer.

- Asia-Pacific bioplastics market share in global capacity is growing: from approximately 58% in 2024 to a projected 65% by 2029 as Chinese and Thai expansions outpace European and US investment.

North America

North America compostable plastics market is primarily driven by state-level legislation rather than federal mandate.

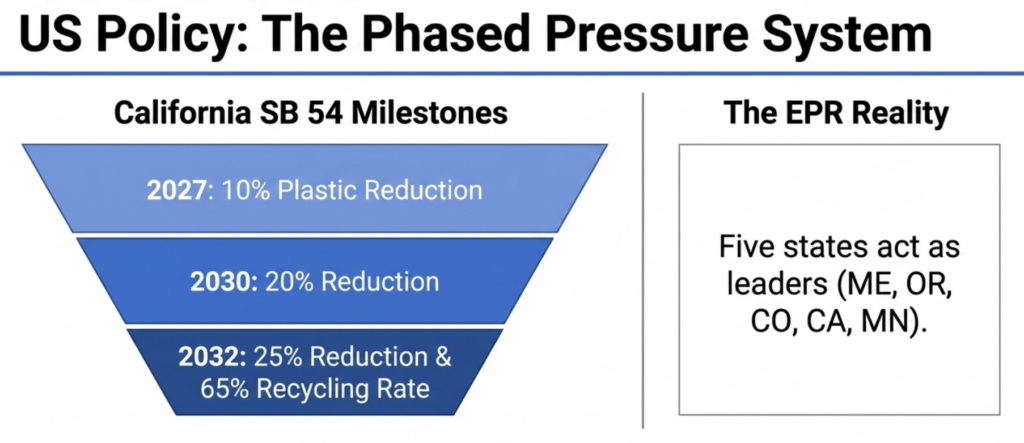

- California’s SB 54, the most consequential US packaging law, requires 100% of single-use packaging to be recyclable or compostable by 2032.

- The Circular Action Alliance (CAA), designated as the Producer Responsibility Organisation for California, Colorado, and Oregon, began invoicing the first producer fees in August 2026.

- Oregon’s EPR programme became operational in July 2025, making it the first state to collect producer fees.

- Colorado’s fee programme followed in January 2026.

- Compostable foodservice is well-established commercially in the US, with Eco-Products, World Centric, and Vegware serving national accounts from PLA-sourced cutlery and container lines.

- The constraint is infrastructure, as there are fewer than 200 of approximately 4,700 US composting facilities that accept certified compostable packaging, limiting the credibility of on-pack claims.

- US federal policy remains limited to advisory guidance and no federal EPR or compostability mandate exists as of mid-2026.

Middle East and Other Emerging Markets

The UAE compostable plastics investment story centres on Emirates Biotech’s planned 160,000 t/yr PLA facility in Abu Dhabi’s KEZAD zone (Sulzer technology licensed December 2024; first phase targeting 2028 commissioning).

If delivered, this would be the world’s largest single PLA site and would reshape global PLA supply economics from 2028 onward.

Latin America and Southeast Asia (Indonesia, Vietnam, Malaysia) are adopting city-level single-use bans but lack the composting infrastructure to support compostable-specific claims at scale.

3. Compostable Plastics for Injection Molding – Market by Material

This chapter offers a profile of each compostable polymer used in injection moulding across four dimensions:

- what the material is and how it performs,

- what it takes operationally and economically for a molder to switch from conventional resin to this material

- what it costs, and

- how large the market is globally and by region.

The materials covered are PLA, PHA, starch blends, PBAT, and PBS, with cellulose acetate included as a watch-list boundary case.

3.1 PLA (Polylactic Acid)

3.1.1 What Is PLA and What Are Its Properties

Polylactic acid (PLA) is the dominant compostable polymer in use today.

It is a bio-based polyester made by fermenting plant sugars and converting the resulting lactic acid into lactide, then into polymer.

The feedstock is nearly 100% bio-based carbon, and the material carries full industrial compostability certification under EN 13432, ASTM D6400, and ISO 17088.

Standard injection-moulding grades are not home-compostable. Home composting happens at ambient temperatures of 20 to 30°C, and PLA breaks down too slowly at those temperatures to pass the home-composting standards.

Industrial composting, which runs at 55 to 60°C in managed facilities, is the end-of-life route that standard PLA is certified for.

PLA mechanical and thermal properties relevant to injection moulding:

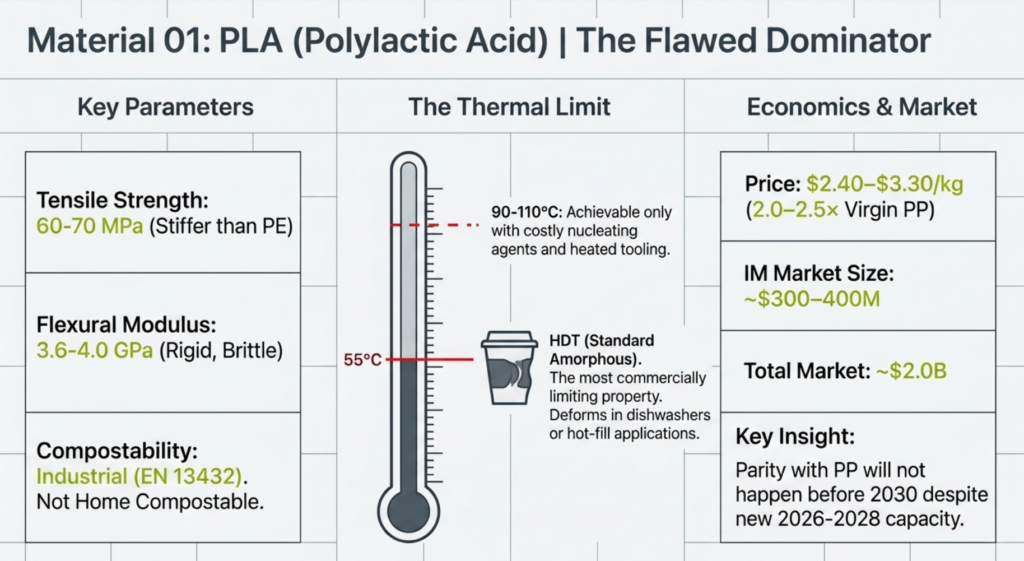

- Tensile strength at yield: 60 to 70 MPa — stiffer than polyethylene, comparable to polystyrene (PS)

- Flexural modulus: 3.6 to 4.0 GPa — rigid, slightly brittle

- Notched Izod impact: 2.5 to 5 kJ/m² — low, a persistent weakness

- HDT (standard amorphous grades): approximately 55°C — this is the material’s most commercially limiting property

- HDT (crystallised, nucleated grades): 90 to 110°C achievable with nucleating agents and heated tooling

- HDT (stereocomplex sc-PLA): up to 180°C, but commercially limited by cost

The 55°C heat deflection temperature of standard amorphous PLA is the most important number for buyers and investors to internalize.

It means a standard PLA cup deforms in a dishwasher or with hot-fill beverages. Solving this requires nucleating agents, higher mould temperatures, and longer cycle times — each of which adds costs to the process.

PLA applications in injection moulding include single-use cutlery, coffee capsules, cold-drink cups and lids, thin-wall food containers, cosmetic packaging closures, and some electronics casings.

PLA is also the dominant material in 3D printing filament, holding over 50% of the FDM filament market globally.

Known limitations: brittleness, poor impact resistance, inadequate heat tolerance for hot-fill applications, and susceptibility to hydrolytic degradation above 40°C in humid conditions.

3.1.2 PLA Cost: Price per kg vs PP and PS

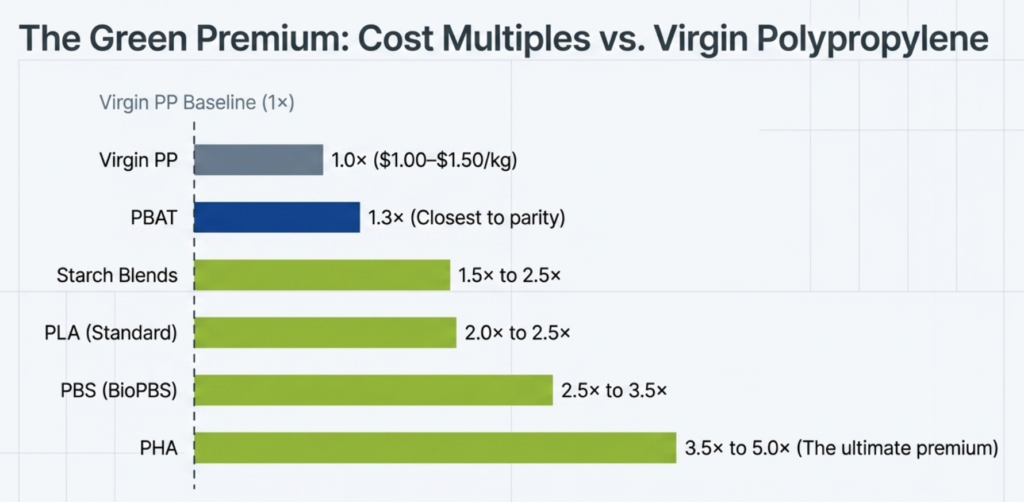

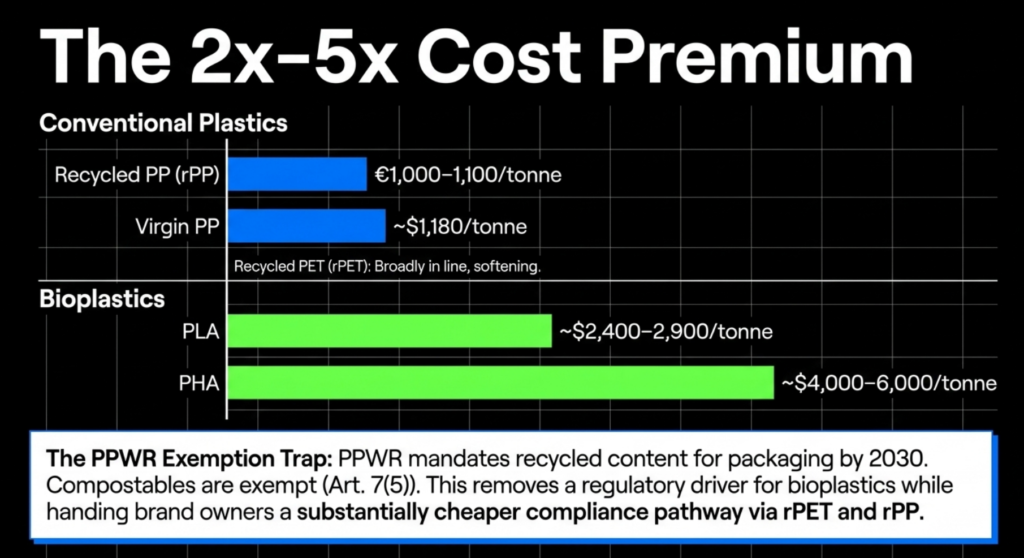

PLA price vs conventional plastics:

| Material | Spot price 2025 (USD/kg) | Multiplier vs PP |

|---|---|---|

| Virgin PP | 1.00 to 1.50 | 1× |

| Virgin PS | 1.10 to 1.60 | ~1.1× |

| Virgin PET | 1.00 to 1.40 | ~1.0× |

| PLA (standard grades) | 2.40 to 3.30 | 2.0 to 2.5× |

| PLA (high-heat nucleated compound) | 2.70 to 3.80 | 2.3 to 3.0× |

Regional pricing in 2025:

- approximately $2.42/kg in Northeast Asia,

- $2.72/kg in Germany (CFR Hamburg),

- $2.80 to $3.35/kg CIF India

Will PLA reach cost parity with PP?

Not before 2030. NatureWorks’ new Thailand plant (75 kt, commissioning delayed to 2026/2027) and Emirates Biotech’s UAE facility (160 kt, targeted 2028) will add meaningful global supply and may push spot prices to $1.80 to $2.20/kg by 2028, still 1.5 to 2× PP.

3.1.3 PLA Market Size: Global and Regional

Global PLA market size 2024 to 2025: Approximately $2.0 billion, growing at 15 to 18% CAGR.

By 2030, the base-case estimate is $4.0 to $4.5 billion. Forecast range variation is wide across syndicated research (ranging from $1.1 billion to $2.6 billion for the 2024 to 2025 base year).

This reflects different scope boundaries on whether bio-PE and non-compostable bio-resins are included. The figures above apply to PLA specifically.

PLA injection-moulding sub-market:

No published source isolates this cleanly. Applying a 15 to 20% injection-moulding share of total PLA value (the balance going to thermoformed packaging, films, and 3D printing filament), the PLA injection moulding market was approximately $300 to $400 million in 2024.

Regional split:

- North America: Approximately 38 to 41% of global PLA demand by value. The US is the world’s largest single consumer of PLA in food service applications (cutlery, cold cups, containers).

- Europe: Approximately 28 to 32% of global PLA demand. Europe is the fastest-growing regulated market, with the EU PPWR mandating compostable formats for tea bags, coffee single-serve units, and fruit stickers from February 2028.

- Asia-Pacific: Approximately 25 to 30% of global PLA demand by value, but the dominant production region. China holds an estimated 15% of global PLA capacity.

- India: Pre-commercial as a consumer market but capital is arriving. India’s Plastic Waste Management Rules exempt certified compostables from single-use plastic bans, creating demand.

- Middle East: Emirates Biotech’s 160 kt plant in Abu Dhabi’s KEZAD zone targets first-phase commissioning in early 2028. At $800 million total investment across two 80 kt phases, this would be the world’s largest single-site PLA facility.

3.2 PHA (Polyhydroxyalkanoates)

3.2.1 What Is PHA and What Are Its Properties

Polyhydroxyalkanoates (PHA) are a family of bio-based polyesters produced by bacterial fermentation. Microorganisms accumulate PHA granules intracellularly when grown under nutrient stress on feedstocks including plant oils, canola oil, sugars, or methane.

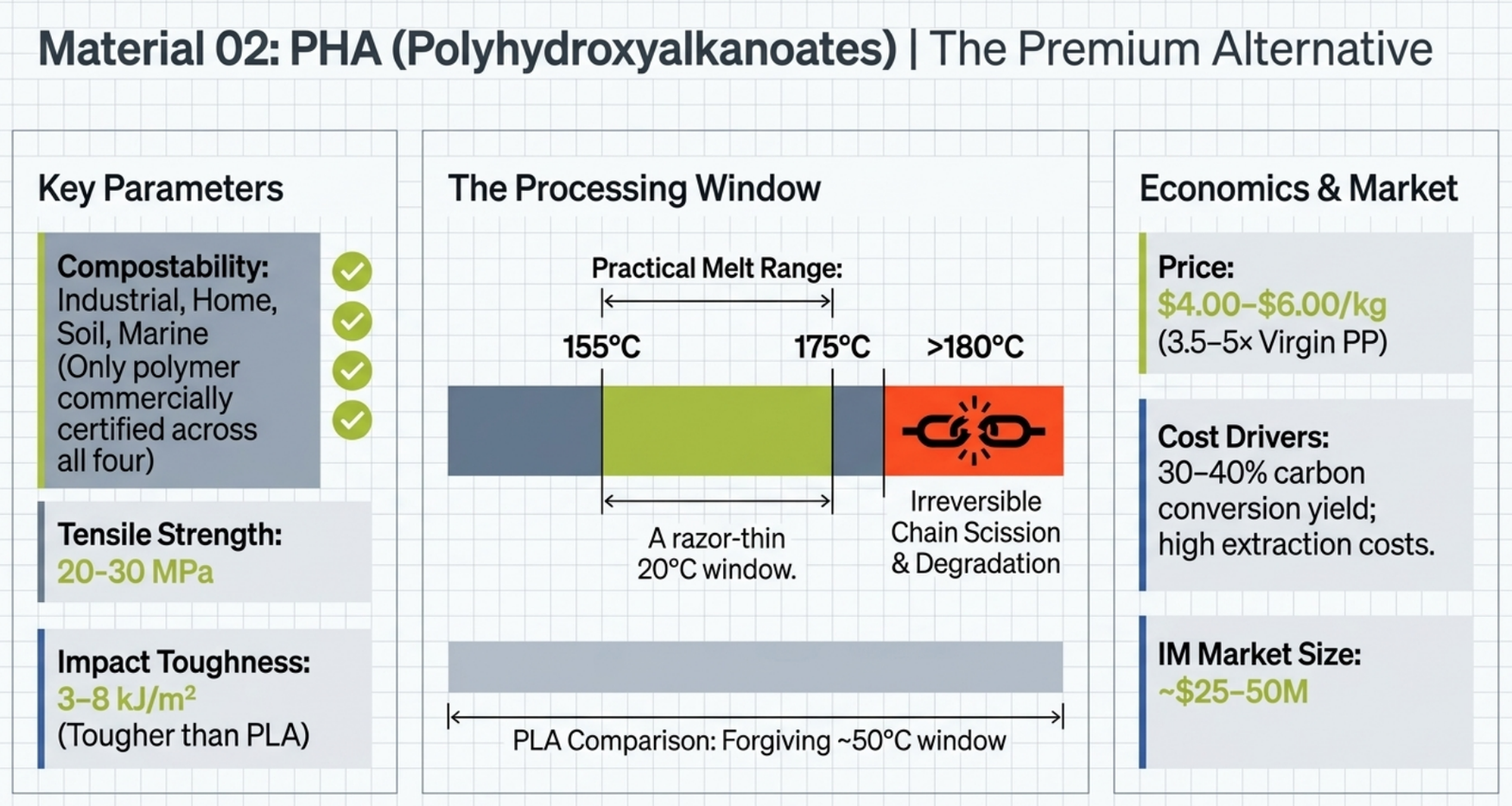

Most compostable plastics are certified for one end-of-life route only: industrial composting at 55 to 60°C in managed facilities. PHA is different. It is the only polymer family commercially certified compostable across all four recognised pathways — industrial composting, home composting, soil biodegradation, and marine biodegradation — meaning it breaks down in environments where the other materials in this chapter do not.

The PHA family includes several grades:

- PHB (polyhydroxybutyrate): The simplest PHA. Crystallises rapidly, brittle, narrow processing window. Rarely moulded in pure form.

- PHBV: A copolymer of 3-hydroxybutyrate and 3-hydroxyvalerate. TianAn Biologic (Ningbo, China) is the leading producer. Better processability than pure PHB.

- PHBH: Kaneka’s Aonilex / Green Planet brand. The 3-hydroxyhexanoate comonomer disrupts crystallinity, improving toughness and lowering the melting point to a more manageable range. This is currently the most commercially deployed injection-moulding PHA.

- PHACT: CJ Biomaterials’ brand. PHACT A1000P is amorphous and used as a modifier; PHACT S1000P is semi-crystalline and the primary injection grade. Both carry FDA food-contact substance listing and home-compost and marine certifications.

Key properties for injection moulding:

- Tensile strength: 20 to 30 MPa (lower than PLA)

- Notched Izod impact: 3 to 8 kJ/m² (significantly tougher than PLA)

- Melt point: 145 to 155°C for PHBH at 6 mol% 3HHx

- HDT: 80 to 110°C for crystalline PHB-rich grades

- Gas and moisture barrier: better than PLA, PBS, PBAT per Kaneka technical literature

The most important limitation of PHA in injection moulding is its narrow thermal processing window.

Degradation of PHB begins at 170 to 180°C, with chain scission accelerating sharply above 180°C.

The practical melt temperature range for PHBH is 155 to 175°C, which implies a 20°C window, compared with approximately 50°C for PLA.

This demands precise temperature control throughout the screw and barrel.

3.2.2 PHA Cost per kg

PHA is the most expensive compostable injection-moulding material by a wide margin.

| Material | Spot price 2025 (USD/kg) | Multiplier vs PP |

|---|---|---|

| Virgin PP | 1.00 to 1.50 | 1× |

| PHA (packaging/industrial grade) | 4.00 to 6.00 | 3.5 to 5× |

| PHA (medical-grade specialty) | 20 to 50 | 15 to 40× |

Why is PHA so expensive? Cost structure analysis from multiple peer-reviewed studies anchors PHA production cost at $4 to $6/kg at current scale. Three factors drive this:

- Fermentation yield: PHA fermentation achieves 30 to 40% carbon conversion from glucose, against 90 to 95% for PP from propylene. More feedstock is required per tonne of output.

- Feedstock cost: Vegetable oils account for 30 to 50% of PHA operating cost. Palm kernel oil (Kaneka) and canola oil (Danimer/Teknor Apex) are the primary substrates.

- Downstream extraction: Isolating PHA from inside bacterial cells requires solvent extraction, solvent recovery, and drying. These are expensive steps that have no equivalent in petrochemical production.

Scale: Global PHA production in 2024 was approximately 35,000 tonnes, against PLA at over 600,000 tonnes nameplate capacity. The scale gap is roughly 17×.

Path to lower PHA pricing: Credible analysis points to $2/kg as achievable if single-site capacity exceeds 100,000 tonnes and feedstocks shift to waste cooking oil, municipal wastewater-sludge PHA, or methane fermentation.

Realistic timeline: 2030 to 2032, contingent on execution that the industry has not yet demonstrated.

3.2.3 PHA Market Size: Global and Regional

Global PHA market size 2024: Approximately $100 to $150 million.

Published estimates vary significantly as some reports cite figures above $600 million, but those appear to include broader biopolyester categories rather than PHA specifically. The $100 to $150 million range is consistent with known physical production of approximately 35,000 tonnes globally in 2024 at average prices of $3,500 to $4,500/tonne, and is the anchor used in this report.

PHA market CAGR and forecast: 10 to 18% CAGR is the credible range.

This CAGR range would put the market at $250 to $400 million by 2030, contingent on the surviving producers (Kaneka, CJ Biomaterials, RWDC, and TianAn) executing planned capacity expansions. Forecasts published before 2025 that showed PHA reaching $1.2 billion or more by 2030 were built on assumptions about Danimer’s Bainbridge plant reaching 113 kt/yr. That expansion is now indefinitely paused. Those figures should be set aside.

PHA injection-moulding sub-market:

Approximately $25 to $50 million in 2024. The largest volume application is drinking straws, followed by coffee capsules, cutlery, cosmetic containers (Kaneka and Shiseido collaboration), and agricultural clips.

Regional split:

- Europe: The largest demand region, accounting for 40 to 55% of global PHA consumption by value. EU regulatory pull, strong consumer sustainability awareness, and premium packaging willingness to pay drive this. Europe lacks native PHA production capacity at scale.

-

Asia-Pacific: The primary production hub.

- Kaneka operates 5 kt/yr PHBH with an announced expansion to 20 kt/yr total;

- TianAn Biologic (Ningbo, China) operates approximately 10 kt PHBV;

- CJ Biomaterials operates 5 kt in Pasuruan, Indonesia.

- Japan is the most advanced PHA consumption market in Asia, driven by Kaneka’s Seven-Eleven deployment and Shiseido luxury cosmetics.

-

North America: Post-Danimer, the primary production assets are:

- RWDC Industries in Athens, Georgia (demonstration scale, 25 kt expansion targeted) and

- the Teknor Apex-owned Winchester, Kentucky and Bainbridge, Georgia plants (whose operational future is uncertain).

- US demand is served largely by imports.

Stat: PHA holds 2.4% of global bioplastics production capacity in 2024 but is forecast to reach 17% by 2029 under the European Bioplastics base case. This forecast relies on aggressive capacity additions that are now in question following Danimer’s collapse. Investors should treat the 17% figure as a theoretical ceiling, not a probable outcome.

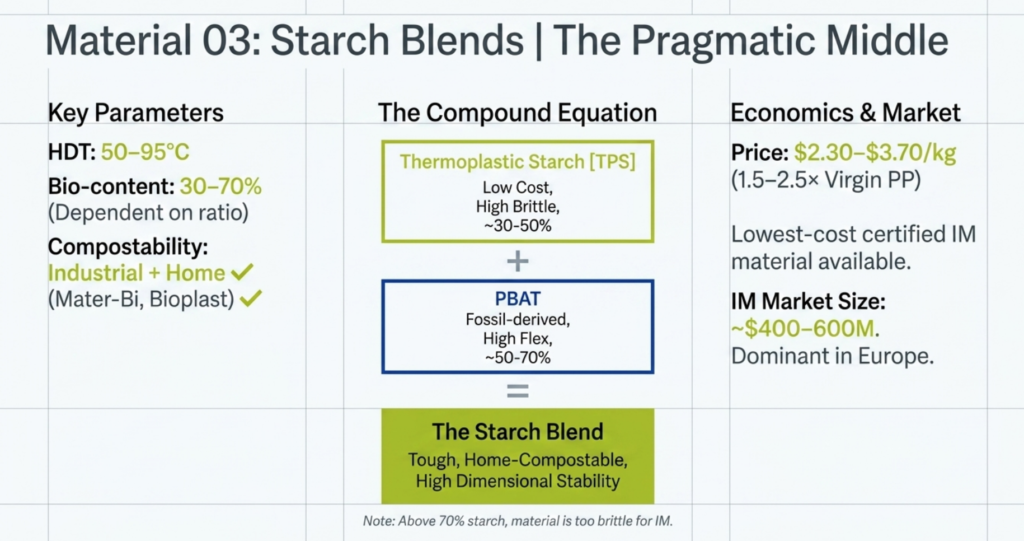

3.3 Starch Blends

3.3.1 What Are Starch Blends and What Are Their Properties

Starch blends are compounds made from thermoplastic starch (TPS) combined with a polyester, most commonly PBAT (polybutylene adipate terephthalate), sometimes PCL (polycaprolactone) or PLA.

Neither pure starch nor pure polyester alone performs adequately in injection moulding:

- starch without a polyester is too weak and brittle;

- PBAT without starch is too flexible.

The blend balances biodegradability, home-compostability, toughness, and processability.

Leading commercial brands for injection moulding:

- Novamont Mater-Bi (Italy): The category leader. Mater-Bi is a TPS/PBAT blend using Novamont’s proprietary Origo-Bi PBAT.

- Biotec Bioplast 900 (Germany): A plasticiser-free, GMO-free starch blend with 69% bio-based content. Marketed specifically for coffee capsule injection moulding with a claimed 5-second cycle time.

- Rodenburg Solanyl (Netherlands): Potato starch recovered from food-processing waste. Lower cost, more limited mechanical performance.

Key properties:

- Tensile strength: 18 to 35 MPa (lower than PLA, adequate for most cutlery and capsule applications)

- Tensile modulus: 0.7 to 2.5 GPa (broad range across starch:polyester ratios)

- Notched Izod impact: 4 to 20 kJ/m² (significantly tougher than PLA in flexible-leaning grades)

- HDT: 50 to 95°C depending on grade (Bioplast 900 targets resistance to boiling water; Mater-Bi rigid grades typically achieve 55 to 75°C)

- Starch content in injection grades: 30 to 50% starch with 50 to 70% polyester and additives. Above 70% starch, the material becomes too brittle for injection moulding and is limited to extrusion or compression moulding.

Compostability distinction: This is the category’s key commercial advantage over PLA. Most injection-grade starch blends carry both EN 13432 industrial compostability and home-compost certification, making them among the very few rigid moulded materials that can be placed in a household compost bin.

Known limitations: Surface bloom (plasticiser migration of glycerol or sorbitol to the surface, visible as a white haze), dimensional change in high-humidity environments, surface tackiness at elevated temperature, and limited HDT for hot-fill applications.

3.3.2 Starch Blend Cost: Price per kg vs PP and PS

Starch blend pricing vs conventional plastics:

| Material | Spot price 2025 (USD/kg) | Multiplier vs PP |

|---|---|---|

| Virgin PP | 1.00 to 1.50 | 1× |

| Virgin PS | 1.10 to 1.60 | ~1.1× |

| Starch blends (Mater-Bi, Bioplast injection grades) | 2.30 to 3.70 | 1.5 to 2.5× |

Starch blends are generally the lowest-cost certified-compostable injection material available, below PLA, PHA, and PBS. Industry trade pricing for Mater-Bi and Bioplast grades is not publicly listed, but is consistent with Mordor Europe Bioplastics data showing starch blends selling approximately 15% below PLA in comparable market segments.

Why starch blends are relatively cost-competitive:

- Starch (corn, potato, cassava) is an established commodity: low cost, stable supply

- Glycerol plasticiser is a near-zero-cost biodiesel by-product

- PBAT, the polyester component, has fallen sharply in price as Chinese capacity has expanded: from approximately $2,000/tonne in 2022 to approximately $1,400/tonne in 2025

PBAT’s impact on starch-blend pricing: Because PBAT constitutes 50 to 70% of most injection-grade starch blends, PBAT spot pricing is the dominant cost driver.

The fossil-content caveat: The cheapening of PBAT is good news for starch-blend cost competitiveness, but PBAT is 100% fossil-derived.

Processing cost premium vs PP: Minimal. Comparable cycle times and similar barrel temperatures mean energy costs are similar. The main additional cost is drying energy (approximately $0.02 to $0.05/kg). Scrap rates are slightly elevated in transition (4 to 6% vs 2 to 3% for PP) but reach PP-comparable levels once the process is dialled in.

3.3.3 Starch Blend Market Size: Global and Regional

Global starch-blend market size 2024: Approximately $1.5 to $1.8 billion. This figure refers to the starch-based bioplastics market including film, bag, and injection applications.

Starch-blend injection-moulding sub-market: Applying a 25 to 35% injection-moulded share (the balance is films, bags, and mulch), the starch-blend injection moulding market is approximately $400 to $600 million in 2024.

CAGR: 7 to 10%, reaching approximately $2.5 to $3.0 billion by 2030.

Regional split:

- Europe: The dominant consumption region, accounting for an estimated 45 to 55% of global starch-blend demand. Italy is the most advanced market. Germany is the second-largest market.

- Asia-Pacific: Growing fastest. China, Japan, and South Korea are the primary growth markets. Chinese domestic production of TPS compounds is expanding.

- North America: Demand is present but infrastructure-constrained. California’s SB 54, requiring 100% of single-use packaging to be recyclable or compostable by 2032, is the primary regulatory demand lever.

Stat: Starch-containing polymer compounds represented approximately 7.5% of global bioplastics installed capacity in 2024 per European Bioplastics data. This is forecast to fall to approximately 6.9% by 2029 as PLA and PHA grow faster in the capacity mix.

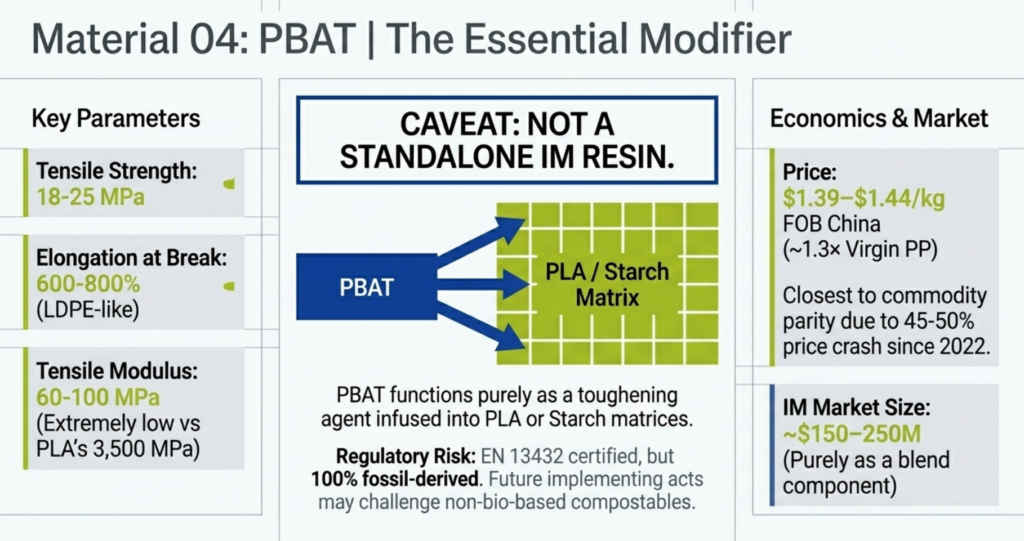

3.4 PBAT (Polybutylene Adipate Terephthalate)

3.4.1 What Is PBAT and What Are Its Properties

Polybutylene adipate terephthalate (PBAT) is a fossil-derived but certified-compostable polyester made from three petroleum-based monomers: 1,4-butanediol, adipic acid, and terephthalic acid (PTA). BASF commercialised it in 1998 under the ecoflex brand. It carries industrial compostability certification under EN 13432, ASTM D6400, and AS 4736. It does not pass home-compostability standards.

Caveat: PBAT is not really an injection-moulding resin in its own right. It is too flexible to stand alone in a rigid moulded part. In injection moulding, it functions almost exclusively as a toughening blend partner for PLA and starch blends, where it solves brittleness at the cost of adding a fossil-derived component.

Key properties (BASF ecoflex F Blend C1200):

- Tensile strength: 18 to 25 MPa

- Elongation at break: 600 to 800% (LDPE-like, very flexible)

- Tensile modulus: 60 to 100 MPa (far below PLA’s 3,500 MPa)

- Melt point: 110 to 115°C

- HDT: approximately 55°C

- MFR: 2.7 to 4.9 g/10 min at 190°C

The regulatory risk specific to PBAT deserves flagging. Despite EN 13432 certification, PBAT is 100% fossil-derived. As of mid-2026, no EU proposal formally excludes fossil-derived biodegradables from compostability certification, but NGO and policy pressure is building toward a “bio-based AND biodegradable” combined requirement.

3.4.2 PBAT Cost: Price per kg vs PP and PS

| Material | Spot price 2025 (USD/kg) | Multiplier vs PP |

|---|---|---|

| Virgin PP | 1.00 to 1.50 | 1× |

| PBAT (China FOB) | 1.39 to 1.44 | ~1.3× |

| PBAT (European CFR) | 1.83 to 2.00 | ~1.5 to 1.6× |

| ecovio IS compound | 2.50 to 3.50 | ~2.0 to 2.5× |

PBAT is the closest of all compostable polymers to commodity parity with PP.

Why PBAT is priced near PP: All three monomers are established petrochemical commodities. BDO, adipic acid, and PTA are all produced at large scale in China’s integrated chemical parks. Chinese PBAT prices fell from approximately $2,000/tonne in 2022 to $1,391 to $1,435/tonne by mid-2025, a decline of approximately 45 to 50%, driven by aggressive Chinese capacity expansion.

3.4.3 PBAT Market Size: Global and Regional

Global PBAT market size 2024: $1.5 to $1.8 billion.

CAGR of 9 to 13%, reaching approximately $2.8 to $3.0 billion by 2030.

PBAT in injection moulding specifically: Approximately 10 to 15% of total PBAT volume ends up in moulded applications, primarily as a blend component. The PBAT injection-moulding sub-market is approximately $150 to $250 million in 2024. The balance goes into mulch films, carrier bags, and organic-waste liners.

Regional split:

- China: Approximately 60 to 65% of global PBAT capacity.

- Europe: BASF (Schwarzheide and Ludwigshafen) is the only meaningful Western producer at approximately 74 kt/yr.

- North America: Minimal native production; predominantly import-served.

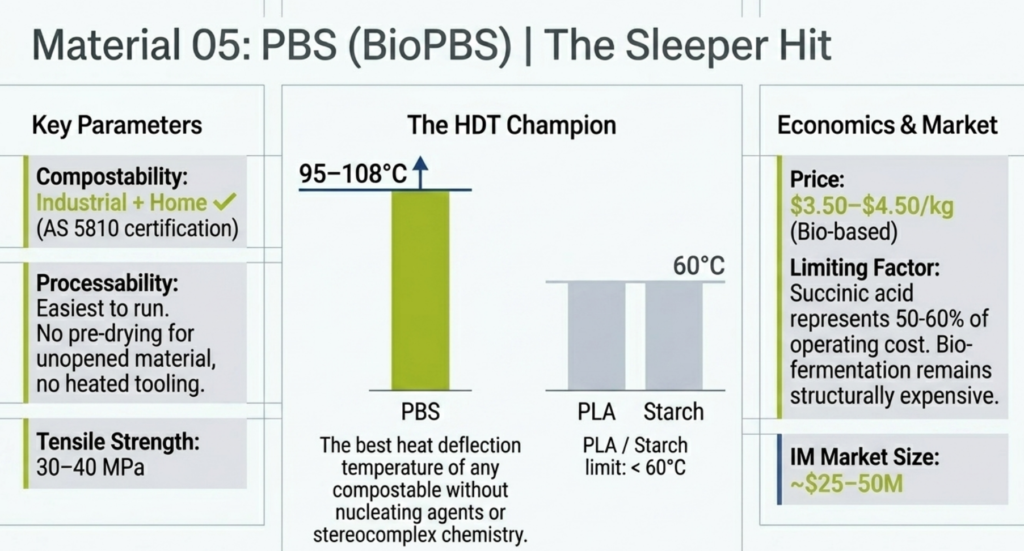

3.5 PBS (Polybutylene Succinate)

3.5.1 What Is PBS and What Are Its Properties

Polybutylene succinate (PBS) is a semi-crystalline aliphatic polyester made from 1,4-butanediol and succinic acid. Succinic acid can be petrochemically produced from maleic anhydride or bio-fermented from sugars.

PBS carries EN 13432, ASTM D6400, ISO 17088 certification and, for several BioPBS grades, AS 5810 home-compostability certification, which places it alongside PHA and starch blends as one of the few materials that can claim home-compostable status for injection-moulded parts.

Why PBS deserves more investor attention than it receives:

- HDT: 95 to 108°C for neat BioPBS injection grades — the best heat deflection temperature of any compostable polymer covered in this chapter without nucleating agents or stereocomplex chemistry

- Cycle time vs PP: Comparable, with PTT MCC literature explicitly positioning “short cycle time” as a BioPBS feature

- Processability: The easiest compostable injection material to run, with no heated tool requirement and no mandatory pre-drying for unopened material

- Home-compost certification: Certified under AS 5810, unlike standard PLA

Key properties (PTT MCC BioPBS FZ91PB injection grade):

- Tensile strength: 30 to 40 MPa

- Tensile modulus: 0.4 to 0.7 GPa (more flexible than PLA, stiffer than PBAT)

- Notched Izod impact: 5 to 20 kJ/m² (tough)

- Melting point: approximately 115°C

- HDT (0.45 MPa): 95 to 108°C

- MFR: 5 g/10 min at 190°C/2.16 kg

Known limitations: Higher price than PLA, constrained supply (PTT MCC BioPBS capacity is approximately 20 kt/yr globally), and secondary embrittlement after weeks of storage reported in some grades.

3.5.2 PBS Cost: Price per kg vs PP and PS

| Material | Spot price 2025 (USD/kg) | Multiplier vs PP |

|---|---|---|

| Virgin PP | 1.00 to 1.50 | 1× |

| BioPBS (PTT MCC, bio-based) | 3.50 to 4.50 | 2.5 to 3.5× |

| Petrochemical PBS (Chinese producers) | 2.50 to 3.50 | 2.0 to 2.5× |

Why is PBS more expensive than PLA despite lower production scale?

- The dominant cost driver is succinic acid (50 to 60% of operating cost).

- Bio-succinic acid from fermentation has been structurally more expensive than petrochemical succinic acid at every commercial attempt to date, which is why every bio-succinic acid scale-up venture has either failed or stalled.

Petrochemical PBS from China is approaching $2.50/kg at scale, closing toward commodity territory. However, fossil-derived PBS faces the same regulatory headwind as PBAT: it is certified compostable but not bio-based, which may be challenged in future PPWR (Europe) implementing acts.

3.5.3 PBS Market Size: Global and Regional

Global PBS market size 2024: Approximately $130 to $180 million on a neat-resin basis. The $128.6 million figure at 7.6% CAGR from OMR Global is the most defensible anchor and is consistent with Global Market Insights ($115 million for 2023 growing at 12.2% CAGR).

PBS market forecast: $250 to $400 million by 2030 at the 8 to 12% CAGR consensus. Upside risk if Chinese petrochemical PBS expands volume and PTT MCC executes its planned doubling to 40 kt/yr.

PBS injection-moulding sub-market: Approximately $25 to $50 million in 2024.

Regional split:

- Asia-Pacific: Production-dominated. PTT MCC Biochem in Thailand supplies the global bio-PBS market. Xinjiang Blue Ridge Tunhe reportedly holds up to 120 kt/yr of PBS capacity in China, the largest single asset globally.

- Europe: Strong latent demand, no native production. BioPBS imports from Thailand serve premium foodservice accounts.

- North America: Small but growing. US market demand is import-served. California SB 54’s compostable-or-recyclable requirement by 2032 could accelerate PBS specification for hot-fill containers.

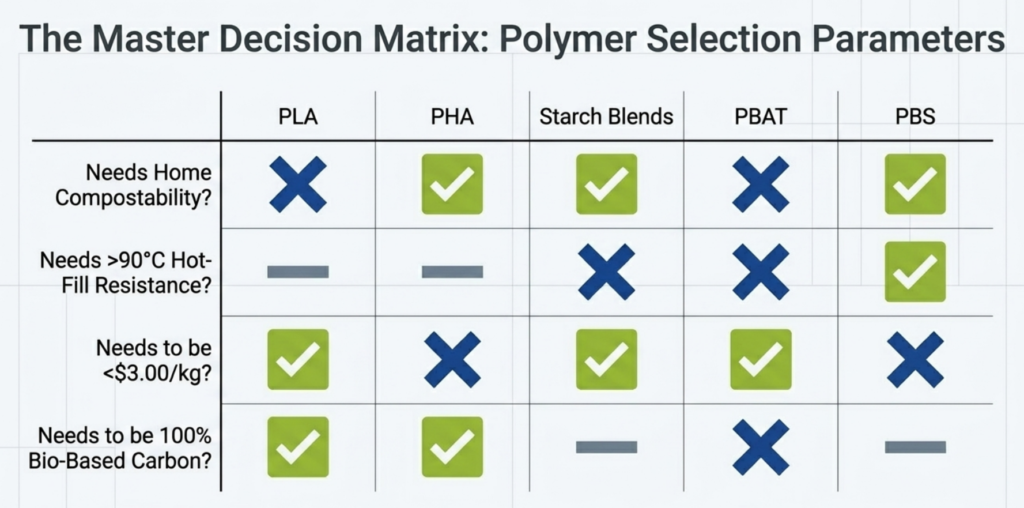

Compostable Plastics for Injection Molding – Cross-Material Comparison

Table 1: Material Properties and Processing Comparison

| Property | PLA | PHA | Starch Blends | PBAT | PBS |

|---|---|---|---|---|---|

| Bio-based content | ~100% | 100% | 30 to 70% | 0% | 0 to 99% |

| EN 13432 certified | Yes | Yes | Yes | Yes | Yes |

| Home-compostable | No | Yes | Yes | No | Yes |

| Marine biodegradable | No | Yes | No | No | No |

| Tensile strength | 60–70 MPa | 20–30 MPa | 18–35 MPa | 18–25 MPa | 30–40 MPa |

| Flexural modulus | 3.6–4.0 GPa | 0.5–1.5 GPa | 0.7–2.5 GPa | 0.06–0.10 GPa | 0.4–0.7 GPa |

| HDT (standard) | 55°C | 80–110°C | 50–75°C | ~55°C | 95–108°C |

| Impact toughness | Low | Medium | Medium–High | Very high | Medium |

| Moisture sensitivity | High | High | Very high | Moderate | Low |

| Cycle time vs PP | 20–50% longer | Comparable | Comparable | Comparable | Comparable |

| Standalone IM use | Yes | Yes | Yes | No | Yes |

Table 2: Cost Comparison Against Conventional Plastics

| Material | Price (USD/kg) | vs PP | vs PS | vs PET |

|---|---|---|---|---|

| Virgin PP | 1.00–1.50 | Baseline | ~1× | ~1× |

| PLA | 2.40–3.30 | 2–2.5× | ~2× | ~2.5× |

| PHA | 4.00–6.00 | 3.5–5× | ~4× | ~5× |

| Starch blends | 2.30–3.70 | 1.5–2.5× | ~2× | ~2.8× |

| PBAT | 1.39–2.00 | 1.2–1.6× | ~1.4× | ~1.6× |

| PBS | 3.50–4.50 | 2.5–3.5× | ~3× | ~3.5× |

Table 3: Global Market Size Summary by Material (2024–2030)

| Material | 2024 Market | CAGR | 2030 Market | IM Sub-market 2024 |

|---|---|---|---|---|

| PLA | $2.0 bn | 15–18% | $4.0–4.5 bn | $300–400 m |

| PHA | $100–150 m | 10–18% | $250–400 m | $25–50 m |

| Starch blends | $1.5–1.8 bn | 7–10% | $2.5–3.0 bn | $400–600 m |

| PBAT | $1.5–1.8 bn | 9–13% | $2.8–3.0 bn | $150–250 m |

| PBS | $130–180 m | 8–12% | $250–400 m | $25–50 m |

4. Compostable Plastics for Injection Moulding – Demand Drivers and Regulatory Landscape

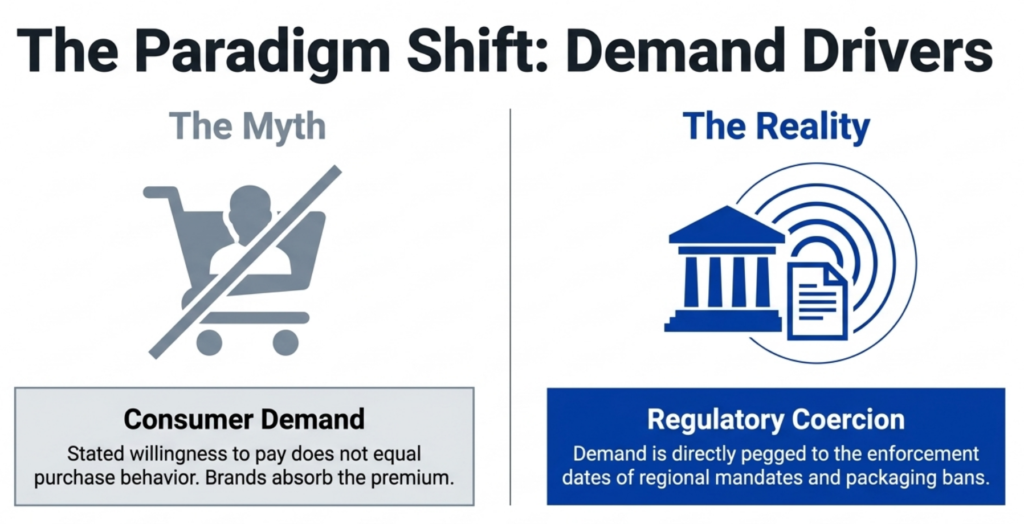

Demand for compostable formats in injection-moulded categories is coming from two directions: brand owners responding to regulatory pressure, and a smaller but growing body of consumers willing to pay a premium for certified sustainable packaging. Of the two, regulation is the more reliable and durable signal.

This chapter covers both, starting with the commercial picture and then mapping the regulatory architecture that sits behind it.

Compostable Plastics for Injection Moulding – Demand Drivers

Brand-Owner Adoption: Where Compostable Volume Is Actually Moving

Single-serve coffee capsule

The clearest brand-owner pull into injection-moulded compostable formats today is in the single-serve coffee capsule category.

Nespresso (Nestlé) launched a paper-based home-compostable Original capsule in spring 2023, TÜV Austria-certified for both industrial and home composting.

Lavazza launched its 100% industrially compostable Eco Caps (EN 13432) in 2019 and has progressively replaced its A Modo Mio home-use range.

Italian producers Covim and Flo supply fully bio-based, industrially compostable capsules using BASF’s ecovio IS injection-moulding compound.

Foodservice

In foodservice, European operators have moved further than North American chains, driven by the SUPD and national plastic levies.

At the QSR level, Starbucks and McDonald’s co-funded the NextGen Cup Consortium in 2018 with a combined $10 million to develop compostable and recyclable cup-and-lid solutions.

Adoption has been uneven: fibre lids have been rolled out in select markets but also pulled back where composting infrastructure does not support the end-of-life claim.

Retail

Companies using compostable packaging at retailer level include Carrefour, Tesco, Waitrose, Aldi (UK/Ireland) and Migros. All of them are aligned with Italian and French fruit-and-vegetable packaging requirements. TIPA (Israel) supplies compostable flexible packaging to Waitrose, Woolworths, Pangaia and Riverford. Its November 2025 acquisition of Sealpap, a rigid-packaging specialist, signals an intention to extend into compostable closures and rigid formats.

Consumer Willingness to Pay

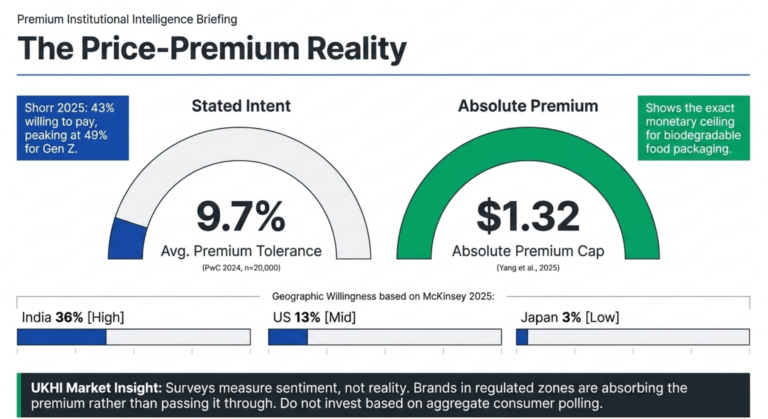

Consumer research consistently shows stated willingness to pay for sustainable packaging, though the gap between stated preference and actual purchase behaviour is well documented. The most useful data points for investors are:

- PwC 2024 Voice of the Consumer Survey (n=20,000, 31 countries): 80% of consumers say they will pay more for sustainably produced goods, with an average stated premium tolerance of 9.7%.

- McKinsey 2025 Global Packaging Survey (n=11,000, 11 countries): willingness to pay significantly more is highest in India (36%) and lowest in Japan (3%); the US sits at 13%.

- Shorr Packaging 2025 Consumer Report (n=2,016 US): 43% willing to pay extra for sustainable packaging, rising to 49% among Gen Z and 47% among Millennials.

- A 2025 peer-reviewed choice-experiment study (Yang et al., Journal of Agricultural and Applied Economics Association) found that consumers placed a $1.32 average premium on biodegradable food packaging over conventional alternatives, rising by a further $0.50 when supporting information about biodegradability was provided.

Stated willingness to pay does not reliably predict purchase behaviour, and most brands absorb the compostable-resin premium rather than passing it to consumers. For investment purposes, procurement commitments from brand owners in mandated categories are a more bankable signal than aggregate survey data on consumer intentions.

The Regulatory Landscape for Compostable Packaging

The EU

Packaging and Packaging Waste Regulation (PPWR)

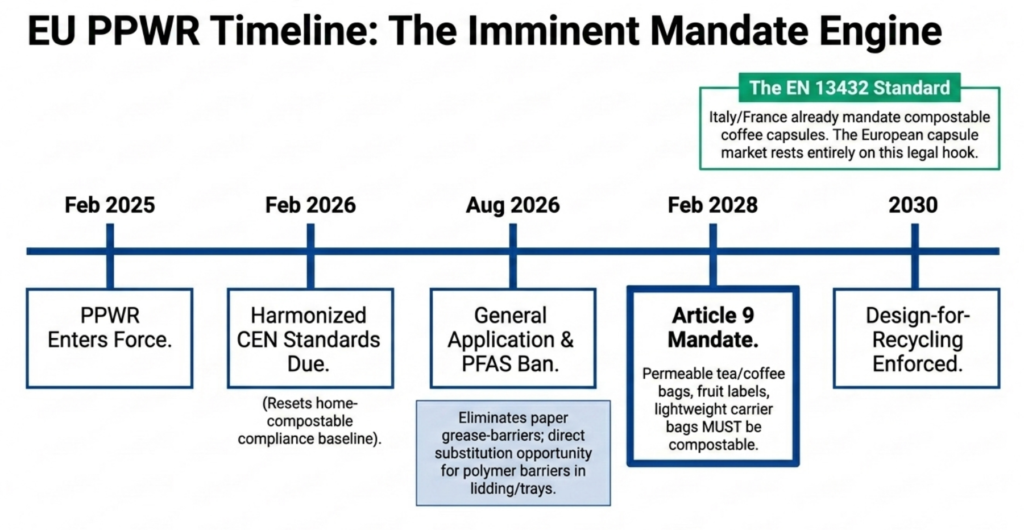

The most consequential piece of EU packaging regulation for this market is Regulation (EU) 2025/40, the Packaging and Packaging Waste Regulation (PPWR).

Published in January 2025, it entered force in February 2025 and applies from 12 August 2026.

As a regulation rather than a directive, it is directly enforceable across all 27 EU member states without national transposition and aims to eliminate the compliance patchwork that previously fragmented the European market.

Definition: Under PPWR, compostability is not a default compliance route. All packaging must be recyclable unless it falls within a defined category where composting is the more appropriate end-of-life route.

The mandatory compostable categories, under Article 9, apply from 12 February 2028 (an 18-month derogation beyond the general application date):

- Permeable tea and coffee bags and single-serve units designed to be disposed of with the product

- Sticky labels on fruit and vegetables

- Very lightweight plastic carrier bags, where required by member states

Member states may also mandate compostability for non-metal coffee capsules, lightweight carrier bags, and any packaging category already required to be compostable under pre-existing national law.

Italy and France had such rules before August 2026 and can maintain and extend them. This is the legal hook on which the European compostable coffee capsule market rests.

Compostability Standards and Certification in the EU

The operative compostable packaging certification standard in the EU is EN 13432, which specifies industrial compostability requirements: full disintegration within 12 weeks and biodegradation above 90% within 6 months under controlled conditions.

Products are certified against this standard by TÜV Austria (OK compost INDUSTRIAL and OK compost HOME marks) or DIN CERTCO.

The European Commission has mandated CEN to develop updated harmonized standards by February 2026, which will reset the compliance baseline, particularly for home compostable packaging standards.

The Single-Use Plastics Directive (SUPD) and Its Limits for Injection Moulding

The Single-Use Plastics Directive (SUPD), in force since July 2021, bans single-use plastic cutlery, plates, straws, stirrers and expanded polystyrene food containers.

Compostable plastics are not exempt from these bans. This eliminates the largest traditional injection-moulded categories from EU foodservice.

What remains open is: coffee capsules, rigid food-contact lids, trays and closures that enter the biowaste stream, and fruit-sticker carrier systems.

Insight: PPWR also restricts PFAS in food-contact packaging from August 2026, removing fluorinated grease-barrier coatings from paper products. This creates a direct substitution opportunity for compostable polymer barriers in lidding and tray applications.

USA

USA

EPR Packaging Laws: US (State-by-State)

There is no federal packaging mandate in the United States.

Five states have enacted Extended Producer Responsibility (EPR) laws for packaging: Maine, Oregon, Colorado, California and Minnesota. Washington followed in 2025.

EPR schemes work by requiring companies that sell packaged goods to register with a Producer Responsibility Organisation (PRO) and pay fees based on the volume and type of packaging they place on the market.

Oregon began collecting fees in July 2025, making it the first US state to operationalise the programme. Colorado followed in January 2026.

California SB 54 is the most consequential US state law for this market. It requires all single-use packaging and plastic foodservice ware sold in California to be either recyclable or compostable by 2032, with the following interim milestones:

- 10% plastic reduction by 2027

- 20% by 2030

- 25% by 2032

- 65% plastic recycling rate by 2032

California’s EPR fee structure is designed to reward better-performing packaging with lower fees — a mechanism called eco-modulation. Under this approach, compostable packaging qualifies for reduced fees, but only in markets where industrial composting facilities that accept the material are actually accessible to consumers. In most parts of the US today, that condition is not met, which limits the practical fee benefit.

California’s AB 1201 governs what products can be labelled “compostable” in the state. For a product to carry that claim, it must be processable in commercial composting facilities that are reasonably accessible to the consumers buying it. This is a high bar: most US composting facilities do not accept compostable plastics, particularly rigid items like cutlery and capsules. Governor Newsom directed CalRecycle to restart the rulemaking process in March 2025, introducing some timing uncertainty into implementation, but the statutory requirements of SB 54 remain in force.

All five state programmes recognise compostable packaging as a legitimate compliance pathway alongside recyclable packaging. None of them replicates the PPWR’s approach of mandating compostable formats for specific product categories. The practical result for brand owners is financial incentive rather than legal obligation: compostable packaging may attract lower EPR fees and count toward recyclable-or-compostable targets, but choosing conventional packaging does not yet put a company in breach of US law the way it will in the EU from 2028.

India

India’s plastic ban came into force 1 July 2022 under the Plastic Waste Management Rules. It banned 19 categories of single-use plastics including cutlery, plates, straws and stirrers.

Certified compostable alternatives are explicitly exempt, provided they meet Indian Standard IS/ISO 17088 and have been manufactured by someone duly certified by the Central Pollution Control Board (CPCB).

As of the latest CPCB data, 201 manufacturers hold this certification.

For injection-moulded compostable products, India represents one of the clearest near-term volume opportunities in Asia: there is an active ban, a formal exemption for certified alternatives, and a growing domestic manufacturing base. The missing piece is composting infrastructure, which remains at a very early stage.

China

China’s regulatory framework on plastic pollution is anchored in the January 2020 policy guidance from the National Development and Reform Commission (NDRC) and the Ministry of Ecology and Environment (MEE), followed by implementation targets under the 14th Five-Year Plan. Its targets are:

- A 30% reduction in non-biodegradable single-use tableware in prefecture-level city foodservice by 2025

- A phase-out of non-biodegradable plastic bags and non-degradable straws in major cities

- A complete phase-out of non-biodegradable plastic packaging in postal and express delivery

Hainan Province operates the most stringent regional regime, with comprehensive plastic-substitute mandates in force. However, Beijing’s policy appetite for biodegradable plastics has cooled since the initial 2020 surge. The 14th Five-Year Plan’s plastic-pollution annex called for further research and evaluation before extending mandates, and raised questions about the environmental credentials of some biodegradable materials when composting infrastructure does not exist.

Investors should treat Chinese biodegradable plastics demand forecasts with caution: announced capacity has significantly outrun both policy-driven demand and actual composting capacity.

Elsewhere in Asia-Pacific

Australia permits certified compostable alternatives to banned single-use plastics under AS 4736 (industrial composting) or AS 5810 (home composting) in Western Australia, South Australia and Queensland, where state-level single-use bans are in force.

South Korea has enforced a ban on single-use plastic cups and straws in cafes and restaurants since 2022, with compostable certified alternatives permitted.

Indonesia, Thailand and Vietnam have each introduced plastic restrictions, but these are city-level or sector-specific rather than national mandates, and composting infrastructure is limited across all three markets.

5. Compostable Plastics for Injection Molding – Competitive Landscape & Investment Activity

Compostable Plastics for Injection Molding: Supply Chain

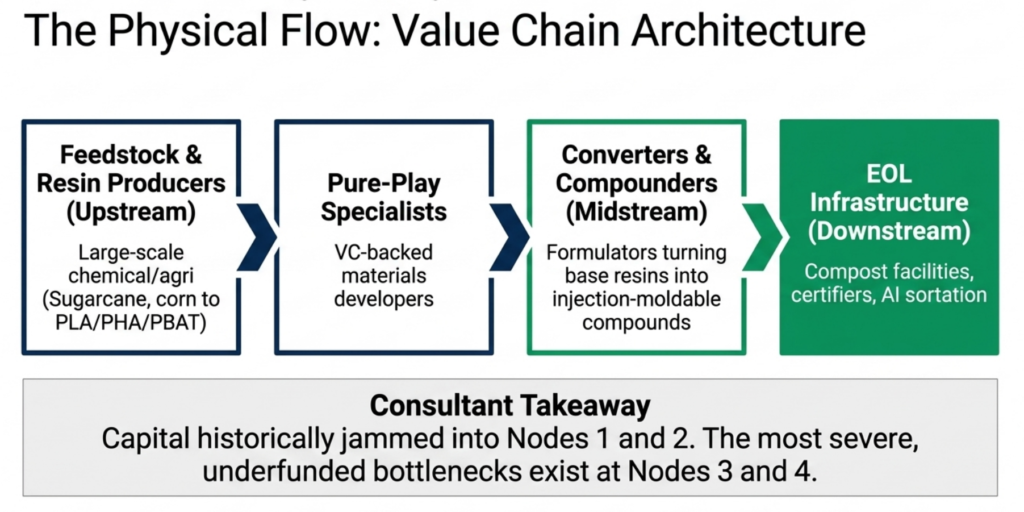

The compostable plastics supply chain starts with agricultural feedstock — sugarcane, corn, cassava, plant oils — and runs through resin production, compounding, and conversion into finished injection-moulded goods. Four distinct types of business operate across it, with very different risk and return profiles:

- Integrated resin producers: large-scale chemical or agri-industrial companies producing PLA, PHA, PBAT or starch-blend polymers

- Pure-play specialists: VC-backed or grant-funded companies developing compostable materials or finished products, typically at smaller scale

- Converters and compounders: mid-chain operators who formulate base resins into injection-mouldable compounds or finished goods

- Infrastructure and enabling technology players: composting facility operators, certification bodies, digital sortation technology companies

Investment to date has been heavily weighted toward resin producers and pure-play specialists. Compounding, infrastructure, and end-of-life technology are the underserved positions.

Compostable Plastics for Injection Molding – Key Players

Integrated Resin Producers

NatureWorks

NatureWorks (Plymouth, Minnesota) is the global PLA market leader, jointly owned by Cargill and PTT Global Chemical. It operates a 150,000 t/yr Ingeo PLA plant in Blair, Nebraska and is ramping up a new 75,000 t/yr fully integrated facility in Nakhon Sawan, Thailand, funded in part by a $350 million green loan from Krungthai Bank.

TotalEnergies Corbion

TotalEnergies Corbion (Netherlands, 50/50 JV between TotalEnergies and Corbion) produces Luminy PLA at a 75,000 t/yr plant in Rayong, Thailand, which reached nameplate capacity in 2022. Its high-heat PDLA grades are among the few commercially available PLA formulations suited to demanding injection-moulded applications.

Novamont

Novamont (Novara, Italy) produces the Mater-Bi family of starch-polyester compostable blends, which are the dominant material in European compostable cutlery and carrier bags. It was fully acquired by Versalis, the chemicals subsidiary of Eni, in October 2023, giving one of the world’s largest energy companies direct ownership of Europe’s leading compostable polymer brand.

BASF

BASF (Ludwigshafen) produces ecoflex, a certified-compostable fossil-derived polyester, and ecovio, which blends ecoflex with PLA to create an injection-mouldable compound. ecovio IS grades are used in compostable coffee capsules, cutlery and food-contact lids, and BASF is currently the primary resin supplier to the European compostable capsule market.

Other producers

Other producers with relevant positions include Mitsubishi Chemical (BioPBS, approximately 20,000 t/yr bio-based PBS in Thailand), Hisun Biomaterials (Zhejiang, China, PLA), Kingfa (China, PLA and PBAT compounds) and Anhui BBCA Biochemical (PLA, expanding capacity).

Pure-Play Specialists

Danimer Scientific

Danimer Scientific (US) was the world’s leading commercial PHA producer until it filed for Chapter 11 in March 2025, having accumulated $402 million in debt against revenues that never reached the level needed to service it. Teknor Apex, a private US compounder, acquired its Kentucky production facility and 480+ patents for $19 million in July 2025 — the most-cited cautionary data point in compostable plastics investment today.

Biome Bioplastics

Biome Bioplastics (Southampton, UK), a subsidiary of Biome Technologies plc, is an R&D-stage business developing compostable materials for capsule, film and packaging applications, funded primarily through Innovate UK grants and a C$1.5 million joint development with Renaissance BioScience announced in November 2025.

TIPA

TIPA (Israel) develops certified compostable flexible films and laminates for food and fashion packaging, with accounts including Waitrose, Woolworths and Pangaia. Total funding raised is approximately $121 million; its November 2025 acquisition of rigid-packaging specialist Sealpap extends its offer into compostable closures.

Cove

Cove (US) produced PHA-based water bottles using Danimer’s Nodax resin. Its supply chain was disrupted by Danimer’s bankruptcy and commercial activity has been minimal through 2025, making it a clear example of the risks of single-supplier dependency in early-stage PHA downstream businesses.

Emerging Asian PLA and PHA Producers

Chinese producers including Hisun Biomaterials, BBCA Biochemical, Wanhua Chemical, Kingfa and COFCO have announced PLA and PBAT capacity in the 30,000 to 75,000 t/yr range per plant, with aggregate announced capacity exceeding one million tonnes per year combined. Actual utilisation is materially lower: China’s policy enthusiasm for biodegradable plastics has cooled since 2022, and domestic demand has not grown fast enough to absorb the capacity that has been built.

Ukhi (India)

Ukhi (India) is a compostable biopolymer compounder supplying EcoGran™ injection-moulding compounds certified to ISO 17088, EN 13432 and ASTM D6400. Its compounds are formulated from Indian agricultural residues and are designed to run on standard PP and ABS processing lines without retooling, targeting the conversion layer of the supply chain rather than primary resin manufacturing. Ukhi also supplies blown film, profile extrusion, cast film, and extrusion coating resins, as well as custom bio-granule formulations, positioning it as a broad-line compostable compounder serving the Indian and export markets.

Compostable Packaging for Injection Molding – Recent Funding, M&A and Capacity Expansions

The significant transactions and capacity commitments of 2022 to 2025 are summarised below.

| Transaction | Date | Value | What happened |

|---|---|---|---|

| TIPA Series C | January 2022 | $70 million | Compostable flexible packaging; led by Millennium Food-Tech and Meitav Dash. Total raised across six rounds: approximately $121 million. |

| Versalis (Eni) acquires Novamont | October 2023 | Undisclosed | Eni’s chemicals arm purchased the remaining 64% of Novamont, consolidating Europe’s leading compostable starch-blend producer. |

| NatureWorks Thailand | Ongoing; green loan May 2024 | >$600 million total | 75,000 t/yr integrated PLA facility; $350 million green loan from Krungthai Bank; full production targeted 2025 to 2026. |

| Emirates Biotech / Sulzer, UAE | Technology licence December 2024; equipment contract May 2025 | ~$800 million total | 160,000 t/yr PLA facility in two phases at KEZAD, Abu Dhabi. Sulzer Chemtech is the technology licensor; Samsung E&A is EPC contractor. Phase 1 commissioning targeted early 2028. Would be the world’s largest single PLA site. |

| Ukhi, India | December 2024 | $1.2 million (pre-seed) | Pre-seed round led by 100Unicorns, with participation from Venture Catalysts and angel investor Avtar Monga, plus debt financing from SIDBI (Small Industries Development Bank of India). |

| Balrampur Chini Mills, India | Announced 2025; capex revised 2025 | ~$370 million | 80,000 t/yr PLA plant at Kumbhi, Uttar Pradesh using local sugarcane. India’s first industrial-scale PLA facility; commercial production target December 2027. |

| Teknor Apex acquires Danimer Scientific | July 2025 | $19 million | Distressed acquisition out of Chapter 11. Assets include the Winchester, Kentucky PHA facility, a laboratory and pilot plant in Bainbridge, Georgia, and 480+ patents across 20+ countries. |