Bioplastics Opportunity Index Explorer

Browse, sort and compare 25 countries ranked by the commercial opportunity their single-use plastic bans create for bioplastics.

| Rank ↑ | Country | Region | P1 | P2 | P3 | Score |

|---|

Prepared by

Ukhi Research Division

Ukhi Bioplastics Private Limited

India

Report Highlights

- • A country-by-country ranking of where single-use plastic bans are creating the biggest commercial opportunities for bioplastics.

- • Assessments of 25 markets across 4 regions: Asia-Pacific, Europe, the Americas, the Middle East and Africa.

- • Explanation of how SUP bans work in practice globally — including direct bans, fiscal measures, EPR systems, phased rollouts, and voluntary models — and where the gap between regulation and reality is widest.

- • An analysis of where bans are genuinely creating bioplastics demand through compostable exemptions, structural recycling shortfalls, fiscal tipping points, feedstock advantages, and the EU’s 2026 PPWR harmonisation.

- • Strategic implications for bioplastics companies and investors, covering volume versus value market selection, feedstock positioning, fiscal forcing events, and policy reversal risk.

Publication Details

Publication Date: April 2026

Publisher: Ukhi Bioplastics Private Limited

Location: New Delhi, India

Report Period Covered: Regulatory and market data current as of Q1 2026

Data Last Updated: 23rd April, 2026

Countries Covered: 25 countries across 4 regions (Asia-Pacific, Europe, Americas, Middle East, Africa & Oceania)

Disclaimer

This report is based on data and information available from government gazettes, national environmental agencies, legislative databases, peer-reviewed research, credible industry sources (European Bioplastics, OECD, UNEP, World Bank), and verified trade publications as of March 2026.

Enforcement assessments draw on reported evidence including government compliance data, investigative journalism, and NGO assessments and involve informed judgment where hard data is unavailable.

While every effort has been made to ensure accuracy, Ukhi does not guarantee completeness in cases where official data is unpublished, inconsistent across sources, or unavailable for specific countries.

Scoring methodology is fully disclosed in the report and readers are invited to scrutinize individual country scores against the stated criteria. This report prioritizes factual integrity and transparency over speculative modelling.

Executive Summary

This report ranks 25 countries by the commercial opportunity their single-use plastic bans create for bioplastics — based on regulatory strength, enforcement reality, and the gap between plastic being removed and bioplastic supply available to replace it.

The Global SUP Ban-linked Bioplastics Opportunity Index 2026: Full Rankings

The Bioplastics Opportunity Index: At a Glance

The top 10 and bottom 5 countries from our full 25-country ranking:

🔺 Top 10 Markets

| Rank | Country | Region | Composite Score |

|---|---|---|---|

| 1 | France | Europe | 12.7 / 15 |

| 2 | Italy | Europe | 12.3 / 15 |

| 3 | India | Asia-Pacific | 11.0 / 15 |

| 4 | Germany | Europe | 11.0 / 15 |

| 5 | Indonesia | Asia-Pacific | 10.7 / 15 |

| 6 | Spain | Europe | 10.3 / 15 |

| 7 | UAE | MEAO | 10.3 / 15 |

| 8 | Australia | MEAO | 10.0 / 15 |

| 9 | United Kingdom | Europe | 9.7 / 15 |

| 10 | Colombia | Americas | 9.5 / 15 |

🔻 Bottom 5 Markets

| Rank | Country | Region | Composite Score |

|---|---|---|---|

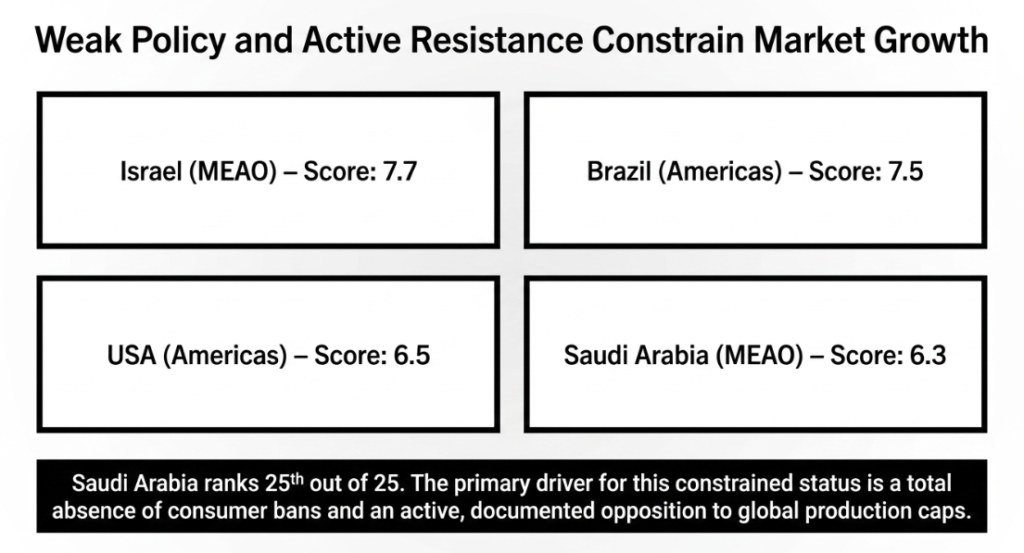

| 21 | Kenya | MEAO | 8.0 / 15 |

| 22 | Israel | MEAO | 7.7 / 15 |

| 23 | Brazil | Americas | 7.5 / 15 |

| 24 | USA | Americas | 6.5 / 15 |

| 25 | Saudi Arabia | MEAO | 6.3 / 15 |

The full 25-country ranking with pillar-level scores appears in Section 3.

Key Findings

1. Regulation and opportunity are inversely correlated in the countries that matter most

France has the world’s strongest SUP legislation but a moderate opportunity gap because European bioplastics suppliers already serve the market. India has the world’s largest unmet demand (Pillar 3: 5.0) but weak enforcement (Pillar 2: 2.0) limits the addressable market to the formal sector. So, the countries with the best regulation are not always the countries with the biggest supply gaps. This means bioplastics companies must choose: enter well-regulated, competitive markets, or target under-served markets where enforcement is the binding constraint.

2. Italy’s position as Europe’s #1 bioplastics market is under direct legal threat

Italy ranks second globally because of a unique compostable exemption that allows certified bioplastic cutlery, plates and cups to replace banned plastic equivalents, which creates 40-50% of EU bioplastics demand. The European Commission issued a formal infringement notice in July 2024 challenging this exemption. If Italy is forced to remove it, the foundation of a €704 million market could erode. The EU PPWR’s August 2026 application date is the likely resolution deadline. Any investment thesis built on Italian bioplastics demand must account for this risk.

3. Taxes and EPR fees are more reliable demand drivers than bans

The UK’s combined regulatory cost burden on virgin plastic packaging (~£650/tonne from pEPR and Plastic Packaging Tax) is creating stronger demand pull for alternatives than many countries with outright bans but weak enforcement. Spain’s €0.45/kg plastic tax and Colombia’s 17% IPUSUI surcharge work similarly. Fiscal mechanisms work through the tax system, which is harder to evade than a product ban. India’s escalating EPR targets through 2028-29 (60% recycled content for rigid packaging) will likely drive more volume bioplastics demand than the 2022 item ban itself.

4. Three forcing events will reshape the market before 2028

- • EU PPWR — August 2026. Harmonises SUP bans across 27 member states (450 million consumers), resolves the Italy exemption question, and transforms Europe from 27 separate regulatory stories into one market.

- • Emirates Biotech PLA plant — early 2028. At 160,000 TPA, the world’s largest single-site PLA facility. Reshapes Middle Eastern and African supply chains. Both a threat to current exporters and an opportunity for downstream converters.

- • India EPR recycled-content deadline — 2028-29. Forces every major FMCG brand, retailer and e-commerce company in India to restructure packaging procurement. This is where India’s volume bioplastics demand will actually materialize.

5. Policy reversal is a real and underpriced risk

This report documents regulatory reversals or significant pauses in six countries:

- • Israel (utensil tax repeal)

- • South Korea (cup ban withdrawal)

- • Netherlands (enforcement pause)

- • Saudi Arabia (partial oxo-degradable mandate suspension)

- • Kenya (EPR judicially suspended)

- • the USA (federal policy reversal via executive order)

These follow a common pattern of political backlash when bans impose visible costs on consumers or specific communities. Any market where bioplastics demand depends on a single regulatory provision carries concentration risk. The most resilient opportunities are in markets with multiple, reinforcing regulatory layers — like India (ban + EPR + traceability + recycled content mandates) or France (AGEC + EPR + PPWR).

About This Report

This report ranks 25 countries by the commercial opportunity their single-use plastic bans create for bioplastics companies, exporters and investors.

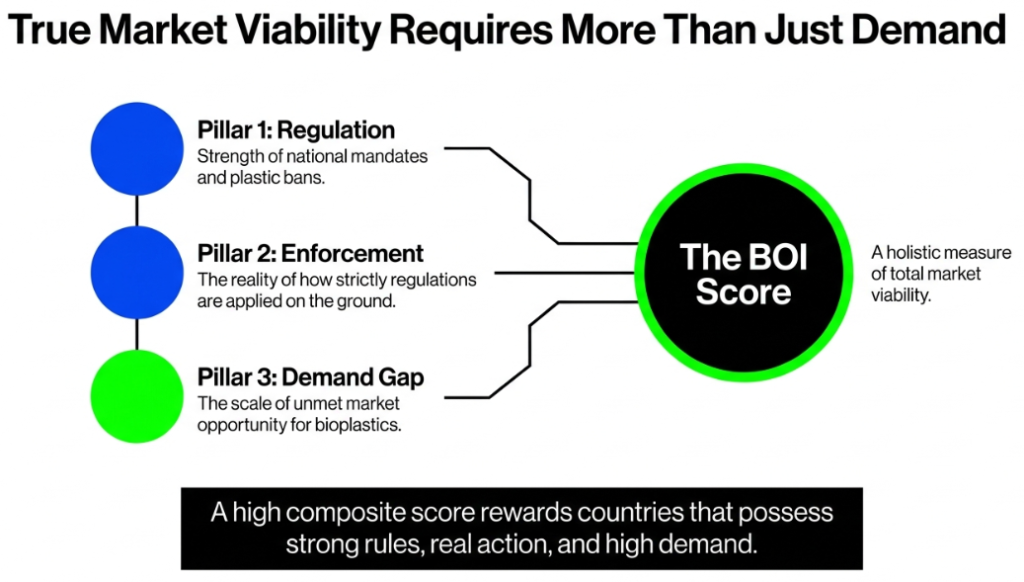

To make this ranking rigorous and comparable, we developed the Bioplastics Opportunity Index (BOI) — a composite scoring framework that rates each country across three dimensions: how strong its SUP regulation is, whether that regulation is actually enforced, and how large the unmet demand for bioplastic alternatives is.

Every country in this report is scored on the same scale, using the same criteria, so readers can compare any two markets at a glance. The methodology is fully disclosed in the next section and readers are invited to scrutinise individual scores against the stated criteria.

The report is published by Ukhi as a strategic reference for anyone evaluating where to sell, manufacture, invest in, or source bioplastics.

That includes:

- • bioplastics entrepreneurs,

- • packaging companies exploring material switches,

- • investors scanning the sector for geographic tailwinds,

- • sustainability consultants advising corporates on compliance,

- • policy researchers studying the plastics-to-bioplastics transition,

- • and trade bodies helping companies identify export markets.

All data is current as of Q1 2026 unless otherwise noted.

Regulatory information reflects enacted legislation and published enforcement data and disregards proposed bills, draft rules or announced intentions unless explicitly flagged.

How We Selected the 25 Countries In Scope For This Report

We considered four criteria:

- •

Regulatory action. The country must have enacted legislation restricting or banning single-use plastics, or imposing EPR/fiscal obligations on plastic packaging. - •

Market scale. The country must have a meaningful plastic consumption volume. - •

Regional representation. The report is positioned as a global index. It covers every major geography. We ensured no region was left out and that each region contains enough countries to show meaningful internal variation. - •

Diversity of regulatory approach. We deliberately included countries that use different regulatory tools such as outright bans (India, France, Kenya), fiscal measures (Spain, UK, Colombia), EPR-led systems (Australia, South Africa, California within the USA), voluntary models (Japan), and hybrid approaches (Germany, Canada).

The result is 25 countries across four regions:

- • Asia-Pacific (6): India, China, Indonesia, Japan, South Korea, Thailand

- • Europe (8): France, Germany, UK, Italy, Spain, Netherlands, Sweden, Denmark

- • Americas (5): USA, Canada, Brazil, Mexico, Colombia

- • Middle East, Africa & Oceania (6): Australia, Israel, UAE, Saudi Arabia, Kenya, South Africa

How the Bioplastics Opportunity Index (BOI) Works

The BOI measures one thing: how attractive is this country as a market for bioplastics, given its SUP regulation, enforcement and supply gap?

To do this, we rate each country on three criteria:

Pillar 1 — Regulatory Strength.

Pillar 2 — Enforcement Reality.

Pillar 3 — Market Opportunity Gap.

We score each country on a scale of 1 to 5 for each criteria, and then arrive at a composite score out of 15.

The index then ranks the countries.

The three criteria are explained here:

Pillar 1 — Regulatory Strength

This measures how strong and forward-looking the country’s SUP regulation is. Because regulation has multiple dimensions, this pillar is itself the average of three sub-scores:

1A — Legal Framework Robustness.

Does comprehensive legislation exist? Are penalties meaningful? Is there a clear enforcing body? A score of 1 means no formal legislation. A score of 5 means world-leading regulatory architecture.

1B — Ban Breadth.

How many product categories are actually banned? A score of 1 means only one category (usually bags). A score of 5 means virtually all SUP categories are covered including packaging.

1C — Future Trajectory.

Where is the regulation heading? A score of 1 means static or at risk of rollback. A score of 5 means ambitious, legally binding targets with near-term milestones.

Pillar 1 score = average of 1A + 1B + 1C, rounded to one decimal.

Pillar 2 — Enforcement Reality

A score assessing whether the ban is actually implemented on the ground. This is the hardest pillar to score objectively, but arguably the most important, because a country with perfect regulation and zero enforcement is a worse opportunity than one with a partial ban that’s strictly enforced.

- • 1 = virtually no enforcement, banned items freely sold

- • 2 = sporadic enforcement, mostly in capital cities or against large manufacturers

- • 3 = moderate enforcement, fines being issued but non-compliance still common

- • 4 = strong enforcement across the formal sector, compliance is the norm for businesses

- • 5 = strict and consistent enforcement with meaningful consequences, high compliance across both formal and informal sectors

Enforcement scoring draws on reported evidence such as news coverage, government compliance data, NGO assessments, and investigative journalism.

Pillar 3 — Market Opportunity Gap

This measures the distance between how much plastic is being removed by bans and how much bioplastics capacity exists to fill that gap. A large gap means high opportunity.

- • 1 = small gap — the country already has substantial domestic bioplastics production and import channels

- • 2 = moderate gap — some supply exists but doesn’t fully cover demand

- • 3 = significant gap — large plastic consumption, limited bioplastics supply, heavy import reliance

- • 4 = large gap — very limited bioplastics presence despite active bans

- • 5 = massive gap — very high plastic consumption being disrupted by bans, almost no domestic bioplastics capacity

Composite Score

Composite = Pillar 1 + Pillar 2 + Pillar 3. Range: 3 to 15.

How the Report Is Organised

Countries are grouped by region — Asia-Pacific, Europe, Americas, and Middle East, Africa & Oceania. Within each region, countries are ordered by composite score from highest to lowest, not alphabetically. This means the strongest opportunities appear first in each regional section.

Global Overview of Single-Use Plastic Bans

1.1 The Global Landscape: How Single-Use Plastic Bans Are Reshaping Markets

Every ban on single-use plastic creates a vacuum. The product disappears but the demand doesn’t. People still need bags, cups, cutlery and packaging. What changes is the material. That shift is the commercial opportunity this report attempts to map.

But to understand where the opportunity is biggest, you need to understand what’s actually happening with SUP bans worldwide.

How Countries Are Regulating Single-Use Plastics

Plastic bans are not moving in one direction globally, but are splintering, as some countries accelerate, others reverse, and the gap between law and enforcement is often enormous. Most countries use a combination of these five approaches:

1. Direct Product Bans

A law prohibiting specific items from being manufactured, imported, sold or used. This is the most common approach, and is used by India, France, Kenya, Canada, the UAE and most EU countries.

The scope varies hugely. France bans fruit-and-vegetable packaging, fast-food dine-in disposables and plastic toys in kids’ meals. India bans 14 specific items plus carry bags below 120 microns. Kenya bans all carrier bags but not cups or cutlery outside national parks.

2. Fiscal Pressure

Taxing conventional plastic rather than banning it and making alternatives price-competitive through cost signals rather than prohibition.

- • Spain: €0.45/kg on non-recycled plastic packaging

- • UK: £224/tonne Plastic Packaging Tax + £423/tonne EPR fee — combined, among the highest regulatory cost burdens on virgin plastic anywhere

- • Colombia: IPUSUI tax adds ~17% to rigid plastic container costs

- • Japan and Israel: Mandatory bag charges that cut consumption by ~70%

Insight: Fiscal signals don’t remove plastic from the market. But they’re more effective than poorly enforced bans because they work through the tax system, which is harder to evade.

3. Extended Producer Responsibility (EPR)

Requiring companies that put plastic packaging on the market to pay for its collection and recycling. This doesn’t ban anything directly but restructures packaging economics so bio-based materials become financially attractive.

California’s SB 54, South Africa’s Section 18, and India’s escalating recycled-content mandates (30% for rigid packaging in 2025-26, rising to 60% by 2028-29) all work this way.

4. Phased Rollouts

Bans that start with easy items and progressively expand. The phase schedule tells businesses exactly when the next wave of demand will arrive.

- • China: Geographic tiers — major cities first, then smaller ones

- • Colombia: Two phases through 2030 — bags and straws first, then food containers and cutlery

- • UAE: Bags in 2024, then cups, cutlery and Styrofoam in 2026

5. Voluntary and Market-Based Models

Reduction through disclosure, reputation and corporate pressure rather than legal prohibition.

Japan has no law banning any single-use plastic item. Its Plastic Resource Circulation Act uses mandatory charging, public reporting and industry cooperation. The bag charge alone cut usage ~70%.

Caveat: Voluntary models can reduce consumption significantly but don’t create the hard demand floor that a legal ban does. For bioplastics suppliers, mandatory bans are a more reliable demand signal.

1.2 The Reputation-Versus-Reality Problem

A critical finding from our research: the relationship between how strict a ban looks on paper and how much demand it actually creates is weak.

Three patterns explain why.

Strong law, weak enforcement

Kenya’s 2017 bag ban carries up to 4 years’ imprisonment. But cross-border smuggling is endemic, enforcement has softened, and Nairobi’s governor publicly acknowledged in 2024 that bags “have come back.” In India, a Toxics Link study found 64% of market sites still had banned plastics a year after the ban.

Policy reversal

Israel repealed a utensil tax that had cut consumption 40%, to fulfil coalition demands. South Korea withdrew its paper cup ban indefinitely. The Netherlands paused SUP surcharge enforcement. The US reversed federal plastics policy via executive order. These follow a common pattern: political backlash when bans impose visible costs on consumers.

Ban without alternatives

Some countries ban plastic but lack the supply chain, composting infrastructure or certification systems to make bioplastics viable. The ban pushes demand to paper, cloth or non-compliance, not to bioplastics.

Key takeaway: A ban only creates a bioplastics opportunity to the extent it is actually enforced and alternatives are available and affordable.

1.3 Where Single-Use-Plastic Bans Are Creating Real Opportunities

Amid this complexity, five patterns stand out where SUP regulation is genuinely creating commercial demand for bioplastics.

The Exemption Effect

The most powerful mechanism: ban conventional plastic but explicitly exempt certified compostable alternatives. Italy did this, and went on to create Europe’s largest bioplastics market (40-50% of EU demand) and the foundation for Novamont’s 150,000 TPA operation. The UAE similarly recognises PLA as a permitted substitute.

Structural Recycling Shortfalls

Australia faces a 64% gap between waste volumes and recycling capacity. Domestic virgin polymer production has nearly exited. When a country can neither recycle nor produce enough conventional plastic, bio-based alternatives fill a structural need.

Fiscal Tipping Points

When the combined regulatory cost on conventional plastic exceeds the bioplastics price premium, substitution becomes economically rational without any ban. The UK is approaching this: ~£650/tonne in combined regulatory costs before manufacturing begins.

Feedstock-Driven Cost Advantage

Local agricultural feedstocks make bioplastics cheaper in certain geographies. Examples:

- • Indonesia’s cassava and seaweed

- • Thailand’s sugar and cassava (with 8-year tax holidays for bioplastic projects)

- • Brazil’s sugarcane ethanol powering Braskem’s 275,000 TPA bio-PE — the world’s largest

The 2026 EU Harmonisation Event

The Packaging and Packaging Waste Regulation (PPWR), entering application in August 2026, will impose uniform bans on fruit-and-veg packaging, HORECA dine-in disposables, hotel toiletries and condiment sachets across all 27 EU member states.

It transforms the opportunity from navigating 27 separate regimes to serving a single harmonised market of 450 million consumers. This makes PPWR the most important regulatory event for European bioplastics before 2030.

The Bioplastics Opportunity Index: Full 25-Country Rankings

The table below ranks all 25 countries assessed in this report by their BOI composite score. Countries are grouped by region in the detailed assessments that follow, but here they are presented in a single ranked list for direct comparison.

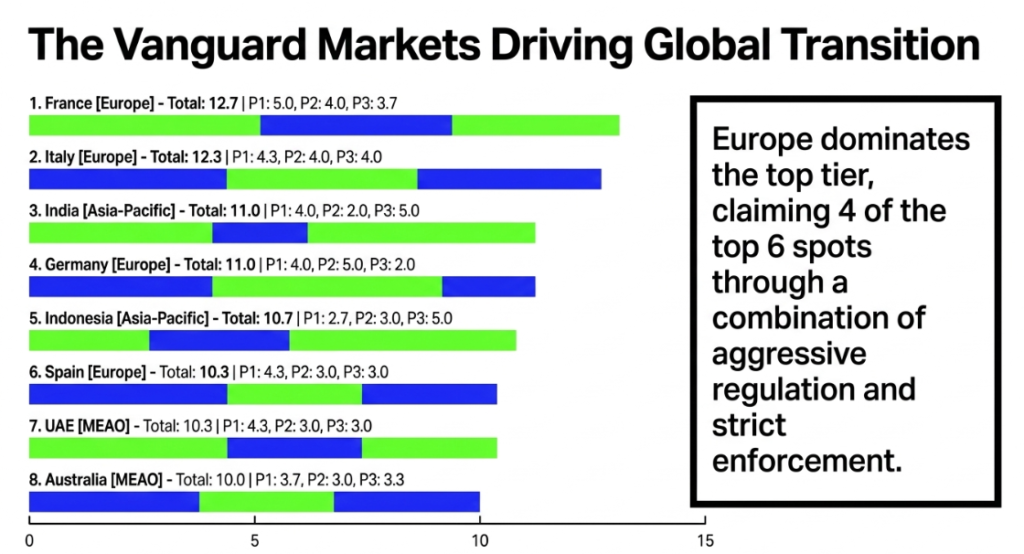

🟢 High Opportunity (10.0+)

| Rank | Country | Region | Pillar 1 | Pillar 2 | Pillar 3 | Composite |

|---|---|---|---|---|---|---|

| 1 | France | Europe | 5.0 | 4.0 | 3.7 | 12.7 |

| 2 | Italy | Europe | 4.3 | 4.0 | 4.0 | 12.3 |

| 3 | India | Asia-Pacific | 4.0 | 2.0 | 5.0 | 11.0 |

| 4 | Germany | Europe | 4.0 | 5.0 | 2.0 | 11.0 |

| 5 | Indonesia | Asia-Pacific | 2.7 | 3.0 | 5.0 | 10.7 |

| 6 | Spain | Europe | 4.3 | 3.0 | 3.0 | 10.3 |

| 7 | UAE | MEAO | 4.3 | 3.0 | 3.0 | 10.3 |

| 8 | Australia | MEAO | 3.7 | 3.0 | 3.3 | 10.0 |

🟡 Moderate Opportunity (8.0–9.9)

| Rank | Country | Region | Pillar 1 | Pillar 2 | Pillar 3 | Composite |

|---|---|---|---|---|---|---|

| 9 | United Kingdom | Europe | 3.7 | 3.0 | 3.0 | 9.7 |

| 10 | Colombia | Americas | 4.5 | 3.0 | 2.0 | 9.5 |

| 11 | China | Asia-Pacific | 3.3 | 3.0 | 3.0 | 9.3 |

| 12 | Netherlands | Europe | 3.3 | 2.0 | 4.0 | 9.3 |

| 13 | Japan | Asia-Pacific | 3.0 | 4.0 | 2.0 | 9.0 |

| 14 | Sweden | Europe | 3.7 | 4.0 | 1.3 | 9.0 |

| 15 | South Korea | Asia-Pacific | 2.7 | 3.0 | 3.0 | 8.7 |

| 16 | Denmark | Europe | 3.7 | 3.0 | 2.0 | 8.7 |

| 17 | Thailand | Asia-Pacific | 2.3 | 2.0 | 4.0 | 8.3 |

| 18 | South Africa | MEAO | 3.3 | 3.0 | 2.0 | 8.3 |

| 19 | Mexico | Americas | 3.2 | 2.0 | 3.0 | 8.2 |

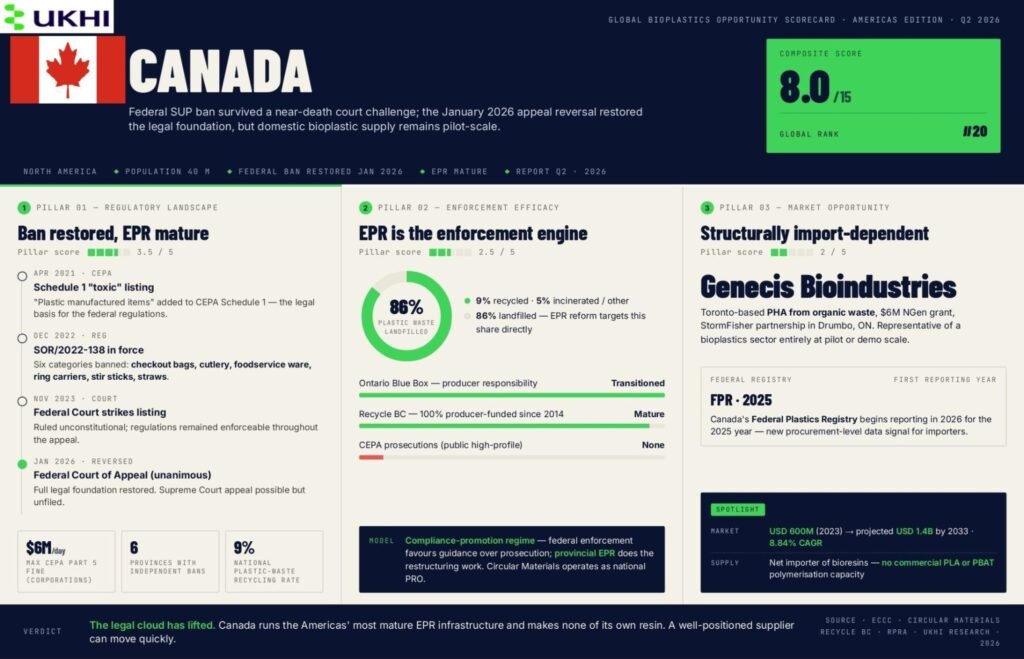

| 20 | Canada | Americas | 3.5 | 2.5 | 2.0 | 8.0 |

| 21 | Kenya | MEAO | 3.0 | 2.0 | 3.0 | 8.0 |

🔴 Emerging / Constrained Opportunity (below 8.0)

| Rank | Country | Region | Pillar 1 | Pillar 2 | Pillar 3 | Composite |

|---|---|---|---|---|---|---|

| 22 | Israel | MEAO | 2.0 | 2.7 | 3.0 | 7.7 |

| 23 | Brazil | Americas | 2.5 | 2.0 | 3.0 | 7.5 |

| 24 | USA | Americas | 2.5 | 2.0 | 2.0 | 6.5 |

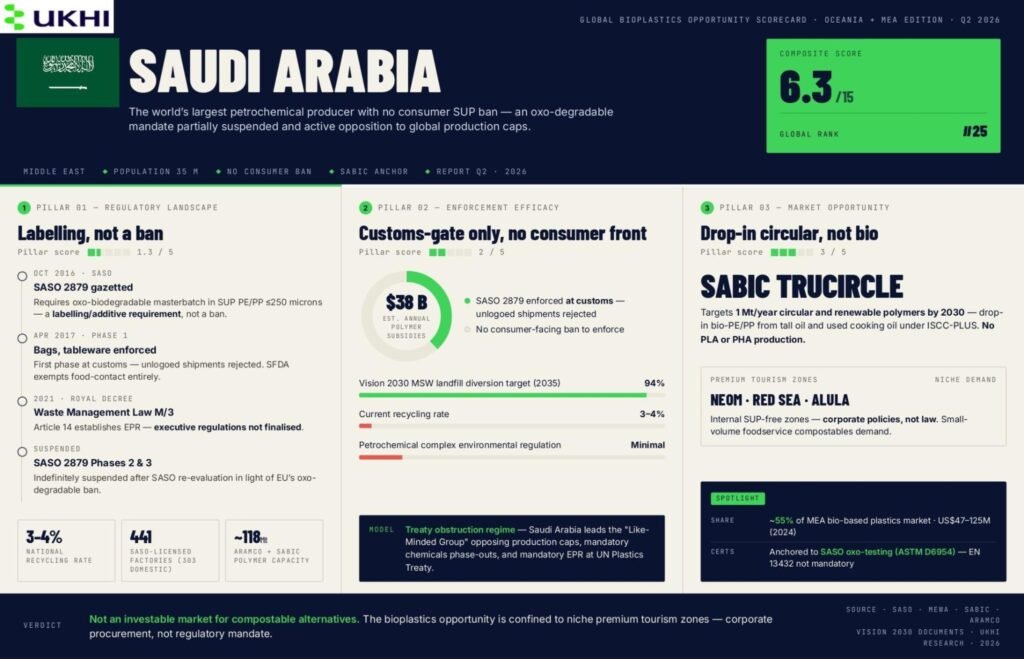

| 25 | Saudi Arabia | MEAO | 1.3 | 2.0 | 3.0 | 6.3 |

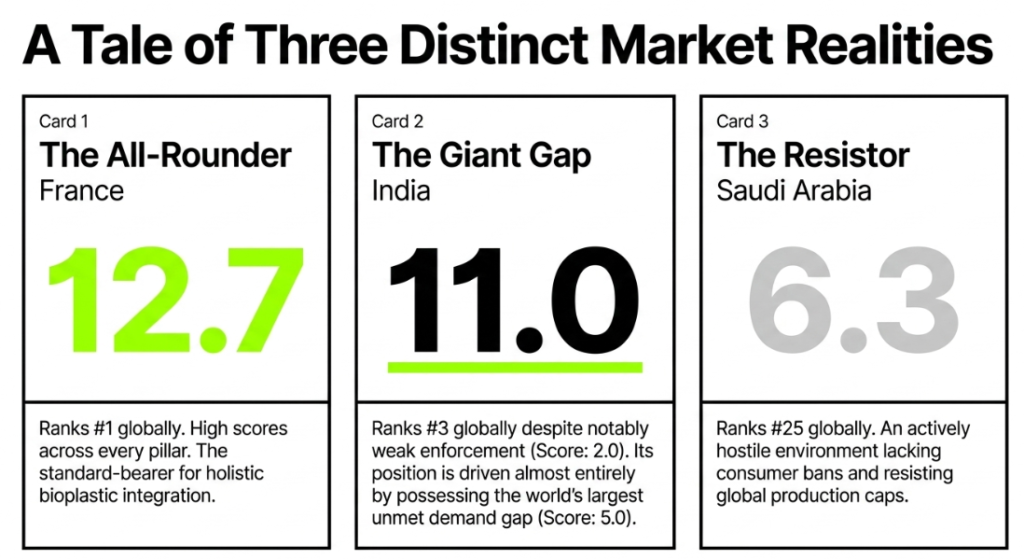

How to read this table: A high Pillar 1 score means strong regulation. A high Pillar 2 means the regulation is actually enforced. A high Pillar 3 means there is a large unmet demand gap for bioplastics. The composite rewards countries that are strong across all three. France leads because it scores high everywhere. India ranks third despite weak enforcement because its opportunity gap is the largest in the world. Saudi Arabia ranks last because it has no consumer ban and actively opposes global production caps.

The Bioplastics Opportunity Index: 25-Country Assessment

The following is a country-by-country evaluation of 25 markets across four regions. Each is scored on the same three-pillar framework and presented in a consistent format so any two countries can be compared at a glance. Within each region, countries are ordered by composite score from highest to lowest.

3.1 INDIA – Single-Use Plastic Ban: Market Opportunity Index

Composite Score: 11.0 / 15 | Global Rank: #3

Massive regulatory ambition and the world’s largest unmet bioplastics demand, but held back by enforcement gaps in the informal economy.

3.1.1 India’s Single-Use Plastic Ban: Laws and Regulations

3.1.1.1 Key Laws Governing India’s Plastic Ban

- • Primary legislation: The Plastic Waste Management Rules, 2016, amended significantly in 2021 (banning 19 SUP items), 2022 (EPR guidelines), 2025 (QR code traceability), and 2026 (escalated recycled content mandates).

- • Enforcing bodies: Central Pollution Control Board (CPCB) at national level, State Pollution Control Boards at state level, Urban Local Bodies on the ground.

- • Penalties for non-compliance: Fines up to ₹15 lakh per violation under the Environment (Protection) Act, 1986. Environmental compensation of ₹5,000–20,000 per tonne of banned items. Prosecution and factory closure for repeat offenders.

3.1.1.2 Which Plastic Items Are Banned in India?

19 banned items (from 1 July 2022): Earbuds, balloon sticks, flags, candy sticks, ice-cream sticks, thermocol for decoration, plates, cups, glasses, forks, spoons, knives, straws, trays, wrapping films around sweet boxes, invitation cards, cigarette packets, PVC banners under 100 microns, and stirrers.

Plastic carry bags below 120 microns banned since December 2022. Plastic sachets for gutkha and tobacco are completely prohibited.

Exemptions: Compostable plastics certified to IS/ISO 17088:2021, export-oriented SEZ units, and flexible food packaging (covered under EPR instead).

3.1.1.3 India’s Plastic Ban Timeline and Future Goals

- • Phase 1 (Jan 2022): Smaller items like earbuds, candy sticks, balloon sticks.

- • Phase 2 (Jul 2022): Larger categories like plates, cups, cutlery, straws, wrapping films.

- • EPR targets through 2028-29: Rigid packaging must include 30% recycled content in 2025-26, rising to 60% by 2028-29. Collection targets reach 80%. Reuse targets for large water containers reach 85%.

- • From July 2025: All plastic packaging must carry QR codes or barcodes for traceability.

Stated goal: 100% recyclable or compostable packaging by 2030.

3.1.2 India’s Plastic Ban Enforcement: Ground Reality

- • Organised retail broadly complies. In the ban’s first month, 775,000 kg of illegal plastics seized and ₹5.82 crore collected in penalties.

- • Informal markets remain non-compliant. A Toxics Link study found 64% of market sites still had banned plastics a year post-ban, with Delhi at 88%.

- • Scope is limited. The 19-item ban addresses only ~11% of India’s SUP waste. Sachets and multi-layered packaging remain outside scope.

- • Digital enforcement tightening. Over 100,000 entities received show-cause notices for EPR non-compliance in FY 2023-24.

3.1.3 India’s Bioplastics Market Size and Opportunity Gap

- • Plastic consumption: ~20 million tonnes annually, growing at ~10%/year.

- • Bioplastics market: ~USD 450 million (2024), ~193,000 tonnes — under 1% of total use.

- • Domestic capacity: Fragmented. Balrampur Chini (75,000 TPA PLA) is the largest addition.

- • Import dependence: High. PLA (Thailand/USA), PBAT (Germany/China), PHA (South Korea).

3.1.4 Commentary and Insights

- • EPR is the bigger demand driver than the ban itself.

- • Two parallel markets exist: formal vs informal economy.

- • Composting infrastructure is the critical gap.

3.1.5 India Opportunity Scorecard

| Factor | Score |

| Pillar 1: Regulatory Strength | 4.0 / 5 |

| 1A — Legal Framework | 4 |

| 1B — Ban Breadth | 4 |

| 1C — Future Trajectory | 4 |

| Pillar 2: Enforcement | 2 / 5 |

| Pillar 3: Opportunity Gap | 5 / 5 |

| Composite Score | 11.0 / 15 |

Verdict: India offers the world’s largest bioplastics opportunity by scale. Enforcement is the drag, but the formal sector opportunity alone is substantial and growing as EPR mandates tighten through 2028-29.

3.2 INDONESIA – Single-Use Plastic Ban: Market Opportunity Index

Composite Score: 10.7 / 15 | Global Rank: #5

Dense regulatory architecture and unique feedstock advantages in cassava and seaweed, but enforcement is delegated to cities, and most of the country lacks basic waste collection.

3.2.1 Indonesia’s Single-Use Plastic Ban: Laws and Regulations

3.2.1.1 Key Laws Governing Indonesia’s Plastic Ban

- • National framework: Law No. 18/2008 on Waste Management sets the foundation. Presidential Regulation No. 83/2018 established the National Action Plan on Marine Plastic Debris with a 70% marine plastic reduction target by 2025.

- • EPR regulation: MoEF Regulation P.75/2019 requires producers to cut baseline waste by 30% by 2029 and schedules a national ban on Styrofoam food packaging, plastic cutlery, straws, shopping bags, and sachet packaging by 2030.

- • Enforcing bodies: Coordinating Ministry for Maritime and Investment Affairs, Ministry of Environment (KLH), and provincial/city governments.

- • Penalties: Vary by jurisdiction. Jakarta fines range from IDR 5–25 million (~USD 300–1,500). National-level penalties are rarely applied.

3.2.1.2 Which Plastic Items Are Banned in Indonesia?

No nationwide product-specific SUP ban exists. Indonesia relies on subnational regulations, as roughly 100+ cities and regencies have enacted their own rules.

- • Bali: Bans SUP bags, Styrofoam, straws, and now plastic bottles under 1 litre.

- • Jakarta: Bans plastic shopping bags since July 2020.

- • Other cities: Bogor, Bandung, Surabaya, Semarang, Banjarmasin, Balikpapan, Denpasar, Makassar.

Exemptions: Medical packaging, industrial wrapping. Sachets remain unregulated nationally.

3.2.1.3 Indonesia’s Plastic Ban Timeline and Future Goals

- • 2025 target: 70% marine plastic reduction (progress ~42% by 2024).

- • 2030 target: National ban on Styrofoam, cutlery, straws, bags, and sachets.

- • Draft Sustainable Packaging Act under development (EPR expansion expected).

3.2.2 Indonesia’s Plastic Ban Enforcement: Ground Reality

- • Bali success: Plastic bags down 57%, straws 70%, Styrofoam 81%, strong village-level enforcement.

- • Jakarta mixed: Retail complies, but sachets untouched.

- • Infrastructure gap: 40% urban population lacks waste collection, 85% rural waste uncollected.

3.2.3 Indonesia’s Bioplastics Market Size and Opportunity Gap

- • Plastic consumption: ~6.1 Mt (2020), projected ~8.6 Mt by 2025.

- • Waste: ~7.8 Mt/year, 63% mismanaged.

- • Bioplastics capacity: CJ Biomaterials PHA plant (5,000 → 65,000 TPA planned).

- • Feedstock advantage: Cassava, seaweed (~38% global output).

Import dependence remains high for PLA and PBAT. :contentReference[oaicite:0]{index=0}

3.2.4 Commentary and Insights

- • Opportunity is feedstock-driven, not regulation-driven.

- • Subnational enforcement (Bali model) is key.

- • Sachets remain the largest unresolved waste category.

- • CJ Biomaterials positions Indonesia as a regional PHA hub.

3.2.5 Indonesia Opportunity Scorecard

| Factor | Score |

| Pillar 1: Regulatory Strength | 2.7 / 5 |

| Pillar 2: Enforcement Reality | 3 / 5 |

| Pillar 3: Opportunity Gap | 5 / 5 |

| Composite Score | 10.7 / 15 |

Verdict: Indonesia’s regulatory framework is weaker, but feedstock advantages and PHA capacity create a unique opportunity. Infrastructure remains the key constraint.

3.3 CHINA – Single-Use Plastic Ban: Market Opportunity Index

Composite Score: 9.3 / 15 | Global Rank: #11

The world’s largest bioplastics producer but with structural overcapacity, uneven enforcement, and domestic demand that cannot absorb what its factories make.

3.3.1 China’s Single-Use Plastic Ban: Laws and Regulations

3.3.1.1 Key Laws Governing China’s Plastic Ban

- • Primary policy: The NDRC/MEE “Opinions on Further Strengthening Plastic Pollution Treatment” (January 2020).

- • Statutory backing: The revised Solid Waste Law (effective September 2020). Article 69 prohibits production, sale, and use of non-degradable SUPs. Article 106 penalties: RMB 10,000–100,000 (~USD 1,400–14,000) for retail violations.

- • Implementation plan: The 14th Five-Year Plan Action Plan for Plastic Pollution Control (September 2021) operationalises province-level rollout.

- • Biodegradable standard: GB/T 41010-2021 (June 2022) requires ≥90% biodegradation and mandates the “双J” identification mark.

- • Strictest jurisdiction: Hainan Province — island-wide ban on all non-degradable SUPs from December 2020, with 11 million illicit bags seized at ports by end-2021.

3.3.1.2 Which Plastic Items Are Banned in China?

- • Plastic bags: Banned in tier-1 city retail from end-2020, all prefecture-level cities by end-2022, wet markets nationally by end-2025.

- • Straws and foam tableware: Disposable plastic straws banned nationwide in catering from January 2021. Foam tableware banned nationwide.

- • Food delivery cutlery: 30% reduction target by 2025 in tier-1+ cities.

- • Hotels: “Six small items” (toothbrushes, combs, razors etc.) restricted in star-rated hotels by 2022, all hotels by end-2025.

- • Microbeads: Production banned by end-2020, sales by end-2022.

- • Express delivery packaging: Required to be fully degradable in seven coastal provinces by end-2022, nationally by end-2025.

3.3.1.3 China’s Plastic Ban Timeline and Future Commitments

- • End-2025 deadlines were the key milestone: wet market bag bans go national, hotel single-use items eliminated, express packaging goes degradable.

- • No quantified long-term elimination target comparable to France’s 2040 or India’s 2030 ambitions.

- • Agricultural mulch film (2.6 Mt/year) — mandates for biodegradable mulch in provinces like Xinjiang and Yunnan represent a massive upcoming use case.

UN Plastics Treaty position: China sits in the Like-Minded Countries bloc, opposing binding polymer production caps.

3.3.2 China’s Plastic Ban Enforcement: Ground Reality

- • Province-level variation is extreme. Hainan enforces regulations with port seizures. Tier-1 cities show moderate retail compliance. Lower-tier and rural markets are largely unaffected.

- • Platforms, not police, drive compliance. Meituan and Ele.me cutlery opt-out systems cover 30M+ daily orders. Over 70% of Shanghai food delivery orders now skip cutlery. Platforms are de facto regulators.

- • The historical pattern is cautionary. The 2008 bag ban initially cut supermarket bag use by two-thirds, then enforcement waned. Researchers flag the same risk with the 2020 regime.

3.3.3 China’s Bioplastics Market Size and Capacity

- • Plastic consumption: World’s largest — 138 million tonnes of resin produced (2023), ~32% of global output. Plastic waste: 81.5 million tonnes (2022).

- • Bioplastics capacity: ~20% of global installed capacity. Over 50% of global PBAT capacity. Combined PLA+PBAT at ~1.5 Mt but running at only 17% utilisation.

Key manufacturers:

- • Kingfa (70,000 TPA PBAT)

- • BBCA Biochemical (100,000 TPA PLA)

- • Blue Ridge Tunhe (128,000+ TPA PBAT+PBS)

- • COFCO (300,000 TPA PBAT announced)

Aggregate announced capacity exceeds 7 million TPA.

Net exporter. China is the primary bio-resin supply source for India, Southeast Asia, and Europe. This is not a supply-gap market but a demand-gap market. :contentReference[oaicite:0]{index=0}

3.3.4 Commentary and Insights

China is a price-compression threat, not an entry opportunity. With PLA+PBAT capacity at 17% utilisation and millions of tonnes announced, Chinese overcapacity will keep global bio-resin prices under pressure through 2028.

Agricultural mulch film is the real demand story. At 2.6 Mt/year of plastic mulch (much left in soil), government mandates for biodegradable mulch represent a far larger addressable market than food service SUP replacement.

Platform-driven compliance is unique. The most effective SUP reduction has happened through Meituan and Ele.me’s opt-out defaults. This suggests that the bioplastics opportunity in China lies in B2B partnerships with delivery and e-commerce platforms, not retail substitution via ban enforcement.

3.3.5 China Opportunity Scorecard

| Factor | Score |

| Pillar 1: Regulatory Strength | 3.3 / 5 |

| 1A — Legal Framework Robustness | 4 |

| 1B — Ban Breadth | 3 |

| 1C — Future Trajectory | 3 |

| Pillar 2: Enforcement Reality | 3 / 5 |

| Pillar 3: Market Opportunity Gap | 3 / 5 |

| Composite Score | 9.3 / 15 |

Verdict: China has the world’s strongest bioplastics manufacturing base but weak demand absorption. Its capacity vastly outstrips what enforcement currently pulls through. The opportunity is not selling into China but watching its export pricing, which sets the floor for global bio-resin costs.

3.4 JAPAN – Single-Use Plastic Ban: Market Opportunity Index

Composite Score: 9.0 / 15 | Global Rank: #13

No outright ban but a market-based model that quietly achieves more substitution than most bans, driven by corporate compliance culture and specialty bioplastics innovation.

3.4.1 Japan’s Single-Use Plastic Reduction: Laws and Regulations

3.4.1.1 Key Laws Governing Japan’s Plastic Policy

- • Primary legislation: Act on Promotion of Resource Circulation for Plastics (2021, enforced April 2022). Administered by METI and Ministry of the Environment.

- • Bag charge (July 2020): Mandatory ≥¥1 fee at all retailers. Bags with ≥25% biomass content or certified biodegradable are exempt.

- • Compliance model: Guidance → recommendation → public disclosure → order → fine up to ¥500,000 (~USD 3,300). Reputational pressure, not heavy penalties.

3.4.1.2 Which Plastic Items Are Restricted in Japan?

No items are outright banned. The 2022 Act designates 12 products (forks, spoons, knives, stirrers, straws, hairbrushes, combs, razors, toothbrushes, shower caps, hangers, laundry covers) — businesses providing ≥5 tonnes/year must take reduction measures. They choose their own approach: charging, lightweighting, or switching to biomass materials.

3.4.1.3 Japan’s Plastic Reduction Timeline and Future Goals

- • July 2025: METI launches eco-design certification for PET bottles, stationery, cosmetic containers.

- • 2030: 25% SUP reduction, 60% packaging recycling, aspirational 2 Mt bioplastic introduction (current consumption: ~42,000 tonnes — target will be missed by 25×).

- • 2035: 100% effective utilization of waste plastic.

3.4.2 Japan’s Plastic Ban Enforcement: Ground Reality

- • Bag charge works. Refusal rates rose from 30.4% to 71.9% within eight months. ~13.88 billion fewer bags distributed nationally.

- • Corporate compliance is extensive without enforcement. 7-Eleven’s plant-based onigiri wraps cover 2.2 billion rice balls/year. Starbucks Japan rolled out Kaneka PHBH straws nationwide by March 2025.

- • Recycling figures are misleading. 89% “effective utilisation” claimed, but only ~6% is truly mechanically recycled. Rest is incineration or export.

3.4.3 Japan’s Bioplastics Market Size and Manufacturers

- • Plastic consumption: 7,690 kt (2023). Bioplastics: ~42,000 tonnes consumed, valued ~USD 329 million.

- • Key manufacturers: Kaneka (20,000 TPA PHBH — world’s first commercial PHBH), Mitsubishi Chemical (BioPBS, DURABIO bio-PC), Mitsui Chemicals (Prasus™), Toray (Ecodear).

- • Import dependent for commodity PLA/bio-PE. Domestic focus is specialty high-margin materials (PHA, bio-PC, bio-PBS).

3.4.4 Commentary and Insights

- • Japan proves bans are not the only path. Charging plus corporate culture achieved sustained change without a single ban.

- • Opportunity is specialty, not commodity. Japanese manufacturers lead in PHBH, bio-PBS, bio-PC. Volume PLA/PBAT competition is ceded to China and Thailand.

- • Brand owners drive demand, not regulators. Starbucks, Lawson, 7-Eleven, Honda adopt bioplastics faster than policy requires. Supplier opportunity is through brand partnerships.

- • The 2 Mt target is fiction. At 42,000 tonnes actual vs. 2 Mt target, policy tightening is inevitable.

3.4.5 Japan Opportunity Scorecard

| Factor | Score |

| Pillar 1: Regulatory Strength | 3.0 / 5 |

| 1A — Legal Framework Robustness | 3 |

| 1B — Ban Breadth (product categories) | 2 |

| 1C — Future Trajectory | 4 |

| Pillar 2: Enforcement Reality | 4 / 5 |

| Pillar 3: Market Opportunity Gap | 2 / 5 |

| Composite Score | 9.0 / 15 |

Verdict: Narrow but high-value market. Not a volume market but a premium market where brand-owner partnerships and specialty material innovation determine who wins.

3.5 SOUTH KOREA – Single-Use Plastic Ban: Market Opportunity Index

Composite Score: 8.7 / 15 | Global Rank: #15

Petrochemical giants are pivoting to bioplastics but policy whiplash (bans enacted, reversed, re-enacted in 18 months) makes the regulatory signal unreliable.

3.5.1 South Korea’s Single-Use Plastic Ban: Laws and Regulations

3.5.1.1 Key Laws Governing South Korea’s Plastic Ban

- • Primary legislation: Act on Promotion of Saving and Recycling of Resources (1992, amended 2002), plus Framework Act on Resource Circulation (2016) and Carbon Neutrality Act (2021).

- • K-Circular Economy Plan (2021): 50% plastic waste reduction, 70% recycling by 2030.

- • Penalties: Up to KRW 3 million (~USD 2,290) for providing banned SUP items.

3.5.1.2 Which Plastic Items Are Banned in South Korea?

Dine-in plastic cups banned since 2018. Plastic bags in large retailers since January 2019. November 2022: Expanded to straws, stirrers, convenience-store bags.

November 2023 reversal: Yoon administration withdrew paper cup ban, extended straw grace periods indefinitely, and returned convenience-store bags to voluntary.

December 2025 re-tightening: Lee administration announced 30% SUP reduction by 2030, mandatory 10% recycled PET from 2026 (30% by 2030), ban on all straws. Not yet legislated.

3.5.1.3 South Korea’s Plastic Ban Timeline

- • Cup deposit (300-won): Piloted in Jeju/Sejong only. 51% return rate in 2023. Nationwide rollout indefinitely delayed.

- • 2028: MCEE will reclassify thermal recycling separately which means headline recycling rate will drop from ~57% to ~16%.

3.5.2 South Korea’s Plastic Ban Enforcement

- • Policy whiplash is the story. The 2023 reversal left Seoil Corp with 200M+ unsold paper straws. Two firms sued for KRW 6.4 billion in losses. The 2025 re-tightening is not yet law.

- • Recycling is inflated. Official: 57.5%. Greenpeace/Chungnam University using EU methodology: actual material recycling 16.4%.

- • Highest per-capita plastic waste in the OECD — 103.9 kg (MOE), up to 208 kg under broader measurement.

3.5.3 South Korea’s Bioplastics Market Size and Manufacturers

- • Plastic consumption: 12.6 Mt (2022), up 31% since 2019. Bioplastics: ~64,680 tonnes (2024).

- • Key manufacturers — investing offshore: CJ Biomaterials (5,000 TPA PHA in Indonesia, expanding to 65,000). LG Chem (75,000 TPA PLA with ADM in Illinois). SK Geo Centric (KRW 1.8 trillion Ulsan cluster; PBAT JV with Kolon). SKC (70,000 TPA PBAT in Vietnam). Lotte Chemical (1 Mt recycled plastic target by 2030).

3.5.4 Commentary and Insights

- • Policy instability is Korea’s biggest liability. Industry cannot invest on regulations enacted, reversed, and re-enacted within 18 months.

- • 2028 recycling reclassification will be a forcing event. When thermal recovery is separated, the headline rate drops to ~16% which creates political pressure for real circular economy measures.

- • For outside companies, the play is partnership with Korean conglomerates expanding across Asia, not selling into Korea’s unstable domestic market.

3.5.5 South Korea Opportunity Scorecard

| Factor | Score |

| Pillar 1: Regulatory Strength | 2.7 / 5 |

| 1A — Legal Framework Robustness | 3 |

| 1B — Ban Breadth (product categories) | 3 |

| 1C — Future Trajectory | 2 |

| Pillar 2: Enforcement Reality | 3 / 5 |

| Pillar 3: Market Opportunity Gap | 3 / 5 |

| Composite Score | 8.7 / 15 |

Verdict: Korea has capital, technology, and corporate ambition but domestic policy is too unstable to generate reliable demand. Opportunity lies in partnering with Korean conglomerates building capacity across Asia and the Americas, not selling into the domestic market.

3.6 THAILAND – Single-Use Plastic Ban: Market Opportunity Index

Composite Score: 8.3 / 15 | Global Rank: #17

ASEAN’s largest bioplastics production hub and a global export platform but domestic regulation is almost entirely voluntary. A supply story, not a demand story.

3.6.1 Thailand’s Single-Use Plastic Ban: Laws and Regulations

3.6.1.1 Key Laws Governing Thailand’s Plastic Policy

- • Primary framework: Plastic Waste Management Roadmap 2018–2030 (Cabinet-approved April 2019). No legal penalties.

- • Only binding national ban: National Parks SUP ban (April 2022) with fines up to 100,000 baht (~USD 3,000). Applies inside national parks only.

- • Plastic waste import ban (January 2025): Bans plastic scrap imports, with discretionary exceptions.

- • Draft Sustainable Packaging Management Act (2024): First attempt at mandatory EPR. Targeted enactment 2027, penalties ~2029.

3.6.1.2 Which Plastic Items Are Restricted in Thailand?

- • Voluntary retailer bag ban (January 2020): 75 retailers (CP All/7-Eleven, Central Group, Big C, Makro) stopped providing bags. Covers ~30% of bag universe. No statutory force.

- • Roadmap targets (no penalties): Lightweight bags <36 μm, Styrofoam food containers, cups <100 μm, straws.

- • No nationwide ban on cutlery, plates, stirrers, or packaging. Most permissive regime among the six countries covered.

3.6.1.3 Thailand’s Plastic Reduction Timeline

- • 2027: 100% recyclable plastic (aspirational). Draft EPR Act enactment target.

- • 2029: Earliest date for real EPR penalties.

- • BCG Economy Model: Bioplastics as priority sector — 8-year BOI tax holidays, 1.25× green-tax deductions.

3.6.2 Thailand’s Plastic Ban Enforcement

- • Voluntary ban had a real but limited impact. 7-Eleven reported 169 million bags unused in the first two months. But franchises were documented still distributing bags because of no enforcement mechanism.

- • COVID reversed progress. Plastic waste surged 62% (2019–2020). Bangkok recycling rate fell from 27% to 19%.

- • 2021 recycling rate: 17.6% — missed the roadmap’s 50% target. Outside national parks and the import ban, Thailand’s regime is voluntary soft-law.

3.6.3 Thailand’s Bioplastics Market Size and Manufacturers

- • Plastic consumption: ~75 billion bags/year. Total waste: 25.7 Mt (2022), 28% poorly managed.

- • Bioplastics capacity: #2 global production hubs after the US. ~95,000 TPA, targeting 375,000–400,000 TPA. Over 90% is export-oriented.

- • Key plants: NatureWorks Ingeo PLA (Nakhon Sawan, 75,000 TPA, ~USD 600M). TotalEnergies Corbion PLA (Rayong, 75,000 TPA). PTT MCC Biochem (Bio-PBS). Braskem Siam (announced ~200,000 TPA bio-ethylene).

- • Feedstock advantage: World’s #1 cassava exporter (>60% global share), #5 sugar producers. Production costs ~USD 1,200/tonne vs. USD 2,100 in Western markets.

3.6.4 Commentary and Insights

- • Thailand is a production platform, not a demand market. 90%+ of bioplastics output is exported. Domestic regulation is almost irrelevant to its global supply chain role.

- • Cassava advantage is structural. Largest exporter, lowest cost, BOI incentives — most cost-competitive bioplastics manufacturing location in Asia-Pacific.

- • Voluntary model has a ceiling. Without binding EPR or penalties, domestic SUP reduction will plateau. Draft Packaging Act (2027/2029) is years from having teeth.

3.6.5 Thailand Opportunity Scorecard

| Factor | Score |

| Pillar 1: Regulatory Strength | 2.3 / 5 |

| 1A — Legal Framework Robustness | 2 |

| 1B — Ban Breadth (product categories) | 3 |

| 1C — Future Trajectory | 2 |

| Pillar 2: Enforcement Reality | 2 / 5 |

| Pillar 3: Market Opportunity Gap | 4 / 5 |

| Composite Score | 8.3 / 15 |

Verdict: Thailand’s demand-side score is modest. But Thailand is the region’s bioplastics supply engine: lowest-cost feedstock, largest installed capacity, major global players. The strategic question is not whether to sell into Thailand, but how to position against Thai-produced resin in every other market.

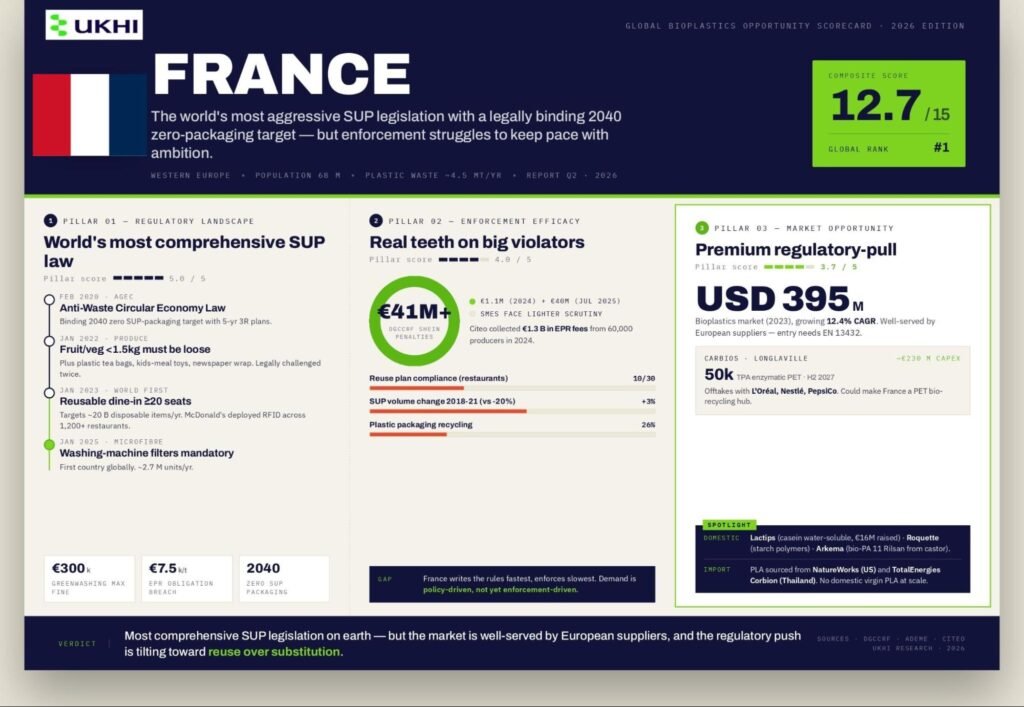

3.7 FRANCE – Single-Use Plastic Ban: Market Opportunity Index

Composite Score: 12.7 / 15 | Global Rank: #1

The world’s most aggressive SUP legislation with a legally binding 2040 zero single-use plastic packaging target, but enforcement struggles to keep pace with ambition.

3.7.1 France’s Single-Use Plastic Ban: Laws and Regulations

3.7.1.1 Key Laws Governing France’s Plastic Ban

- • Primary legislation: The AGEC Law (Loi n° 2020-105) of 10 February 2020 — France’s “Anti-Waste for a Circular Economy” law. Goes far beyond the EU SUP Directive with a legally binding target to eliminate all single-use plastic packaging by 2040.

- • Supporting legislation: The Loi Climat et Résilience (2021) tightened greenwashing rules. SUP Directive transposed via Décret n° 2021-461.

- • Enforcing bodies: Ministry of Ecological Transition (policy), ADEME (producer registrations), DGCCRF (consumer-facing enforcement and penalties).

- • Penalties for non-compliance: EPR non-registration: up to €30,000. EPR obligation breaches: up to €7,500 per tonne. Greenwashing: up to €300,000 or 10% of annual turnover plus two years’ imprisonment. DGCCRF fined Shein €1.098 million in 2024 and €40 million in July 2025.

3.7.1.2 Which Plastic Items Are Banned in France?

- • From January 2020: Plastic cups, plates, straws, cutlery, stirrers, ice-cream tubs, meal trays, salad bowls, confetti.

- • From January 2022: Plastic packaging for fruit and vegetables under 1.5 kg, plastic tea bags, free plastic toys in fast-food kids’ meals, plastic wrap on newspapers. Mandatory compostable produce stickers.

- • From January 2023: France became the first country to mandate reusable containers for dine-in at all restaurants with 20+ seats — targeting ~20 billion disposable items/year. McDonald’s France deployed RFID-tracked reusable containers across 1,200+ restaurants.

- • From January 2025: France is the first country to require microfibre filters on all new washing machines (~2.7 million units/year).

Exemptions: Medical packaging. The fruit-and-veg ban has been legally challenged twice — the Conseil d’État annulled the implementing decree in December 2022 and again in 2023. Currently in legal limbo pending EU PPWR harmonisation.

3.7.1.3 France’s Plastic Ban Timeline and Future Goals

- • 2040 target: Zero single-use plastic packaging — legally binding under AGEC with five-year 3R (reduce-reuse-recycle) action plans.

- • EU PPWR (August 2026): Will harmonise some French rules (fruit/veg packaging, hotel toiletries) at EU level, potentially resolving France’s Conseil d’État impasse.

- • Citeo (France’s packaging EPR body) collected €1.3 billion in EPR contributions in 2024 across 60,000 producers.

3.7.2 France’s Plastic Ban Enforcement: Ground Reality

- • Compliance is uneven. A March 2023 Ministry inspection found 10 of 30 sampled restaurant chains had no reuse compliance plan. McDonald’s publicly said the reuse model “doesn’t work” and France remains the only market requiring it.

- • SUP packaging volumes rose 3% between 2018 and 2021 against a minus-20% AGEC target. Plastic packaging recycling stands at just 26-27% (Citeo 2024), despite household packaging recycling at 69%.

- • Enforcement is real at the top. DGCCRF’s €41M+ in Shein penalties show France will pursue major violators. But small and mid-sized businesses face lighter scrutiny.

3.7.3 France’s Bioplastics Market Size and Manufacturers

- • Plastic waste: ~4.5 Mt/year. Only 23% recycled, 41% incinerated, 36% landfilled.

- • Bioplastics market: Valued at ~USD 395 million (2023), growing at 12.4% CAGR.

- • Key French bioplastics companies: Carbios (enzymatic PET recycling, 50,000 TPA plant at Longlaville with Indorama, ~€230M capex, online H2 2027, offtakes with L’Oréal, Nestlé, PepsiCo). Lactips (casein-based water-soluble bioplastic, €16M raised 2024-25). Roquette (starch-based biopolymers). Arkema (bio-PA 11 Rilsan from castor oil).

Import dependent for PLA — sourced from NatureWorks (USA) and TotalEnergies Corbion (Thailand). :contentReference[oaicite:0]{index=0}

3.7.4 Commentary and Insights

- • France writes the rules fastest but enforces slowest. The gap between AGEC’s ambition and on-ground compliance is the defining tension. For bioplastics suppliers, this means demand is policy-driven but not yet enforcement-driven.

- • The 2023 reusable dine-in mandate is a global first and a test case. If it succeeds in France, expect it to spread via PPWR across the EU. If it fails (McDonald’s is publicly sceptical), it will be a cautionary tale.

- • Carbios is the French bioplastics story to watch. Its enzymatic recycling technology, if it scales at Longlaville by 2027, could make France a PET bio-recycling hub. But this is recycling technology, not virgin bioplastics production.

- • For Ukhi, France is a premium regulatory-pull market. High compliance costs for conventional plastics, strong EPR fees (€1.3B/year), and an aggressive ban calendar create demand, but the market is well-served by European suppliers. Entry requires EN 13432 certification and Citeo registration.

3.7.5 France Opportunity Scorecard

| Factor | Score |

| Pillar 1: Regulatory Strength | 5.0 / 5 |

| 1A — Legal Framework Robustness | 5 |

| 1B — Ban Breadth (product categories) | 5 |

| 1C — Future Trajectory | 5 |

| Pillar 2: Enforcement Reality | 4 / 5 |

| Pillar 3: Market Opportunity Gap | 3.7 / 5 |

| Composite Score | 12.7 / 15 |

Verdict: France has the world’s most comprehensive SUP legislation and the strongest enforcement teeth in Europe. But the market is already well-served by European bioplastics suppliers, and the regulatory push is increasingly toward reuse rather than single-use substitution.

3.8 ITALY – Single-Use Plastic Ban: Market Opportunity Index

Composite Score: 12.3 / 15 | Global Rank: #2

Europe’s largest bioplastics market by far, and built on a unique compostable exemption and Novamont’s 150,000 TPA Mater-Bi capacity. But the European Commission is now formally challenging the exemption.

3.8.1 Italy’s Single-Use Plastic Ban: Laws and Regulations

3.8.1.1 Key Laws Governing Italy’s Plastic Ban

- • Primary legislation: D.Lgs. 196/2021 (8 November 2021, in force 14 January 2022) transposes the EU SUP Directive.

- • Historical bans predating the directive: Non-biodegradable shopping bags banned since 2011 (the first in the EU). Oxo-degradables and ultralight bags banned 2018. Cosmetic microplastics 2020. Plastic cotton buds 2019.

- • Enforcing bodies: MASE (environment), MIMIT (industry), ISPRA (data).

- • Penalties: €2,500–€25,000 per infraction, doubled to €50,000 where infringing goods exceed 10% of turnover.

3.8.1.2 Italy’s Unique Compostable Plastics Exemption

Article 5(3) of D.Lgs. 196/2021 exempts any SUP product from the ban if it is certified under UNI EN 13432 or UNI EN 14995, contains a minimum 40% renewable raw material (60% from January 2024), and meets at least one additional condition (no reusable alternative, organic collection environment, hygiene requirement, LCA justification).

This exemption makes Italy the only EU country where compostable plastic cutlery, plates, cups, and straws remain legally on sale. It created Europe’s largest bioplastics demand market.

The European Commission issued a formal infringement notice in July 2024 covering 13 points of D.Lgs. 196/2021, including the compostable exemption. A CJEU referral is probable if Italy does not amend.

3.8.1.3 Italy’s Plastic Ban Timeline and Future Goals

- • EU PPWR (August 2026): Will override many Italian national rules. Italy has sought PPWR exemptions for compostable packaging but outcome is uncertain.

- • Biorepack targets: Italy’s dedicated compostable packaging EPR consortium already exceeds both the 2025 EU 50% and 2030 EU 55% recycling targets, achieving 57.8% recycling in 2024 across 82,246 tonnes placed on market.

3.8.2 Italy’s Plastic Ban Enforcement: Ground Reality

- • The compostable exemption works — but creates a grey market. Assobioplastiche estimates ~25% of bags on the Italian market are illegal or non-compliant. Customs seized 9 tonnes of illegally imported Chinese plastic bags in October 2024.

- • Biorepack’s collection system is mature. Covers 85.5% of the Italian population, 74.3% of municipalities, with ~300 composting facilities producing 1.9 Mt compost/year. €12.7 million paid to local authorities in 2024.

- • Sector just contracted. 2024 turnover: €704 million, down 15% from 2023’s €828 million peak across 278 companies and 121,500 tonnes. Peak was €1 billion in 2021.

3.8.3 Italy’s Bioplastics Market Size and Manufacturers

- • Market position: Italy takes an estimated 40-50% of EU bioplastics demand by far the largest single market.

- • Novamont (Novara, fully owned by Versalis/Eni since 2023): 150,000 TPA Mater-Bi capacity, 100,000 TPA Origo-Bi biopolyesters. Bio-BDO production at Bottrighe di Adria. €414M turnover (2021), 1,400+ patents, B Corp certified.

- • Biorepack: Europe’s only EPR consortium for compostable packaging. Environmental contribution: €130/tonne (2024).

- • Import pressure: Cheap Asian PBAT and starch blends are undercutting domestic producers. Assobioplastiche flagged “pseudo-reusable” tableware circumvention and dumping at June 2025 forum.

Source: :contentReference[oaicite:0]{index=0}

3.8.4 Commentary and Insights

- • Italy’s compostable exemption is the single most important policy for bioplastics demand in Europe. It created a market where compostable alternatives replaced banned plastics at scale. No other EU country replicated this.

- • The Commission’s July 2024 infringement notice is the biggest risk. If Italy is forced to remove the exemption, demand for compostable SUP items could collapse overnight. PPWR’s August 2026 application date is the likely deadline for resolution.

- • Novamont/Versalis is the industrial backbone. At 150,000 TPA Mater-Bi plus 100,000 TPA biopolyesters, Novamont’s capacity is an order of magnitude larger than any other European bioplastics producer. Italy’s bioplastics story is largely a Novamont story.

- • The 15% revenue contraction in 2024 signals the market is either maturing or shrinking. Import competition, legal uncertainty around the exemption, and AGCM enforcement actions against Novamont itself suggest the peak may have passed.

3.8.5 Italy Opportunity Scorecard

| Factor | Score |

| Pillar 1: Regulatory Strength | 4.3 / 5 |

| 1A — Legal Framework Robustness | 4 |

| 1B — Ban Breadth (product categories) | 5 |

| 1C — Future Trajectory | 4 |

| Pillar 2: Enforcement Reality | 4 / 5 |

| Pillar 3: Market Opportunity Gap | 4 / 5 |

| Composite Score | 12.3 / 15 |

Verdict: Italy is Europe’s largest bioplastics market and the global proof-of-concept for how a compostable exemption can create real demand at scale. But the Commission’s infringement action and PPWR harmonisation create material risk. The 15% revenue decline in 2024, combined with import pressure from Asian producers, suggests the window of easy growth is closing. For an exporter, Italy remains the single best European market but one that requires careful positioning against both Novamont’s dominance and regulatory uncertainty.

3.9 GERMANY – Single-Use Plastic Ban: Market Opportunity Index

Composite Score: 11.0 / 15 | Global Rank: #4

Europe’s largest bioplastics production hub with strong administrative infrastructure and mature EPR, but no national regulatory push beyond the EU minimum.

3.9.1 Germany’s Single-Use Plastic Ban: Laws and Regulations

3.9.1.1 Key Laws Governing Germany’s Plastic Ban

- • SUP ban: The Einwegkunststoffverbotsverordnung (EWKVerbotsV) (in force 3 July 2021) transposes the EU SUP Directive’s Article 5 product bans. Einwegkunststoffkennzeichnungsverordnung (EWKKennzV) covers labelling.

- • Litter clean-up fund: The Einwegkunststofffondsgesetz (EWKFondsG) (effective 1 January 2024) created a fund administered by the Umweltbundesamt (UBA) via the DIVID platform. Projected at ~€434 million/year.

- • Packaging EPR: The Verpackungsgesetz (VerpackG) requires all packaging producers to register in the LUCID registry at the Zentrale Stelle Verpackungsregister (ZSVR). Plastic packaging recycling quota: 63%.

- • Penalties: Up to €100,000 for non-compliance.

Fund levy rates (per kg): Beverage cups €1.236, lightweight carrier bags €3.801, balloons €4.340, tobacco filters €8.972.

3.9.1.2 Which Plastic Items Are Banned in Germany?

- • Standard EU SUP Directive list: Cotton bud sticks, cutlery, plates, straws, stirrers, balloon sticks, expanded polystyrene food containers and cups, all oxo-degradable plastics.

- • Germany has not banned any additional items beyond the EU minimum. No fruit-and-veg packaging ban. No reusable dine-in mandate.

- • Mandatory deposit return on PET bottles and cans since July 2022. Tethered caps required since July 2024.

3.9.1.3 Germany’s Plastic Ban Timeline and Future Goals

- • EU PPWR (August 2026): Germany is preparing a Verpackungs-Durchführungsgesetz to implement PPWR, in consultation through December 2025. PPWR will bring HORECA reuse mandates and fruit/veg packaging bans that Germany does not currently have.

- • 2025: First EWKFonds levy payments due. 25% recycled content in PET bottles.

- • 2030: 30% recycled content in all SUP plastic bottles (EU target). PPWR recyclability requirements.

3.9.2 Germany’s Plastic Ban Enforcement: Ground Reality

- • Strong administrative infrastructure. The LUCID registry, dual-system collections (5.5 Mt from households in 2023), and established EPR machinery make Germany the most data-rich market in Europe.

- • Packaging waste: 19.0 Mt in 2022 (225 kg per capita, down 3.4% YoY). Plastic packaging recycling rate: 66-67%, which is among the highest in Europe.

- • Few published fines. Compliance is presumed high through regulatory design rather than aggressive prosecution.

3.9.3 Germany’s Bioplastics Market Size and Manufacturers

- • Plastic waste: ~6.15 Mt/year, ~46% recycling rate overall.

- • Bioplastics market share: Germany holds ~25-27% of the European bioplastics market (Mordor Intelligence) and is the largest production hub in Europe.

- • Key German bioplastics manufacturers: BASF (ecoflex PBAT and ecovio compounds at Ludwigshafen and Schwarzheide, ~74,000 TPA PBAT capacity; launched mass-balance “ecoflex BMB” under ISCC-PLUS), Biotec GmbH (Emmerich, starch-based compounds), FKuR (Willich — Bio-Flex, Biograde, Fibrolon, Terralene; distributes Braskem bio-PE). thyssenkrupp Uhde licenses the PLAneo PLA process.

European Bioplastics (Berlin) reports capacity growth from 2.47 Mt (2024) to 5.73 Mt by 2029. :contentReference[oaicite:0]{index=0}

3.9.4 Commentary and Insights

- • Germany is a production hub, not a demand-pull market. Its regulatory framework matches the EU minimum. Bioplastics demand in Germany is driven by brand-owner sustainability commitments and EU-wide regulation, not by German policy.

- • BASF’s ecoflex/ecovio makes Germany the PBAT capital of Europe. At ~74,000 TPA, BASF is the largest European PBAT producer. Combined with FKuR and Biotec, Germany’s position as production anchor is durable.

- • PPWR will be the forcing event. From August 2026, Germany will face reuse mandates and packaging bans it currently lacks. Adjustment should be smoother than in Southern or Eastern Europe due to existing infrastructure.

3.9.5 Germany Opportunity Scorecard

| Factor | Score |

| Pillar 1: Regulatory Strength | 4.0 / 5 |

| 1A — Legal Framework Robustness | 4 |

| 1B — Ban Breadth (product categories) | 3 |

| 1C — Future Trajectory | 5 |

| Pillar 2: Enforcement Reality | 5 / 5 |

| Pillar 3: Market Opportunity Gap | 2 / 5 |

| Composite Score | 11.0 / 15 |

Verdict: Germany’s score is strong on regulation and enforcement but weak on opportunity gap. The market is already well-served by Europe’s largest bioplastics producers. PPWR will tighten requirements from 2026, but German industry is best-positioned to absorb those changes. For outside entrants, this is a mature, competitive market.

3.10 SPAIN – Single-Use Plastic Ban: Market Opportunity Index

Composite Score: 10.3 / 15 | Global Rank: #6

Europe’s strongest plastic tax signal at €0.45/kg but without Italy’s composting infrastructure or France’s enforcement machinery.

3.10.1 Spain’s Single-Use Plastic Ban: Laws and Regulations

3.10.1.1 Key Laws Governing Spain’s Plastic Ban

- • Primary legislation: Ley 7/2022 (8 April 2022) transposes the SUP Directive. Real Decreto 1055/2022 implements packaging-specific EPR.

- • Lead ministry: MITECO. Fines: very serious infractions €100,001–€3.5 million, serious €2,001–€100,000.

- • Plastic packaging tax: €0.45/kg on non-recycled plastic in non-reusable packaging since January 2023. Projected revenue: ~€724 million/year. Recycled content exemptions require UNE-EN 15343 certification.

3.10.1.2 Which Plastic Items Are Banned in Spain?

- • EU SUP Directive standard list plus: BPA and phthalates banned in food packaging. HORECA must offer free tap water and accept reusable containers. Fresh fruit and vegetables under 1.5 kg must be sold loose.

- • No compostable exemption like Italy.

- • No reusable dine-in mandate like France.

3.10.1.3 Spain’s Plastic Ban Timeline

- • January 2024: Financial EPR obligations in force.

- • January 2025: Industrial/commercial packaging EPR.

- • EU PPWR (August 2026): Will layer additional HORECA reuse mandates and recycled content requirements.

3.10.2 Spain’s Plastic Ban Enforcement

- • Ecoembes runs household packaging EPR (1.5 Mt recycled in 2024). But Zero Waste Europe/Eunomia have credibly accused Ecoembes of overstating PET collection rates.

- • The €0.45/kg tax is the real enforcement lever — harder to evade than product bans. It creates a direct cost incentive to switch to recycled or bio-based materials.

- • Composting infrastructure is limited. Without Italian-scale organic waste collection, compostable bioplastics have constrained end-of-life options.

3.10.3 Spain’s Bioplastics Market Size and Manufacturers

- • Position: Fourth-largest European bioplastics consumer. No producer at Novamont’s scale.

- • Key players: AIMPLAS (Valencia — leading technology centre, 35+ pilot plants, coordinates EU projects). Venvirotech (Barcelona — PHA from organic waste via bacterial fermentation, BEO brand). ADBioplastics (Paterna — bio-based additives).

- • Import dependent for PLA and PBAT. Effectively 100% reliant on imports for commodity bio-resins.

3.10.4 Commentary and Insights

- • The €0.45/kg tax is Europe’s strongest fiscal signal outside the UK. It makes Spain attractive for bio-based packaging suppliers who can demonstrate recycled or renewable content.

- • No Italian-style compostable exemption limits the addressable market. Without an exemption allowing compostable cutlery and plates, demand is concentrated in bags and packaging rather than food service items.

- • AIMPLAS makes Spain a strong R&D partner geography but not a production base.

3.10.5 Spain Opportunity Scorecard

| Factor | Score |

| Pillar 1: Regulatory Strength | 4.3 / 5 |

| 1A — Legal Framework Robustness | 5 |

| 1B — Ban Breadth (product categories) | 4 |

| 1C — Future Trajectory | 4 |

| Pillar 2: Enforcement Reality | 3 / 5 |

| Pillar 3: Market Opportunity Gap | 3 / 5 |

| Composite Score | 10.3 / 15 |

Verdict: Spain’s plastic tax creates a genuine cost incentive for bioplastics, but the market lacks Italy’s compostable exemption and France’s enforcement apparatus. A strong R&D ecosystem (AIMPLAS) and full import dependence make it a viable secondary European market.

3.11 UNITED KINGDOM – Single-Use Plastic Ban: Market Opportunity Index

Composite Score: 9.7 / 15 | Global Rank: #9

Four separate jurisdictions, diverging ban timelines, and a powerful Plastic Packaging Tax — but fragmented enforcement and no national bioplastics production at scale.

3.11.1 UK’s Single-Use Plastic Ban: Laws and Regulations

3.11.1.1 Key Laws Governing the UK’s Plastic Ban

- • England: SI 2020/971 banned plastic straws, cotton buds, and stirrers (effective July 2021). SI 2023/982 (October 2023) added plates, cutlery, balloon sticks, and polystyrene food/drink containers.

- • Scotland: SSI 2021/373 is the broadest UK ban, covering manufacture and supply. In force August 2022. Maximum fine: £5,000. No fines issued as of mid-2023.

- • Wales: Single-use Plastic Products (Wales) Act 2023 — Phase 1 from October 2023, unlimited fines. Phase 2 (bags, polystyrene lids, oxo-degradables) delayed indefinitely per February 2026 Written Statement. Wet wipes ban: December 2026.

- • Northern Ireland: Bound to EU SUP via Windsor Framework but never formally transposed item bans. Wet wipes ban: May 2027.

3.11.1.2 Which Plastic Items Are Banned in the UK?

- • Across England, Scotland, Wales: Straws, stirrers, cotton buds (2020/21). Plates, cutlery, balloon sticks, polystyrene food containers (2023). Scotland also bans polystyrene cup lids.

- • Not banned: Plastic bags (subject to mandatory 10p charge in England since 2015, currently at 25p in Scotland and Wales). No ban on plastic packaging for fruit/veg. No reusable dine-in mandate.

- • Plastic Packaging Tax (UK-wide): £223.69/tonne (2025/26) on packaging with <30% recycled content. Revenue: £259 million (2024/25). 4,927 registered businesses.

3.11.1.3 UK’s Plastic Ban Timeline and Future Goals

- • October 2025: First pEPR (Extended Producer Responsibility) invoices. Plastic base fee: £423/tonne, which is highest of any material.

- • October 2027: Deposit Return Scheme across England, Scotland, Northern Ireland (PET, steel, aluminium). Wales runs a separate DRS including glass.

- • No 2040 zero-plastic target like France. UK’s trajectory depends on pEPR fee escalation and PPWR alignment for exports to EU.

3.11.2 UK’s Plastic Ban Enforcement: Ground Reality

- • Enforcement is light across all four jurisdictions. Scotland issued no fines in year one of its ban. English local authority enforcement data is minimal.

- • Scotland’s DRS collapsed. The planned August 2023 launch was abandoned. Circularity Scotland went into administration. Biffa is pursuing a ~£166 million compensation claim from the Scottish Government.

- • The Plastic Packaging Tax is the real enforcement lever. HMRC-administered, tax-based, and far harder to evade than a local trading standards prosecution. The taxable share fell to 38% in 2025, suggesting it’s driving reformulation toward recycled content.

3.11.3 UK’s Bioplastics Market Size and Manufacturers

- • Plastic waste: ~5 Mt/year total, 2.1–2.2 Mt plastic packaging waste. Recycling rate: 52.5%. Per-capita short-life plastic: 31.1 kg/year (vs. 20.9 kg global average).

- • UK bioplastics producers (scale-limited): Biome Bioplastics (Southampton), Floreon (Sheffield, PLA-based materials), Aquapak Polymers (Hydropol PVOH, ~50 kt capacity), Polymateria (London, biotransformation tech).

- • Import dependent for PLA and PBAT feedstocks. No large-scale bio-resin production.

Source: :contentReference[oaicite:0]{index=0}

3.11.4 Commentary and Insights

- • The £423/tonne pEPR fee is the UK’s most powerful bioplastics incentive. Combined with the Plastic Packaging Tax, the regulatory cost burden on virgin plastic is among Europe’s highest.

- • Four-jurisdiction fragmentation is a major market barrier. Different bans, DRS timelines, UKIMA complications, and Windsor Framework complexity create regulatory friction.

- • The UK is an importer, not a producer. This creates a supply gap but also makes the market highly price-sensitive and exposed to global resin pricing.

3.11.5 UK Opportunity Scorecard

| Factor | Score |

| Pillar 1: Regulatory Strength | 3.7 / 5 |

| 1A — Legal Framework Robustness | 4 |

| 1B — Ban Breadth (product categories) | 3 |

| 1C — Future Trajectory | 4 |

| Pillar 2: Enforcement Reality | 3 / 5 |

| Pillar 3: Market Opportunity Gap | 3 / 5 |

| Composite Score | 9.7 / 15 |

Verdict: The UK’s regulatory cost burden on conventional plastics (pEPR + Plastic Packaging Tax) is among Europe’s highest, creating genuine demand pull for alternatives. But four-jurisdiction fragmentation, weak enforcement, and lack of domestic production make it a complex, compliance-heavy market best suited for experienced exporters.

3.12 NETHERLANDS – Single-Use Plastic Ban: Market Opportunity Index

Composite Score: 9.3 / 15 | Global Rank: #12

Home to Avantium’s PEF and Corbion’s lactide platform; a bioplastics innovation hub, but domestic regulation is in flux and enforcement has been paused.

3.12.1 Netherlands’ Single-Use Plastic Ban: Laws and Regulations

- • Primary legislation: Besluit kunststofproducten voor eenmalig gebruik (Staatsblad 2021, 294) transposes the SUP Directive. Enforced by ILT (Human Environment and Transport Inspectorate).

- • SUP charge (July 2023): Guideline tariffs of €0.25/cup, €0.50/meal container, €0.05/small wrapper, including bioplastic items.

- • January 2024 ban: SUP cups and food packaging for on-site consumption in hospitality, canteens, festivals, sports clubs.

- • December 2024 reversal: Government narrowed scope and fixed €0.25 surcharge only on takeaway filled on-site from January 2026, exempting supermarkets and delivery.

- • Enforcement paused: State Secretary Aartsen instructed ILT not to enforce SUP surcharge rules through 31 December 2025.

- • Penalties: Up to ~€25,750 under the Economic Offences Act.

3.12.2 Netherlands’ Plastic Ban Enforcement

- • Enforcement is effectively suspended. The ILT non-enforcement instruction through end-2025 means compliance is voluntary for now.

- • McDonald’s Netherlands reportedly reintroduced plastic-coated paper cups for on-site service while charging €0.15/cup, to which the Fair Resource Foundation filed an enforcement request in November 2024. France’s McDonald’s reuse rate: 33.9% vs. Netherlands: 3.3%.

- • Policy is unstable. Rules enacted in 2023, partially reversed in 2024, narrowed again for 2026. Businesses face uncertainty.

3.12.3 Netherlands’ Bioplastics Market and Innovation

- • EPR body: Verpact (formerly Afvalfonds Verpakkingen). Reusable plastic cup fee: €0.28/kg. Small bottle deposit: €0.15.

- • Avantium (Amsterdam-listed): Opened 5 kt/year FDCA Flagship Plant at Delfzijl in October 2024. ~€175M capex. Commercial PEF sales (Releaf brand) expected Q1 2026. Full capacity within 24 months.

- • Corbion (Gorinchem HQ): Global lactic acid and lactide leader. TotalEnergies Corbion JV operates 75 kt/year Luminy PLA plant in Thailand, with lactide capacity at 100 kt/year.

- • Paques Biomaterials (Balk): Scaling PHA under Caleyda brand. €14M raised 2024. First commercial extraction Emmen 2026. Full-scale 6,000 TPA by 2028.

3.12.4 Commentary and Insights

- • Netherlands is an innovation hub, not a demand market. Avantium’s PEF, Corbion’s lactide, and Paques’ PHA represent next-generation bioplastics technology, but domestic consumption is modest.

- • Policy instability undermines the market signal. Businesses cannot plan when rules are enacted, paused, reversed, and narrowed within 18 months. Until enforcement resumes, the SUP regime is effectively voluntary.

3.12.5 Netherlands Opportunity Scorecard

| Factor | Score |

| Pillar 1: Regulatory Strength | 3.3 / 5 |

| 1A — Legal Framework Robustness | 3 |

| 1B — Ban Breadth (product categories) | 3 |

| 1C — Future Trajectory | 4 |

| Pillar 2: Enforcement Reality | 2 / 5 |

| Pillar 3: Market Opportunity Gap | 4 / 5 |

| Composite Score | 9.3 / 15 |

Verdict: The Netherlands punches far above its weight in bioplastics innovation (Avantium, Corbion, Paques) but underperforms on domestic regulation and enforcement.

3.13 SWEDEN – Single-Use Plastic Ban: Market Opportunity Index

Composite Score: 9.0 / 15 | Global Rank: #14

One of the rare EU countries to repeal a plastic tax — bag consumption already fell below targets. Strong on innovation, light on volume demand.

4. Compostable Plastics for Injection Moulding – Demand Drivers and Regulatory Landscape

Demand for compostable formats in injection-moulded categories is coming from two directions: brand owners responding to regulatory pressure, and a smaller but growing body of consumers willing to pay a premium for certified sustainable packaging. Of the two, regulation is the more reliable and durable signal.

3.13.1 Sweden’s Single-Use Plastic Ban: Laws and Regulations

- • Primary legislation: Förordning (2021:996) transposes the SUP Directive. Enforced by the Swedish EPA (Naturvårdsverket).

- • Section 14: Banned single-use cups with >15% plastic from January 2024.

- • Sections 17–22: Food/drink servers providing >150 cups/containers per open day must offer reusable alternatives (threshold drops to 75 from January 2026).

- • Section 24–25: 50% reduction target for SUP cups and food containers by 2026.

- • Penalties: Environmental sanction fees from SEK 5,000 for ≤100 products, scaling upward.

- • Sweden’s plastic bag tax (3 SEK/bag, introduced May 2020) was abolished 1 November 2024. Per-capita consumption had already fallen from 83 bags (2017) to 17 (2023), well below the EU 40-bag target.