Side-by-Side Comparison

Executive Summary

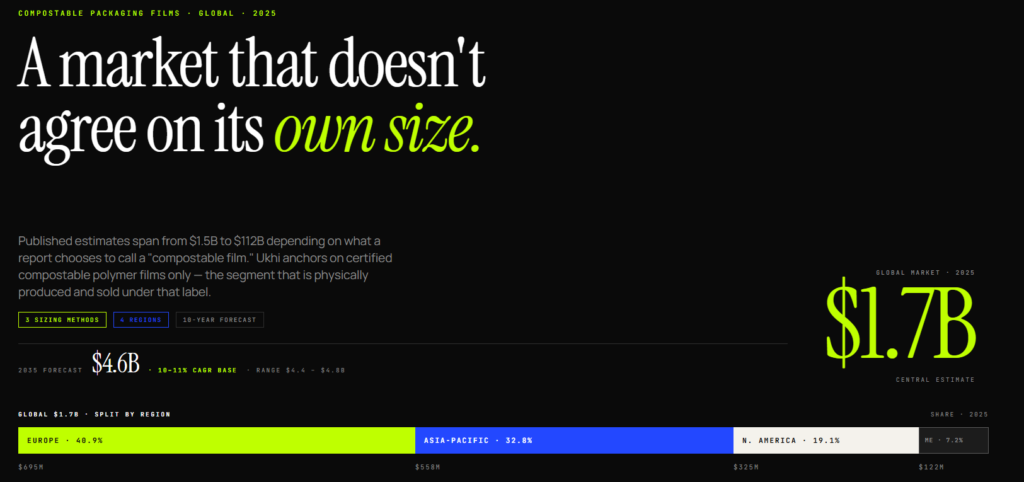

The global market for compostable packaging films is valued at approximately $1.7 billion in 2025 and is projected to grow at a compound annual growth rate of 10 to 11%, reaching $4.4 to $4.8 billion by 2035.

This market covers thin, flexible polymer films made from compostable materials (PLA, PBAT, PHA, starch blends, PBS, and regenerated cellulose) used in packaging applications including pouches, bags, wraps, lidding, and flow-wrap.

The sector is at an inflection point: regulatory mandates in the EU, India, and parts of the United States are converting voluntary corporate sustainability pledges into enforceable requirements, while production capacity, particularly in China and Southeast Asia, is scaling rapidly to meet anticipated demand.

The decade ahead will be defined by whether composting infrastructure, material costs, and supply chain readiness can keep pace with the regulatory and commercial momentum driving adoption.

Key Insights

1. The compostable packaging films market is significant but widely misreported.

Published estimates for “compostable packaging films” range from $1.2 billion to over $11 billion, depending on how broadly the scope is defined.

The $10 billion+ figures include paper-based flexible packaging, conventional biodegradable films, and broader product categories beyond polymer films.

Our estimate of $1.7 billion is derived from three independent analytical approaches (triangulation of narrowly scoped published data, top-down resin production analysis, and material-level build-up) and reflects only certified compostable polymer films used in packaging.

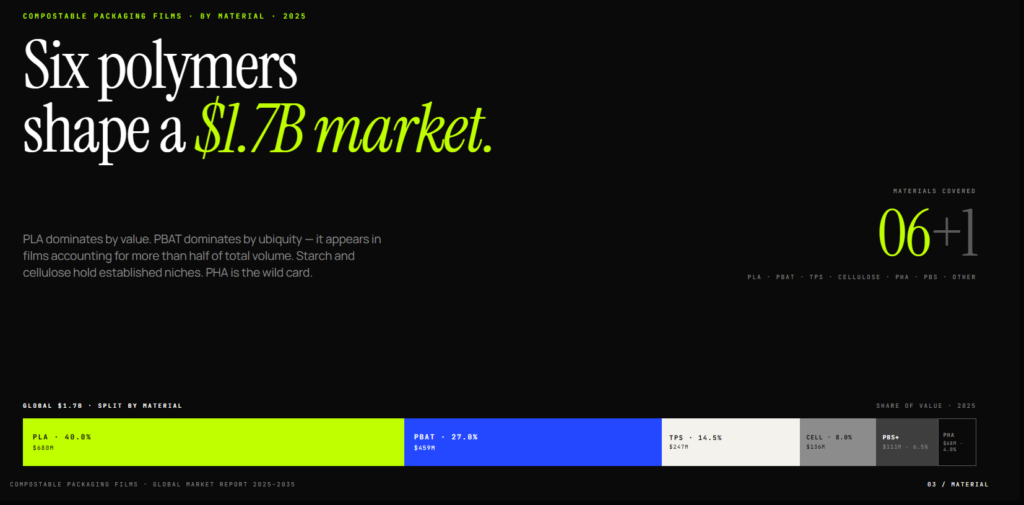

2. PLA and PBAT dominate the compostable packaging films market, but PHA is the material to watch.

PLA holds approximately 40% of global market value ($680 million), leading in cast film and coated substrate applications.

PBAT and PBAT-dominant blends account for 27% ($459 million), anchoring the blown film segment for bags and flexible wraps.

PHA currently represents just 4% ($65 million) but is growing at 15 to 21% annually and is the only compostable polymer certified for marine biodegradation, a property that is becoming increasingly valuable under tightening coastal and ocean-leakage regulations.

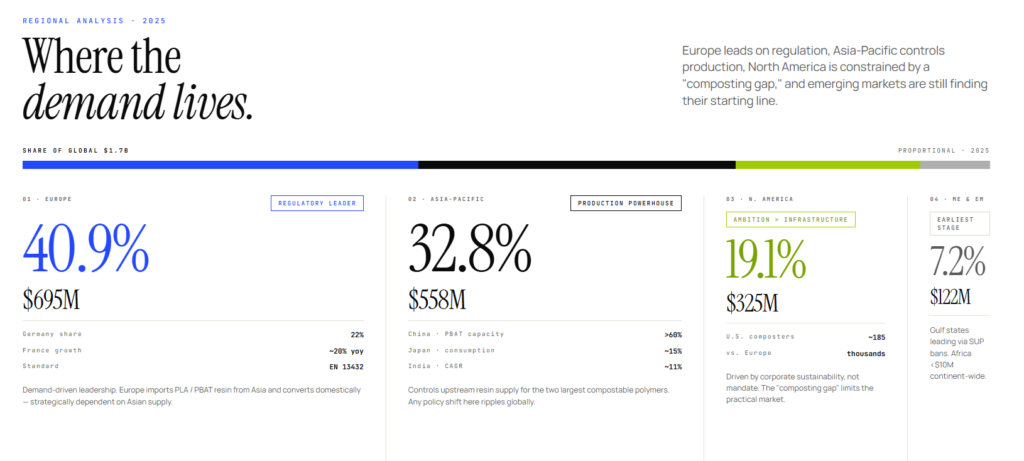

3. Europe leads in demand for compostable packaging films; Asia-Pacific controls supply.

Europe accounts for approximately 41% of global compostable film consumption ($695 million), driven by EN 13432 certification infrastructure and the EU Packaging and Packaging Waste Regulation.

Asia-Pacific holds 33% of demand ($558 million) but controls the upstream supply of PLA and PBAT resin, with China alone holding over 60% of global PBAT capacity.

This geographic split between demand leadership and supply dominance creates strategic dependencies that shape pricing, trade flows, and supply chain risk across the industry.

4. Regulation is the primary growth engine for the compostable packaging films market.

The EU PPWR mandates industrial compostability for specific packaging categories by February 2028.

California’s SB 54 requires all single-use packaging to be recyclable or compostable by 2032.

India exempts certified compostable plastics from its single-use plastics ban.

These regulations create guaranteed demand on fixed timelines.

5. Infrastructure is the binding constraint for the growth of the compostable packaging films market.

Compostable films that reach landfill or contaminate recycling streams deliver no environmental benefit.

Only 30% of U.S. municipalities have access to industrial composting facilities that accept packaging.

European coverage is better but uneven.

Until composting infrastructure scales to match product availability, the market faces a credibility gap that limits both consumer trust and brand-owner investment.

The most strategically valuable investments in this sector over the next decade will target this infrastructure bottleneck: AI-driven sortation, specialised collection systems, and regional composting facility development.

Introduction and Framework

About This Report

This report provides a comprehensive analysis of the global market for compostable packaging films covering the period 2025 to 2035.

It is produced by Ukhi to serve packaging professionals, investors, brand owners, material scientists, and policy analysts who need a clear, evidence-based picture of this market.

The report covers:

1. the material landscape (PLA, PBAT, PHA, starch blends, PBS, and cellulose-based films),

2. key producers and converters, end-use demand segments, regulatory drivers across major economies, and

3. the commercial outlook for the decade ahead.

It is structured to be useful both as a reference document (with standardised market size tables by material and geography) and as a strategic briefing (with analysis of demand drivers, risks, and investment opportunities).

Scope and Boundaries

This report sizes the global market for compostable polymer films used in packaging applications.

The scope covers thin, flexible sheets made from certified compostable polymers, produced as rollstock and converted into packaging formats including pouches, bags, wraps, lidding films, and flow-wrap.

Included in scope:

1. Mono-layer and multi-layer compostable films for food and non-food packaging

2. Extrusion-coated compostable polymer layers on paper or board substrates, where the polymer film is the functional barrier component

3. Films certified to recognised industrial or home composting standards, including EN 13432, ASTM D6400, AS 5810, and TÜV OK Compost

Excluded from scope:

1. Rigid compostable packaging (cups, trays, clamshells, bottles)

2. Moulded fibre and paper-based compostable packaging without a polymer film layer

3. Agricultural mulch films

4. Medical and pharmaceutical films

5. Conventional biodegradable films that do not meet certified composting standards, including oxo-degradable plastics

Methodology

Market Sizing Approach

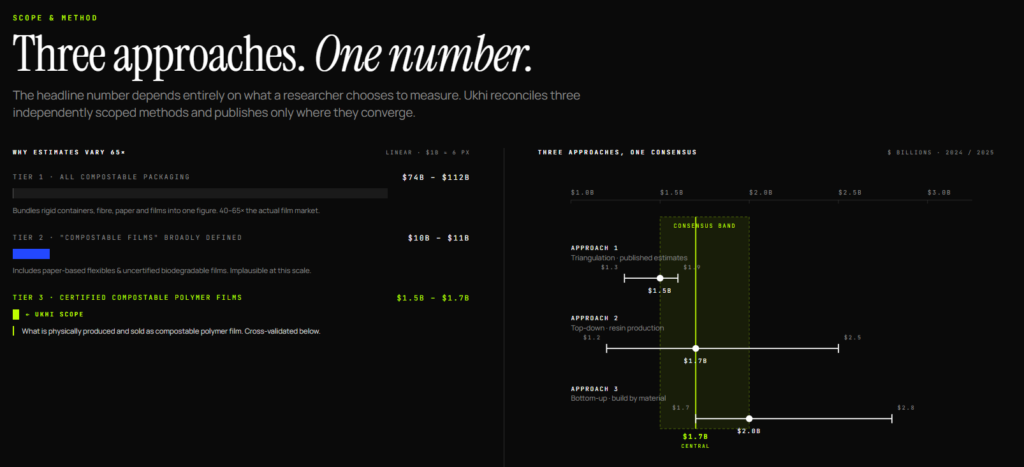

Published market data for compostable packaging films varies by a factor of seven or more depending on source and scope definition.

To navigate this, we did not rely on any single published estimate.

Instead, we applied three independent sizing approaches and used their convergence to establish a defensible range.

Approach 1: Triangulation from narrowly scoped published estimates.

We identified three published data points whose defined scope most closely matched ours: the biodegradable plastic films market (Grand View Research, $1.22 billion, 2024), the compostable flexible packaging market (Custom Market Insights, $1.63 billion in 2026, back-calculated to approximately $1.35 billion for 2024), and the compostable multilayer films market (Grand View Research, $1.42 billion, 2024, representing only multi-layer structures).

We adjusted each for known coverage gaps (cellulose-based films, mono-layer formats, coated substrates) to produce a range of $1.3 to $1.9 billion.

Approach 2: Top-down from compostable resin production.

We estimated total global compostable polymer production capacity at approximately 1.4 million tonnes, with a market value of $5 to $7 billion across all applications and formats.

We then estimated that packaging films consume 20 to 30% of this resin output and applied standard resin-to-film conversion cost markups, yielding a range of $1.2 to $2.5 billion.

Approach 3: Material-level build-up.

We estimated the packaging film market share for each of the six major compostable polymer families individually (PLA, PBAT, PHA, starch blends, PBS, cellulose), drawing on resin market data, production capacity figures, and application-specific share percentages.

Summing these individual estimates produced a range of $1.7 to $2.8 billion.

The three approaches converged on a range of $1.5 to $2.0 billion, with $1.7 billion as the central estimate for 2024/2025.

Growth Rate Derivation

The forecast CAGR of 10 to 11% was derived by filtering reported growth rates from adjacent market segments for scope relevance.

We excluded rates from overly broad categories (total compostable packaging at 6.5 to 8.4%) and overly narrow or high-growth niches (biodegradable plastic packaging at 20.1%).

The three most scope-relevant rates, compostable multilayer films (9.7%), compostable flexible packaging (12.3%), and broadly defined compostable packaging films (8.7%), clustered around a 9 to 12% range from which we selected a 10 to 11% central corridor.

Regional and Material Allocation

Regional market shares were derived by cross-referencing published regional share data (adjusted for scope differences), resin trade flow patterns, and known regulatory demand drivers.

Material-level splits followed the same logic: published share percentages from multiple sources were compared, adjusted for scope (particularly removing agricultural mulch from starch and PBAT figures), and applied to the $1.7 billion global total.

Data Sources and Limitations

Market data was drawn from published reports by Grand View Research, Custom Market Insights, Mordor Intelligence, Fortune Business Insights, Global Market Insights, Future Market Insights, Dataintelo, and European Bioplastics, supplemented by resin producer disclosures and industry press reporting.

All figures carry an estimated uncertainty of plus or minus 20 to 25%, reflecting the inherent limitations of a market where definitions are inconsistently applied across reporting firms and where a significant share of production (particularly in China) is not fully captured by Western market research methodologies.

- What Are Compostable Packaging Films?

1.1 What Is a Packaging Film?

A packaging film is a thin, flexible sheet of polymer, typically between 20 and 200 micrometres thick, used to wrap, contain, or seal products for protection, preservation, and display.

Films are the workhorse of flexible packaging: they keep moisture, oxygen, dust, and light away from the product while providing a printable surface for branding.

The conventional packaging film market is dominated by petroleum-based polymers:

1. Polyethylene (PE): the most widely used plastic film globally, valued for moisture resistance and flexibility. Subtypes include LDPE, HDPE, and LLDPE.

2. Polypropylene (PP): prized for high clarity and gloss, especially in its biaxially oriented form (BOPP), a staple of snack and confectionery packaging.

3. PET (Polyethylene Terephthalate): offers high tensile strength, thermal stability, and chemical resistance.

4. Polyamide (Nylon): used where puncture resistance and oxygen barrier performance are critical, such as vacuum-sealed meat.

5. EVOH (Ethylene Vinyl Alcohol): a specialist barrier layer for oxygen-sensitive products like dairy and baby food.

Compostable packaging films are the emerging alternative to these conventional materials.

They are engineered from bio-based or biodegradable polymers, such as PLA, PBAT, PHA, and starch blends, to deliver comparable packaging performance while breaking down safely in composting environments.

This report focuses exclusively on this category.

1.2 What Makes a Packaging Film Compostable?

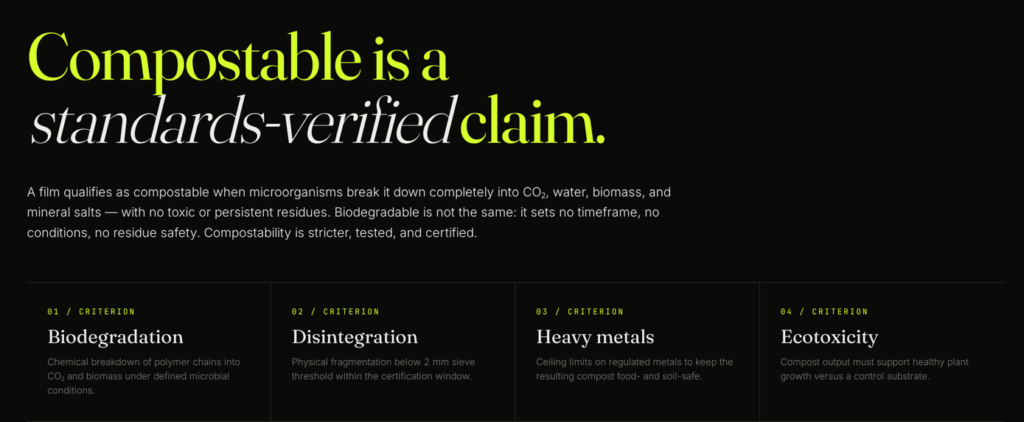

A film qualifies as compostable when microorganisms can break it down fully into carbon dioxide, water, biomass, and mineral salts, leaving no toxic or persistent residues.

Officially, to be compostable, a material has to pass tests across four criteria:

1. biodegradation (chemical breakdown of polymer chains),

2. disintegration (physical fragmentation),

3. heavy metal limits, and

4. ecotoxicity (the resulting compost must support healthy plant growth).

Key distinction: “Biodegradable” is not the same as “compostable.”

A biodegradable material will eventually break down, but with no guarantee of timeframe, conditions, or residue safety.

Compostability is a stricter, standards-verified claim.

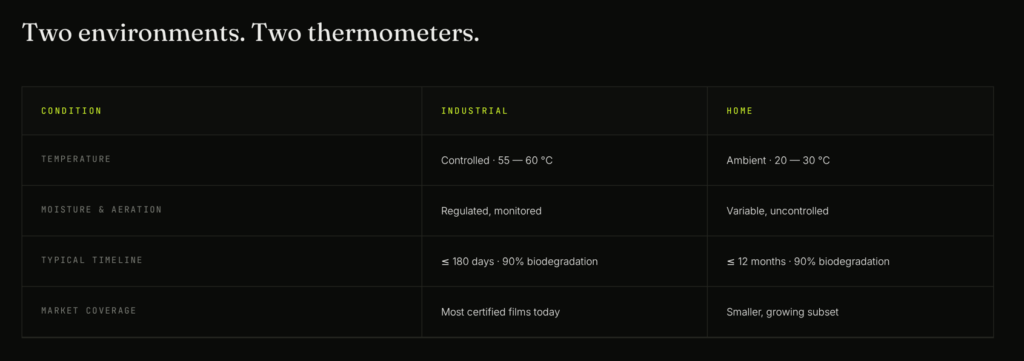

Industrial vs. Home Composting

Industrial composting takes place in controlled, high-temperature facilities (typically 55 to 60°C) with regulated moisture and aeration.

Most compostable films on the market today are certified only for this environment.

Home composting occurs at lower, variable ambient temperatures (around 20 to 30°C) in garden compost bins.

Films certified for home composting must degrade under these less predictable conditions over a longer period.

Key Standards and Certifications of Compostability

1. EN 13432: the European standard, requiring 90% biodegradation within 6 months and disintegration below 2mm within 12 weeks under industrial conditions. Compliance is marked by the Seedling label.

2. ASTM D6400: the North American equivalent, requiring 90% biodegradation within 180 days. Products meeting this standard can carry BPI Certification.

3. AS 5810: the Australian standard specifically for home compostability, requiring 90% biodegradation within 12 months at ambient temperatures.

4. TÜV OK Compost: a widely recognised certification scheme with two tiers.

1. OK compost INDUSTRIAL certifies compliance with EN 13432.

2. OK compost HOME verifies biodegradability in garden compost conditions within 12 months.

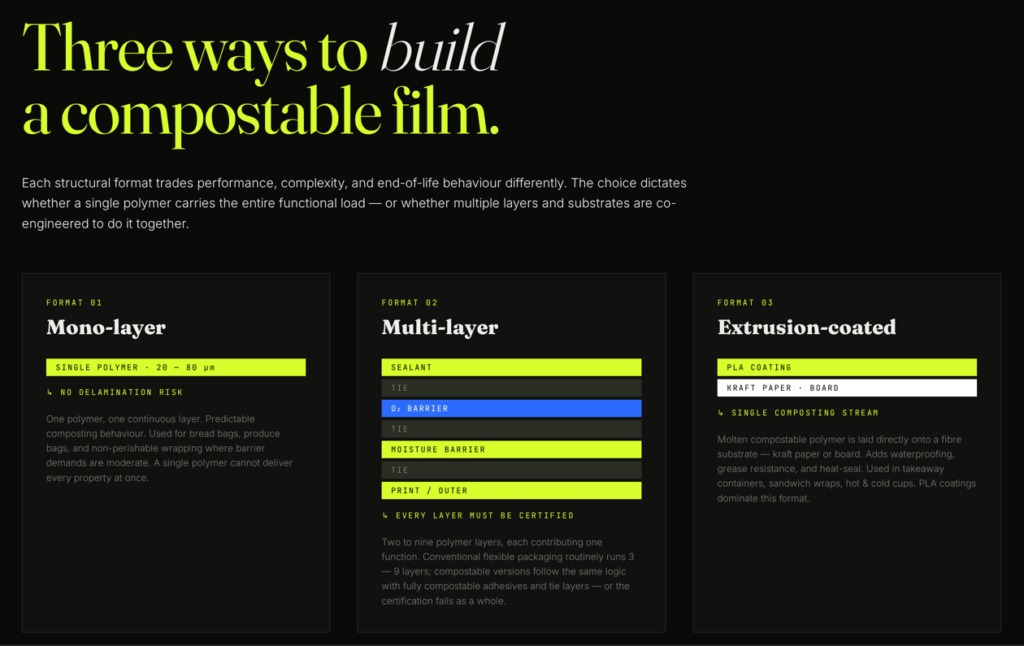

1.3 Types of Compostable Film Structures

Compostable packaging films are built in three main formats.

Each format offers a different balance of performance, complexity, and end-of-life behaviour.

Mono-layer Films

A mono-layer film is made from a single polymer or resin in one continuous layer.

These films are valued for their simplicity: there is no risk of delamination (the separation of bonded layers that causes packaging failure), and because only one material is involved, composting behaviour is more predictable.

Mono-layer compostable films are typically 20 to 80 micrometres thick and are used for applications where barrier demands are moderate, such as bread bags, produce bags, and non-perishable item wrapping.

Their limitation is that a single polymer fails to deliver high performance across all properties (barrier, strength, sealability) simultaneously.

Multi-layer and Laminate Films

Multi-layer films combine two or more polymer layers, and each layer contributes a specific function: one layer may provide an oxygen barrier, another moisture resistance, and an outer layer may be optimised for heat sealing.

Conventional flexible packaging routinely uses structures of 3 to 9 layers.

Compostable multi-layer films follow the same logic but substitute each layer with a compostable polymer.

Insight: For a multi-layer film to be certified compostable, every layer and every adhesive must independently meet the relevant composting standard. A single non-compostable tie layer or adhesive disqualifies the entire structure.

Extrusion-Coated Substrates (Film on Paper or Board)

Extrusion coating applies a thin layer of molten compostable polymer directly onto a fibre-based substrate like kraft paper or paperboard.

This gives the substrate waterproofing, grease resistance, and heat-seal capability while retaining the structural properties and consumer appeal of paper.

Common applications include takeaway containers, sandwich wraps, and hot and cold beverage cups.

PLA coatings are the most established option in this format.

When both the coating and the substrate are compostable, the entire structure can be processed in a single composting stream, which means it can avoid the separation challenges that plague conventional plastic-coated paperboard.

1.4 How Compostable Packaging Films Are Made

Three primary extrusion processes are used to manufacture compostable packaging films at industrial scale.

Blown Film Extrusion

In blown film extrusion, molten polymer is pushed through a ring-shaped (annular) die to form a continuous tube.

Air is injected into the centre of the tube, inflating it into a bubble that is pulled upward by nip rollers as it cools and solidifies.

The bubble is then collapsed and wound into flat film rolls.

In this method, the material is stretched in two directions simultaneously during inflation, which produces films with balanced mechanical properties (good strength in both the machine and cross directions).

Blown film is the dominant process for producing compostable bags, food wraps, and agricultural mulch films. Most PBAT and starch-blend films are produced this way.

Cast Film Extrusion

Cast film extrusion is a technique where molten polymer is pushed through a flat, horizontal slot die (known as a T-die) onto a chilled roller that rapidly freezes the film.

This quenching process produces films with superior thickness uniformity and optical clarity compared to blown film.

Cast extrusion is the preferred method for PLA films, where high transparency and gloss are valued, such as window films on bakery boxes, flow-wrap for confectionery, and thermoformed lidding.

An additional step called Machine Direction Orientation (MDO) stretching can be applied to further enhance strength and reduce thickness.

Extrusion Coating and Lamination

Extrusion coating applies a layer of molten resin directly onto a moving substrate (paper, board, or another film) to create a composite material in a single pass.

Extrusion lamination uses a molten resin as a bonding agent to join two separate substrates together.

Both processes operate at high speeds (exceeding 300 metres per minute) and are essential for producing liquid packaging boards, coated paper wraps, and specialty food packaging. For compostable applications, PLA is the most commonly used coating resin.

1.5 Key Performance Requirements for Compostable Packaging Films

Compostable films must meet the same functional demands as their conventional counterparts. Performance is evaluated across four areas.

Barrier Properties

1. Moisture barrier: measured by the Water Vapour Transmission Rate (WVTR).

PLA offers a reasonable moisture barrier, but starch-based films are naturally hydrophilic (moisture-absorbing) and require blending or coating to perform adequately.

2. Oxygen barrier: measured by the Oxygen Transmission Rate (OTR), critical for preventing oxidation in perishable goods.

Starch-based interlayers in multi-layer structures can function as effective gas barriers.

Advanced high-barrier compostable films can reduce oxygen transfer by up to 99% compared to standard PLA.

3. Grease resistance: essential for food contact applications.

Cellulose-based films and specialised biopolymer grades (such as BASF’s ecovio PS1606) are engineered specifically for grease and mineral oil resistance.

Sealability and Machinability

Sealability is a film’s ability to form strong, consistent bonds under heat and pressure on high-speed packaging lines.

Compostable multi-layer films typically include a dedicated sealant layer optimised for this purpose.

Machinability depends on controlling the Coefficient of Friction (COF): for vertical form-fill-seal (VFFS) machines, the film’s inner surface needs to be more slippery (COF 0.200 to 0.300) than the outer surface (COF 0.300 to 0.400) to slide over the forming tube while being gripped by pull belts.

Printability and Optics

High transparency and gloss allow consumers to see the product inside.

PLA films deliver low haze and excellent gloss comparable to conventional PET.

For printability, compostable polymers like PLA and PHA have naturally high surface energy (wettability), meaning inks adhere well without always requiring surface treatments such as corona treatment.

Mechanical Properties

1. Tensile strength and stiffness (measured by Young’s Modulus) determine resistance to pulling and rigidity.

PLA is strong and stiff but naturally brittle, with elongation at break often below 3%.

2. Tear and impact resistance are improved by blending brittle polymers like PLA with flexible materials such as PBAT.

Blends containing 60 to 70 wt% PBAT typically achieve the best balance of flexibility and strength.

3. Puncture resistance is critical for packaging products with sharp edges.

Multi-layer compostable structures can improve puncture performance by a factor of 7 to 10 compared to mono-layer films of the same thickness.

2. Compostable Packaging Films — Market Sizing

Anyone researching the compostable packaging films market size will encounter a confusing spread of numbers.

Some sources report the global market at over $10 billion.

Others put it closer to $1.5 billion.

The gap is a result of fundamentally different definitions of what is being measured.

The published data falls into three broad tiers of scope:

Tier 1: All compostable packaging (all formats, all materials)

These reports bundle rigid containers, moulded fibre, paper-based packaging, and flexible films into a single figure.

Published estimates for this tier range from $74 billion to $112 billion (2024/2025).

Some extend even further by including recyclable or “eco-friendly” packaging alongside compostable materials.

These figures are useful as context for the overall sustainable packaging landscape, but they overstate the film-specific market by a factor of 40 or more.

Tier 2: “Compostable packaging films” (broadly defined)

Two widely cited sources place this market at $10 to $11 billion (2024/2025).

These figures are labelled as film markets, but they almost certainly include paper-based flexible packaging, conventional biodegradable films without composting certification, or broader flexible packaging categories beyond polymer films.

A simple cross-check confirms the inflation: at $10 billion, compostable films alone would represent nearly 10% of the entire global packaging films market (all materials), which is implausible when compostable polymers account for well under 2% of total plastic production.

Tier 3: Compostable flexible packaging and biodegradable plastic films (narrowly defined)

Reports scoped to certified compostable flexible packaging or biodegradable plastic films specifically cluster in the $1.2 to $1.6 billion range (2024/2025).

These align much more closely with what is physically produced and sold as compostable polymer film for packaging use.

Ukhi Insight:

We base our sizing on Tier 3 data, cross-validated through three independent analytical approaches described below. Where we reference Tier 1 or Tier 2 figures, we do so only for context or sanity-checking.

2.1 How We Sized The Compostable Packaging Films Market

We used three approaches and looked for convergence in the data.

Approach 1: Triangulation from narrowly scoped published estimates.

We compared three data points closest to our scope: biodegradable plastic films ($1.22B, 2024), compostable flexible packaging ($1.63B, 2026, back-calculated to ~$1.35B for 2024), and compostable multilayer films ($1.42B, 2024, representing only the multi-layer subset). Adjusting for coverage gaps (cellulose-based films, mono-layer formats), this approach yields a range of $1.3 to $1.9 billion, centred around $1.5 billion.

Approach 2: Top-down from compostable resin production.

Total global compostable polymer production capacity is approximately 1.4 million tonnes, with an estimated market value of $5 to $7 billion across all applications and formats. Packaging films consume an estimated 20 to 30% of this resin output (the remainder going to rigid packaging, agricultural film, and non-packaging uses). Applying conversion cost markups from resin to finished film gives a range of $1.2 to $2.5 billion, with a midpoint around $1.7 billion.

Approach 3: Material-level build-up.

We estimated the packaging film share of each major resin market individually (PBAT, PLA, PHA, starch blends, PBS, cellulose) and summed them. This bottom-up approach produced a range of $1.7 to $2.8 billion, centred on $2.0 billion. The higher figure reflects the inclusion of resin-to-film conversion value and may slightly overcount where source data already incorporates some downstream value.

Consensus:

The three approaches converge on a global compostable packaging films market size of approximately $1.5 to $2.0 billion in 2024/2025, with $1.7 billion as our central estimate.

2.2 Compostable Packaging Films – Global Market Size and Forecast (2025 to 2035)

The compostable packaging films market is valued at approximately $1.7 billion globally in 2025.

We project the compostable packaging films market to grow at a compound annual growth rate (CAGR) of 10 to 11% over the forecast period, reaching approximately $4.4 to $4.8 billion by 2035, with a central forecast of $4.6 billion.

This CAGR is derived from growth rates reported across the most closely scoped market segments:

1. compostable multilayer films (9.7% CAGR),

2. compostable flexible packaging (12.3%), and

3. broadly defined compostable packaging films (8.7%).

The 10 to 11% range sits at the centre of this cluster, reflecting a market that is growing faster than mature biodegradable plastic films (4.5%) but not as fast as niche high-growth segments like biodegradable plastic packaging overall (20%), which is inflated by rapid rigid-format substitution in food service.

Key assumption:

This forecast assumes continued regulatory tightening, particularly the EU Packaging and Packaging Waste Regulation (PPWR) taking full effect around 2030, steady expansion of industrial composting infrastructure, and no major supply disruption in PLA or PBAT resin (where Chinese capacity additions are critical).

Downside scenarios (regulatory delays, infrastructure bottlenecks) could compress the CAGR to 7 to 8%.

Upside scenarios (faster PHA cost reduction, home-compostable breakthroughs, broader global bans on conventional flexible packaging) could push it to 13 to 15%.

Penetration context:

At $4.6 billion in 2035, compostable packaging films would represent roughly 2.8% of the total global packaging films market (projected at ~$167 billion), up from approximately 1.6% today. This near-doubling of market share over a decade is ambitious but consistent with the regulatory trajectory in major economies.

2.3 Compostable Packaging Films – Regional Market Analysis

Compostable Packaging Films Market In Europe: The Regulatory Leader

Estimated compostable packaging films market size: ~$695 million (2025), approximately 40.9% of the global total.

Europe leads the compostable packaging films market by a significant margin, driven by the world’s most mature regulatory framework and the most developed composting infrastructure.

EN 13432 is the benchmark certification standard globally, and the EU Single-Use Plastics Directive has created mandatory demand for compostable alternatives in several product categories.

Germany alone accounts for an estimated 22% of European demand, followed by Italy (which has mandated compostable carrier bags since 2011), France (growing rapidly at nearly 20% annually as new domestic production capacity comes online), and the Nordic countries.

Europe’s lead is demand-driven, not production-driven. The region imports significant volumes of PLA and PBAT resin from Asia, particularly China, and converts it into finished films domestically. This makes European converters strategically dependent on Asian resin supply chains.

Compostable Packaging Films Market In Asia-Pacific: The Production Powerhouse

Estimated compostable packaging films market size: ~$558 million (2025), approximately 32.8% of the global total.

Asia-Pacific is the fastest-growing regional market for compostable films and the dominant global production base.

China controls over 60% of global PBAT manufacturing capacity and is rapidly scaling PLA production through producers like Zhejiang Hisun, Anhui BBCA, and others.

Domestic demand within China is growing alongside production, driven by provincial single-use plastic restrictions rolling out since 2020.

Japan represents an estimated 15% of global compostable packaging film consumption, reflecting the country’s advanced waste management systems and strong brand-owner commitment to sustainable packaging.

India’s compostable films segment is growing at approximately 11% annually, accelerated by the nationwide ban on identified single-use plastics under the Plastic Waste Management Rules (2022), though composting infrastructure remains a constraint.

Insight: Asia-Pacific’s 32% demand share understates its strategic importance. The region controls upstream resin supply for the two largest compostable film polymers. Any policy shift or supply disruption in China would ripple through the global compostable film supply chain.

Compostable Packaging Films Market In North America: Ambition Outpacing Infrastructure

Estimated compostable packaging films market size: ~$325 million (2025), approximately 19.1% of the global total.

The North American compostable packaging films market is driven primarily by corporate sustainability commitments from major brand owners and retailers (Walmart, Amazon, PepsiCo) rather than regulatory mandates.

The United States accounts for the large majority of regional demand, with California and Washington leading at the state level through compostable packaging requirements for food service.

However, North America faces a structural constraint: the “composting gap.”

The U.S. has only approximately 185 full-scale composting facilities that accept food-soiled packaging, compared to thousands across Europe.

This limits the practical addressable market, because brand owners are reluctant to invest in compostable packaging formats when end-of-life composting cannot be guaranteed for most consumers.

Canada shows high growth potential following federal single-use plastics regulations, but from a small base.

Compostable Packaging Films Market In Middle East and Emerging Markets

Estimated compostable packaging films market size: ~$122 million (2025), approximately 7.2% of the global total.

This grouping covers the Middle East, Africa, and Latin America.

The Middle East is the most active sub-region, with the UAE and Saudi Arabia implementing aggressive single-use plastic bans that are creating new demand for compostable alternatives.

Saudi Arabia holds the largest share of Middle Eastern revenues (approximately 36%), though the absolute base remains small.

In Latin America, Brazil is the primary market, driven by municipal waste legislation in São Paulo and other major cities.

Africa’s compostable film market is negligible in absolute terms (likely under $10 million continent-wide), though countries like South Africa and Kenya are beginning to explore compostable packaging through pilot programmes linked to single-use plastic bans.

These markets collectively represent the earliest stage of the adoption curve, with growth constrained by limited composting infrastructure and low consumer awareness of compostable packaging as a distinct category.

Table: Compostable Packaging Films – Regional Market Size

| Region | Share of Global | Market Size (2025) |

|---|---|---|

| Europe | 40.9% | $695M |

| Asia-Pacific | 32.8% | $558M |

| North America | 19.1% | $325M |

| ME & Emerging | 7.2% | $122M |

| Total | 100% | $1,700M |

3. Compostable Packaging Films — Market by Material

3.1 PLA (Polylactic Acid) for Compostable Packaging Films

3.1.1 PLA Film Properties and Processing Behaviour

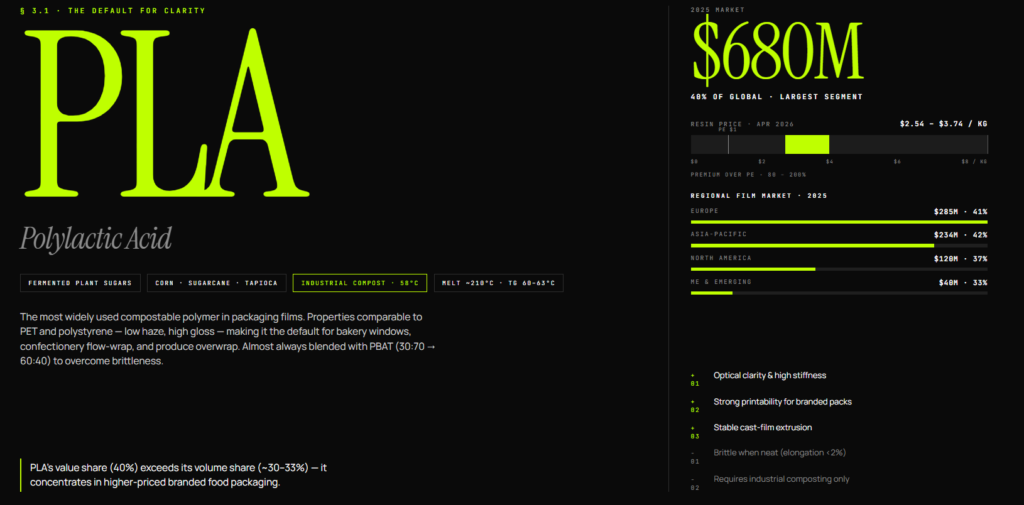

Polylactic acid (PLA) is a biobased thermoplastic derived from fermented plant sugars, most commonly sourced from corn starch, sugarcane, or tapioca.

It is the most widely used compostable polymer in packaging films, valued for its high stiffness, optical clarity, and mechanical strength, which are comparable to conventional PET and polystyrene.

PLA’s key advantage for packaging is visual: it produces films with low haze and high gloss, which makes it the default choice for applications where the consumer needs to see the product inside, such as bakery windows, confectionery flow-wrap, and fresh produce overwrap.

However, PLA has well-known limitations in film applications:

1. Brittleness: Pure PLA has very low elongation at break (often under 2%), meaning it cracks rather than stretches under stress. This makes it unsuitable as a standalone material for flexible bags or pouches.

2. Narrow composting window: PLA is predominantly amorphous and requires industrial composting conditions (approximately 58°C and high humidity) to biodegrade effectively. It does not break down reliably in home compost or ambient soil.

3. Bubble instability: In blown film extrusion, pure PLA produces unstable film bubbles with frequent breakage during stretching, which limits its use in that process without modification.

For these reasons, PLA is nearly always blended with PBAT in flexible film applications, typically in ratios of 30:70 to 60:40 (PLA:PBAT).

PBAT provides the flexibility and elongation that PLA lacks, while PLA contributes stiffness, clarity, and printability.

In cast film extrusion, PLA performs well with fewer modifications, which is why it dominates applications like lidding films and thermoformed overwrap.

Processing note: PLA resins must be pre-dried before extrusion to prevent degradation. Typical melt temperatures for film-grade PLA sit around 210°C, with a glass transition temperature of 60 to 63°C and tensile strength exceeding 60 MPa.

3.1.2 PLA Cost

PLA resin prices vary significantly by region. As of April 2026:

| Region | Price (USD/kg) |

|---|---|

| Europe | $3.66 to $3.74 |

| Southeast Asia | $2.98 to $3.04 |

| Northeast Asia | $2.67 to $2.72 |

| North America | $2.54 to $2.60 |

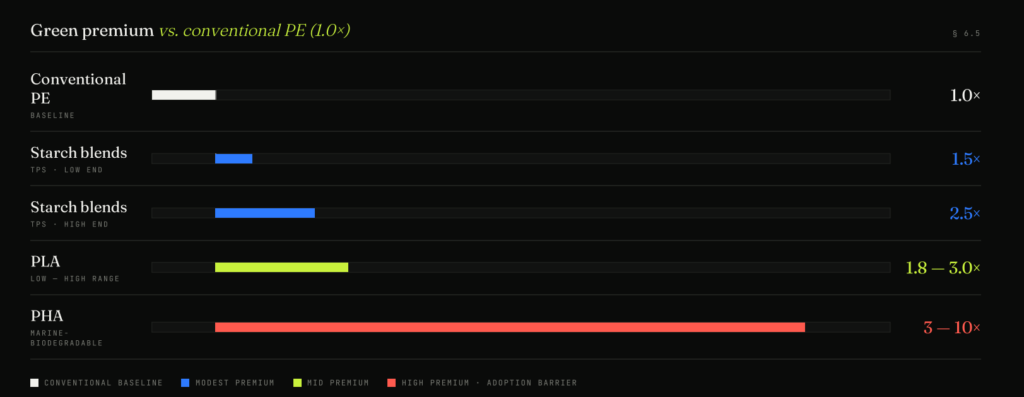

PLA commands an 80% to 200% price premium over conventional polyethylene.

The primary cost driver is the price of fermentable sugars and lactic acid feedstock, which together dominate resin economics.

In early 2026, Northeast Asian prices rose by 10.3% on strong demand from the biodegradable packaging sector, while European prices softened under competition from lower-priced Asian imports.

The geographic price gap reflects both feedstock costs and production scale. China and Southeast Asia benefit from cheaper agricultural inputs and newer, larger-scale production facilities. Europe’s higher prices reflect import logistics and a smaller domestic production base.

3.1.3 PLA for Compostable Packaging Films – Market Size

PLA is the largest material segment in the compostable packaging films market, representing approximately 40% of global revenue in 2025.

Global: We estimate the PLA (for compostable packaging films) market at approximately $680 million in 2025.

PLA dominates cast film applications (lidding, overwrap, flow-wrap) and is the primary resin for extrusion-coated paper and board substrates.

Its share is higher by value than by volume (estimated 30 to 33% by volume) because PLA films concentrate in branded food packaging where per-unit prices are higher.

For context, PLA is used across the broader packaging industry well beyond films.

Published sources report PLA holding 38% of the compostable flexible packaging market and 44% of the compostable multilayer films segment.

Our 40% share for packaging films specifically sits within this range, which reflects PLA’s dominance in cast film formats that are less prominent in the broader flexible packaging category.

Regional breakdown:

1. Europe (~$285M, 41% of regional film market): The largest single regional market for PLA films. European converters import significant PLA resin from Asia and convert it domestically into food packaging films. Germany, France, and the Nordics are the primary demand centres.

2. Asia-Pacific (~$234.4M, 42% of regional film market): China is both the fastest-growing PLA producer and a major consumer. Domestic PLA film consumption is rising alongside export-oriented production from manufacturers including Zhejiang Hisun and Anhui BBCA.

3. North America (~$120M, 37% of regional film market): PLA cast films and PLA-coated substrates are common in food service packaging. The lower PLA share relative to other regions reflects stronger competition from PBAT-based products in the U.S. carrier bag segment.

4. Middle East and Emerging Markets (~$40.3M, 33%): PLA’s wide availability and established supply chains make it the default entry material for markets in early stages of compostable packaging adoption.

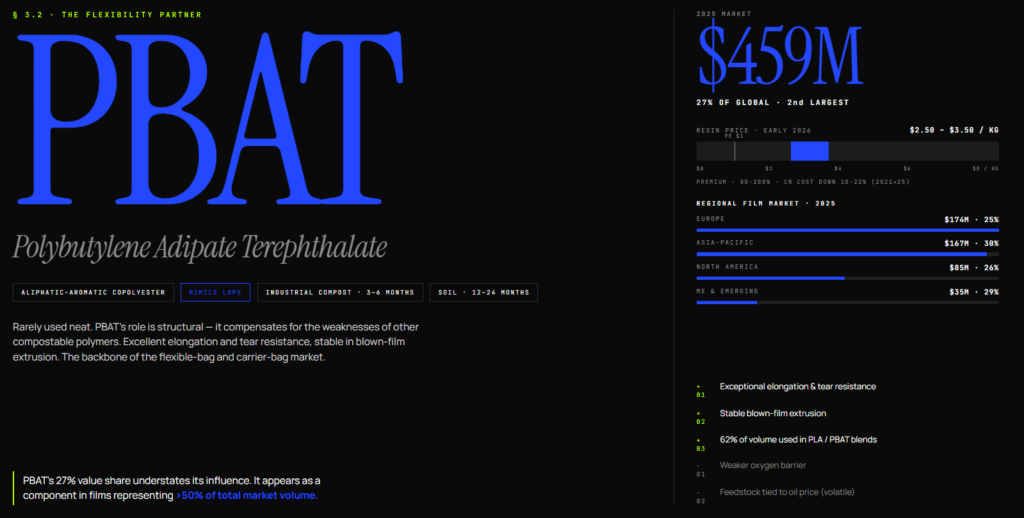

3.2 PBAT (Polybutylene Adipate Terephthalate) for Compostable Packaging Films

3.2.1 PBAT Film Properties and Processing Behaviour

Polybutylene adipate terephthalate (PBAT) is an aliphatic-aromatic co-polyester whose mechanical properties closely mimic those of low-density polyethylene (LDPE), the conventional plastic most widely used for bags and flexible wraps.

This makes PBAT the natural compostable substitute in applications where flexibility and toughness matter more than clarity or stiffness.

PBAT’s defining characteristics for film applications:

1. Flexibility and elongation: PBAT offers exceptional elongation at break and tear resistance, which makes it useful to produce films that stretch and bend without cracking.

2. Stable processing: PBAT runs well on conventional blown film, cast film, and extrusion coating equipment with minimal modifications. Its aromatic molecular segments provide processability, while the aliphatic segments ensure biodegradability. Film bubbles are stable during blown extrusion, which is a significant practical advantage over pure PLA.

3. Composting profile: PBAT typically degrades within 3 to 6 months under industrial composting conditions and 12 to 24 months in soil environments.

4. Limitations: PBAT has lower thermal resistance and a weaker oxygen barrier compared to aromatic polyesters, which limits its use in high-barrier applications without blending or multi-layering.

3.2.2 PBAT as a Blend Component vs. Standalone Film

PBAT is rarely used in pure form for commercial packaging films.

Its primary role is as a system component that compensates for the weaknesses of other compostable polymers.

PLA/PBAT blends are the backbone of the compostable flexible packaging industry.

PLA alone is too brittle; PBAT alone is too soft.

Blended in ratios of 30:70 to 60:40, the two produce films with both structural integrity and flexibility.

In 2025, approximately 62% of global PBAT volume was consumed in PLA/PBAT blends.

TPS/PBAT blends combine thermoplastic starch with PBAT for cost-effective carrier bags and bin liners, particularly in European markets where Novamont’s Mater-Bi product family dominates.

PHA/PBAT and mineral-filled blends serve more specialised applications with specific degradation or mechanical targets.

Insight: PBAT’s influence on the compostable films market is substantially larger than its standalone revenue suggests. While PBAT accounts for approximately 27% of the market under our categorisation (where revenue is attributed to the majority resin in a blend), PBAT appears as a component in films representing over 50% of total market volume.

3.2.3 PBAT Cost

As of early 2026, PBAT resin prices sit in a broadly similar range to PLA, typically $2.50 to $3.50 per kilogram depending on region and grade, though subject to sharper short-term volatility due to petrochemical feedstock exposure.

PBAT-based products command an 80% to 200% price premium over conventional polyethylene equivalents.

The resin is synthesised from 1,4-butanediol, adipic acid, and purified terephthalic acid, a process that remains more expensive than PE production even at current scale.

Chinese producers have driven the most significant cost reductions, lowering production costs by 18 to 22% between 2021 and 2025 through economies of scale.

Despite this progress, PBAT retains a structural cost gap because its petrochemical feedstocks (adipic acid and terephthalic acid) track oil-derived commodity prices, while conventional PE benefits from the same cheap fossil inputs without the added synthesis complexity.

In early March 2026, U.S. PBAT prices spiked by over 78% due to supply disruptions, highlighting the market’s vulnerability to feedstock volatility.

3.2.4 PBAT for Compostable Packaging Films – Market Size

PBAT and PBAT-dominant blends represent approximately 27% of the global compostable packaging films market, valued at an estimated $459 million in 2025.

Global: The total PBAT resin market across all applications was valued at approximately $1.8 billion in 2025.

Of this, the films segment (including agricultural mulch) accounted for $693 million.

After excluding agricultural mulch films (which consume an estimated 35 to 45% of PBAT film production) and adjusting for our packaging-only scope, the PBAT compostable packaging films segment sits at approximately $460 million.

PBAT’s market presence is concentrated in blown film applications: carrier bags, produce bags, bin liners, and flexible food wraps.

These are high-volume, lower-value-per-unit products compared to PLA’s cast film applications, which explains why PBAT’s 27% value share translates to a higher volume share of roughly 30 to 35%.

Regional breakdown:

1. Europe (~$173.8M, 25% of regional film market): Strong demand driven by EN 13432 certified carrier bags and food packaging wraps, with particular concentration in Italy, France, and Germany.

2. Asia-Pacific (~$167.4M, 30% of regional film market): China is both the world’s largest PBAT producer and a major domestic consumer. India’s ban on single-use plastics below certain thickness thresholds has triggered significant conversion to PBAT-based films.

3. North America (~$84.5M, 26%): PBAT is primarily used as a blending partner for PLA in flexible films and as a coating on paper substrates for food service.

4. Middle East and Emerging Markets (~$35.4M, 29%): Growing from a small base as single-use plastic bans take effect across the Gulf states.

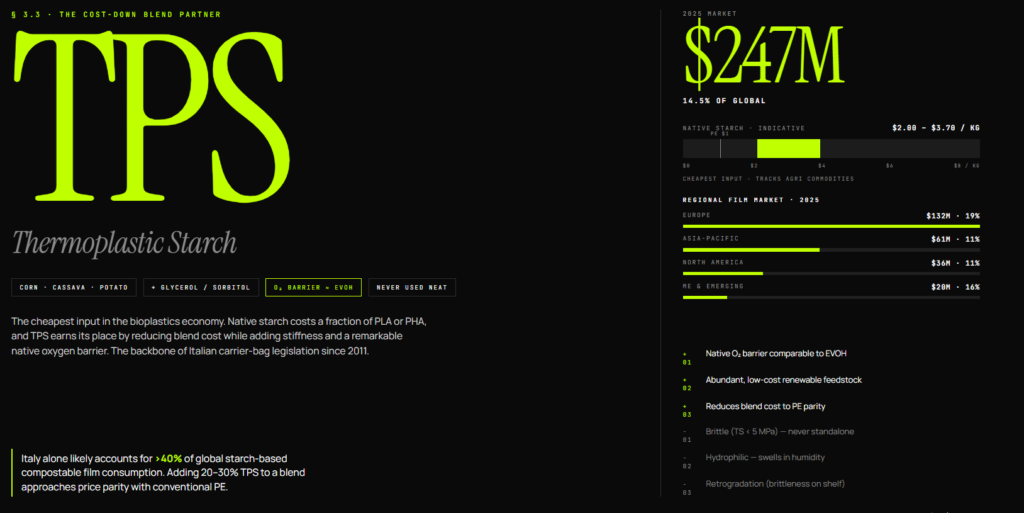

3.3 Starch-Based Films (TPS and Blends) for Compostable Packaging Films

3.3.1 TPS Film Properties and Limitations

Thermoplastic starch (TPS) is produced by heating native starch (from corn, cassava, or potato) with plasticisers such as glycerol or sorbitol under shear force.

This process breaks down the semi-crystalline structure of raw starch and turns it into a mouldable, extrudable thermoplastic.

TPS brings two strong advantages to compostable packaging films.

1. It is derived from abundant, inexpensive renewable feedstock.

2. It delivers excellent oxygen barrier properties, comparable to EVOH, one of the best conventional barrier materials.

However, TPS has serious limitations in its neat form that prevent standalone use:

1. Mechanical weakness: Tensile strength is typically below 5 MPa, with very low elongation at break (under 50%), making pure TPS films brittle and fragile.

2. Moisture sensitivity: TPS is naturally hydrophilic (water-absorbing). Exposure to humidity causes swelling and rapid loss of structural integrity, which is fundamentally incompatible with most packaging applications.

3. Retrogradation: Over time, TPS undergoes recrystallisation, becoming increasingly brittle during storage. This makes shelf life unpredictable for pure TPS products.

For these reasons, TPS is used almost exclusively as a blend component rather than a standalone film material.

3.3.2 TPS Blend Strategies

TPS/PBAT blends are the dominant commercial format.

PBAT provides the flexibility, tear resistance, and hydrophobic protection that TPS lacks, while TPS adds stiffness (higher Young’s modulus) and reduces overall material cost.

These blends form the basis of most compostable carrier bags and bin liners sold in Europe, with Novamont’s Mater-Bi product family being the most established commercial example.

TPS/PLA blends take a different approach.

Here, the glycerol in TPS acts as a plasticiser for the PLA matrix, lowering PLA’s glass transition temperature and improving its elongation at break.

Research indicates that 20 to 30 wt% TPS is the optimal loading range before phase separation and film quality begin to degrade.

Technical note: A critical challenge in all TPS blends is that starch is hydrophilic while PBAT and PLA are hydrophobic, resulting in poor interfacial adhesion. Commercial formulations address this through reactive compatibilisers (such as glycidyl methacrylate) that create chemical bridges between the starch and polyester phases, or through inorganic nanofillers like montmorillonite clay that improve phase compatibility and mechanical performance.

3.3.3 TPS Cost

Starch is the most cost-competitive raw material in the bioplastics industry.

Native starch costs a fraction of PLA ($2.00 to $3.70/kg) or PHA ($4.00 to $7.00/kg), and its primary commercial role is as an inexpensive filler that reduces the total cost of blends built around more expensive biopolymers.

Adding 20 to 30% TPS to a PBAT or PLA blend can bring the final material cost close to price parity with conventional polyethylene, which is a significant factor in the high-volume, low-margin carrier bag market.

The main cost risk is feedstock volatility: starch prices track global corn, tapioca, and potato commodity markets, which are subject to agricultural cycles and climate events.

3.3.4 TPS for Compostable Packaging Films – Market Size

Starch-based films represent approximately 14.5% of the global compostable packaging films market, valued at an estimated $246.5 million in 2025.

Global: Published data reports starch blends holding 41.72% of the biodegradable plastic films market ($1.22B, GVR 2024).

However, that figure includes agricultural mulch films, where TPS commands over 61% share.

After removing agri-mulch and non-packaging applications, starch’s share of compostable packaging films specifically drops to approximately 14.5%.

Starch films hold a high volume share but a lower value share because the end applications (carrier bags, bin liners, produce bags) are low-value products and the starch component itself is cheap.

Regional breakdown:

1. Europe (~$132.1M, 19% of regional film demand): The dominant market globally for starch-based films, driven almost entirely by Italy’s mandatory compostable carrier bag law (in force since 2011). Italy alone likely accounts for over 40% of global starch-based compostable film consumption.

2. Asia-Pacific (~$61.4M, 11%): Growing steadily, particularly in Southeast Asian markets where cassava-based starch feedstock is abundant and cheap. India is a notable emerging market, with local startups developing cost-effective starch-based films for the food delivery sector.

3. North America (~$35.8M, 11%): Modest presence. Starch-blend bags are available but compete against established PLA and PBAT alternatives with stronger brand recognition among U.S. converters.

4. Middle East and Emerging Markets (~$19.5M, 16%): Specialist suppliers (such as Ecoway Global in the UAE) provide starch-based compostable bags and waste liners to meet new single-use plastic regulations in the Gulf states.

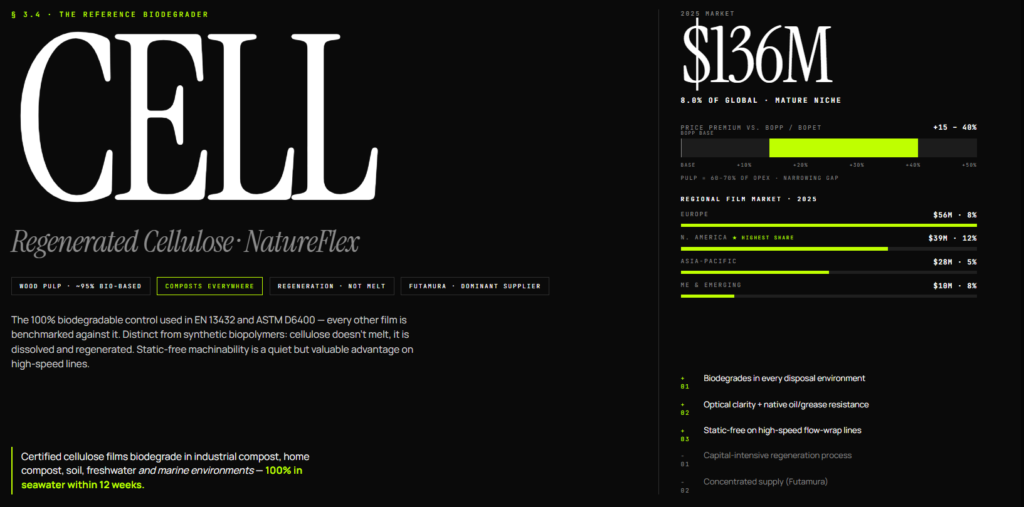

3.4 Cellulose-Based Films for Compostable Packaging Films

3.4.1 Cellulose Film Properties and Behaviour

Cellulose-based films are produced from regenerated cellulose, the most abundant natural biopolymer, sourced primarily from wood pulp.

The leading commercial product is Futamura’s NatureFlex range, which typically contains approximately 95% renewable bio-based content by weight.

Cellulose films offer a distinctive combination of properties that sets them apart from synthetic biopolymers:

1. Optical clarity and stiffness: Unlike soft biopolymers like PBAT, cellulose films are dimensionally stable with high stiffness, making them suitable for twist-wrap confectionery, flow-wrap, and window applications where a crisp, clear presentation is essential.

2. Barrier performance: Native cellulose is hydrophilic and porous, but modern coated cellulose films deliver excellent oxygen and grease resistance. Advanced bio-coatings have narrowed the moisture barrier gap with fossil-based films, extending cellulose into frozen food and pharmaceutical applications.

3. Oil and fat resistance: High resistance to grease penetration makes cellulose films well suited to snack and confectionery packaging without additional treatment layers.

4. Key differentiator: Cellulose is the reference material for biodegradability, used as the 100% biodegradable control in international composting standards including EN 13432 and ASTM D6400. Certified cellulose films biodegrade in industrial compost, home compost, soil, freshwater, and marine environments. Some certified forms achieve 100% disintegration in seawater within 12 weeks. This breadth of end-of-life options is unmatched by any synthetic biopolymer except PHA.

3.4.2 How Cellulose Film Processing Differs from Synthetic Biopolymers

Cellulose films are manufactured through a fundamentally different process than PLA, PBAT, or PHA:

1. Regeneration, not melting: Native cellulose does not melt. It must be dissolved in a solvent system (the viscose process or ionic liquids) and then regenerated into film form through a coagulation bath. This is a chemical process, not the melt-extrusion used for synthetic biopolymers, and it requires specialised capital equipment.

2. Machinability: Once formed, cellulose films are static-free, a practical advantage on high-speed flow-wrap and form-fill-seal lines where static buildup causes misfeeds and downtime with synthetic films.

3. Heat sealing: Pure cellulose does not heat-seal. Commercial grades are finished with a biodegradable coating that provides a heat-seal range of approximately 170°F to 390°F, ensuring compatibility with standard packaging machinery.

The capital-intensive nature of the regeneration process and the need for solvent recovery systems are the main reasons why cellulose film production is concentrated among a small number of manufacturers, with Futamura holding the dominant global position.

3.4.3 Cellulose Film Cost

Cellulose films command a 15% to 40% price premium over comparable petroleum-based films like BOPP or BOPET.

This is a notably smaller premium than PLA (80 to 200% over PE) or PHA (3 to 10x over PE), reflecting cellulose’s more mature production base and established supply chains.

The primary cost driver is wood pulp feedstock, which typically accounts for 60 to 70% of a production plant’s operating expenses.

The capital-intensive regeneration process and sophisticated solvent recovery requirements add further cost.

However, the price gap with conventional films is gradually narrowing as fossil-based resin costs rise and cellulose manufacturing scales, particularly in Asia-Pacific.

3.4.4 Cellulose for Compostable Films Packaging – Market Size

Cellulose-based films represent approximately 8% of the global compostable packaging films market, valued at an estimated $136 million in 2025.

This is a stable, mature segment rather than a high-growth one, reflecting the concentrated supply base (Futamura dominance) and the premium positioning in specific packaging niches.

Regional breakdown:

1. Europe (~$55.6M, 8%): The largest regional market in absolute terms. Cellulose films are established in premium confectionery packaging (twist-wraps, chocolate bar overwrap) and increasingly in organic food retail, where the combination of bio-based credentials and home compostability aligns with consumer expectations.

2. Asia-Pacific (~$27.9M, 5%): A smaller share reflecting the region’s price sensitivity and the dominance of cheaper PLA and PBAT alternatives. However, Japan is a notable exception, with established cellulose film use in premium food gifting and convenience store packaging.

3. North America (~$39M, 12% of regional film demand): The highest cellulose share of any region. North American brand owners are willing to pay the premium for NatureFlex in confectionery, bakery, and premium snack applications where optical clarity and shelf appeal drive purchasing decisions. Cellulose’s home compostability is also an advantage in a region where industrial composting infrastructure is limited.

4. Middle East and Emerging Markets (~$9.8M, 8%): Small volumes, with emerging interest driven by startups using local agricultural residue to develop regionally produced cellulose-based films as an alternative to imported synthetic biopolymers.

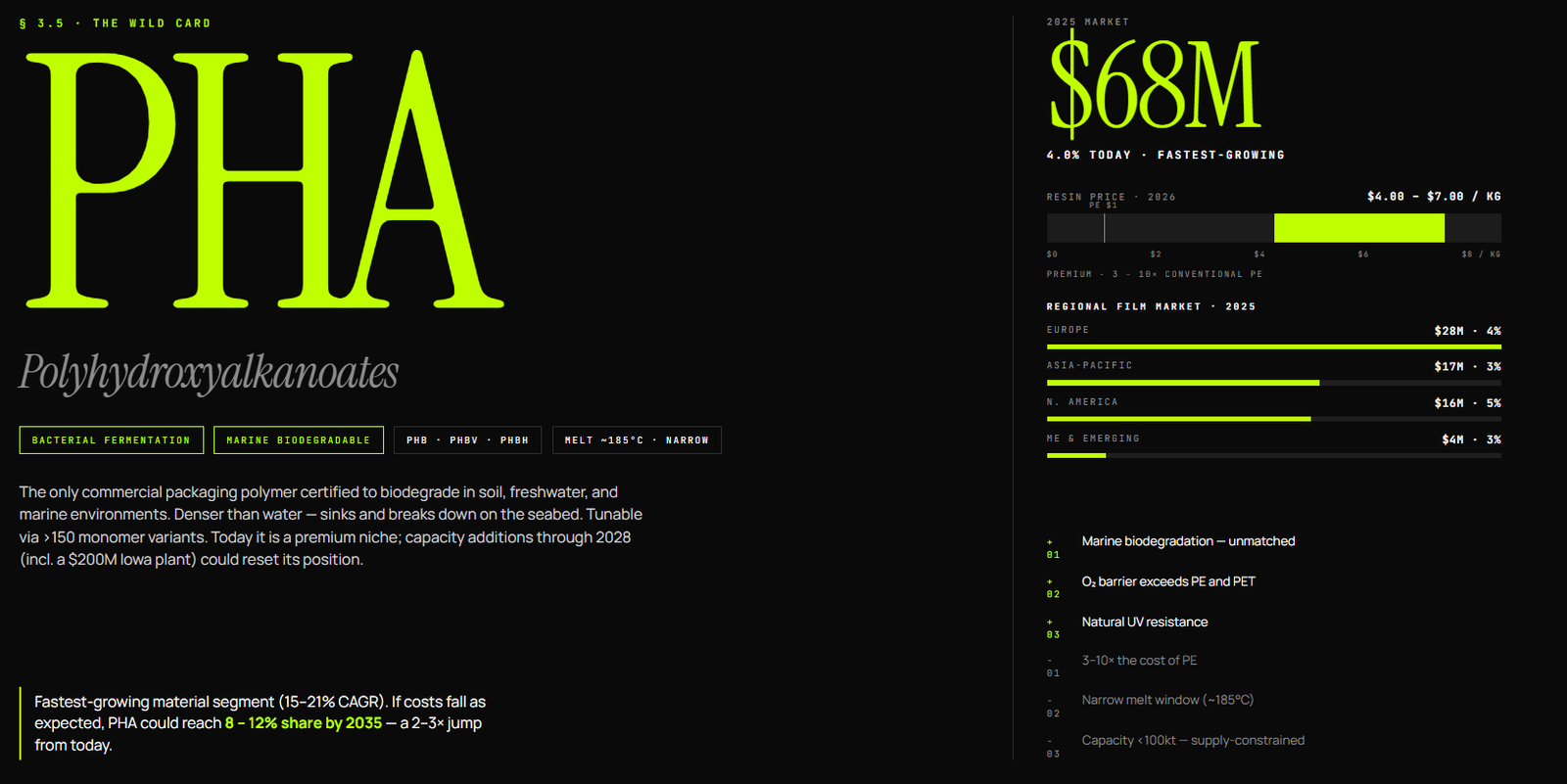

3.5 PHA (Polyhydroxyalkanoates) for Compostable Packaging Films

3.5.1 PHA Film Properties and Behaviour

Polyhydroxyalkanoates (PHA) are a family of biopolyesters produced naturally by microorganisms through bacterial fermentation.

Unlike PLA or PBAT, which are chemically synthesised, PHA is fully biosynthesised, which makes it unique among compostable packaging polymers.

The PHA family includes over 150 different monomers. This allows for PHA’s properties to be tuned to specific packaging requirements.

The three main PHA types relevant to packaging films:

1. Short-chain-length PHAs (e.g. PHB): Highly crystalline, stiff, and strong but brittle, with properties similar to polypropylene. Limited use in flexible films without modification.

2. Medium-chain-length PHAs: Elastomeric and flexible with lower melting points, suited to soft packaging films that need to bend without cracking.

3. Copolymers (PHBV, PHBH): The commercially relevant grades for packaging. These balance stiffness with flexibility and offer improved processing behaviour over pure PHB.

PHA’s standout advantage is its barrier performance.

Its oxygen barrier is superior to both PE and PET, and it is naturally hydrophobic and water-insoluble, which means it delivers moisture resistance that outperforms polypropylene.

It also provides natural UV resistance, protecting light-sensitive contents.

Key differentiator: PHA is the only commercially available packaging polymer certified to biodegrade in soil, freshwater, and marine environments.

It is denser than water and sinks to the ocean floor, where microbial activity in the benthic zone breaks it down completely.

This marine biodegradability sets PHA apart from every other compostable film material and is its primary commercial justification in coastal, seafood, and marine-adjacent packaging.

The main processing challenge is a narrow thermal window: pure PHB melts close to the temperature at which it begins to degrade (~185°C), requiring strict temperature control during extrusion.

Copolymers like PHBV can widen this window.

Biaxially oriented PHA (BoPHA) films have been developed to deliver high clarity, good printability, and quiet, flexible handling.

3.5.2 PHA Cost

PHA is the most expensive compostable film material on the market.

Current resin price: $4.00 to $7.00 per kilogram, approximately 3 to 10 times the cost of conventional PE or PP ($1.00 to $1.74/kg) and significantly above PLA ($2.00 to $3.00/kg in most regions).

Cost structure: Fermentation feedstocks account for 50 to 60% of production cost.

Downstream processing (extracting PHA from bacterial cells) adds another 30 to 50%.

Maintaining sterile fermentation conditions is a further significant expense.

Cost reduction pathway: The industry is moving toward next-generation industrial biotechnology (NGIB), using halophilic (salt-tolerant) bacteria that can operate in unsterile, open-tank, continuous production using seawater.

Combined with a shift to waste-based feedstocks (food waste, sewage sludge, captured CO₂), this approach could substantially reduce both capital and operating costs.

A $200 million, 75,000-tonne PHA plant in Iowa (scheduled for 2028 startup) is a good example of the scale of investment now entering the sector.

3.5.3 PHA for Compostable Packaging Films – Market Size

PHA represents approximately 4% of the global compostable packaging films market, valued at an estimated $68 million in 2025.

It is the smallest of the six material segments by revenue but the fastest-growing, with reported CAGRs of 15 to 21% across various PHA packaging sub-segments.

Global: The total PHA market for all packaging applications was approximately $97 million in 2024.

Films represent a subset of this, with the remainder in rigid formats and experimental applications.

PHA films are currently a premium, low-volume niche concentrated in applications where marine biodegradability is a genuine functional requirement (coastal food service, seafood packaging) or where home compostability is needed and PLA cannot deliver.

Production is constrained by limited global manufacturing capacity (under 100,000 tonnes) and the price premium described above.

The capacity picture will shift meaningfully in the second half of our forecast period.

The Iowa plant and Chinese government subsidies for bio-resin expansion signal that PHA supply constraints should ease from 2028 onward.

If costs fall as expected, PHA’s market share could reach 8 to 12% by 2035.

Regional breakdown:

1. Europe (~$27.8M, 4% of regional film market): The largest PHA films market today, driven by coastal and marine-focused regulations in Nordic, Baltic, and Mediterranean economies. European demand is shaped by tightening rules on plastic leakage into the Baltic and North Sea, which specifically favour PHA over industrially-compostable-only materials like PLA.

2. Asia-Pacific (~$16.7M, 3%): The region is seeing the most rapid PHA capacity additions, supported by Chinese subsidies and abundant fermentation feedstock. However, domestic demand for premium-priced PHA films remains limited relative to cheaper PLA and PBAT alternatives.

3. North America (~$16.3M, 5%): Investment activity is high (the Iowa plant is the flagship example) but current film consumption is small, concentrated in pilot programmes with premium brand owners.

4. Middle East and Emerging Markets (~$3.7M, 3%): Negligible current demand. PHA’s cost premium puts it beyond the reach of most emerging market applications at present.

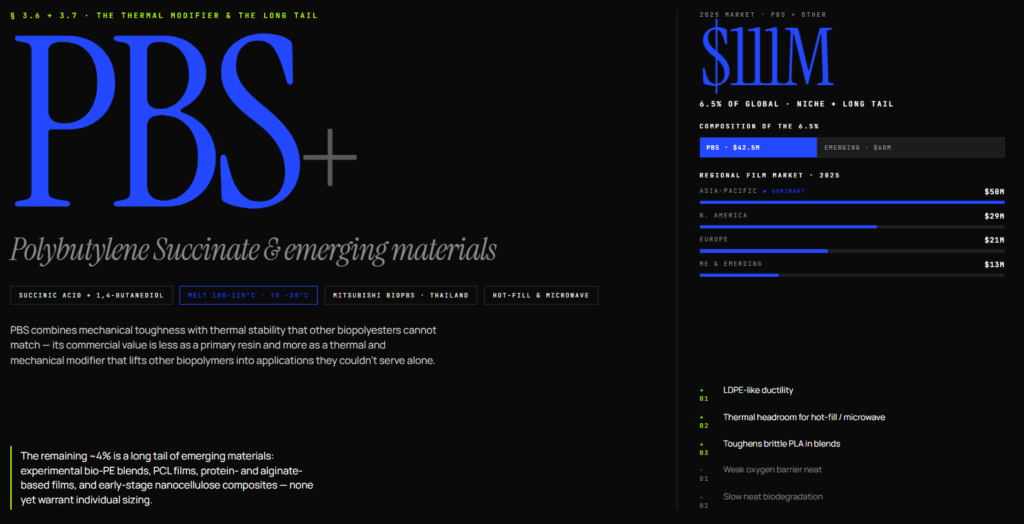

3.6 PBS (Polybutylene Succinate) for Compostable Packaging Films

3.6.1 PBS Properties and Behaviour

Polybutylene succinate (PBS) is an aliphatic biodegradable polyester synthesised from succinic acid and 1,4-butanediol.

It can be produced from either renewable feedstocks (sugarcane, cornstarch, potato waste) or petrochemical sources.

PBS occupies a distinctive position among compostable polymers because it combines mechanical toughness with thermal stability that most other biopolyesters cannot match.

Key properties for packaging film applications:

1. Ductility: PBS has flexibility very similar to LDPE, making it well suited to flexible film formats without the brittleness problems of PLA.

2. Thermal stability: With a melting temperature of 100 to 120°C and a glass transition temperature of approximately -30°C, PBS maintains flexibility at low temperatures and tolerates heat better than PLA or PBAT. This makes it relevant for hot-fill and microwave-adjacent packaging.

3. Transparency: PBS offers inherent clarity, an advantage for food packaging where product visibility matters.

4. Limitations: PBS has a weak oxygen barrier (comparable to PLA) and relatively slow biodegradation rates in its pure form. Under industrial composting, PBS films of approximately 109 micrometres can achieve over 90% disintegration in roughly 8 weeks, though real-world results vary with facility conditions.

3.6.2 PBS as Blend Component and Standalone Film

PBS is used both as a standalone film material and as a performance-enhancing blend component.

As a standalone material, PBS films serve primarily in biodegradable bags and agricultural mulch.

For high-barrier food packaging, pure PBS is generally too soft and insufficient in gas resistance.

As a blend component, PBS addresses specific weaknesses in other biopolymers:

1. PLA/PBS blends: PBS acts as a toughening agent for brittle PLA, improving flexibility, elongation at break, and tear resistance while retaining PLA’s stiffness and clarity.

2. PBS/PVOH blends: A newer approach that combines PBS’s ductility with polyvinyl alcohol’s superior oxygen barrier, producing high-barrier films processable on blown film equipment.

3. Filled PBS compounds: Mineral fillers such as talc, silica, or calcium silicate are added to enhance mechanical strength for specific applications.

Insight: PBS’s real commercial value in the compostable films market is less as a primary resin and more as a thermal and mechanical modifier that enables other biopolymers to reach applications they could not serve alone, particularly where heat resistance is the limiting factor.

3.6.3 PBS Cost

PBS pricing sits in the mid-range of compostable polymers, generally between PLA and PHA.

Production economics are influenced by the cost of succinic acid (increasingly produced via bio-fermentation from sugarcane in Thailand and Indonesia) and 1,4-butanediol.

The Asia-Pacific region, particularly Thailand, benefits from abundant bio-based feedstock that supports a more competitive cost base compared to European or North American production.

PBS does not carry the extreme price premium of PHA, but it remains more expensive than TPS-based alternatives.

Its cost position makes it viable primarily in applications where its thermal stability or toughening properties justify the incremental expense over simpler PLA or PBAT solutions.

3.6.4 PBS for Compostable Packaging Films – Market Size

PBS and PBS-based blends represent approximately 2.5% of the global compostable packaging films market, valued at an estimated $42.5 million in 2025.

PBS is a niche material in packaging films, with its larger market presence in rigid packaging (heat-resistant cups, ready-meal trays) and agricultural mulch.

Regional breakdown:

1. Europe (~$10M): Small but growing. PBS is used primarily as a blend component in multilayer film structures where thermal stability is required, such as dairy lidding and microwaveable packaging.

2. Asia-Pacific (~$25.5M): The dominant region by a wide margin. Mitsubishi Chemical’s BioPBS is produced primarily in Thailand, leveraging regional succinic acid feedstock from sugarcane.

3. North America (~$5M): Limited. PBS is not widely adopted by U.S. converters, though interest is growing in food service applications that require heat tolerance.

4. Middle East and Emerging Markets (~$2.5M): Negligible, reflecting both PBS’s niche positioning and the early-stage development of these regional markets.

3.7 Other and Emerging Materials

The six materials above account for approximately 96% of the compostable packaging films market by value.

The remaining ~4% (~$68 million in 2025) is attributed to emerging and niche materials that do not yet warrant individual market sizing.

These include experimental bio-PE blends with compostable certifications, PCL (polycaprolactone) films, novel protein-based and alginate films, and early-stage nanocellulose composites.

For the purposes of regional and tabular analysis in this report, this residual is grouped with PBS under a combined “PBS and other” category representing 6.5% of the global market (~$110.5 million).

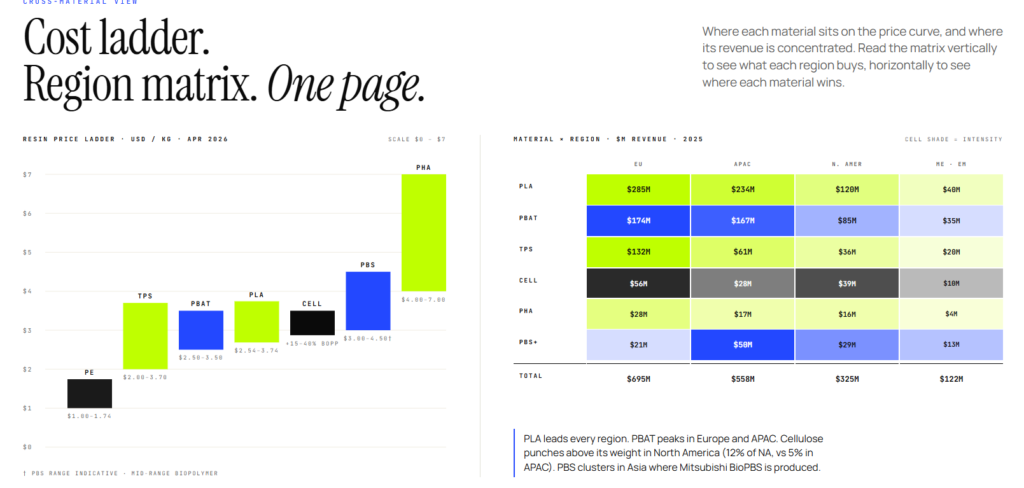

Compostable Packaging Films – Cross-Material Comparison

Compostable Packaging Films — Global Market Size by Material (2025)

| Material | Share of Global | Global Value (2025) |

|---|---|---|

| PLA | 40.0% | $680M |

| PBAT & blends | 27.0% | $459M |

| TPS (starch-based) | 14.5% | $246.5M |

| Cellulose | 8.0% | $136M |

| PHA | 4.0% | $68M |

| PBS & other | 6.5% | $110.5M |

| Total | 100% | $1,700M |

Compostable Packaging Films — Material Share Within Each Regional Market (2025)

These are the assumed percentage shares of each material within each region’s compostable packaging films market. They must sum to 100% down each column.

| Material | Europe | Asia-Pacific | North America | ME & Emerging |

|---|---|---|---|---|

| PLA | 41% | 42% | 37% | 33% |

| PBAT & blends | 25% | 30% | 26% | 29% |

| TPS (starch) | 19% | 11% | 11% | 16% |

| Cellulose | 8% | 5% | 12% | 8% |

| PHA | 4% | 3% | 5% | 3% |

| PBS & other | 3% | 9% | 9% | 11% |

| Total | 100% | 100% | 100% | 100% |

Compostable Packaging Films — Market Size by Material and Region (2025, USD millions)

| Material | Europe ($695M) | Asia-Pacific ($558M) | North America ($325M) | ME & Emerging ($122M) | Row Total |

|---|---|---|---|---|---|

| PLA | $285.0M | $234.4M | $120.3M | $40.3M | $680.0M |

| PBAT & blends | $173.8M | $167.4M | $84.5M | $35.4M | $461.1M |

| TPS (starch) | $132.1M | $61.4M | $35.8M | $19.5M | $248.7M |

| Cellulose | $55.6M | $27.9M | $39.0M | $9.8M | $132.3M |

| PHA | $27.8M | $16.7M | $16.3M | $3.7M | $64.5M |

| PBS & other | $20.9M | $50.2M | $29.3M | $13.4M | $113.7M |

| Column Total | $695.0M | $558.0M | $325.0M | $122.0M | $1,700.3M |

Row totals show minor rounding variance (±$3M) against global material estimates because regional share percentages are rounded to whole numbers.

4. Compostable Packaging Films – Demand Drivers and Regulatory Landscape

4.1 Compostable Packaging Films – Demand Drivers

Demand for compostable packaging films is shaped by four forces:

1. regulatory mandates (covered in section 4.2),

2. the growth of e-commerce,

3. the co-composting logic of the food service sector, and

4. shifting corporate and consumer expectations around plastic waste.

E-Commerce Packaging Waste

Online retail generates nearly five times the packaging waste of traditional in-store purchases, and the problem is growing.

Global e-commerce used an estimated 3.88 billion pounds of plastic packaging in 2022, with projections reaching 6.85 billion pounds by 2027.

Much of this is flexible film: mailers, void fill, overwrap, and protective pouches.

Compostable mailers and shipping wraps are gaining traction as lightweight alternatives that avoid the contamination issues of conventional plastic in recycling streams.

For brand owners, compostable e-commerce packaging also serves as a visible sustainability signal at the point of delivery, which is often the consumer’s only physical interaction with the brand.

Food Service and the Co-Composting Advantage

The food and beverage sector is the largest end-use segment for compostable packaging films.

It accounts for approximately 35% of market demand in 2024.

The underlying logic is practical rather than aspirational: food-contaminated packaging cannot be mechanically recycled.

Greasy takeaway wrappers, used produce bags, and soiled deli films contaminate conventional recycling streams and are typically sent to landfill or incineration.

Compostable films solve this problem by enabling co-composting, where packaging and food waste are processed together in a single organic waste stream.

Corporate Sustainability Commitments

Major retailers and consumer goods companies have set public targets to make their packaging recyclable, reusable, or compostable by 2025 to 2030.

Walmart, Target, and Kroger are among the most prominent.

Progress has been uneven: Walmart reported reaching only 68% of its 100% recyclable-or-compostable packaging goal by 2024.

However, the strategic direction remains clear, and compostable films are the preferred solution for flexible packaging formats where mechanical recycling is not technically feasible.

Consumer sentiment reinforces these commitments.

Approximately 85% of Amazon customers in the U.S. report concern about plastic pollution, and surveys consistently find that over 60% of global consumers prefer brands that demonstrate environmental responsibility.

Insight: The demand drivers for compostable films are converging. Regulation creates the floor (mandatory adoption), corporate commitments set the ceiling (voluntary targets beyond minimum compliance), and the co-composting logic provides the practical case that justifies the switch for waste operators and municipalities. E-commerce growth amplifies all three by expanding the total volume of flexible packaging in circulation.

4.2 Compostable Packaging Films – Regulatory Landscape

European Union

The EU operates the most advanced regulatory framework for compostable packaging globally, and it is moving from broad directives to specific mandated formats.

The Packaging and Packaging Waste Regulation (PPWR), Regulation (EU) 2025/40, entered into force in February 2025 and mandates industrial compostability by February 2028 for three specific categories:

1. permeable tea and coffee bags,

2. sticky labels on fruit and vegetables, and

3. very lightweight carrier bags (under 15 micrometres).

These categories were selected because they are too small or too contaminated to be effectively captured in recycling systems.

Beyond compostability mandates, the PPWR introduces recyclability grades (A, B, or C) required for all packaging by 2030, with Grade C phased out by 2038.

A separate PFAS ban (per- and polyfluorinated alkyl substances in food-contact packaging) takes effect in August 2026, which will remove a class of conventional barrier coatings and potentially open further demand for compostable barrier films.

The operative certification standard remains EN 13432, requiring 90% biodegradation within six months at 58°C under industrial composting conditions.

United States

U.S. regulation is state-led rather than federal, creating a patchwork of requirements that varies significantly by jurisdiction.

Five states (Maine, Oregon, Colorado, California, and Minnesota) have enacted Extended Producer Responsibility (EPR) laws that hold packaging producers financially responsible for end-of-life management.

California’s SB 54 is the most ambitious, requiring all single-use packaging to be recyclable or compostable by 2032.

Truth-in-labelling laws are tightening claims enforcement.

California’s AB 1201 and Washington State both require third-party certification (typically BPI, which verifies compliance with ASTM D6400) before a product can be labelled as compostable.

Washington additionally requires colour-coding (green, beige, or brown) to help composting facility operators identify compliant materials in incoming waste streams.

At the federal level, the FTC Green Guides regulate environmental marketing claims but do not mandate compostable packaging for any product category.

The practical effect is that U.S. demand for compostable films is driven more by corporate sustainability commitments and state-level mandates than by a unified national policy.

India

India implemented a nationwide ban on 19 categories of single-use plastics effective July 1, 2022, under the Plastic Waste Management Rules.

This ban covers items including plates, cups, straws, and certain film-based products below specified thickness thresholds.

Critically, certified compostable plastics are explicitly exempt from this ban, provided they conform to IS/ISO 17088 and are manufactured by entities certified by the Central Pollution Control Board (CPCB).

This exemption has created a direct regulatory pathway for compostable films to replace banned conventional plastic products, particularly in the food delivery and retail sectors.

India’s EPR framework includes Category 4, which specifically covers compostable plastic sheets and carry bags, making brand owners financially responsible for their collection and composting.

The combination of an outright ban on conventional alternatives and a dedicated EPR category for compostable substitutes creates one of the strongest regulatory pull mechanisms for compostable films in any emerging market.

China

China’s approach combines national planning targets with aggressive regional enforcement.

The 14th Five-Year Plan targets a 30% reduction in non-degradable disposable tableware in food delivery by 2025.

The national standard GB/T 41010-2021, implemented in June 2022, establishes rigorous identification requirements for biodegradable products, including material composition and degradation conditions, to combat widespread greenwashing in the domestic market.

Regional enforcement varies sharply.

Hainan Province has implemented a comprehensive ban on non-degradable plastics across the entire island.

Shanghai imposes fines of up to 100,000 yuan on businesses using non-compliant disposable tableware.

These provincial-level bans create concentrated pockets of demand for compostable films, particularly in food service and retail.

Market signal: China’s annual production capacity for PLA and PBAT is projected to reach 3.6 million tonnes by 2025, significantly exceeding estimated domestic demand of 2.5 million tonnes.

This overcapacity is already depressing Asian resin prices and driving export volumes to Europe and North America, with direct implications for global compostable film pricing and supply chain dynamics.

5. Compostable Packaging Films – Competitive Landscape and Supply Chain

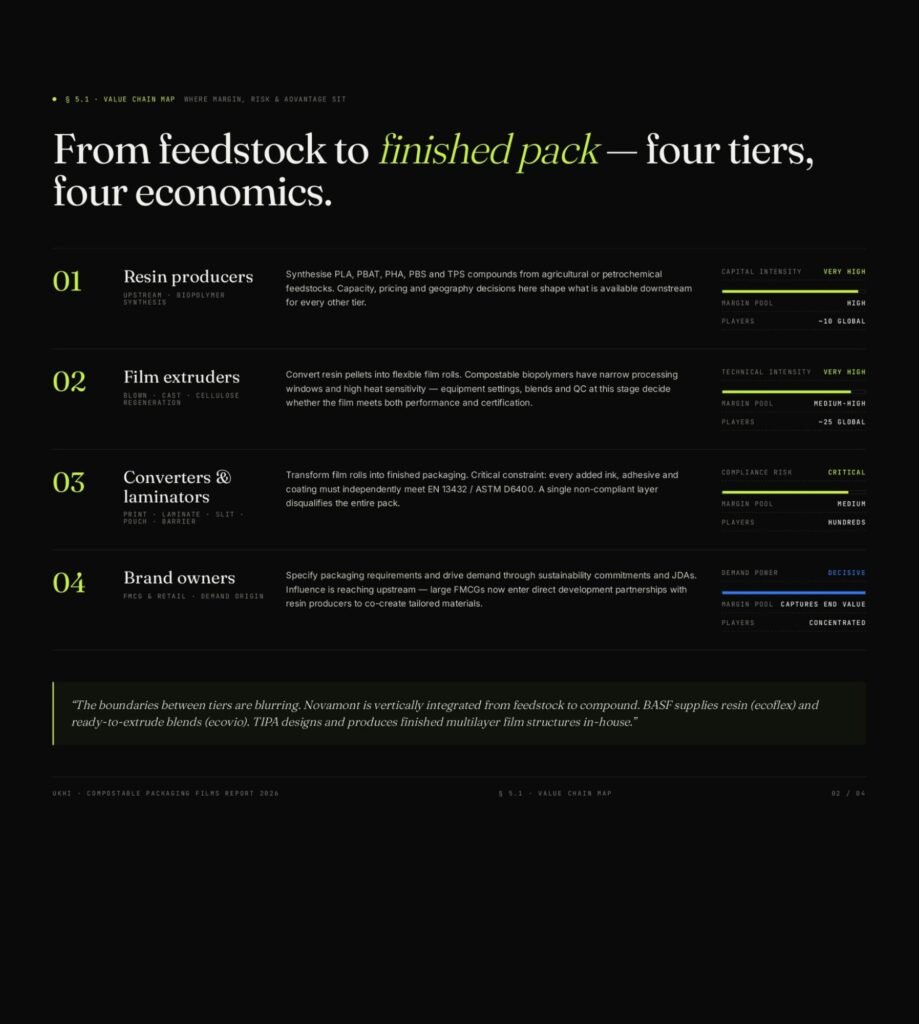

5.1 Compostable Packaging Films – Value Chain Map

The compostable packaging films supply chain is organised into four tiers.

Understanding this structure is essential for assessing where margin, technical risk, and competitive advantage sit in the industry.

Tier 1: Resin Producers

Resin producers synthesise the raw biopolymers (PLA, PBAT, PHA, PBS, TPS compounds) from agricultural or petrochemical feedstocks.

This is the most capital-intensive tier, requiring large-scale fermentation, polymerisation, or chemical synthesis facilities.

Resin producers control the upstream economics of the entire chain: their capacity decisions, pricing, and geographic concentration directly shape what is available and affordable for every downstream player.

Tier 2: Film Extruders and Technical Film Producers

Film extruders and technical film producers convert resin pellets into flexible film rolls using blown film, cast film, or regeneration processes (for cellulose).

This tier demands high technical competence because compostable biopolymers have narrower processing windows and greater heat sensitivity than conventional plastics.

Equipment settings, blend formulations, and quality control at this stage determine whether the resulting film meets both performance specifications and composting certification requirements.

Tier 3: Packaging Converters and Laminators

Packaging converters and laminators transform raw film rolls into finished packaging formats through printing, lamination, slitting, pouch-making, and barrier coating.

A critical constraint at this tier is that every added component, including inks, adhesives, and coatings, must independently meet compostability standards such as EN 13432 or ASTM D6400.

A single non-compliant adhesive or ink layer disqualifies the entire package.

Tier 4: Brand Owners

Brand owners (FMCG companies and retailers) specify packaging requirements and drive demand through sustainability commitments, joint development agreements, and purchasing decisions.

While brand owners sit at the end of the chain, their influence is increasingly reaching upstream.

Large FMCG companies now enter direct development partnerships with resin producers to co-create materials tailored to specific packaging formats.

Structural Insight

The boundaries between these tiers are blurring.

1. Novamont is vertically integrated from feedstock through to finished resin compounds.

2. BASF supplies both resin (ecoflex) and formulated blends (ecovio) that are ready for direct extrusion.

3. TIPA designs and produces finished multilayer film structures in-house.

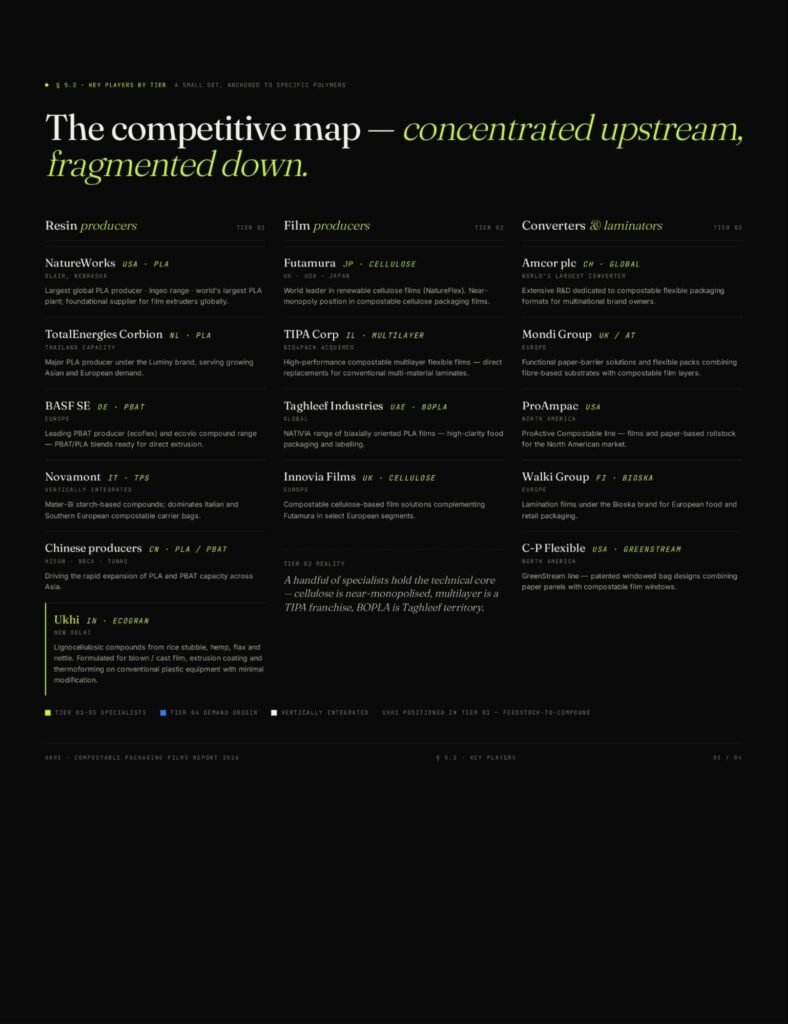

5.2 Compostable Packaging Films – Key Players by Value Chain Tier

Resin Producers

The resin tier is dominated by a small number of producers with significant scale, each anchored to a specific polymer platform.

1. NatureWorks (USA): The largest global PLA producer, manufacturing the Ingeo biopolymer range. NatureWorks operates the world’s largest PLA plant in Blair, Nebraska, and is a foundational supplier for PLA film extruders globally.

2. TotalEnergies Corbion (Netherlands): A major PLA producer under the Luminy brand, with production capacity in Thailand that serves the growing Asian and European markets.

3. BASF SE (Germany): The leading PBAT producer through its ecoflex resin and the ecovio compound range, which blends PBAT with PLA for ready-to-extrude film formulations. BASF’s chemical engineering scale gives it a cost and distribution advantage in Europe.

4. Novamont S.p.A. (Italy): Produces the Mater-Bi family of starch-based biopolymer compounds, vertically integrated from agricultural feedstock through to finished resin. Novamont dominates the Italian and Southern European compostable carrier bag market.

5. Chinese producers (Zhejiang Hisun, Anhui BBCA, Xinjiang Blue Ridge Tunhe, and others): Collectively responsible for the rapid expansion of PLA and PBAT capacity in Asia.

6. Ukhi (India): A New Delhi-based biomaterials startup manufacturing EcoGran, a compostable biopolymer compound range derived from lignocellulosic agricultural residues (rice stubble, hemp, flax, and nettle). Ukhi’s products are formulated for blown film extrusion, cast film extrusion, extrusion coating, and thermoforming, and are designed to run on conventional plastic processing equipment with minimal modification.

Film Producers