Prepared by

Ukhi Research Division

Ukhi Bioplastics Private Limited

India

Report Highlights

This report covers the global sustainable packaging materials market across five material categories: paper and cardboard, bioplastics, recycled plastics, molded fiber and pulp, and emerging next-generation materials. Before reading, five things are worth knowing about what this report contains and how it is put together.

-

Market size data is presented as a range

For every material category, market size estimates from multiple research firms are compared side by side. Where estimates diverge significantly, the report explains why, including what definitional differences are driving the gap. Readers who have encountered conflicting market size figures elsewhere will find those conflicts addressed directly.

-

Every major geography is covered

Each chapter includes regional breakdowns for Asia-Pacific, Europe, North America, and Latin America.

-

The regulatory landscape is mapped concretely, with specific deadlines

Rather than describing regulation in general terms, the report identifies specific rules, the dates they apply, the formats they affect, and the markets they cover. This includes the EU PPWR, India’s Plastic Waste Management Rules, US state-level EPS bans, and the UK Plastic Packaging Tax.

-

Cost premiums are stated

The report does not present sustainable materials as cost-neutral alternatives. Where materials carry a significant price premium over conventional equivalents, that premium is stated with the source data behind it and the conditions under which it narrows.

-

The final chapter is structured for direct use by investors and procurement teams

The strategic chapter does not summarise the report. It draws out the investment thesis, identifies where capital is concentrated and where gaps exist, provides a practical material-switching framework, and maps the regulatory deadlines that require decisions now rather than later.

Publication Details

- Publication Date: May 2026

- Publisher: Ukhi Bioplastics Private Limited

- Location: New Delhi, India

- Report Period Covered: Regulatory and market data current as of Q1 2026

- Data Last Updated: 5th May, 2026

Disclaimer

- This report was produced by Ukhi, a bioplastics company based in India with a commercial interest in one of the five material categories covered. While every effort has been made to ensure consistent and impartial treatment across all categories, readers should be aware of this relationship when interpreting the analysis.

- The market size figures, growth forecasts, and CAGR projections presented throughout this report are drawn from third-party market research publications, industry association data, company disclosures, and publicly available sources. Ukhi has not independently verified these figures. Where estimates vary between sources, the range is presented and the reasons for variation are explained, but no warranty is made as to the accuracy, completeness, or reliability of any third-party data reproduced here.

- All forward-looking statements, including market forecasts, cost parity timelines, and regulatory implementation schedules, are projections based on information available at the time of publication. Actual outcomes may differ materially from those projected. Market conditions, regulatory developments, and technology trajectories can change in ways that are not reflected in the data presented here.

- Nothing in this report constitutes investment advice, financial advice, or a recommendation to buy, sell, or hold any security or asset. Investors should conduct their own due diligence and seek independent professional advice before making any investment decision based on information contained in this report.

- Nothing in this report constitutes legal or regulatory compliance advice. Regulatory information is presented for informational purposes only. The regulatory landscape for packaging materials is evolving rapidly, and specific rules, deadlines, and requirements should be verified against official sources and reviewed by qualified legal counsel before being relied upon for compliance purposes.

- The report was finalised in May, 2026. Regulatory status, company funding positions, market data, and technology readiness assessments reflect information available at that date and may have changed since publication.

- The mention of specific companies, products, certifications, or technologies in this report does not constitute an endorsement by Ukhi of those companies, products, certifications, or technologies, nor does it imply any commercial relationship unless explicitly stated.

Executive Summary

The global sustainable packaging market is one of the most consequential industrial transitions of the current decade. Driven primarily by regulation rather than consumer choice, it is reshaping supply chains across food and beverage, electronics, personal care, pharmaceuticals, and e-commerce simultaneously.

This report covers five material categories that together constitute the core of the sustainable packaging materials market: paper and cardboard, bioplastics, recycled plastics, molded fiber and pulp, and emerging next-generation materials.

Across these five categories, the total addressable market exceeded USD 500 billion in 2025, with the paper and cardboard segment alone accounting for USD 410 to 480 billion.

The remaining four categories range from early-commercial to fully scaled, with individual market sizes from USD 85 million (mycelium packaging) to USD 14 to 20 billion (bioplastics), depending on scope and definition.

The structural driver for this market is regulatory.

- The EU Packaging and Packaging Waste Regulation applying from August 2026

- India’s Plastic Waste Management Rules mandating rising recycled content thresholds to 60% by 2028-29

- 12 US state EPS bans already in force

- The UK Plastic Packaging Tax

Together, these regulations are removing legal alternatives for buyers.

For investors and procurement teams, this means the relevant question is whether supply of sustainable packaging can scale to meet it on the regulatory timeline.

Key Findings

Across every material category in this report, the primary demand signal is a legal mandate or financial penalty on conventional alternatives, not organic consumer pull.

The EU SUP Directive banning EPS food containers, India’s single-use plastic ban covering 19 item categories, and EPR recycled content thresholds all create compliance demand that is structurally different from discretionary purchasing.

Revenue tied to regulatory mandates is more durable than revenue tied to consumer sentiment, but it is also binary: if supply cannot meet mandated demand on the regulatory schedule, the market does not clear smoothly.

With a global market of USD 410 to 480 billion in 2025 and a 4.6 to 5.0% CAGR, paper and cardboard is by far the largest sustainable packaging category. But the carbon case for paper is application-dependent.

Peer-reviewed lifecycle analysis finds that even traditional plastics have lower greenhouse gas emissions than paper in 13 of 14 packaging applications studied.

Paper wins on end-of-life metrics, recyclability infrastructure, and consumer perception. Brands switching to paper primarily for carbon credentials without functional-unit LCA data are taking a position the evidence does not always support.

The global bioplastics packaging market reached USD 8 to 14 billion in 2024 and is growing at 14 to 17% CAGR.

Within the category, PHA is the only mainstream bioplastic that is both bio-based and home compostable, and in some formulations marine biodegradable.

PLA is industrially compostable but does not biodegrade in home compost or soil. Bio-PE and bio-PET are bio-based but not biodegradable at all.

The common conflation of these sub-categories in sustainability claims creates significant greenwashing exposure for brands that do not distinguish between them.

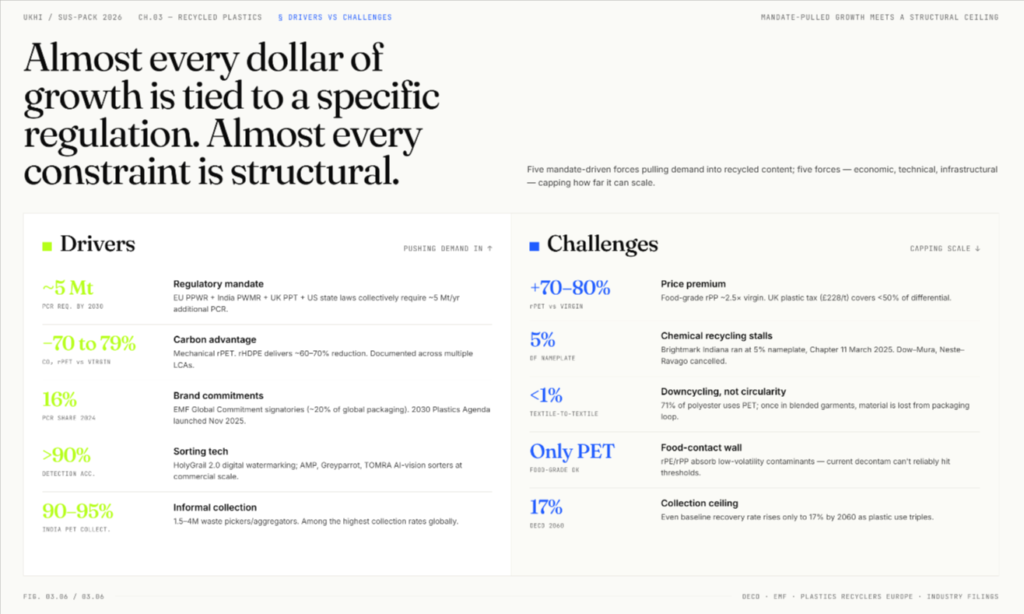

rPET commanded a 70 to 80% premium over virgin PET in mid-2025 despite years of regulatory-driven demand growth. Food-grade rHDPE runs 200 to 300% above virgin in the US.

Chemical recycling, widely expected to close the supply gap, has had a difficult 2024 to 2025:

- Brightmark filed for bankruptcy,

- Dow cancelled its flagship Böhlen plant, and

- Neste cancelled its Vlissingen project.

Eastman’s Kingsport facility is the clearest commercial success, and it works because of long-term offtake contracts, not technology alone.

Mechanical recycling will remain the primary workhorse for recycled plastics through at least 2030.

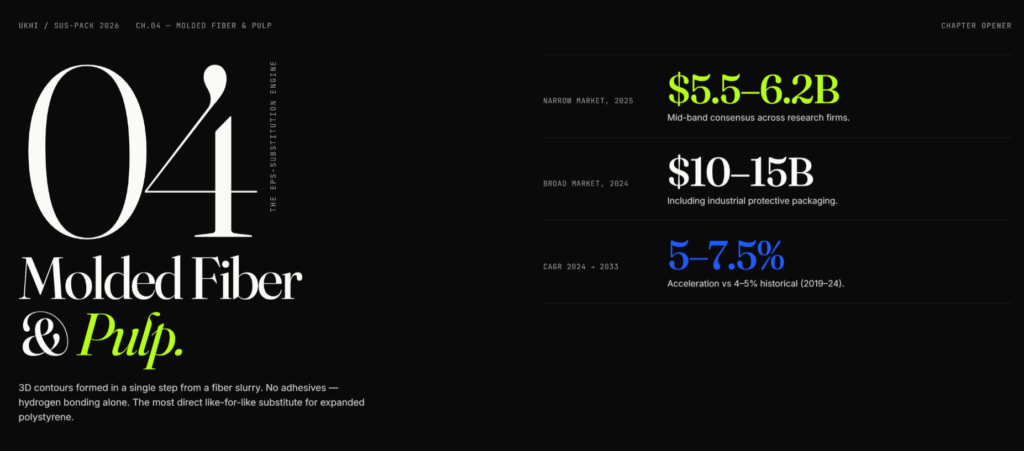

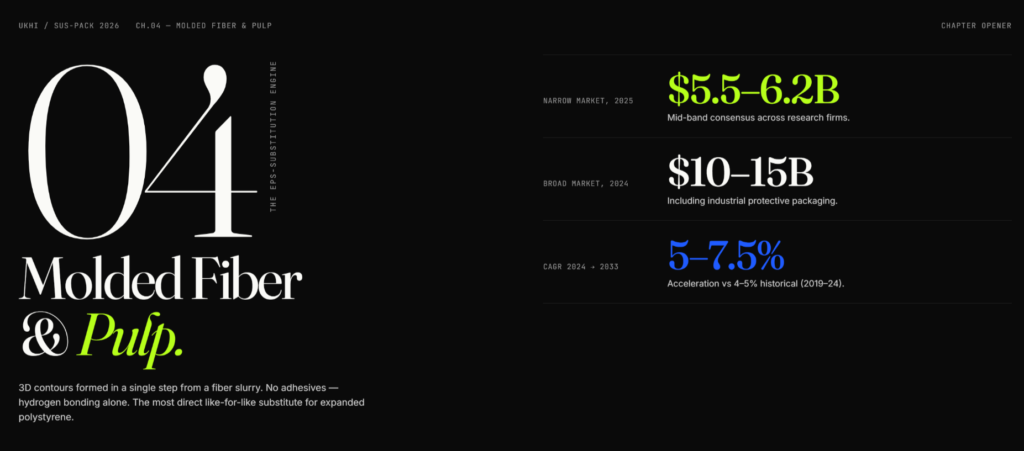

The global molded fiber packaging market is USD 5.5 to 6.2 billion in 2025 on the narrow definition, growing at 5 to 7.5% CAGR.

Electronics brands including Apple, Samsung, and Amazon have made durable, supply-chain-level commitments to molded fiber.

The PFAS-in-food-service issue is the category’s most significant near-term risk: testing has found fluorine in roughly two-thirds of sampled fiber food containers.

Producers that complete the transition to certified PFAS-free barrier chemistry before the EU PPWR’s August 2026 deadline will hold a meaningful compliance advantage.

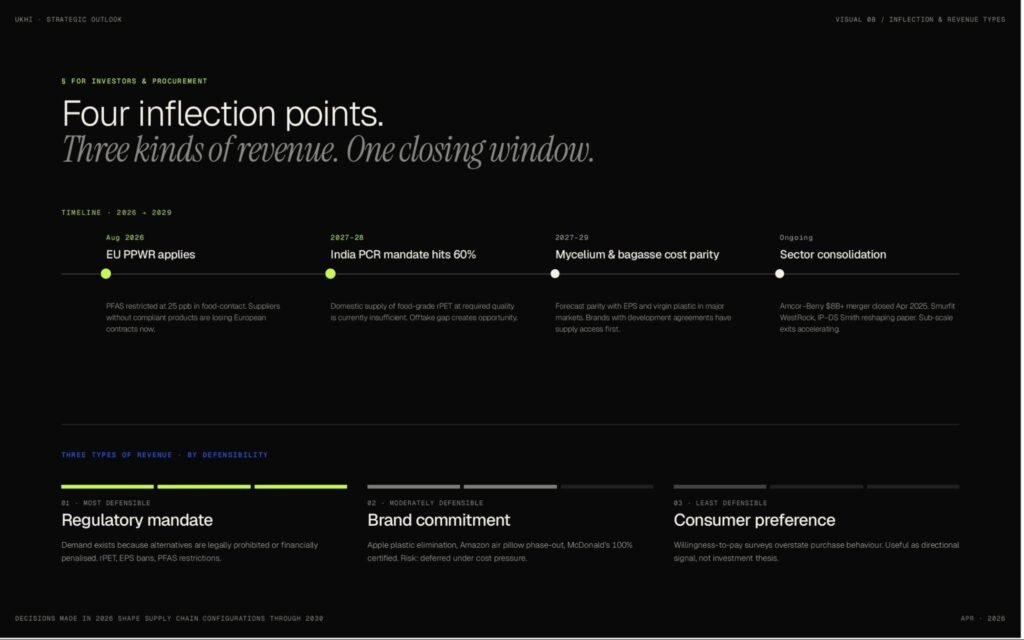

The window between August 2026 and 2030 will determine which sustainable packaging formats become standard supply and which remain niche.

The PPWR recyclability deadline, India’s 60% PCR mandate, the first post-PFAS regulatory cycle, and cost-parity arrival for mycelium and bagasse composites will all resolve in this period.

Procurement teams that map their current packaging formats against these deadlines now, and investors that distinguish between regulatory-mandate revenue and consumer-preference revenue, will be in a structurally stronger position than those treating these as distant sustainability questions.

About This Report

This is a comprehensive market sizing and analysis report covering the global sustainable packaging materials landscape.

It covers five material categories: paper and cardboard packaging, bioplastics, recycled plastics, molded fiber and pulp, and emerging next-generation packaging materials.

Each chapter addresses market size, growth trajectory, geographic distribution, key applications, and the drivers and challenges shaping each category.

This report is intended for four audiences:

- procurement and packaging decision-makers at brands evaluating material options;

- investors and analysts assessing the sustainable packaging space;

- sustainability and ESG professionals tracking regulatory and market developments; and

- industry participants mapping the competitive landscape.

Each chapter is structured to be useful to all four, with the strategic chapter at the end addressing investors and procurement teams directly.

Scope and Boundaries

What this report covers

The report analyses five material families within the sustainable packaging market:

- Paper and cardboard packaging — corrugated board, folding cartons, kraft paper, liquid paperboard, and paper-based flexible packaging

- Bioplastics packaging — PLA, PHA, PBAT, starch blends, and bio-based drop-in plastics (bio-PE, bio-PET)

- Recycled plastics packaging — mechanically and chemically recycled rPET, rHDPE, rPP, and other post-consumer resin (PCR) streams

- Molded fiber and pulp packaging — wet-formed and dry-formed products from wood pulp, sugarcane bagasse, bamboo, wheat straw, and other agricultural fiber feedstocks

- Emerging and next-generation materials — mycelium composites, seaweed and algae-based materials, nanocellulose films, protein-based films, chitosan, and agri-waste structural composites

The report covers global markets with specific geographic breakdowns for Asia-Pacific, Europe, North America, and Latin America.

The forecast horizon is 2026 to 2035. Market sizing figures use 2024 or 2025 as the base year, depending on the most recent data available for each category. All monetary figures are in US dollars unless explicitly noted. India-specific figures are sometimes presented in Indian rupees (INR) where the source data is in that currency.

What this report does not cover in depth

- Glass and metal packaging are not covered. Both are mature, highly recyclable categories with established infrastructure, and neither is experiencing the regulatory disruption or rapid material innovation that characterises the five categories above.

- Reusable packaging systems are addressed as a concept within the three-axis framework in Chapter 2 but are not analysed as a standalone market. Reuse is a system model, not a material — it can apply to glass, plastic, metal, or fiber. A separate analysis of the refill and reuse economy would require different framing and data sources.

- The report does not address active and intelligent packaging (sensors, freshness indicators, RFID) except where these technologies intersect with emerging bio-based materials.

- Packaging machinery, equipment, and services are outside scope.

Methodology

How we handle market size estimates

The most significant methodological challenge in writing a market sizing report for sustainable packaging is that the numbers disagree.

The molded fiber packaging market is cited at USD 5.5 billion by IMARC Group and at USD 14.84 billion by Mordor Intelligence for approximately the same year.

The bioplastics market ranges from under USD 10 billion to over USD 20 billion depending on the research firm.

These are not data quality failures; instead they reflect genuine differences:

- whether the “market” being measured is production capacity, sales value, or end-product value;

- whether the scope is global or regional;

- whether adjacent materials are included or excluded; and

- what counting methodology is applied to multi-material packaging structures.

Our approach throughout this report is to present the range rather than arbitrarily select a single figure. Where consensus exists across multiple research firms, we note it. Where the spread is wide, we explain what is driving the difference.

For each material category, a comparison table of estimates across research firms is included so readers can see the dispersion and understand which definitions produce which numbers.

We do not endorse any single research firm’s methodology. We treat market research reports as useful triangulation tools, not as ground truth.

The most reliable estimates in any given category are those that have convergent outputs across multiple independent firms, that cite their scope definitions clearly, and that are consistent with company-level revenue data and production statistics where those are available.

How we use the three-axis framework

The report organises all sustainable packaging analysis using a three-axis framework established in Chapter 2.

The three dimensions are material (what the package is physically made of), end-of-life property (what happens to it after use), and system or business model (how the packaging flows through the economy).

This framework is not unique to Ukhi, but it is not consistently applied in most industry analysis, which routinely conflates the three dimensions.

- “Compostable packaging” is incorrectly treated as a peer category of “bioplastics” in many market reports, when compostability is actually an end-of-life property that some bioplastics have and others do not.

- “Reusable packaging” is treated as a material category when it is a system model.

These conflations produce analytical errors that show up as misleading comparisons, double-counting, and incoherent market sizing.

Currency, base years, and data recency

- All global market sizes are reported in US dollars.

- Where data is available for both 2024 and 2025, the more recent figure is used.

- CAGR figures are drawn from the research firm source cited and cover the period stated in that source, which varies between firms.

- Readers comparing CAGRs across categories should check the base and end years, as a CAGR covering 2022 to 2030 is not directly comparable to one covering 2025 to 2033 even if the percentage appears similar.

- Company-level data is sourced from company disclosures, stock exchange filings, and verified press releases wherever possible.

1. Understanding Sustainable Packaging

1.1 What Is Sustainable Packaging?

Sustainable packaging is an umbrella term that covers any packaging designed, sourced, manufactured, and managed to reduce its environmental impact across its entire life cycle, right from raw material extraction through to disposal or recovery.

The most widely referenced definition of sustainable packaging comes from the Sustainable Packaging Coalition (SPC), an industry body hosted by GreenBlue.

Sustainable Packaging Definition — Sustainable Packaging Coalition (SPC)

SPC defines sustainable packaging through eight criteria that a package should work toward simultaneously.

These are:

- It is beneficial, safe, and healthy for individuals and communities throughout its life cycle.

- It meets market criteria for both performance and cost.

- It is sourced, manufactured, transported, and recycled using renewable energy.

- It optimises the use of renewable or recycled source materials.

- It is manufactured using clean production technologies and best practices.

- It is made from materials that remain healthy in all probable end-of-life scenarios.

- It is physically designed to optimise materials and energy.

- It is effectively recovered and utilised in biological and/or industrial closed-loop cycles.

The SPC frames this as a direction of travel, not a destination. No package is “sustainable” in absolute terms. It can only be more or less sustainable than the alternatives.

Sustainable Packaging Definition — Ellen MacArthur Foundation (EMF)

The Ellen MacArthur Foundation (EMF) takes a different but complementary approach.

Rather than defining sustainable packaging directly, EMF frames packaging within the circular economy, which is a system built on three principles:

- eliminate waste and pollution,

- keep products and materials in use at their highest value,

- and regenerate natural systems.

EMF’s New Plastics Economy Global Commitment, now signed by over 1,000 organisations, sets a concrete target: all plastic packaging should be reusable, recyclable, or compostable, and actually reused, recycled, or composted in practice.

Ukhi Definition — Sustainable Packaging:

Packaging that is designed and managed to minimize environmental impact across its full life cycle, through responsible sourcing, efficient use of materials, and effective recovery after use.

A common source of confusion is the relationship between sustainable packaging, green packaging, and eco-friendly packaging.

In practice, these terms are often used interchangeably in marketing, but they carry different levels of rigour.

- “Sustainable packaging” implies a life-cycle perspective.

- “Green packaging” and “eco-friendly packaging” are vague, and regulators have taken notice of this.

The U.S. Federal Trade Commission’s Green Guides explicitly warn that broad, unqualified claims like “green” or “eco-friendly” are difficult if not impossible to substantiate and should not be used without clear qualification.

The EU’s Green Claims Directive (in force from 2026) goes further, requiring that any environmental claim made about a product (including packaging) be backed by a recognised scientific methodology and independently verified before it can appear on a label.

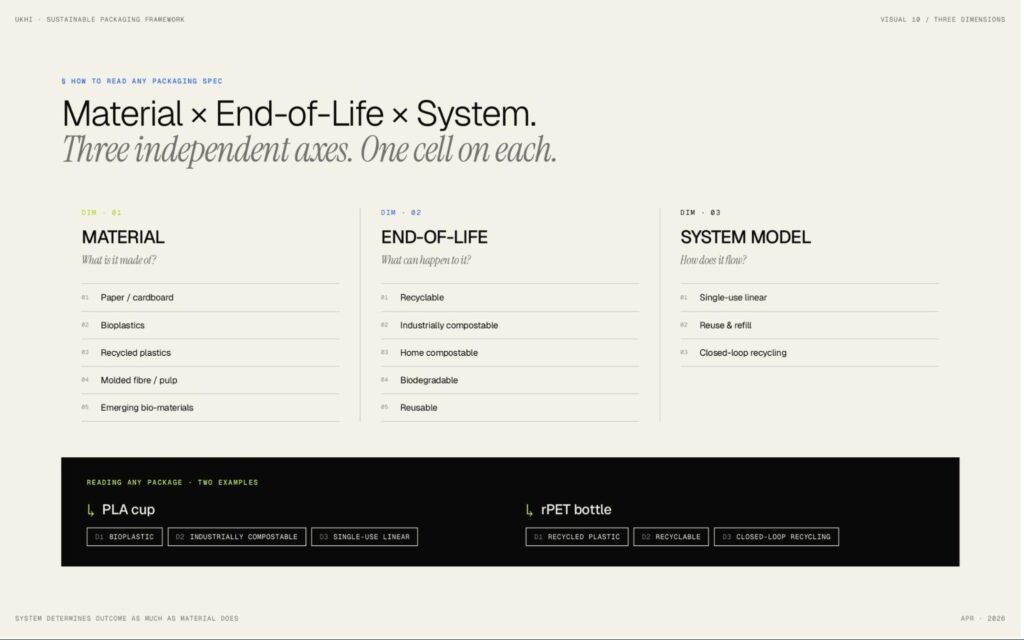

1.2 The Three Dimensions of Sustainable Packaging

To understand what sustainable packaging actually entails, it helps to think of it along three independent dimensions.

Each dimension describes a different aspect of a package — what it is made of, what can happen to it after use, and how it moves through the economy.

Dimension 1: Material — What Is the Packaging Made Of?

This is the most concrete dimension of sustainable packaging, as it asks a physical question: what substance is this package made from?

There are five major material categories across sustainable packaging:

- Paper and cardboard — Renewable, fiber-based materials including corrugated board, folding cartons, kraft paper, and paperboard. These are the most established sustainable packaging materials by market size.

-

Bioplastics — Plastics that are either bio-based (which means they are derived from biological feedstocks like corn, sugarcane, or cellulose), biodegradable (not the same as bio-based), or both.

Major types of bioplastics include PLA (polylactic acid), PHA (polyhydroxyalkanoates), PBAT, starch blends, and bio-based “drop-in” plastics like bio-PE and bio-PET.

-

Recycled plastics — Conventional plastic resins (PET, HDPE, PP) that incorporate post-consumer recycled (PCR) content.

Key forms include rPET (recycled PET), rHDPE, and output from chemical recycling processes.

-

Molded fiber and pulp — Packaging formed from wet or dry pulp using agricultural residues such as bagasse (sugarcane fiber), wheat straw, bamboo, or recycled paper pulp.

Common products include clamshells, trays, and protective packaging inserts.

-

Emerging bio-materials — Next-generation materials at early commercial or pre-commercial stages.

These include mycelium composites (grown from fungal root networks), seaweed-based films, agricultural waste composites, and edible coatings.

Key Insight:

Not all bioplastics are biodegradable, and not all biodegradable plastics are bio-based.

For example:

- Bio-PE (bio-based polyethylene) is made from sugarcane but behaves identically to fossil-based PE. It is recyclable, not biodegradable.

- PBAT is fossil-based but is biodegradable and industrially compostable.

So, in bioplastics, the feedstock origin and the end-of-life behavior are independent properties.

Dimension 2: End-of-Life Property — What Happens To A Package After Use?

This dimension describes what can happen to packaging once the consumer is finished with it. Although it is a property of a material and the design of the packaging, it is not a category parallel to materials.

The key end-of-life pathways for packaging are:

- Recyclable — This means a package can be collected, sorted, and reprocessed into new material. Recyclability is not just a material trait. It depends on three things working together:

- the design of the packaging (no problematic additives or multi-material layers),

- collection access (the U.S. FTC Green Guides state that for a company to make an unqualified “recyclable” claim on its packaging, at least 60% of the population where the product is sold must have access to facilities that actually collect and process that material),

- and the existence of end markets willing to buy the recovered material for remanufacturing.

- Industrially compostable — The package breaks down in a controlled commercial composting facility at temperatures of 55–75°C. The compostability of a packaging material is governed by two main standards:

EN 13432 (Europe) requires that:

- at least 90% of the material biodegrades into CO₂ within 180 days under controlled composting conditions,

- 90% of the material disintegrates into fragments smaller than 2mm within 12 weeks, and the resulting compost shows no eco-toxicity (tested via plant growth assays), and

- heavy metal concentrations remain below specified limits.

ASTM D6400 (North America) sets substantially similar requirements:

- 90% biodegradation within 180 days, 90% disintegration, and eco-toxicity and heavy metal limits.

- Home compostable — The package breaks down at ambient temperatures (20–30°C) in a garden compost bin, typically within 12 months. There is no globally harmonized standard for home-compostability as of 2026. The main references are:

- Australia’s AS 5810

- France’s NF T 51-800

- TÜV Austria’s OK compost HOME scheme

Note: PLA, despite being widely marketed as compostable, generally requires industrial temperatures and does not home compost.

- Biodegradable — The material will eventually break down through natural biological processes. However, “biodegradable” does not specify the timeframe or the conditions required.

For context, wood is biodegradable, but a wooden structure can last centuries. This is why regulators treat the term with caution: the U.S. FTC Green Guides state that a company can only make an unqualified “biodegradable” claim if the product will completely decompose within one year after customary disposal.

Since most packaging ends up in landfill (where decomposition conditions are anaerobic and slow), very few products can legitimately meet this standard. Without specifying the environment, temperature, and timeframe, calling a package “biodegradable” communicates almost nothing useful to the buyer.

- Reusable — The package is designed and supported by a system for multiple use cycles.

Under ISO 18603, a package only qualifies as reusable if three conditions are met:

- it has a designed minimum number of trips or rotations it can withstand,

- there is an operating system for collecting and reconditioning it after each use, and

- there is a control mechanism to track and manage the process.

This means that simply repurposing a jar as a pencil holder, or using a sturdy bag a few extra times before discarding it, does not qualify as reuse in any regulatory or standards-based sense. The system has to exist, not just the intention.

‘Biodegradable’ vs ‘Compostable’:

All compostable materials are biodegradable, but not all biodegradable materials are compostable. The difference is rigour.

- break down within a defined timeframe (180 days for industrial composting),

- at a defined temperature range (55–75°C),

- into fragments smaller than 2mm within 12 weeks,

- leave behind no toxic residue (verified through plant growth tests), and

- pass independent third-party certification.

“Biodegradable,” by contrast, simply means the material will break down at some point, under some conditions, over some undefined period.

A product labelled “biodegradable” with no further qualification gives a procurement team or a consumer no actionable information about what will actually happen to that package after disposal.

Dimension 3: System Model — How Does the Packaging Flow Through the Economy?

This dimension is about the business and logistics model that governs a packaging type, not the materials it is made of, or their chemistry thereof.

Three system models exist:

- Single-use linear — The package is used once and disposed of. This is still the default for the vast majority of packaging worldwide. The environmental outcome depends entirely on what happens at disposal — recycling, composting, landfill, or leakage into the environment.

- Reuse and refill — The package is returned, cleaned, and refilled for another use cycle.

The Ellen MacArthur Foundation identifies four reuse models:

- refill at home (concentrated cleaning products, subscription milk),

- refill on the go (in-store bulk dispensers),

- return from home (collected at the doorstep), and

- return on the go (deposit return schemes, reusable cup systems).

Reuse applies across materials; glass bottles, steel containers, durable plastic crates, and even paper-based systems can all be designed for reuse.

- Closed-loop recycling — The material is recovered and reprocessed into the same application it came from.

Bottle-to-bottle rPET is the canonical example. This is distinct from “downcycling,” where recovered material goes into a lower-value application (PET bottles becoming polyester fiber, for instance), which is a path that delays but does not prevent the material from becoming waste.

The critical point is that system model is independent of material.

A glass bottle in a deposit return scheme is reusable. The same glass bottle sold with no return infrastructure is single-use linear.

A PLA cup in a city with industrial composting infrastructure has a viable circular pathway. The same PLA cup in a city without that infrastructure ends up in landfill, where it will not compost.

So, the system determines the outcome as much as the material does.

Why These Dimensions Get Conflated — and Why It Matters

- Bioplastic ≠ biodegradable.

- Biodegradable ≠ compostable.

- Recyclable ≠ recycled.

- Reusable ≠ durable.

Any single package sits in one cell on each of the three dimensions simultaneously.

A PLA cup is (Material: bioplastic) × (End-of-life: industrially compostable) × (System: single-use linear, routed to industrial composting).

A rPET bottle is (Material: recycled plastic) × (End-of-life: recyclable) × (System: closed-loop recycling).

Reading packaging through this three-dimensional lens prevents the category errors that otherwise dominate sustainability reporting.

For the rest of this report, we use material as the primary organising dimension. Each subsequent chapter analyses one material category in depth.

This keeps the analysis grounded in the physical and commercial reality of what packaging is made from, while recognising that material choice alone does not determine sustainability, and the infrastructure, regulation, and systems around it matter just as much.

2. Global Sustainable Packaging Market — Size, Growth & Outlook

2.1 Global Sustainable Packaging Market Size

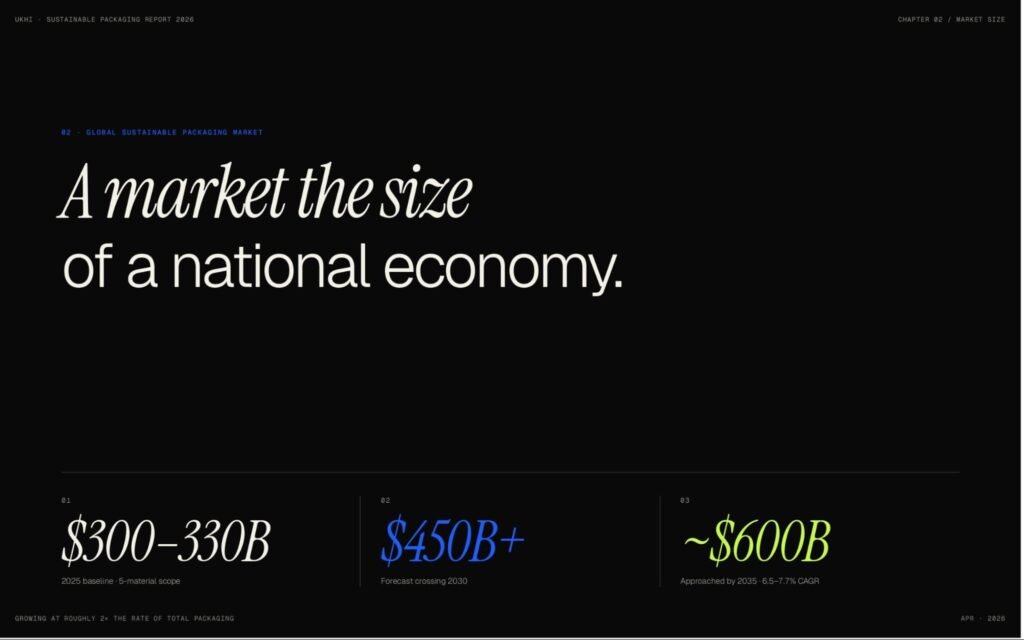

The global sustainable packaging market size was in a band of USD 280–330 billion as of 2025, based on estimates from more than a dozen independent research firms.

This makes sustainable packaging one of the largest and fastest-growing segments within the broader global packaging industry, which Smithers valued at USD 1.23 trillion in 2024.

The range of estimates is wide, from USD 127 billion (Precedence Research) at the low end to USD 498 billion (Market Research Future) at the high end.

This roughly four-fold spread is almost entirely an artefact of scope, as firms that include all paper and cardboard packaging, recycled-content conventional plastics, glass, and metal arrive at higher figures.

Firms that count only the “substituted sustainable share” (packaging that actively replaces a conventional alternative) arrive at lower figures.

Neither approach is wrong; but they are answering different questions about what “sustainable” includes.

For this report, the scope covers five material categories:

- paper and cardboard,

- bioplastics,

- recycled plastics,

- molded fiber, and

- emerging bio-materials.

We exclude recycled glass and recycled metal.

On this basis, the global sustainable packaging market size for 2025 is USD 300–330 billion.

Sustainable Packaging Market Size Estimates by Research Firm

| Research Firm | Market Size Estimate | Forecast | CAGR |

|---|---|---|---|

| Mordor Intelligence (Jan 2026) | USD 303.8B (2025) | USD 463.4B by 2031 | 7.29% |

| Grand View Research | USD 289.0B (2024) | USD 448.5B by 2030 | 7.6% |

| Straits Research | USD 283.4B (2024) | USD 552.5B by 2033 | 7.7% |

| Towards Packaging | USD 313.7B (2025) | USD 594.5B by 2035 | 6.6% |

| Persistence Market Research | USD 280.3B (2025) | USD 493.0B by 2032 | 8.4% |

| Fortune Business Insights | USD 374.9B (2025) | USD 552.45B by 2033 | 6.70% |

| BCC Research | USD 278.1B (2023) | USD 391.1B by 2029 | 6.0% |

Note: Fortune Business Insights uses a broader scope that includes glass and metal packaging. BCC Research uses a conservative scope and an earlier base year.

Insight — Why Market Size Estimates Vary So Widely:

The single biggest variable is whether all paper packaging gets counted as “sustainable.”

This one decision swings the global sustainable packaging market size by USD 150–200 billion.

The second largest variable is whether recycled-content conventional plastic (a PET bottle with 30% rPET, for example) counts as fully sustainable or only the recycled portion counts.

Readers comparing estimates across firms should always check the scope definition before drawing conclusions.

Historical Growth

Working back from the 2025 baseline, the sustainable packaging market has roughly doubled in a decade.

The compound annual growth rate from 2015 to 2025 has been approximately 7–8%, consistently outpacing the total packaging market’s 3.5–4% growth rate over the same period.

Eight inflection points have shaped the trajectory of global sustainable packaging market growth:

- 2015 — The EU Circular Economy Action Plan established the policy direction that would drive European sustainable packaging demand for the next decade.

- 2018 — The Ellen MacArthur Foundation and UNEP launched the New Plastics Economy Global Commitment with 250+ initial signatories, which created the first large-scale voluntary framework for corporate packaging targets.

- July 2021 — The EU Single-Use Plastics Directive entered force, banning 10 single-use plastic items and mandating 25% recycled content in PET bottles by 2025, rising to 30% by 2030.

- April 2022 — The UK Plastic Packaging Tax took effect at £200 per tonne on packaging with less than 30% recycled content.

- July 2022 — India’s single-use plastic ban targeting 19 specific items came into force under the Plastic Waste Management Amendment Rules.

- 2022–2024 — Five U.S. states enacted Extended Producer Responsibility (EPR) laws for packaging: California (SB 54), Maine, Oregon, Colorado, and Minnesota.

-

2024–2025 — A major consolidation wave reshaped the industry:

- Smurfit Kappa merged with WestRock (USD 34 billion),

- International Paper acquired DS Smith (USD 7.2 billion),

- Amcor merged with Berry Global, and

- Novolex acquired Pactiv Evergreen.

-

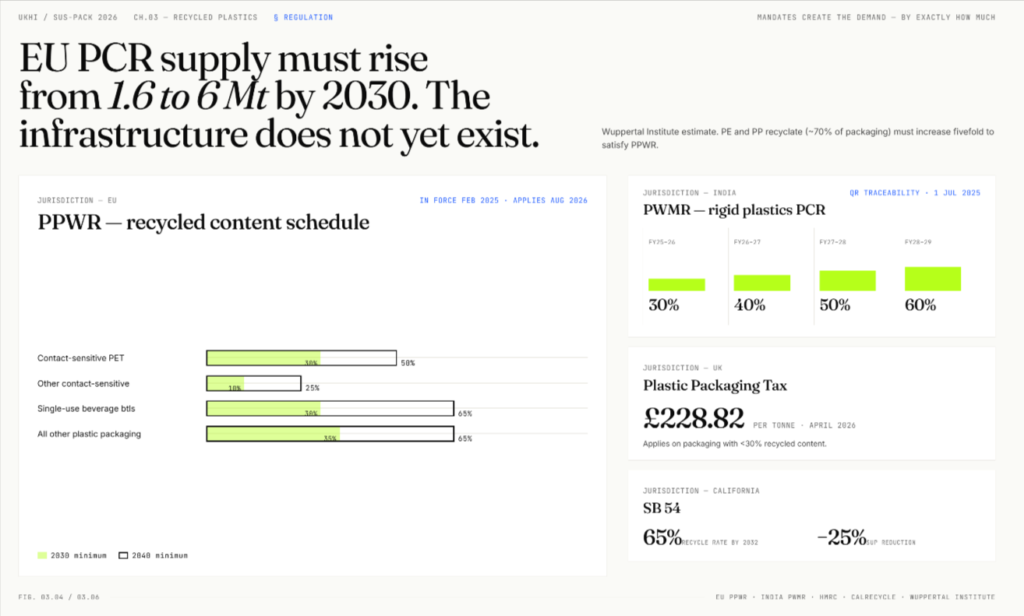

February 2025 — The EU Packaging and Packaging Waste Regulation (PPWR) entered force, mandating 30% recycled content for PET food packaging by 2030, banning intentionally added PFAS in food-contact packaging, and setting binding reuse targets.

General application begins August 2026.

The market grew through the 2020–2021 pandemic at roughly 6–8% annually as e-commerce volumes more than offset disruption to reusable packaging systems.

Smithers reported total packaging demand up 5.8% year-on-year during 2018–2021, with sustainable formats growing faster than the average.

2.2 Sustainable Packaging Market Forecast: 2025–2035

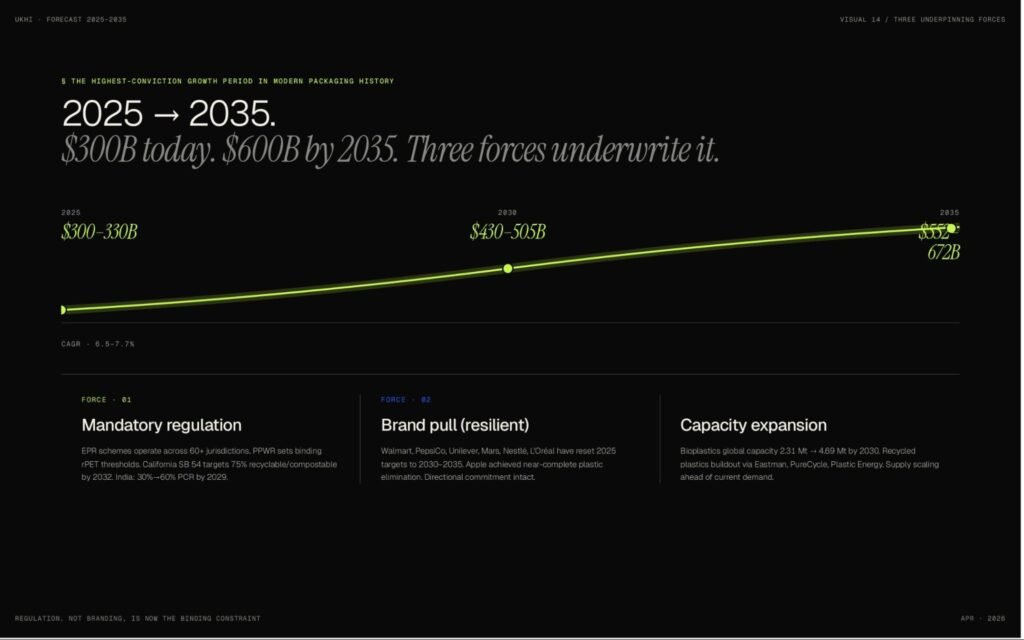

The forward decade is the highest-conviction growth period in the modern history of packaging.

The sustainable packaging market forecast clusters around three ranges:

- By 2030: USD 430–505 billion

- By 2035: USD 552–672 billion

- CAGR through the period: 6.5–7.7%

Three forces underpin this forecast.

Regulation has shifted from voluntary to mandatory.

- Extended Producer Responsibility schemes now operate across 60+ jurisdictions globally.

- The EU PPWR sets binding recycled-content thresholds across all packaging types.

- California’s SB 54 targets 75% recyclable or compostable packaging by 2032.

- India’s recycled content mandate for rigid plastics started at 30% in April 2025 and rises to 60% by 2029.

Brand commitments continue to pull sustainable formats into procurement, even when timelines slip.

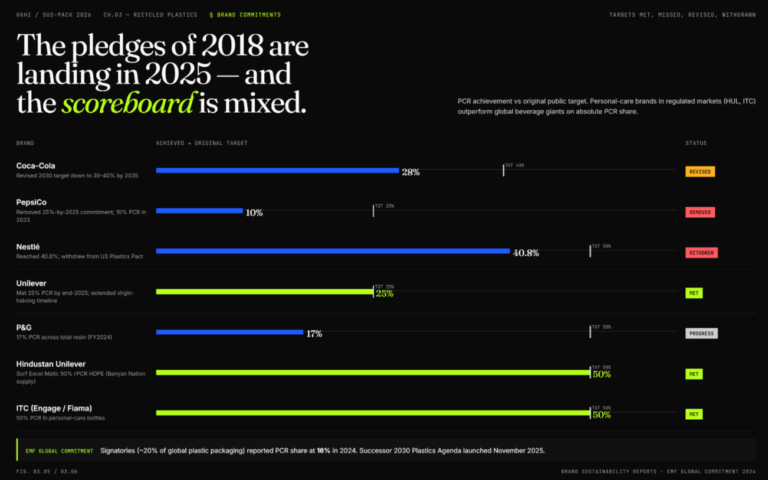

- Walmart, PepsiCo, Unilever, Mars, Nestlé, and L’Oréal have all either missed or reset their 2025 packaging targets, pushing deadlines to 2030 or 2035.

- Several of these companies have exited the U.S. Plastics Pact.

But the directional commitment remains intact, and the regulatory environment now means that even if voluntary pledges weaken, mandatory requirements will fill that gap.

Apple is the standout success story, achieving near-complete plastic packaging elimination ahead of its end-2024 target.

Production capacity for sustainable materials is expanding faster than current demand.

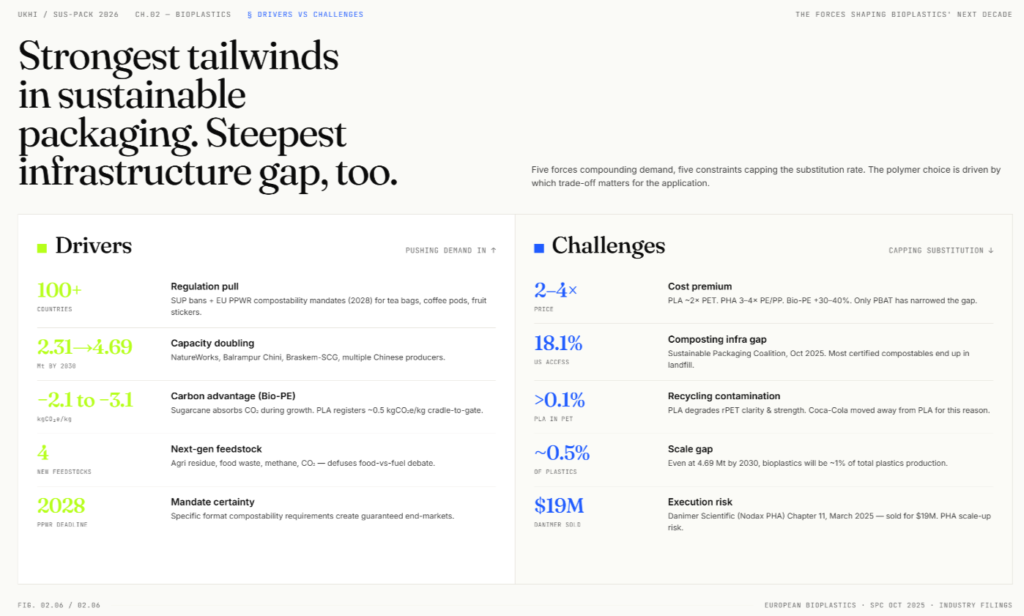

- European Bioplastics projects global bioplastics production capacity will reach 4.69 million tonnes by 2030, roughly doubling from 2.31 million tonnes in 2025.

- Recycled plastics capacity is being built out aggressively, driven by chemical recycling investments from companies like Eastman, PureCycle, and Plastic Energy.

Insight — Regulation, Not Branding, Is Now the Binding Constraint:

The most important industry-wide development of 2024–2025 is the gap between corporate sustainability pledges and actual performance.

Multiple major brands have missed targets or exited voluntary commitments.

Yet the market continues to grow because regulatory mandates now set the floor.

The sustainable packaging growth story has shifted from “brands want to” to “regulations require it.”

What Explains the Wide Range in Sustainable Packaging Market Forecasts?

The variance across research firms is driven primarily by differences in scope, not in analytical method.

Four factors account for most of the gap:

-

Whether all paper packaging counts as sustainable.

This is the single largest variable.

Including all paper and cardboard packaging adds USD 150–200 billion to the total.

Firms that count only paper formats actively replacing conventional plastic arrive at much lower figures.

-

Whether recycled-content conventional plastic counts.

Classifying a PET bottle with 30% rPET as fully “sustainable” inflates the market by 30–50%.

-

Whether glass and metal are included.

Adding these materials raises the baseline by a further USD 80–150 billion.

-

Methodology and base year.

Firms using top-down approaches and older base years (2022 or 2023) tend to produce estimates that diverge from those using bottom-up segment aggregation with more recent data.

The most robust interpretation for decision-makers is that the sustainable packaging market will cross USD 450 billion around 2030 and approach USD 600 billion by 2035, growing at roughly twice the rate of total packaging.

2.3 Sustainable Packaging Market Composition by Material Type

The five material categories that make up the sustainable packaging market are wildly unequal in size but inversely ranked on growth.

Paper dominates revenue.

Bioplastics lead on growth rate.

Understanding this asymmetry is essential before reading the material-specific market analysis that follows.

| Material Category | 2025 Market Size (USD) | Approximate Share | CAGR |

|---|---|---|---|

| Paper and cardboard | $255–290 billion (see note below) | ~80–85% | 4.3–5.1% |

| Recycled plastics packaging | $17–29 billion | ~5–7% | 5.8–10% |

| Bioplastics packaging | $17–25 billion | ~4–6% | 12–17% |

| Molded fiber and pulp | $5–11 billion | ~2% | 5–7% |

| Emerging bio-materials | <$1 billion | <0.3% | 6–10% |

Paper and Cardboard — The Dominant Segment

Paper and cardboard packaging accounts for the overwhelming majority of the sustainable packaging market by value.

The total global paper and paperboard packaging market is USD 410–480 billion in 2025 (detailed in the Paper and Cardboard chapter later), but not all of that is classified as “sustainable packaging” by market research firms.

Most firms include only paper packaging that actively replaces conventional plastic, carries certified recycled or FSC/PEFC content, or meets specific environmental performance criteria.

Commodity corrugated and standard folding cartons without sustainability certification are generally counted as “packaging” rather than “sustainable packaging,” even though paper as a material is renewable and recyclable.

The sustainable subset (the portion included in the USD 300–330 billion total sustainable packaging market) is estimated at roughly USD 255–290 billion.

This scope distinction is the single largest reason sustainable packaging market estimates vary so widely across research firms.

Bioplastics Packaging — The Fastest-Growing Segment

The bioplastics packaging market size was estimated at USD 17–25 billion in 2025, which is similar in absolute terms to recycled plastics, but growing far faster at 12–17% CAGR.

This makes bioplastics the highest-growth material category in sustainable packaging by a significant margin.

European Bioplastics’ 2025 market data report provides the most defensible volume anchor: global bioplastics production capacity of 2.31 million tonnes in 2025 with actual production of 1.67 million tonnes at 72% utilisation.

Global bioplastics production capacity is projected to reach 4.69 million tonnes by 2030.

Packaging accounts for 41.3% of total bioplastics production.

Bioplastics remain approximately 0.5% of total global plastics production of 431 million tonnes, which is small in absolute terms.

Still, the growth trajectory is the steepest in the industry.

Recycled Plastics Packaging — The Regulatory Beneficiary

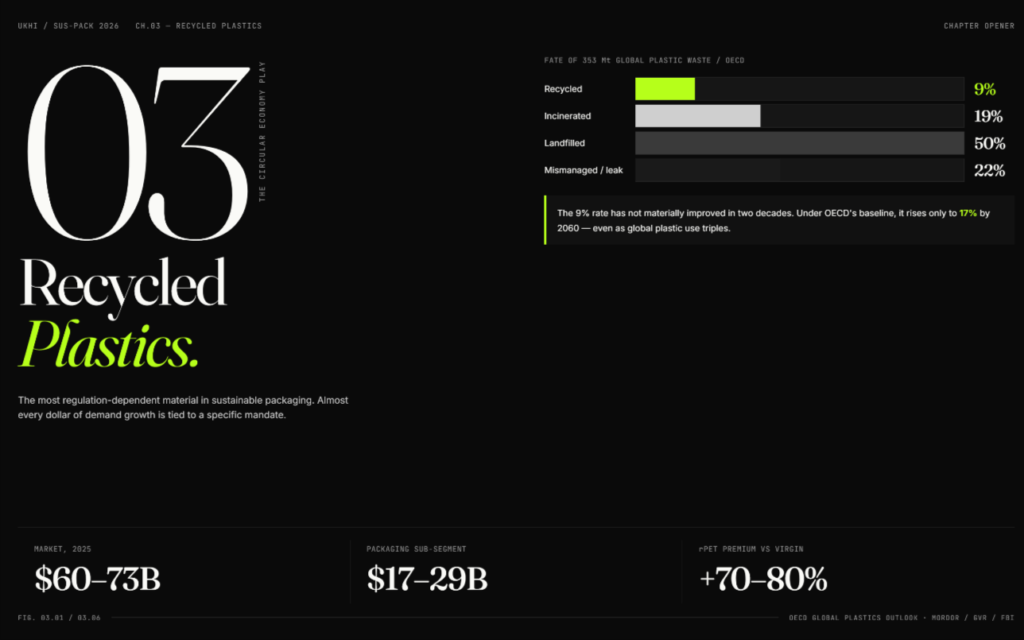

The recycled plastics packaging market size was pegged at USD 17–29 billion in 2025, with the broader recycled plastics market across all applications at USD 60–73 billion.

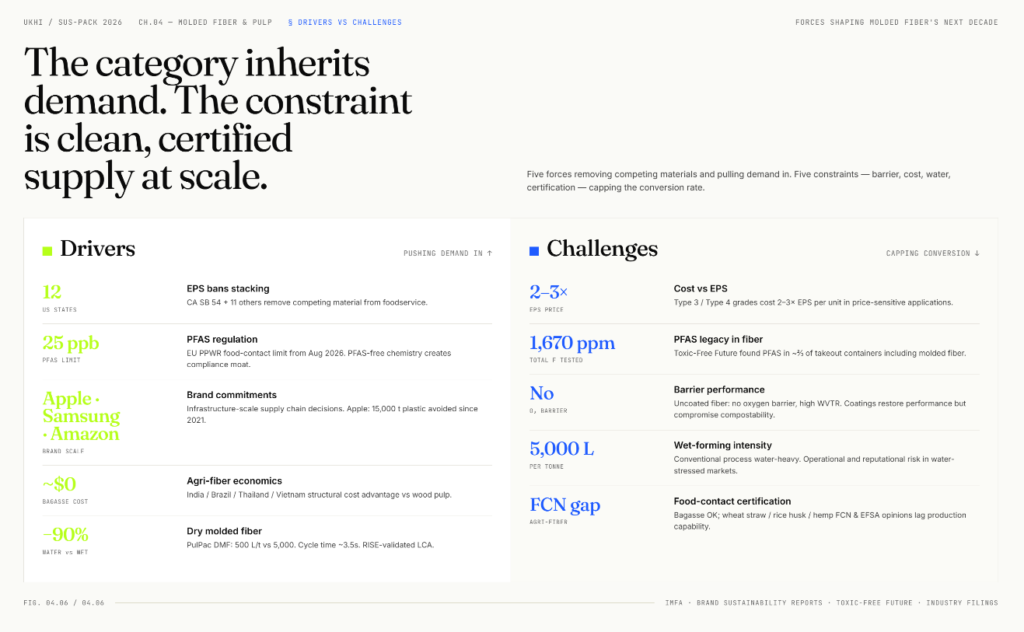

Growth is driven almost entirely by regulatory mandates such as the EU’s 30% recycled content target for PET bottles, the UK’s plastic packaging tax, and India’s escalating PCR requirements.

The recycled plastics market faces a structural tension: demand for food-grade recycled content is rising faster than supply, with rPET commanding an approximately 80% price premium over virgin PET in mid-2025.

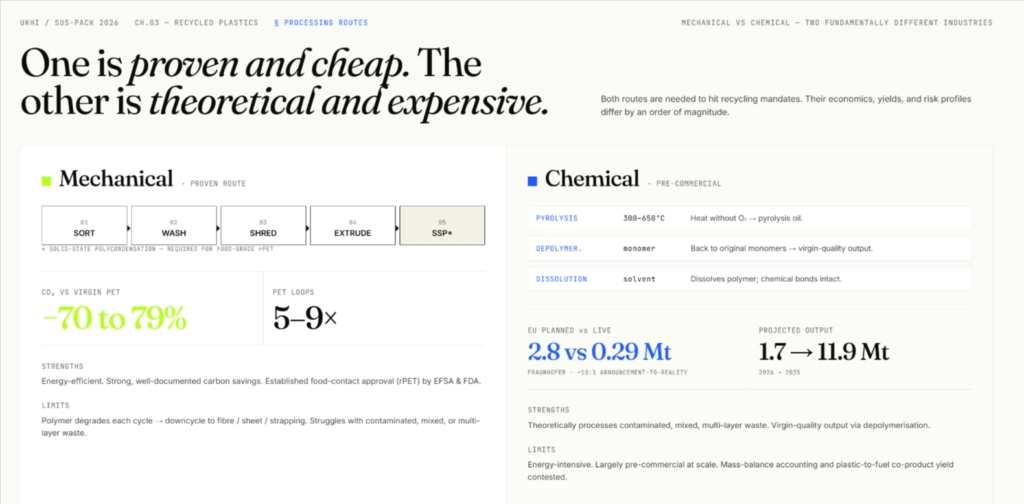

Chemical recycling is the wildcard, with capacity announcements totalling 9 million tonnes per year globally, but actual commercial output remains a fraction of that.

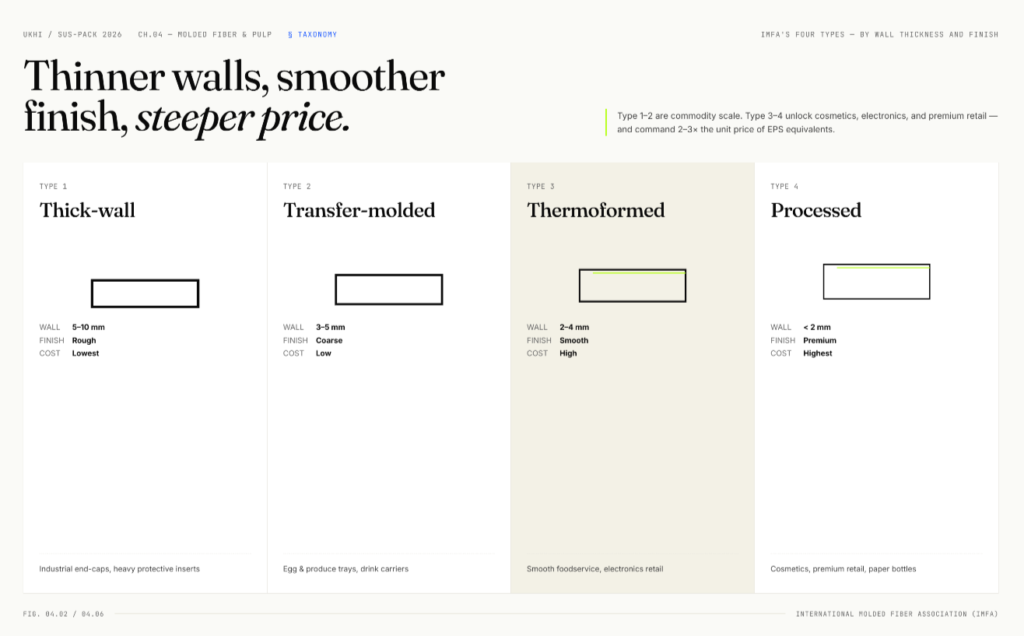

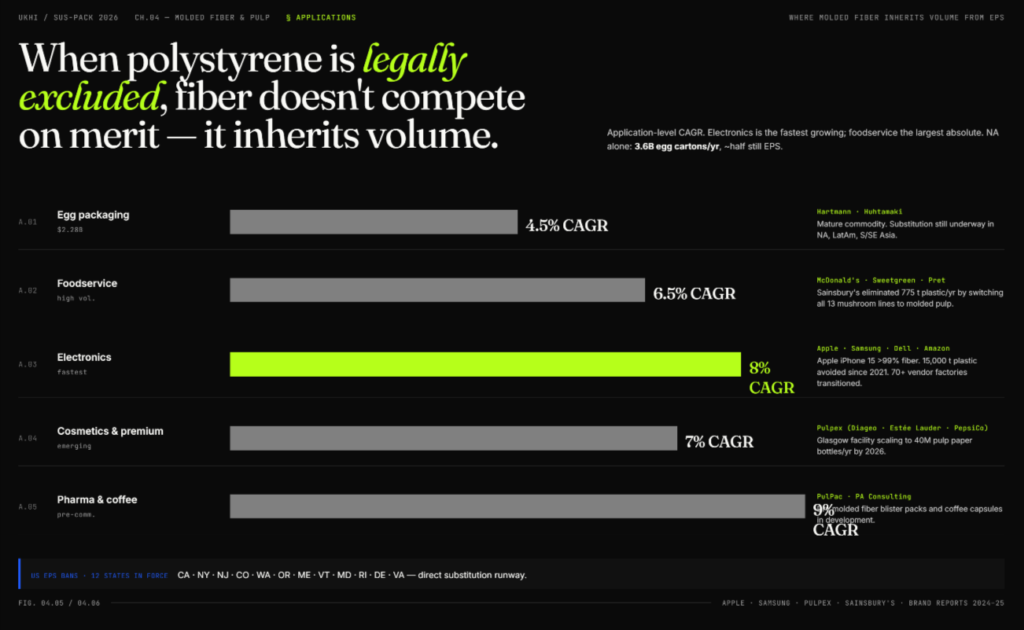

Molded Fiber and Pulp — The EPS Replacement Story

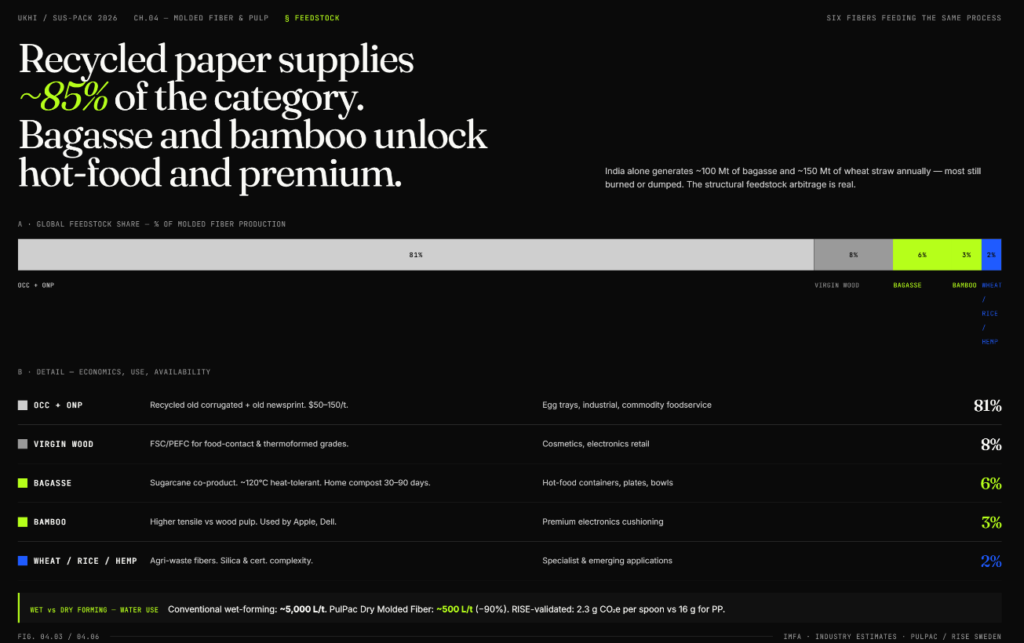

The molded fiber packaging market size was estimated at USD 5–11 billion in 2025.

The wide range exists because some research firms use a narrow “molded pulp” definition that covers only traditional wet-pressed products like egg cartons and fruit trays (yielding the lower figure), while others use a broader “molded fiber” definition that also includes thermoformed food service packaging and moulded protective inserts for electronics (yielding the higher figure).

The consensus growth rate for molded fiber packaging is 5–7% CAGR, which places it in the middle of the pack (faster than paper and cardboard but slower than bioplastics or recycled plastics).

The category’s growth is anchored on replacing expanded polystyrene (EPS) in food service packaging (clamshells, trays, cup lids) and electronics protective packaging.

More than 100 jurisdictions have now banned EPS.

Apple, Google, and Amazon have all shifted to fiber-based protective packaging in recent years.

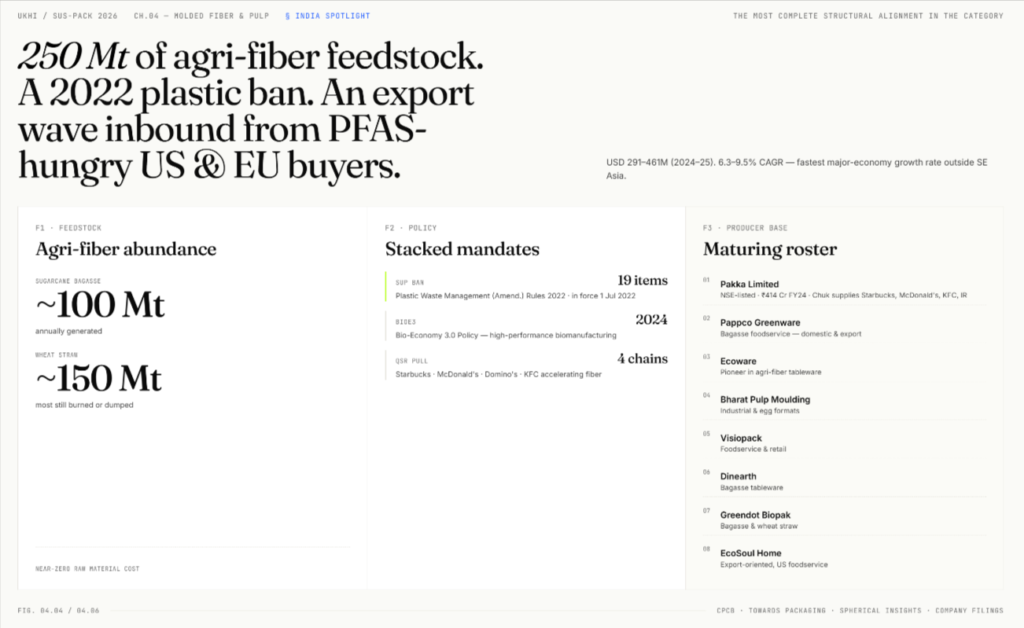

Molded fiber packaging adoption is growing fastest in Asia-Pacific, particularly in China and India, driven by both strong production capacity (India’s sugarcane industry generates large volumes of bagasse, the primary feedstock for moulded fiber food service packaging) and rising domestic demand as local EPS bans take effect.

Emerging Bio-Materials — Small Scale But Large Ambition

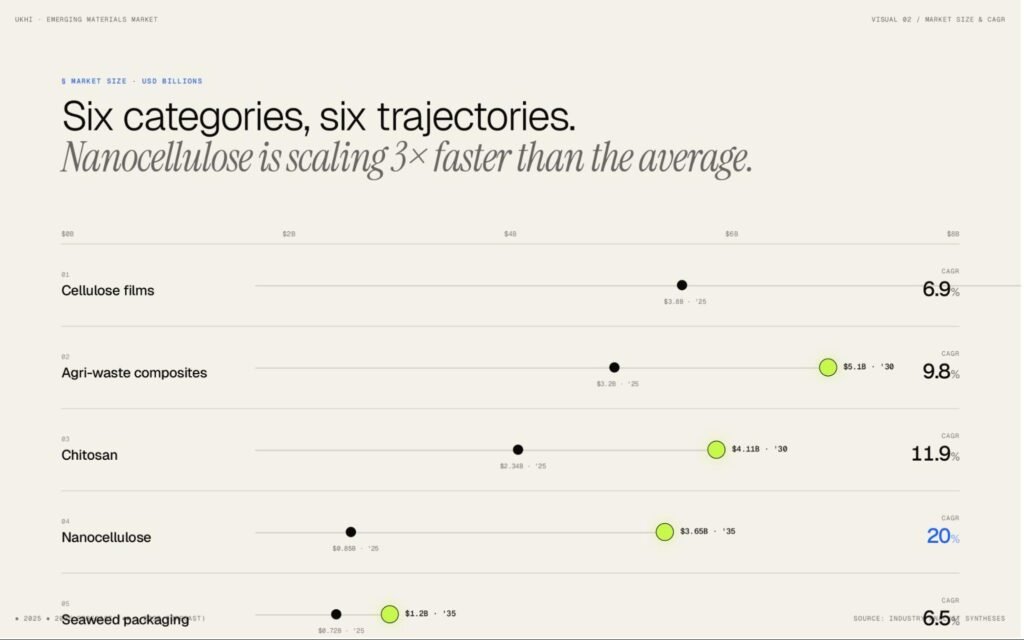

Emerging bio-materials market — mycelium composites, seaweed-based packaging, agricultural waste composites, edible coatings — remain commercially tiny.

Combined market value is under USD 1 billion.

Mycelium packaging sits at approximately USD 85–95 million; seaweed packaging at USD 600–800 million (though much of this is broader food-industry seaweed, not packaging-specific).

These materials matter not for their current revenue contribution but for their long-term disruption potential and for the outsized search interest they generate.

The Takeaway:

Paper carries the absolute dollars.

Bioplastics carry the growth rate.

This asymmetry defines the sustainable packaging investment landscape.

For a procurement decision-maker, paper is the safe, scaled, available option today.

For an investor or strategic planner looking at the 2030–2035 horizon, bioplastics and recycled plastics are where the market is shifting fastest, and where regulatory tailwinds are strongest.

3. Paper and Cardboard Packaging — Market Size, Growth, and Sustainability Analysis

3.1 What Is Paper and Cardboard Packaging?

Paper and cardboard packaging is made from cellulose fibers, which can be either virgin wood pulp or recycled paper fiber.

The fibers are formed into sheets, boards, or molded shapes that serve as packaging to protect, transport, and present products.

Paper and cardboard make the world’s most widely used packaging family, valued for being renewable, recyclable, biodegradable, and highly printable.

The convention separates paper (lighter substrates, generally under 250 gsm) from paperboard or cardboard (thicker, multi-ply, more rigid materials above 250 gsm).

Raw material for this category of packaging comes from two sources:

- Virgin wood pulp, produced through chemical (Kraft/sulphate) or mechanical pulping processes, and

- Recovered fiber from wastepaper collection, which now supplies roughly 54% of paper packaging raw material globally, with each cellulose fiber cycling through approximately five to seven uses before becoming too short for structural applications.

Virgin fiber is essential for food-contact grades, high-strength linerboard, and liquid paperboard.

Responsible sourcing is tracked through FSC (Forest Stewardship Council, certifying approximately 150 million hectares) and PEFC (Programme for the Endorsement of Forest Certification, covering approximately 295 million hectares).

Together, these schemes cover roughly 10–11% of the world’s total forest area.

Key Limitation — Barrier Properties:

Paper has inherently poor moisture, oxygen, and grease barrier properties.

Uncoated paper has water vapour transmission rates over 100 times too high for most moisture-sensitive foods, and oxygen transmission rates that exceed industry thresholds by two to three orders of magnitude.

This is why barrier coatings such as polyethylene lamination, wax, or newer bio-based alternatives are central to paper packaging’s functionality, and why those coatings create the recyclability trade-offs discussed later in this chapter.

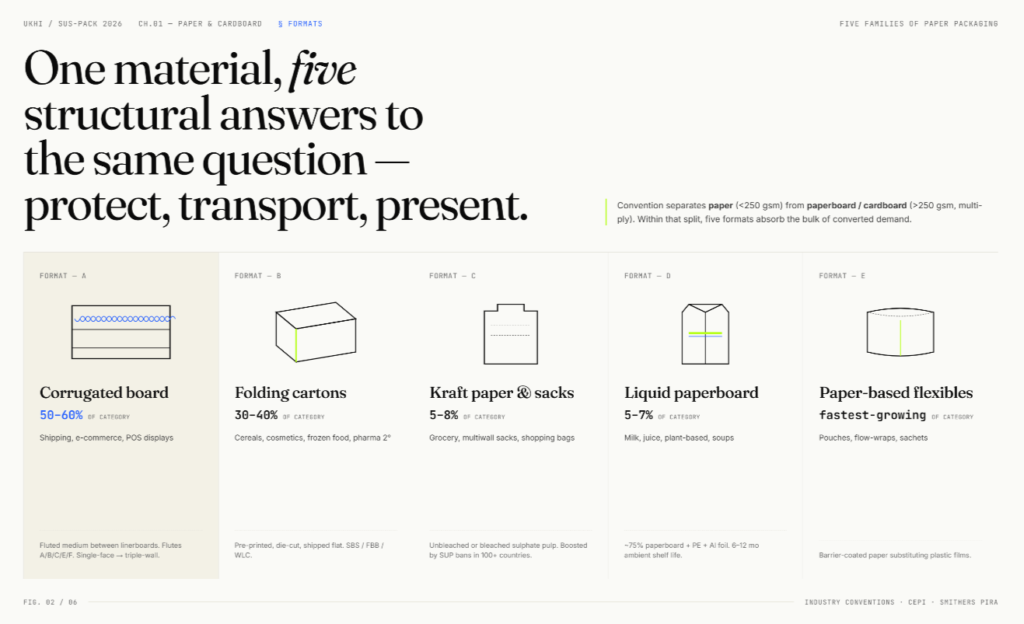

3.2 Types of Paper and Cardboard Packaging

-

Corrugated board — The dominant format, accounting for roughly 50–60% of paper packaging market value globally.

It sandwiches a fluted “medium” between flat linerboards, with different flute profiles (A, B, C, E, F) to determine cushioning and printability.

Walls range from single-face to triple-wall depending on the stacking strength required.

This is the format prevalent for shipping boxes, e-commerce packaging, and point-of-sale displays.

-

Folding cartons — Pre-printed, die-cut paperboard structures shipped flat and erected at the point of fill.

This is the prevalent format for cereal boxes, cosmetics packaging, frozen-food cartons, and pharmaceutical secondary packaging.

Made from Solid Bleached Sulphate (SBS), Folding Box Board (FBB), or recycled White Lined Chipboard (WLC).

-

Kraft paper and paper bags — Unbleached or bleached sulphate-pulp paper used for grocery bags, shopping bags, multiwall sacks (cement, flour, animal feed), and protective wrapping.

Single-use plastic bans across more than 100 countries have significantly increased its adoption.

-

Liquid paperboard and aseptic cartons — The Tetra Pak format.

Multilayer structures of roughly 75% paperboard combined with thin polyethylene layers and often aluminium foil, used for milk, juice, plant-based beverages, and soups.

Aseptic processing enables 6–12 month ambient shelf life without refrigeration.

-

Paper-based flexible packaging — Pouches, flow-wraps, and sachets made from barrier-coated paper, substituting conventional plastic films.

This is one of the fastest-growing sub-segments in the category.

3.3 Paper Packaging Market Size and Growth

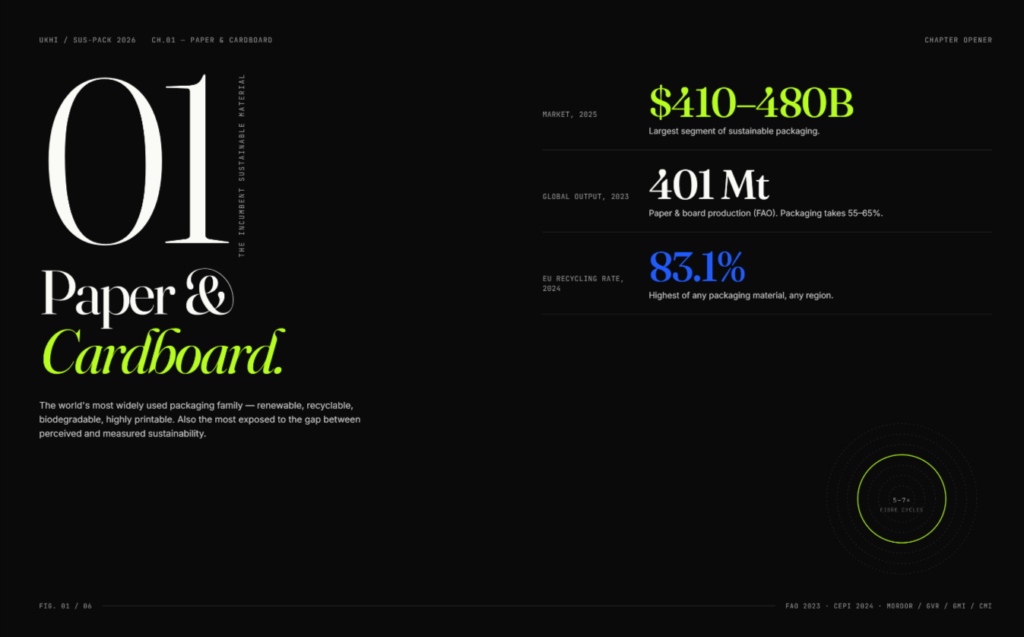

The total global paper and cardboard packaging market size was in the range of USD 410–480 billion in 2025.

This makes paper and cardboard the world’s largest packaging material category by a wide margin.

This figure covers all paper and paperboard packaging — corrugated shipping boxes, folding cartons, liquid paperboard, paper bags, and paper-based flexibles — regardless of whether a given product is specifically marketed or certified as “sustainable.”

A subset of this total, estimated at roughly USD 255–290 billion, is what market research firms classify as sustainable packaging when sizing the overall sustainable packaging market (as discussed in Chapter 2).

The difference reflects commodity corrugated and standard cartons that do not carry sustainability certification but are made from a material that is inherently renewable and widely recycled.

The market size estimates from individual research firms below reflect the total paper packaging market, not only the sustainable subset.

Complete Paper Packaging Market Size Estimates by Research Firm

| Research Firm | Market Size Estimate | Forecast | CAGR |

|---|---|---|---|

| Mordor Intelligence (2026) | USD 480.0B | USD 601.7B by 2031 | 4.6% |

| Grand View Research (2025) | USD 416.1B | USD 611.7B by 2033 | 5.0% |

| Global Market Insights (2024) | USD 410.5B | USD 596.5B by 2034 | 3.8% |

| Coherent Market Insights (2025) | USD 450.0B | USD 629.4B by 2032 | 4.9% |

Market Size by Sub-Segment

Note: The sub-segment figures below refer to the total paper packaging market, not only the sustainable subset discussed in Chapter 2.

Some sub-segments overlap in scope across research firms (for example, paper-based flexible packaging estimates vary widely depending on whether coated and laminated structures are included), so the sub-segment figures should not be summed to arrive at the total.

-

Corrugated packaging — The largest sub-segment, estimated at USD 230–325 billion in 2025 depending on scope.

On a volume basis, global corrugated production has reached roughly 275 billion square metres in 2025, more than doubling from 128 billion square metres in 2005.

Growth runs at 4–5% CAGR, driven primarily by e-commerce shipping volumes.

- Folding cartons — Strong analyst consensus at USD 140–200 billion in 2024, growing at 4.4–5.5% CAGR.

- Paper bags — Estimated at USD 6–12 billion, growing 5–6%, boosted by single-use plastic bag bans across jurisdictions.

- Liquid paperboard and aseptic cartons — The strongest growth rate in the paper category at USD 24–30 billion in 2024 with 7–8% CAGR, driven by emerging-market dairy consumption, plant-based beverages, and plastic bottle substitution.

- Paper-based flexible packaging — Ranges from USD 58–130 billion depending on whether foil-laminated and coated structures are included.

Production Volume

The FAO recorded 401 million tonnes of global paper and board production in 2023.

Packaging now claims roughly 55–65% of that total.

CEPI (the Confederation of European Paper Industries) reported that European paper and board production rebounded 5.2% in 2024 to approximately 78 million tonnes, with packaging-grade output up 6.5%.

In the United States, AF&PA reported production up 3.2% in 2024, with containerboard accounting for over 50% of total US capacity.

Stat: Europe’s paper and board packaging recycling rate reached 83.1% in 2024, the highest of any packaging material in any region globally.

The 4evergreen industry alliance targets 90% by 2030.

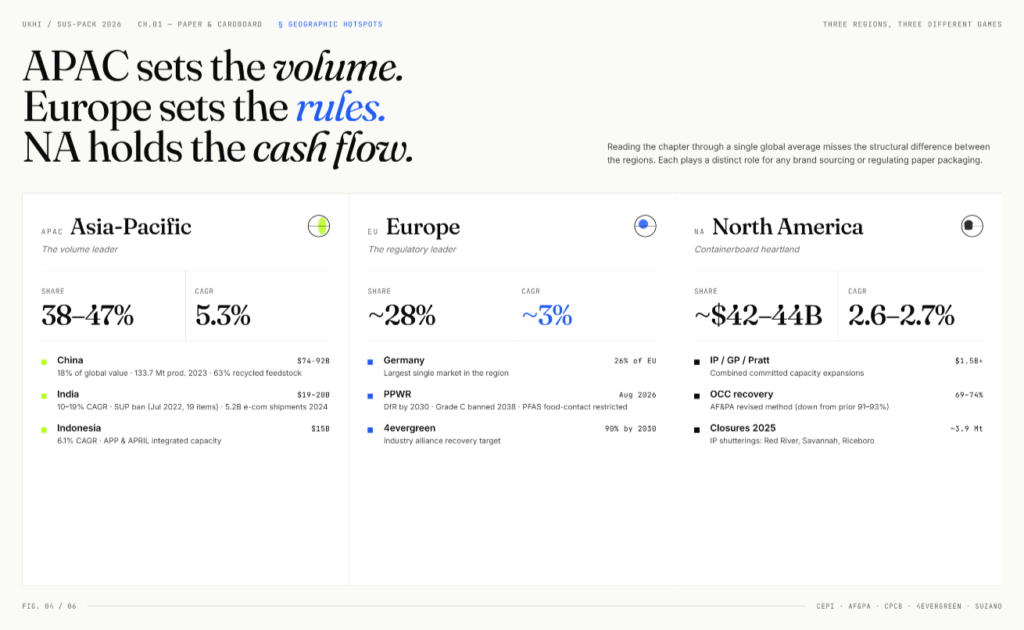

3.4 Geographic Hotspots for Paper Packaging

Asia-Pacific — The Volume Leader

Asia-Pacific holds 38–47% of the global paper packaging market and is the fastest-growing region at approximately 5.3% CAGR.

China is the world’s largest paper producer, manufacturing 133.7 million tonnes in 2023 alone. The China paper packaging market is estimated at USD 74–92 billion in 2025, which is 18% of global value. Nine Dragons Paper, the country’s largest producer, carries 21.7 million tonnes of design capacity. Recycled fiber dominates Chinese feedstock at 63% share.

India is one of the fastest-growing major paper packaging markets globally, estimated at USD 19–20 billion in 2025 and projected to grow at 10–19% CAGR depending on scope. Two forces drive demand: the July 2022 single-use plastic ban targeting 19 items (backed by over 860,000 inspections), and e-commerce shipment volumes that grew from 3.8 billion in 2023 to 5.2 billion in 2024. Recycled fiber supplies approximately 75% of Indian paper production. Major capacity investments include ITC’s barrier-coating line, SIG’s new aseptic carton plant in Ahmedabad (4 billion packs per year), and expansions by JK Paper, Oji India, and Huhtamaki India.

Indonesia is emerging as a production hub at USD 15 billion and 6.1% CAGR, with APP and APRIL controlling massive integrated capacity.

Europe — The Regulatory Leader

Europe’s paper packaging market contributes approximately 28% of global value, estimated at around USD 110 billion in 2025. Growth is slower than Asia-Pacific, but Europe has the world’s most developed recycling infrastructure and the most binding regulation.

The EU Packaging and Packaging Waste Regulation (PPWR), which entered into force in February 2025 and applies from August 2026, sets several provisions directly affecting paper packaging:

- All packaging must be designed for recycling by 2030 (graded A/B/C only; grade C banned from 2038).

- E-commerce packaging must not exceed 50% empty space relative to the product being shipped.

- PFAS restricted in food-contact packaging from August 2026.

- Packaging waste reduction of 5% by 2030 and 15% by 2040 versus 2018 baseline.

Germany alone accounts for 26% of the European paper packaging market.

North America — The Containerboard Heartland

The North American corrugated packaging market is estimated at USD 42–44 billion, and is growing at 2.6–2.7% CAGR.

Growth is slower than other regions, but absolute investment is significant, with International Paper, Georgia-Pacific, and Pratt Industries collectively committing over USD 1.5 billion in capacity expansions.

One notable data revision: AF&PA changed how it calculates recycling rates in 2024, and the updated methodology now reports US old corrugated container (OCC) recovery at 69–74%. Under the previous calculation method, the same metric was reported at 91–93%. The lower figure is considered more accurate because it accounts for exported material that may not actually be recycled at its destination.

Other Key Markets

- Japan — Paper packaging projected at USD 24 billion by 2026, with Oji and Nippon Paper leading innovation.

- Brazil — The global pulp powerhouse.

Suzano’s Cerrado Project, which opened in July 2024, is the world’s largest single-line pulp mill at 2.55 million tonnes per year of eucalyptus pulp, representing a USD 4.3 billion investment.

3.5 Key Applications and End-Use Sectors for Paper Packaging

E-Commerce and Shipping

E-commerce is the single biggest demand driver for paper and cardboard packaging. The sector consumes roughly 55 billion corrugated cartons annually worldwide.

Amazon’s packaging programs have eliminated more than 2 million tonnes of packaging materials since 2008, and in 2024 the company replaced approximately 15 billion plastic air pillows globally with recycled paper filler.

Walmart replaced 65 million plastic mailers per year with recyclable paper mailers across US fulfilment.

Food and Beverage

Food and beverage is the largest end-use sector overall, accounting for approximately 54% of paper packaging demand. Liquid packaging cartons dominate in beverages, with Tetra Pak, SIG, and Elopak as the main producers.

Healthcare, Personal Care, and Confectionery

- Healthcare — Paper-based pharmaceutical packaging is advancing through innovations like PulPac’s Blister Pack Collective, which aims to eliminate over 100,000 tonnes per year of pharmaceutical plastic packaging.

- Personal care — L’Oréal has deployed paper tubes for La Roche-Posay and Garnier (45% plastic reduction); Lush’s “Naked” range has avoided an estimated 30 million plastic bottles since 2010.

- Confectionery — Nestlé’s Smarties became the first global confectionery brand to move to fully recyclable paper packaging. It eliminated over 400 tonnes of plastic. Frugalpac’s recycled paperboard wine bottle is now used by 45 brands across 25 countries, with an 84% lower carbon footprint than glass.

3.6 The Paper Packaging Sustainability Debate

Paper is widely perceived as the default “sustainable” packaging choice. The reality is more nuanced than that perception suggests.

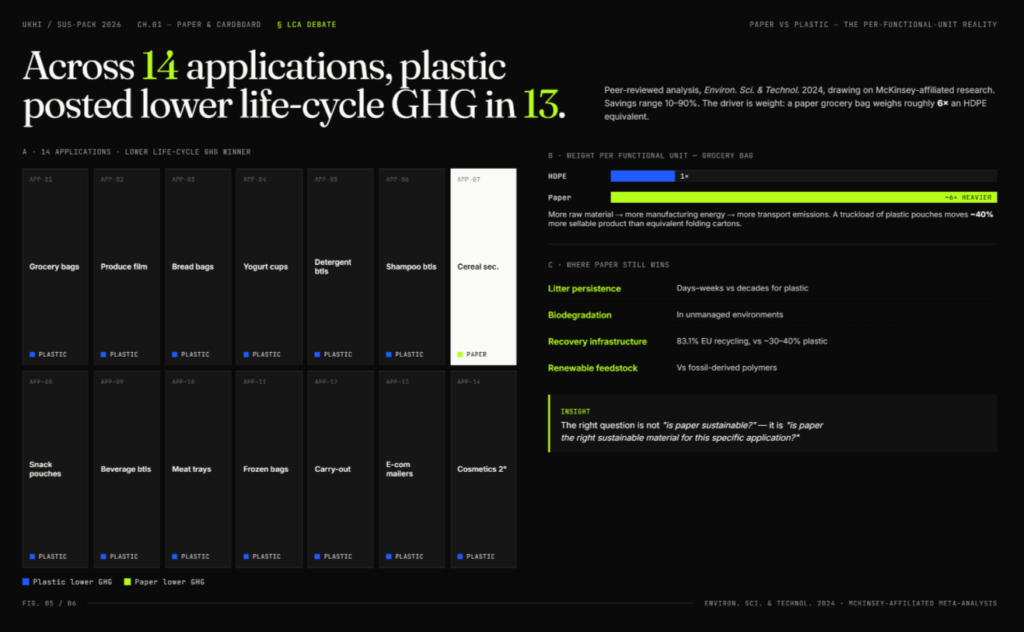

Paper vs Plastic — Carbon Footprint Comparison

Not necessarily. A peer-reviewed analysis published in Environmental Science & Technology (2024), drawing on McKinsey-affiliated research, found that across 14 packaging applications studied, plastics had lower life-cycle greenhouse gas emissions in 13 cases, with savings of 10–90%.

The primary reason is weight:

- a paper grocery bag weighs roughly six times more than an HDPE bag for similar carrying capacity

- this translates into more raw material, more manufacturing energy, and more transport emissions.

But when comparing the carbon footprint of paper and plastic packaging designed to do the same job, the result depends on the specific application. Paper does not automatically win on carbon, and in many cases it does not win at all.

Deforestation and Forest Management

Pulp and paper consume 33–40% of all industrial wood traded globally.

WWF identifies pulp as a relevant deforestation driver in 5 of 11 global deforestation fronts, particularly in Sumatra.

Only 10–11% of the global forest area is FSC- or PEFC-certified, and NGO scrutiny of certification standards is intensifying.

The EU Deforestation Regulation now requires due diligence on wood, paper, and pulp products entering the European market.

PFAS in Paper Packaging

PFAS (per- and polyfluoroalkyl substances) have been widely used as grease-proofing agents in food-contact paper packaging. The regulatory landscape for these is shifting rapidly:

- The US FDA announced in February 2024 that manufacturers had ceased sales of grease-proofing PFAS for food-contact use.

- At least 16 US states have enacted PFAS bans for food packaging.

- The EU PPWR restricts PFAS in food-contact packaging from August 2026.

- Alternatives (silicone coatings, plant-based barriers, mineral coatings) are commercially available but typically at 30–60% cost premiums.

Insight — “Paper-Washing” Is a Risk

Consumer research consistently shows that shoppers are 30–40% more likely to perceive a product as sustainable when packaged in paper, regardless of the underlying life-cycle performance. This makes paper substitution a marketing opportunity but one that regulators are now constraining through the EU Green Claims Directive and PPWR labelling rules. Brands that switch to paper primarily for optics, without genuine environmental benefit, face growing reputational and legal exposure.

3.7 Paper Packaging Market Drivers and Challenges

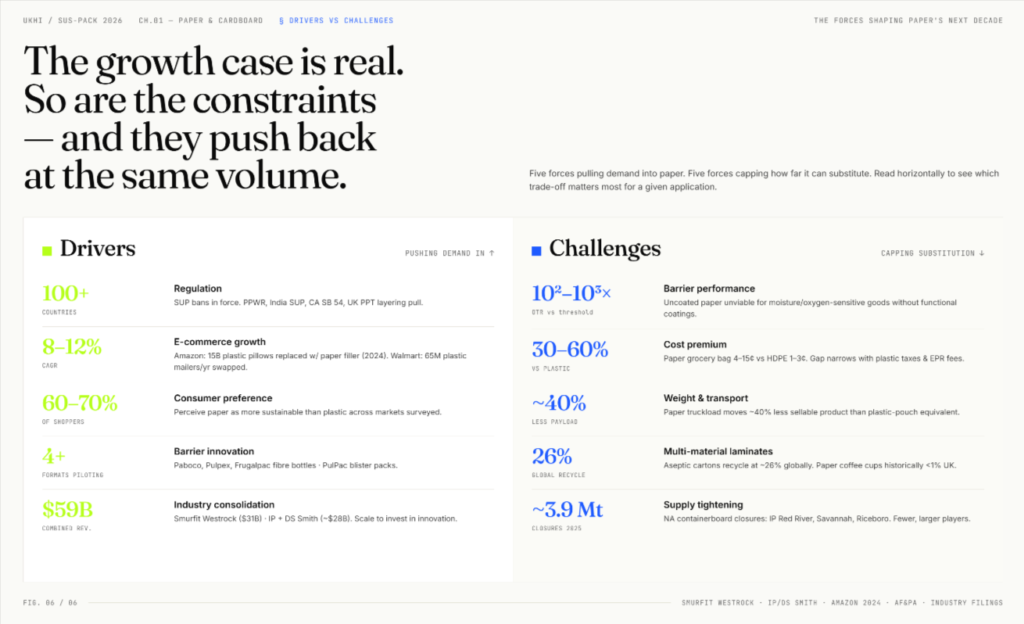

3.7.1 Growth Drivers for Paper Packaging

Regulation is the most powerful demand driver. Single-use plastic bans are now in force across more than 100 countries, and these bans directly shift demand toward paper in bags, wraps, food service, and retail packaging. The EU PPWR, India’s single-use plastic ban, California’s SB 54, and the UK’s plastic packaging tax are all layering additional regulatory pull.

E-commerce growth continues to expand corrugated demand at 8–12% annually. Amazon, Walmart, and Target have all moved away from plastic packaging in fulfilment toward paper-based alternatives.

Consumer preference for paper is strong and consistent, with 60–70% of consumers perceiving paper packaging as more sustainable than plastic in surveys conducted across multiple markets.

Innovation in barrier coatings is expanding paper into new applications that were previously reserved for plastics — chilled and frozen food, snack packaging, personal care.

Fiber-based bottles from Paboco, Pulpex, and Frugalpac are being piloted by Coca-Cola, PepsiCo, Diageo, and L’Oréal.

Paperboard blister packs for pharmaceuticals are under development with Sanofi through the PulPac Blister Pack Collective.

Industry consolidation — the Smurfit Kappa–WestRock merger (creating Smurfit Westrock, USD 31 billion revenue) and International Paper’s acquisition of DS Smith (approximately USD 28 billion combined) — has created two global operators with the scale to invest in innovation, rationalise capacity, and serve multinational brands efficiently.

3.7.2 Challenges and Limitations of Paper Packaging

Barrier performance remains the fundamental constraint. Uncoated paper cannot serve moisture-sensitive foods, oxygen-sensitive snacks, carbonated beverages, or pharmaceutical blister packs without functional coatings. The coatings that restore performance (PE lamination, wax) compromise recyclability, and newer bio-based alternatives command 10–35% price premiums while still lagging conventional coatings on oxygen-barrier performance.

Cost is higher than plastic at the converted-package level, typically by 30–60% for equivalent functionality. A paper grocery bag costs 4–15 cents against 1–3 cents for an HDPE bag. This gap narrows when plastic taxes and EPR fees are factored in, but it has not yet closed in most applications.

Weight and transport emissions represent paper’s most consistent disadvantage in life-cycle assessments. A truckload of plastic pouches moves approximately 40% more sellable product than an equivalent load of folding cartons. For brands shipping by air freight, this weight penalty translates directly into higher emissions.

Multi-material laminates remain a recycling problem. Tetra Pak aseptic cartons (75% paperboard, 20% polyethylene, 5% aluminium) recycle at roughly 26% globally. Paper coffee cups historically recycled at under 1% in the UK. Both formats face high regulatory risk under PPWR’s recyclability grading system.

Supply tightening through consolidation — North American containerboard producers announced closures totalling approximately 3.9 million tonnes in 2025, led by International Paper shuttering facilities at Red River, Savannah, and Riceboro. New recycled-content capacity is being built, but the net effect is a market with fewer, larger players and greater pricing discipline for buyers.

The Bottom Line

Paper packaging will continue to grow, supported by regulation, e-commerce expansion, and consumer preference. But the constraints are equally strong — barrier limitations, cost premiums, weight penalties, and recyclability compromises from coatings. The right question for a packaging decision-maker is not “is paper sustainable?” but “is paper the right sustainable material for this specific application?” Answering that honestly requires functional-unit life-cycle data.

4. Bioplastics Packaging — Market Size, Types, and Growth Analysis

4.1 What Are Bioplastics?

Bioplastics are plastics that are either:

- bio-based (derived from biological feedstocks such as corn starch, sugarcane, or cellulose),

- biodegradable (capable of breaking down through natural biological processes under specific conditions),

- or both.

The term covers a wide range of polymers with very different properties, end-of-life behaviours, and recycling compatibility.

The clearest way to understand the category is through the framework maintained by European Bioplastics, which maps bioplastics along two independent axes:

- whether the feedstock is bio-based or fossil-based, and

- whether the resulting polymer is biodegradable or non-biodegradable.

This produces three distinct product groups:

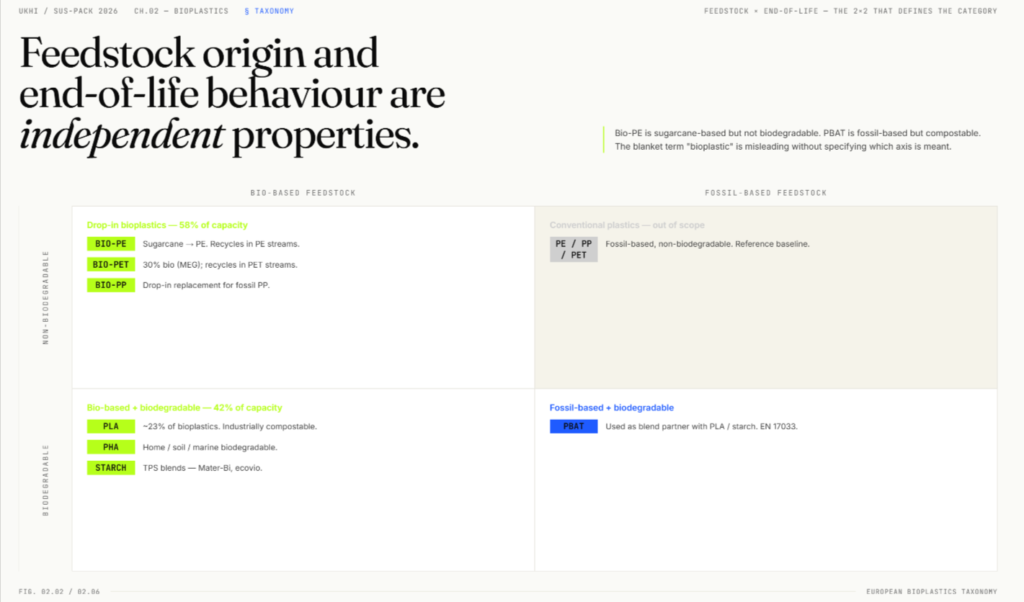

Bio-based, non-biodegradable (“drop-in” bioplastics)

These include bio-PE, bio-PET, and bio-PP.

They are chemically identical to their fossil-based equivalents, which means they perform the same way, recycle in the same streams, and are not biodegradable.

Their sustainability case rests entirely on the fact that the carbon in the polymer comes from plants rather than petroleum.

Drop-ins account for approximately 58% of global bioplastics capacity in 2025.

Bio-based and biodegradable

These include PLA (polylactic acid), PHA (polyhydroxyalkanoates), and starch blends.

They are made from biological feedstocks and can biodegrade under specific conditions, though the conditions required vary significantly by polymer type.

This group accounts for roughly 42% of capacity.

Fossil-based but biodegradable

The most important example is PBAT (polybutylene adipate terephthalate).

It is derived from fossil feedstocks but is industrially compostable and soil-biodegradable.

PBAT is almost always used as a blend partner with PLA or starch to improve flexibility and toughness.

European Bioplastics tracks PBAT under bioplastics only when it is produced from bio-based feedstock. Most commercial PBAT is fossil-derived and therefore falls outside the 100% capacity split above, but it is included in this chapter because of its central role in compostable packaging blends.

Key Distinction

The feedstock origin and the end-of-life behaviour of a bioplastic are independent properties.

For example:

- Bio-PE is made from sugarcane but is not biodegradable.

- PBAT is made from fossil feedstocks but is biodegradable and compostable.

This is why the blanket term “bioplastic” can be misleading without further specification.

4.2 Types of Bioplastics: Material Deep-Dives

4.2.1 PLA (Polylactic Acid)

PLA is the largest biodegradable bioplastic by production volume, accounting for roughly 23% of all bioplastics capacity in 2025.

It is produced by fermenting plant sugars (typically from corn or sugarcane) into lactic acid, which is then polymerised.

Properties: Clear, rigid, good printability, food-contact approved. Limited by a heat-deflection temperature near 55–60°C unless crystallised, which restricts use in hot-fill or microwave applications.

End-of-life: Industrially compostable under EN 13432 and ASTM D6400. Generally does not home compost because PLA requires temperatures above 55°C to begin hydrolysing. PLA also contaminates PET recycling streams at concentrations above 0.1%.

Key producers:

- NatureWorks (Ingeo brand, approximately 150,000 tonnes per year in Nebraska plus a new 75,000 tpa plant in Thailand), and

- TotalEnergies Corbion (Luminy brand, 75,000 tpa in Thailand, with cumulative production passing 100,000 tonnes in 2022).

Price: USD 2,200–3,800 per tonne, roughly double the price of virgin PET.

PLA market size: The global PLA market is estimated at USD 3.5–5.5 billion in 2025, growing at 12–18% CAGR.

4.2.2 PHA (Polyhydroxyalkanoates)

PHA is the fastest-growing bioplastic family and the only commercial polymer certified as home compostable, soil biodegradable, and marine biodegradable.

PHA is produced through bacterial fermentation, where microorganisms convert sugars, oils, or even methane into polymer granules stored inside their cells.

Properties: Versatile — can range from stiff and brittle to flexible depending on the specific PHA type (PHB, PHBH, P3HB4HB). Good oxygen barrier properties. Slower crystallisation than PLA.

End-of-life: Home compostable (TÜV Austria OK compost HOME), soil biodegradable (OK biodegradable SOIL), and marine biodegradable (ASTM D6691). This is PHA’s unique regulatory and environmental advantage.

Key producers:

- Kaneka (PHBH brand, 20,000 tpa in Japan after 2024 expansion),

- CJ Biomaterials (5,000 tpa in Indonesia, expanding),

- Bluepha (5,000–25,000 tpa in China with a 75,000 tpa roadmap),

- RWDC Industries (scaling to 25,000 tpa by 2027 via used cooking oil feedstock), and

- Newlight Technologies (methane-to-PHA, Carbon Trust certified at −88 kg CO₂e per kg).

Price: USD 4,000–7,000 per tonne, approximately 3–4 times the cost of conventional PE or PP. Extraction and purification account for 30–50% of total production cost.

Industry note: Danimer Scientific, previously the most prominent US PHA producer (Nodax brand), filed for Chapter 11 bankruptcy in March 2025 and was sold for USD 19 million, highlighting the execution risk in PHA scale-up.

Stat: PHA’s share of global bioplastics capacity is forecast to grow from 4.7% in 2025 to 16.8% by 2030, according to European Bioplastics. This is the fastest share gain of any bioplastic type.

4.2.3 PBAT (Polybutylene Adipate Terephthalate)

PBAT is a fossil-based but biodegradable polyester used almost exclusively as a blend partner with PLA or starch to improve flexibility and toughness in compostable packaging applications such as bags, wraps, and agricultural mulch films.

Properties: Flexible, tough, good elongation at break. Certified industrially compostable (EN 13432) and soil biodegradable (EN 17033).

Key producers:

- BASF (ecoflex brand)

- Kingfa (China’s largest producer at roughly 320,000 tpa with 240,000 tpa more under construction)

- Novamont (used in Mater-Bi blends).

Ukhi produces PBAT-compatible compostable resin systems from agricultural residue feedstocks including rice husk, hemp, and crop stubble, formulated for blown film and cast film applications.

Chinese capacity dominates, with combined announced PBAT capacity exceeding 2.9 million tonnes — larger than all bio-based plastics combined.

Price: USD 1,400–1,850 per tonne, only 10–50% above conventional LDPE. Chinese FOB prices have fallen roughly 15% since 2023, making PBAT the most cost-competitive biodegradable polymer.

4.2.4 Starch Blends (TPS — Thermoplastic Starch)

Starch blends combine thermoplastic starch with biodegradable polyesters (typically PBAT or PLA) to produce compostable materials used primarily for carrier bags, bin liners, and food packaging films.

Novamont’s Mater-Bi and BASF’s ecovio are the best-known commercial brands.

In India, Ukhi produces home-compostable granules from agricultural residue (hemp, flax, rice husk, and crop stubble) under its EcoGran brand, targeting starch-blend and fiber-composite applications for food service and flexible packaging.

Properties: Cost-effective, good processability on conventional blown-film lines. Limited moisture resistance without blend partners.

Price: USD 2,200–5,000 per tonne depending on the blend ratio and performance grade.

Capacity: Approximately 141,000 tonnes in 2025. Novamont operates 150,000 tpa of Mater-Bi capacity in Italy (now fully owned by Versalis/Eni since October 2023).

Note: Ukhi’s EcoGran range spans blown film, profile extrusion, injection moulding, and cast film grades, and includes a biodegradable extrusion coating resin designed to replace conventional PE and PP coatings on paper substrates such as cups and food trays.

4.2.5 Bio-PE and Bio-PET (Drop-In Bioplastics)

Bio-PE and Bio-PET are chemically identical to conventional polyethylene and PET but are derived wholly or partly from bio-based feedstocks, primarily sugarcane ethanol.

Bio-PE: Bio-PE delivers a cradle-to-gate carbon footprint of approximately −2.1 to −3.1 kg CO₂e per kg, compared to +1.8 to +2.0 for fossil HDPE, because sugarcane absorbs CO₂ during growth.

Braskem’s I’m green brand is the global leader, with 275,000 tpa of bio-based ethylene capacity in Brazil (expanded in May 2025).

A 200,000 tpa joint venture with SCG Chemicals in Thailand is under front-end engineering.

Bio-PET: Currently only 30% bio-based (the MEG component from sugarcane; the PTA component remains fossil-derived).

Coca-Cola’s PlantBottle, which uses 30% bio-PET, has distributed roughly 35 billion bottles since 2009.

A 100% bio-based PET prototype was produced in partnership with Virent in 2021.

Key advantage: Drop-ins recycle in existing PET and PE streams with no contamination risk and no need for composting infrastructure. Their limitation is that they offer no end-of-life biodegradability as their case is purely about reducing fossil carbon input.

4.3 Bioplastics Market Size and Growth

The global bioplastics market size was estimated at USD 14–24 billion in 2025, with the range reflecting scope differences across research firms.

The most defensible volume estimate comes from the European Bioplastics 2025 market data report: global production capacity of 2.31 million tonnes in 2025, with actual production of 1.67 million tonnes at 72% utilization.

Global bioplastics capacity is projected to reach 4.69 million tonnes by 2030.

Bioplastics Market Size Estimates by Research Firm

| Research Firm | 2025 Size (USD) | Forecast | CAGR |

|---|---|---|---|

| Grand View Research | $18.4B | $67.4B by 2033 | 17.6% |

| MarketsandMarkets | $17.6B | $45.0B by 2030 | 20.7% |

| Precedence Research | $23.8B | $119.1B by 2035 | 17.5% |

| Fortune Business Insights | $14.8B | — | 23.3% |

| Mordor Intelligence | $15.6B | $28.9B by 2031 | 10.8% |

The bioplastics packaging market specifically is estimated at USD 17–25 billion in 2025, since packaging accounts for 41.3% of total bioplastics production.

Despite this share declining slightly from 45% in 2024 (as automotive applications grow faster), the absolute packaging volume is forecast to nearly triple to approximately 3 million tonnes by 2029.

Insight

Bioplastics remain approximately 0.5% of total global plastics production of 431 million tonnes. Even at 4.69 million tonnes by 2030, they will represent roughly 1% of the total. The strategic value of bioplastics lies not in replacing conventional plastics across the board, but in serving specific applications — particularly food service, compostable bags, and agricultural films — where regulation mandates compostable or bio-based alternatives and where the necessary composting infrastructure is available or being built.

4.4 Geographic Hotspots for Bioplastics

Asia-Pacific — The Production Leader

Asia-Pacific accounts for approximately 56% of global bioplastics production capacity in 2025, rising toward 63% by 2029.

Thailand has emerged as the global PLA hub, with NatureWorks and TotalEnergies Corbion operating a combined 150,000 tpa of capacity.

China dominates PBAT production, with Kingfa alone holding roughly 320,000 tpa and combined Chinese PLA plus PBAT capacity projected at 3.6 million tonnes.

India — The Strategic Growth Market

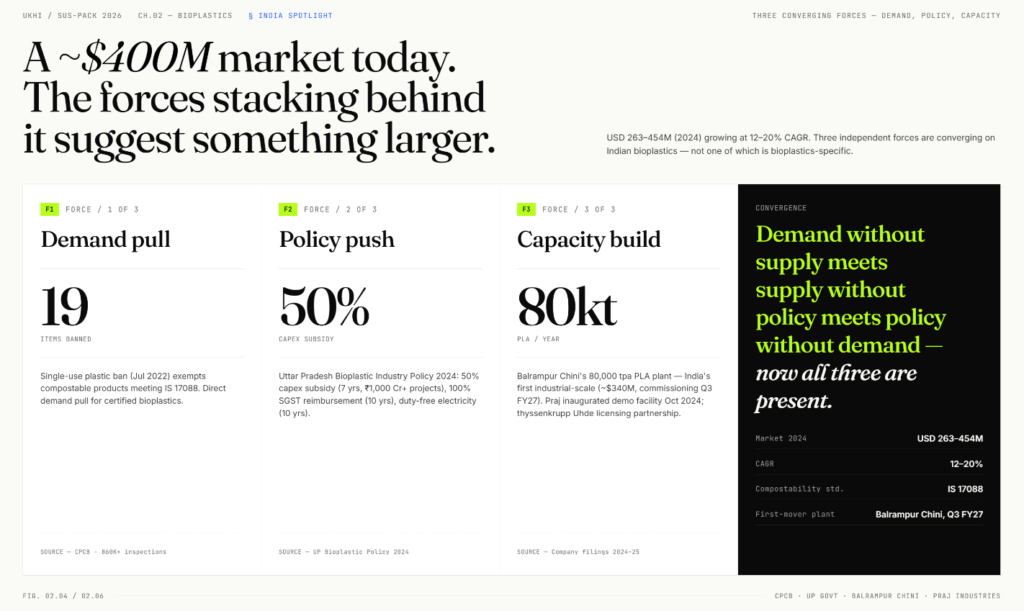

The India bioplastics market is estimated at USD 263–454 million in 2024 and believed to be growing at 12–20% CAGR depending on source.

Three forces are converging to make India a critical bioplastics growth story:

- The July 2022 single-use plastic ban exempts compostable products meeting IS 17088; this has created a massive and direct demand pull for certified bioplastics.

- The Uttar Pradesh Bioplastic Industry Policy 2024 offers a 50% capital subsidy for seven years on bioplastics manufacturing investments above ₹1,000 crore, 100% SGST reimbursement for ten years, and ten years of duty-free electricity, anchored by a designated bioplastic park at Lakhimpur Kheri.

- Balrampur Chini Mills is building India’s first industrial-scale PLA plant at 80,000 tonnes per year (approximately USD 340 million investment, with commissioning expected Q3 FY27). Praj Industries inaugurated a PLA demonstration facility in October 2024 and partnered with thyssenkrupp Uhde to license complete PLA plants globally.

Europe — The Regulatory Leader

The Europe bioplastics market is valued at approximately USD 5.2–6.2 billion in 2025 (Mordor Intelligence), growing at 14–17% CAGR.

Europe holds only about 15% of production capacity but consumes 27–31% of global bioplastics value, making it the largest revenue market.

The EU PPWR mandates compostability from February 2028 for tea bags, coffee pods, and fruit stickers, creating new application-specific demand.

The Americas

North America holds approximately 16–19% of global bioplastics capacity, led by NatureWorks in Nebraska and emerging PHA producers. Brazil anchors the bio-PE story through Braskem’s 275,000 tpa facility.

4.5 Key Applications for Bioplastics Packaging

4.5 Key Applications for Bioplastics Packaging

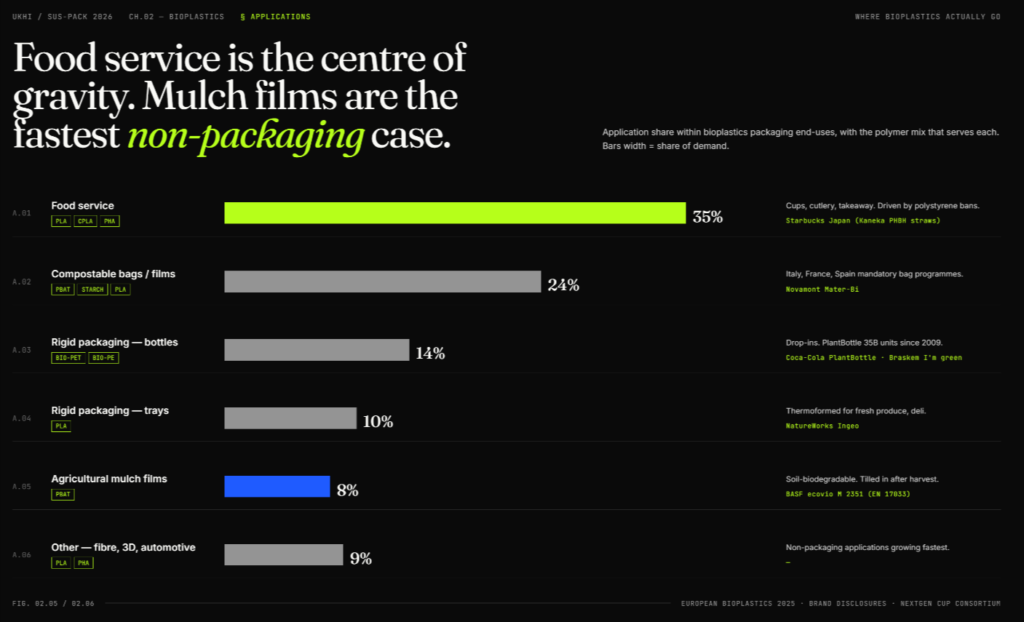

Food service packaging is the largest application for bioplastics, with majority of the demand in PLA cups, CPLA cutlery, and compostable takeaway container, particularly in jurisdictions that have banned polystyrene food service items (the EU’s July 2024 ban, plus over 100 city and state-level bans globally).

Kaneka’s PHBH straws are now used by Starbucks Japan, and the McDonald’s-Starbucks NextGen Cup Consortium has funded USD 10 million toward fiber cups with PLA or PHA liners.

Compostable bags and flexible films — primarily PBAT/starch blends — dominate in regions with mandatory compostable bag requirements, such as Italy (where Novamont’s Mater-Bi supplies a large share of the national market) and parts of France and Spain.

Rigid packaging splits between bio-PET drop-ins for bottles (Coca-Cola’s PlantBottle programme) and PLA thermoformed trays for fresh produce and deli items.

Outside of packaging, agricultural mulch films are a significant application for bioplastics.

These are thin films laid over crop rows to suppress weeds and retain moisture.