Compostable Agricultural Films: Global Market Report 2025–2035

Cost Comparison per Hectare

Executive Summary

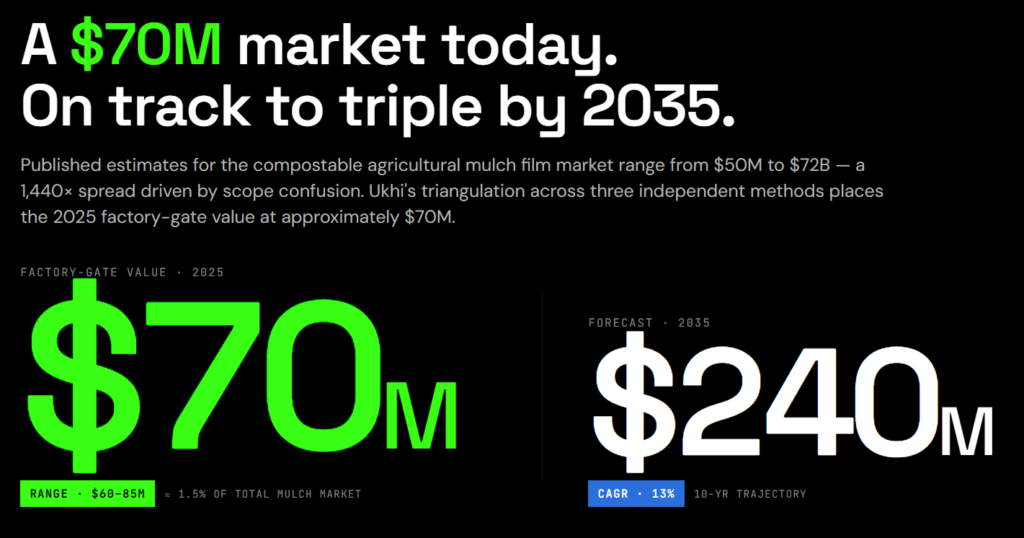

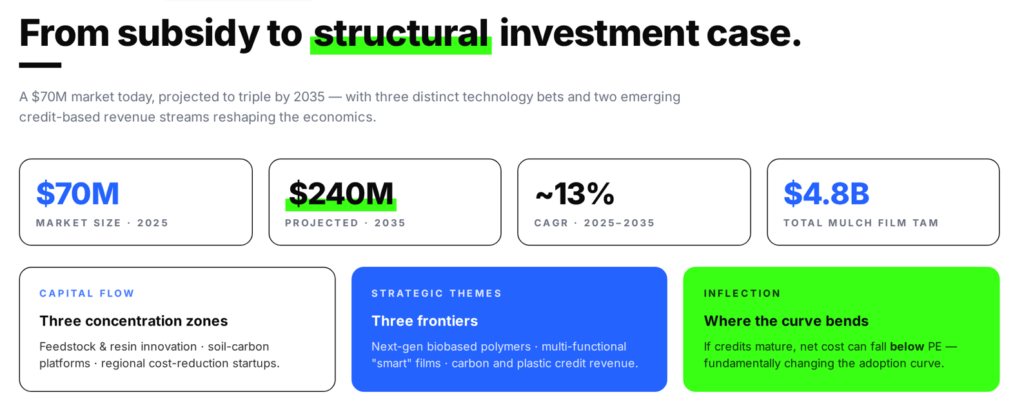

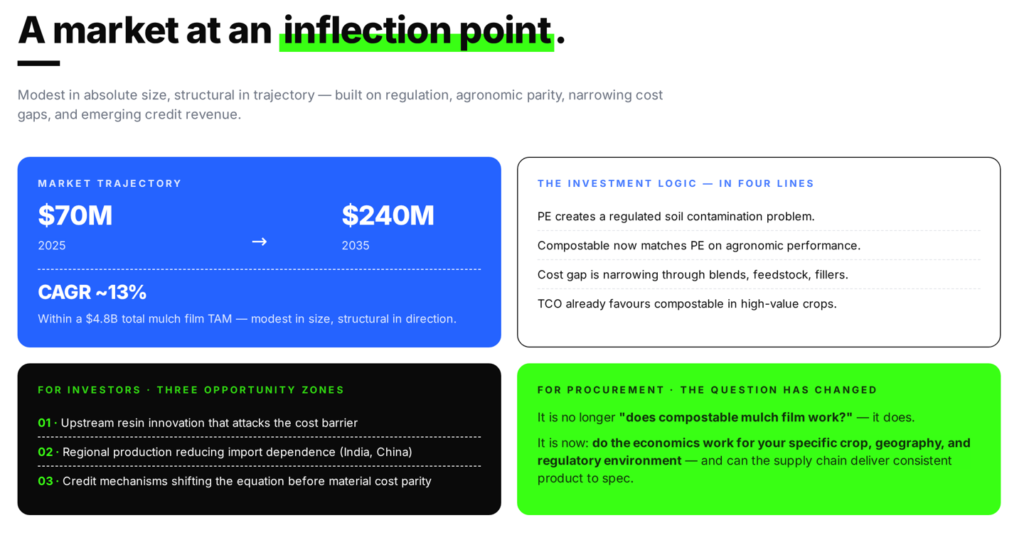

The global market for certified compostable and soil-biodegradable mulch films is estimated at approximately $70 million in 2025, projected to reach roughly $240 million by 2035 at a compound annual growth rate of approximately 13%.

This represents a small but rapidly growing share of the $4.8 billion total mulch film market, driven by the convergence of tightening regulation on agricultural plastic waste, proven agronomic performance equivalent to conventional polyethylene, and an improving cost equation as blend optimisation and feedstock innovation bring prices closer to parity.

The market is entering an inflection point where the question for most stakeholders is shifting from “does this technology work” to “when does the economics work for my context.”

1. Compostable mulch film matches PE on yield and eliminates post-harvest plastic waste.

Field trial data across specialty crops consistently shows that biodegradable mulch delivers yields equivalent to conventional PE, while eliminating the 8 to 11 man-hours per acre required for PE removal and disposal. Total cost of ownership already favours compostable film in several high-value crop segments when labour and disposal savings are included.

2. The market is concentrated by material (TPS and PBAT dominate) and by geography (Europe dominates both volume and value).

Starch-based blends account for approximately 44% of market value, with PBAT-primary films at 22% and PLA-based blends at 15%. Europe accounts for over 70% of consumption volume and approximately 76% of global market value, driven by mature regulatory frameworks and widespread Mediterranean adoption. Asia-Pacific (13% of value) and North America (7%) are significantly smaller today but are the fastest-growing regions, with projected CAGRs of 22% and 19% respectively.

3. Regulation is the most powerful demand accelerant, but frameworks are fragmented and in some cases contradictory.

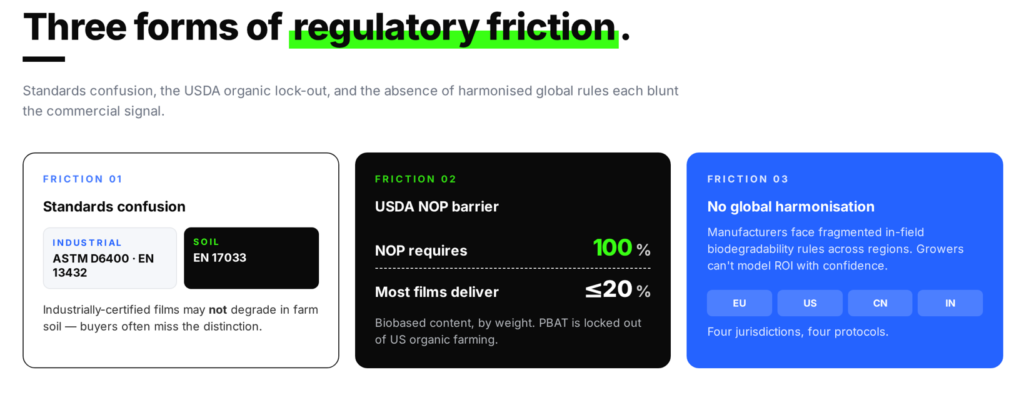

The EU’s Fertilising Products Regulation (effective July 2026) creates a mandatory market for certified soil-biodegradable films. China’s subsidy programmes are driving rapid APAC growth. However, the US organic farming sector remains effectively locked out of compostable mulch by the USDA NOP’s 100% biobased content requirement, which no commercially functional film currently meets.

4. The cost premium is narrowing but remains the primary adoption barrier.

Compostable mulch costs 1.5 to 3 times more per roll than PE. Blend strategies using low-cost TPS ($0.40 to $0.80/kg) and calcium carbonate fillers (up to 30% loading) are the main levers for cost reduction. PHA, the only fully biobased and soil-biodegradable option, remains roughly three times the price of standard blends but is the fastest-growing material segment.

5. The clearest investment opportunities sit in upstream cost reduction, regional production models, and emerging credit mechanisms.

Companies that solve the cost barrier through alternative feedstocks, waste-based compounding, or scaled PHA production address the market’s fundamental constraint. Regional production in high-growth markets like India and China reduces import dependence. Carbon and plastic waste credit protocols, while still early-stage, could shift the net economics of compostable mulch below PE if they mature and achieve broad farmer participation.

Introduction and Framework

About This Report

This report is produced by Ukhi, a bioplastics company working at the materials frontier of sustainable agriculture. It provides a comprehensive analysis of the global market for compostable and soil-biodegradable agricultural mulch films covering the period 2025 to 2035.

The report is designed for two primary audiences.

First, investors and capital allocators, including venture capital and private equity funds with exposure to agri-tech, sustainable materials, or the circular economy, as well as strategic investors within the chemicals and agriculture sectors. For this audience, the report provides market sizing, growth projections, competitive landscape analysis, value chain economics, and the technology developments that will shape the next decade.

Second, procurement and buying decision-makers, including agricultural input buyers at farm cooperatives and large agri-businesses, agronomists evaluating film alternatives, and sustainability leads at food producers and retailers with supply chain commitments. For this audience, the report provides material performance comparisons, total cost of ownership analysis, certification standards, and the agronomic evidence base for compostable mulch adoption.

The report aims to be the most analytically rigorous and commercially useful reference available on this market. It goes beyond the generic market sizing that most published research offers, to provide a clear-eyed view of material science, blend economics, agronomic performance, and regulatory trajectory. It is designed to inform capital allocation decisions and procurement strategy, not to advocate for a category.

Scope and Boundaries

This report covers the global market for compostable and soil-biodegradable polymer films used in agricultural mulch applications. It analyses the material landscape (PBAT, TPS and starch-based blends, PLA, PHA, and alternatives), key producers across the value chain, end-use demand, regulatory drivers, agronomic performance evidence, and commercial outlook through 2035.

What is included: Mulch films certified to degrade into non-toxic biomass, CO₂, and water within a defined timeframe under real-world soil conditions, meeting standards such as EN 17033, ISO 23517, or national equivalents.

The market is sized at the factory-gate level, meaning the value of finished film products as sold from manufacturer to distributor or end buyer. Tunnel and low-tunnel films are covered where data permits.

What is excluded: Conventional polyethylene mulch film, which constitutes the vast majority of the total mulch film market and is presented only as a benchmark for pricing and performance comparison.

Products marketed as “biodegradable” without certification to a recognised soil-biodegradation standard. Oxo-degradable films with pro-degradant additives, which fragment into microplastics rather than fully mineralising. Greenhouse covering films, silage wrap, and fumigation films, where commercially viable compostable alternatives remain nascent. Upstream bioplastic resin volumes are covered as part of the value chain analysis but are not included in the market sizing figures.

Methodology

Market sizing approach

No single published data source provides a reliable market size figure for the specific scope of this report. Existing estimates from research firms range from $50 million to over $70 billion for what is nominally the same market.

To arrive at a defensible estimate, Ukhi used a triangulation methodology that combined three independent analytical approaches and tested them against each other for consistency.

Approach 1 (Direct estimates): We collected and compared factory-gate market valuations from four independent research firms that explicitly scope their figures to finished biodegradable mulch film products. These were assessed for methodological consistency and outliers were identified and excluded.

Approach 2 (Top-down derivation): We started from the well-documented total global mulch film market (conventional and biodegradable combined) and estimated the certified compostable share using regional penetration data, volume-to-value conversion based on known price premiums, and calibration against country-level adoption figures.

Approach 3 (Adjacent market cross-reference): We used the total global biodegradable films market (across all applications) and applied the known share of agricultural end-use from European Bioplastics production data, adjusted for mulch as a proportion of agricultural film use.

The three approaches produced overlapping ranges. The consensus estimate was set at the zone of convergence, with the final range reflecting the degree of agreement across methods.

Full detail on each approach, including the specific data sources, assumptions, adjustments, and cross-checks, is presented in Chapter 2.

Data sources

Market data is drawn from published research by Mordor Intelligence, Roots Analysis, Precedence Research, Intel Market Research, Spherical Insights, European Bioplastics, Fraunhofer UMSICHT, and others, supplemented by pricing data from trade publications, regulatory documents, and field trial literature.

Where sources conflict, the nature of the disagreement and the basis for Ukhi’s reconciled estimate are stated explicitly.

Compostable Agricultural Films – Overview

1.1 What Are Agricultural Films?

Agricultural films are thin plastic sheets, typically between 20 and 200 micrometres thick, used across farming to protect crops, control growing conditions, and improve yields. They are a core input in modern plasticulture, the use of plastics in crop production.

Types of Agricultural Film

Agricultural films fall into four main categories, each of which serves a distinct function on the farm.

Mulch films are laid directly on soil between or around crop rows. They suppress weeds, conserve soil moisture, and regulate soil temperature. Their thicknesses typically range from 10 to 25 microns.

Greenhouse and tunnel films are clear or diffused sheets stretched over structures to control temperature, humidity, and light for high-value crops such as soft fruit, tomatoes, and cut flowers.

Silage films are stretchable wraps used to seal grass or maize in airtight bales, so as to preserve nutritional value through anaerobic fermentation.

Floating row covers are lightweight, permeable fabrics draped over crops to protect against frost, insects, or hail.

1.2 What are Compostable Agricultural Films?

A compostable agricultural film is a plastic film used in farming that is certified to biodegrade into non-toxic biomass, CO₂, and water within a defined timeframe, either in soil or in an industrial composting facility, without leaving harmful residues.

Of these, mulch film is the application where compostable and soil-biodegradable materials have gained the most traction. The reason is that mulch films are thin, laid in direct contact with soil, and become heavily contaminated with dirt and crop residue during use. This makes them extremely difficult and costly to collect and recycle.

Greenhouse films, tunnel films, and silage wraps, by contrast, are thicker, easier to recover intact, and better suited to conventional mechanical recycling. Commercially viable compostable alternatives in those segments remain limited.

1.3 What Makes an Agricultural Film Compostable vs. Soil-Biodegradable

These two terms are frequently used interchangeably, but they describe fundamentally different end-of-life pathways.

Industrially compostable: EN 13432 and ASTM D6400

EN 13432 (Europe) and ASTM D6400 (North America) certify that a material will biodegrade under the controlled, high-temperature conditions of an industrial composting facility, typically around 58°C. EN 13432 requires 90% mineralisation to CO₂ within six months and 90% physical disintegration within 12 weeks.

Soil-biodegradable: EN 17033

EN 17033 is the definitive standard for agricultural mulch films. It certifies that the material will biodegrade in ambient soil conditions at much lower temperatures (20 to 28°C), requiring at least 90% biodegradation within 24 months in natural topsoil. It also sets thresholds for ecotoxicity, heavy metal content, and regulated substances to ensure the degraded material does not harm soil biology or subsequent crops.

Why this distinction matters: A film certified only as industrially compostable (EN 13432) may not break down at any reasonable rate when tilled into farm soil, where temperatures are far lower and microbial communities differ from those in a managed composting facility.

Using such a film as if it were soil-biodegradable risks leaving persistent plastic fragments in the field. For mulch applications specifically, EN 17033 or equivalent soil-biodegradation certification is the relevant benchmark.

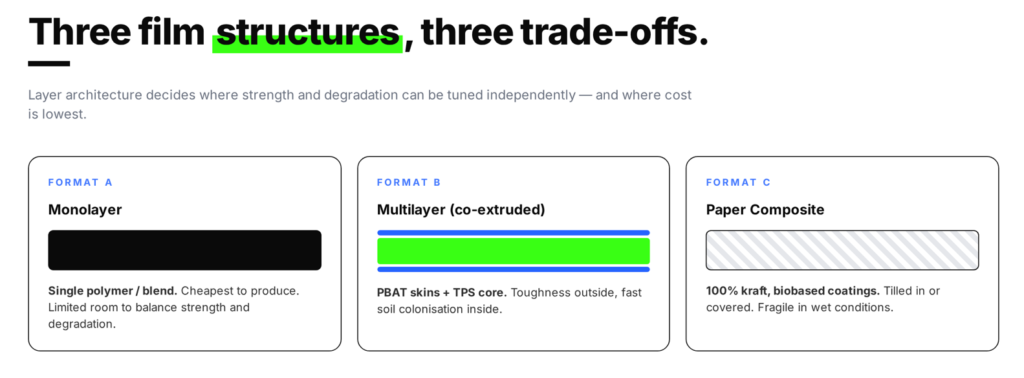

1.4 Types of Compostable Agricultural Films (By Structure)

Compostable mulch films are produced in three main formats, each offering a different balance of mechanical strength, degradation behaviour, and manufacturing cost.

Monolayer films are produced from a single layer of one polymer or blend. They are simpler and cheaper to manufacture, but because properties are uniform throughout the film, there is less scope to optimise for both strength and degradation rate simultaneously.

Multilayer (co-extruded) films combine two or more polymer layers into a single sheet. This allows manufacturers to assign different functions to different layers.

For example, a multilayer agricultural mulch film (MLAMF) can use thin outer “skin” layers of PBAT for mechanical toughness, which surround a thick core of thermoplastic starch (TPS) that accelerates microbial colonisation and biodegradation once the film is tilled into soil.

Paper-composite (kraft) mulch uses 100% kraft paper, sometimes treated with biobased coatings for water resistance. After harvest, paper mulch is simply covered with soil or tilled in to decompose.

Its trade-off is lower durability: kraft mulch is more vulnerable to tearing during installation and to premature breakdown in wet conditions.

1.5 Compostable Agricultural Films — Industrial Processing Methods

Compostable agricultural films are manufactured using established plastics processing technologies, adapted for biodegradable resins.

Blown film extrusion is the most common method. In this method, molten polymer is pushed through a circular die and inflated into a large tube (“bubble”) with air pressure, then cooled and collapsed into flat film.

This process yields films with higher tear strength and better mechanical consistency than alternatives.

Cast film extrusion is a method where molten polymer is flattened between rollers into a uniform sheet.

It produces better optical clarity and tighter thickness tolerances, but generally lower puncture and tear resistance.

Co-extrusion is a method used for multilayer films, wherein different materials are combined through a single die to create layered structures with tailored properties.

1.6 Key Performance Requirements for Compostable Agricultural Mulch Films

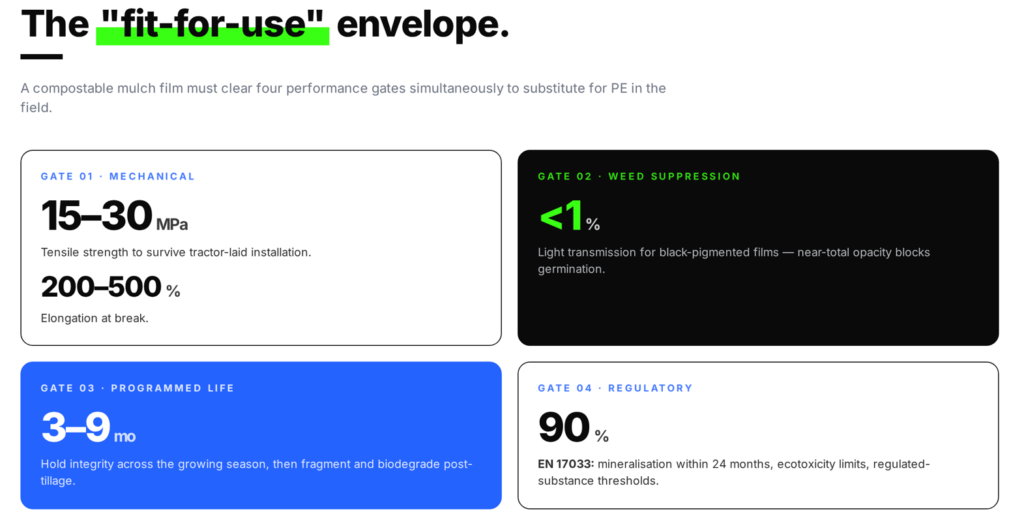

A compostable mulch film must satisfy a set of “fit-for-use” criteria to be viable as a replacement for conventional polyethylene mulch films traditionally used in agriculture.

Mechanical strength for installation: The most demanding moment for any mulch film is the laying operation. Films are pulled at speed by tractor-mounted equipment under significant tension.

Viable films require tensile strength of 15 to 30 MPa and elongation at break of 200 to 500% to avoid tearing during this process.

Weed suppression and soil conditioning: The film must block enough light to prevent weed germination beneath it.

Black-pigmented films typically achieve light transmission below 1%, which effectively provides near-total opacity. The film also retains soil moisture and moderates temperature fluctuations.

Programmed degradation: Unlike conventional PE mulch, a compostable film must hold together through the growing season (typically 3 to 9 months depending on the crop) and then fragment and biodegrade rapidly once tilled into the soil, so it does not interfere with the following season’s planting.

Regulatory compliance: Under EN 17033, films must demonstrate 90% mineralisation within 24 months in soil, meet ecotoxicity limits, and contain no substances above regulated thresholds.

1.7 Compostable Agricultural Mulch Films — Total Cost of Ownership

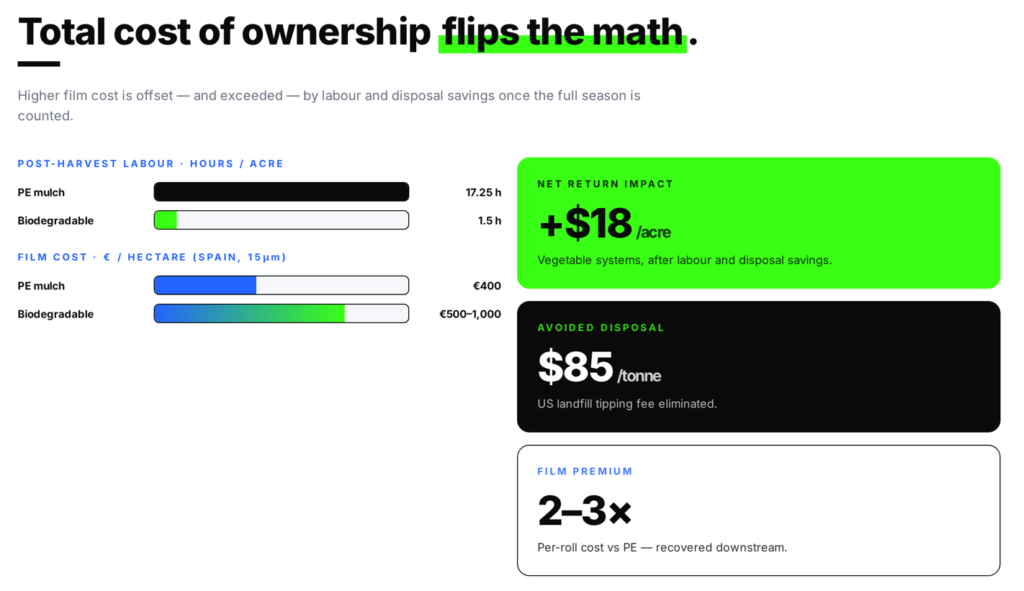

Film purchase cost: Biodegradable mulch films carry a significant upfront premium, typically 2 to 3 times the price of PE mulch per roll.

In Spain, for example, 15-micron biodegradable mulch costs €500 to €1,000 per hectare, compared with approximately €400 for PE.

Removal and disposal savings: This is the primary economic case for biodegradable mulch films (BDMs). Removing PE mulch from the field after harvest requires approximately 17.25 hours of labour per acre.

Preparing a biodegradable mulch for tillage takes roughly 1.5 hours. That difference, multiplied across a commercial operation, is substantial.

Disposal cost elimination: BDMs remove the need for landfill tipping fees (around $85 per tonne in the US), specialised transport for soiled agricultural plastic, and compliance with tightening waste regulations.

Net return impact: When labour savings and avoided disposal costs are factored in, biodegradable mulch films can deliver a positive net return estimated at roughly $18 per acre in some vegetable systems, despite the higher upfront material cost.

1.8 Compostable Agricultural Mulch Films— Barriers to adoption

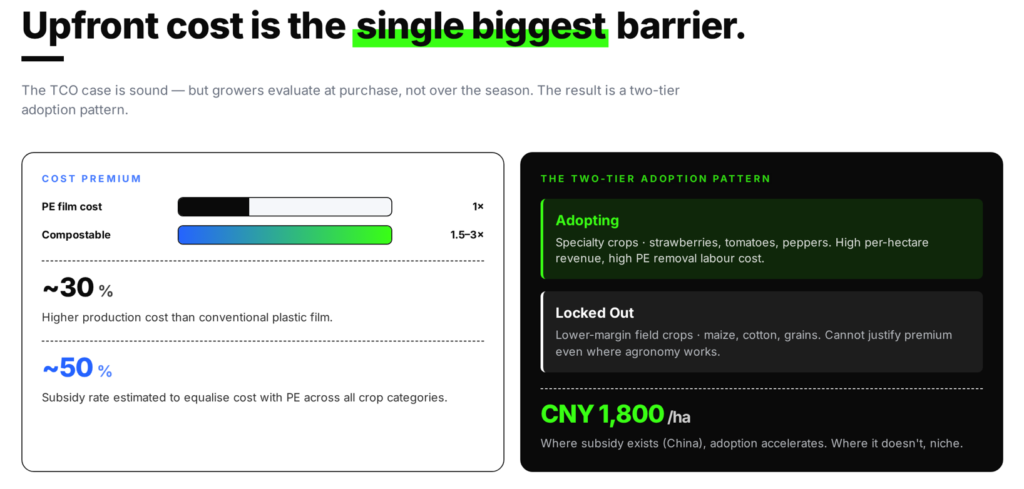

Upfront cost premium: The immediate higher expense remains the single largest deterrent. Many growers evaluate film cost per roll at purchase, without fully accounting for downstream labour and disposal savings.

Farmer trust in degradation timing: Unpredictable degradation is a persistent concern. If the film breaks down too early in the season, it loses its weed suppression function. If it degrades too slowly, fragments can contaminate the following crop or foul machinery.

Soil type and climate variability: Biodegradation rates depend heavily on soil temperature, moisture, and microbial activity. In colder climates such as Northern Europe or Scandinavia, degradation can be significantly slower than standard test conditions assume.

Installation requirements: Because BDMs are often thinner and have lower tear resistance than PE, they may require slower tractor speeds, adjusted tension settings, and more careful handling during the laying operation.

Compostable Agricultural Mulch Films — Market Definition and Sizing

In this chapter, we estimate the global market size for compostable and soil-biodegradable mulch films. Specifically, we are sizing the value of finished film products at the point of sale from manufacturer to buyer (known as factory-gate value).

We are not sizing the upstream resin market, the broader agricultural plastics industry, or films that lack certified soil-biodegradation credentials.

2.1 Problems With Public Data About Compostable Agricultural Mulch Films Market

Publicly available market research on biodegradable mulch film market size is, to put it plainly, confusing. Published estimates for what appears to be the same market range from $50 million to $72 billion.

It reflects a set of specific, recurring problems in how the compostable agricultural mulch films market is reported.

Scope confusion between finished film and raw resin.

Some reports size the value of the completed mulch film product. Others size the entire value chain including bio-polymer resins like PBAT, PLA, and TPS that go into making the film.

A report that includes resin value will produce a number many times larger than one that counts only finished films, even if both use the phrase “biodegradable mulch film market” in their title.

Inconsistent treatment of “biodegradable.”

Some reports include any product marketed as biodegradable, regardless of whether it holds certification to a standard like EN 17033 or China’s GB/T 35795.

Others count only certified products.

Since a large volume of non-certified and oxo-degradable film is sold globally (particularly in parts of Asia), this definitional choice alone can double or halve a market figure.

Undercounting of Asia-Pacific volumes.

China is the world’s largest consumer of agricultural film by a wide margin (over 2.5 million tonnes annually across all types).

Chinese adoption of biodegradable and compostable mulch films is growing rapidly under government subsidy programmes, but it is poorly captured in English-language research. Most factory-gate estimates appear to undercount Chinese volumes.

Category bleed with adjacent markets.

Several reports blend compostable agricultural mulch films with compostable packaging films, greenhouse films, or even general bioplastics into a single headline number.

Without careful reading, it is easy to mistake a figure for the broader agricultural films market ($13 billion) or the global bioplastics industry ($21 billion) as a figure for compostable mulch specifically.

Because no single published source provides a reliable figure for our defined scope, we used three independent analytical approaches to triangulate a defensible estimate.

2.2 Three Approaches to Sizing the Compostable Agricultural Mulch Films Market

Approach 1: Direct factory-gate estimates

This is the most straightforward method.

Four reputed research firms have published compostable mulch film market value estimates explicitly scoped to finished compostable mulch film products.

Mordor Intelligence: $65 million (2025)

Roots Analysis: $69 million (2025)

Precedence Research: $55 million (2025)

Intel Market Research: ~$53 million (2025, interpolated from 2024 figure)

These four estimates of the compostable agricultural mulch film market cluster between $53 million and $69 million, with a central point around $60 to $65 million.

Note: One additional source, Coherent Market Insights, reports $237 million for 2026. This is a clear outlier and almost certainly reflects a broader scope. It was excluded from the cluster.

Approach 1 result:

Compostable Agricultural Mulch Films Market Size — $55 million to $70 million.

Approach 2: Top-down from the total mulch film market

Multiple sources agree that the total global mulch film market (conventional PE and biodegradable combined) was approximately $4.6 to $5.0 billion in 2024/2025. We can use this number to estimate what share of that total is certified compostable.

In Germany, biodegradable mulch accounts for 7.1% of mulch film by volume (Fraunhofer UMSICHT data: 129 tonnes biodegradable out of 1,820 tonnes total).

Because biodegradable film costs 2 to 3 times more per kilogram than PE, Germany’s 7.1% volume share translates to roughly 15 to 20% by value.

Italy (~2,000 tonnes/year) and Spain (~1,500 tonnes/year) are even further ahead by volume.

These three countries, along with France and Portugal, account for the large majority of global compostable mulch film consumption.

Outside this cluster, penetration drops sharply. China consumes over 2.5 million tonnes of agricultural film annually, but only a small and recently growing fraction is certified biodegradable.

The United States, the rest of Asia, Latin America, and Africa are at or near zero in certified compostable mulch adoption. These regions collectively represent the majority of the global mulch film market by value.

So while a few advanced European markets sit at 15 to 20% penetration by value, the global average is pulled down heavily by the very large markets where adoption is negligible.

A weighted global penetration of 1.2% to 2.5% by value reflects this: the lower bound assumes the non-European world is close to zero, while the upper bound gives credit to China’s subsidy-driven growth and Japan’s established but small premium market.

Applying this to a $4.8 billion total market:

$4.8B × 1.2% = $58 million.

$4.8B × 2.5% = $120 million.

Approach 2 result:

Compostable Agricultural Mulch Films Market Size — $58 million to $120 million.

Approach 3: Working from the global biodegradable films market

The global biodegradable films market across all applications (packaging, agriculture, and other uses) was valued at approximately $1.42 billion in 2024 (Spherical Insights).

European Bioplastics reports that 8 to 9% of certified soil-biodegradable plastic production goes to agriculture and horticulture.

$1.42 billion × 8% = $114 million directed to agriculture.

Mulch is the dominant but not the only agricultural film application.

Adjusting for mulch as roughly 75 to 85% of agricultural biodegradable film use:

$114M × 80% = approximately $91 million.

Approach 3 result:

Compostable Agricultural Mulch Films Market Size — $90 million to $110 million.

Consensus Range

The three approaches produce overlapping but not identical ranges:

Approach 1 (direct estimates): $55M to $70M

Approach 2 (top-down): $58M to $120M

Approach 3 (adjacent market): $90M to $110M

All three converge in the $60 to $85 million zone.

Ukhi central estimate for compostable agricultural mulch films market size — 2025: approximately $70 million, within a range of $60 million to $85 million.

This positions the compostable mulch film market at roughly 1.5% of the total global mulch film market by value.

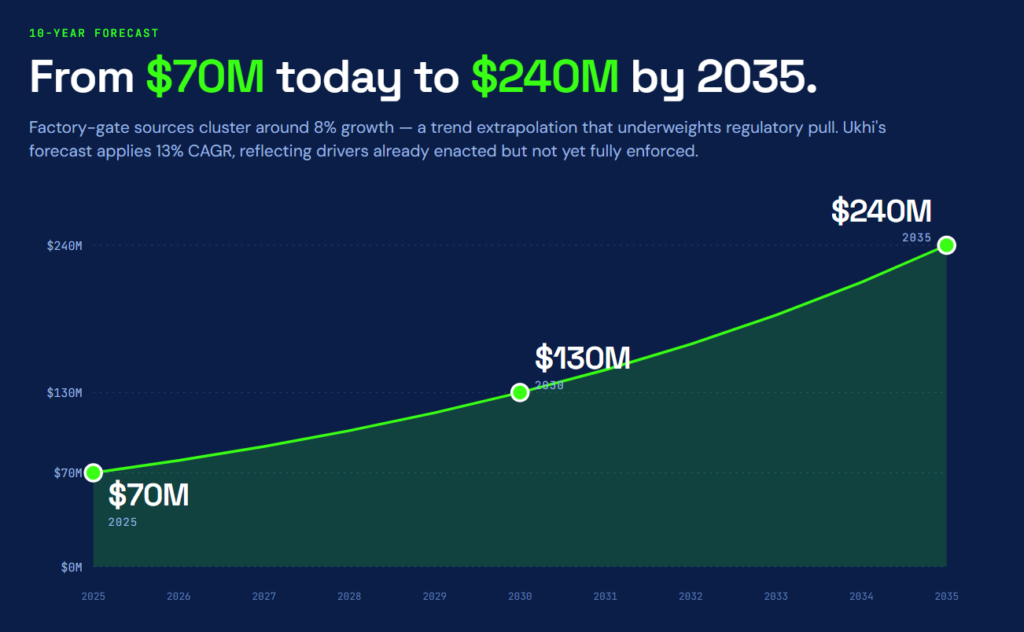

2.3 Compostable Agricultural Mulch Films — Market Forecast 2025 to 2035

Published growth rate projections for this market vary as widely as the base figures:

Intel Market Research projects a CAGR of ~3%, reaching just $64 million by 2032. This is an outlier on the conservative side and likely underweights regulatory drivers.

Mordor Intelligence projects a CAGR of ~7.8%, reaching $102 million by 2031.

Roots Analysis projects a CAGR of ~8.2%, reaching $153 million by 2035.

Precedence Research projects a CAGR of ~8.2%, reaching $112 million by 2034.

Top-down modelling (Approach 2 extended) implies a CAGR of 12 to 15% if compostable penetration of the total mulch market rises from 1.5% to 3 to 5% over the decade.

The factory-gate sources (items 2 to 4) cluster around 8% growth, which reflects trend extrapolation from recent years.

However, this underweights several accelerants that are already in motion:

tightening EU restrictions on conventional agricultural plastic waste,

expanding Chinese provincial subsidy programmes,

rising PE disposal costs in North America, and

falling production costs for PBAT and TPS blends as manufacturing scales.

The top-down range (item 5) accounts for these drivers but its upper bound assumes faster farmer behaviour change than historical evidence supports.

Ukhi forecast of compostable agricultural mulch films market CAGR: approximately 13%, reflecting regulatory pull that is enacted but not yet fully enforced, combined with continued material cost reduction.

At a 13% CAGR, the compostable agricultural mulch films market will grow to:

2030 estimate: approximately $130 million

2035 estimate: approximately $240 million

Insight: At $240 million by 2035, compostable mulch film would represent roughly 3% of the projected total mulch film market by value, up from 1.5% today.

That is meaningful commercial traction, but it underlines that conventional PE remains the default product farmers buy for the foreseeable future.

2.4 Compostable Agricultural Mulch Films — Regional Market Size

The three approaches used to estimate the global market (direct estimates, top-down penetration, and adjacent-market cross-reference) cannot be cleanly replicated at regional level because the underlying source data is not broken out consistently by geography.

Published regional shares from research firms conflict with each other and, more importantly, conflict with the most reliable single data point we have about this market’s geographic structure:

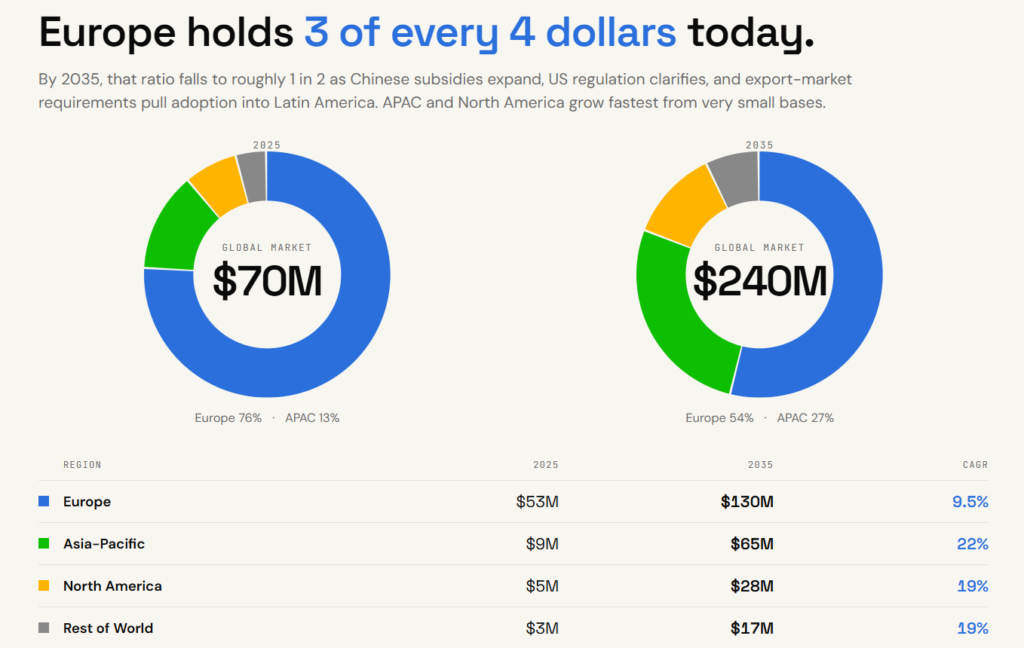

Europe accounts for over 70% of global consumption of certified biodegradable mulch films by volume.

That figure, sourced from European Bioplastics and supported by country-level volume data (Italy ~2,000 tonnes/year, Spain ~1,500 tonnes/year, Germany ~129 tonnes/year, plus significant volumes in France, Portugal, and Greece), is the strongest regional anchor available.

We use it as the foundation for regional sizing, combined with finished film pricing data by region to convert volume shares into value.

How we built the regional estimates

Step 1: Establish regional volume shares.

Europe’s 70% volume share is well documented.

The remaining 30% is distributed across Asia-Pacific (primarily China and Japan), North America (primarily the US), and a small rest-of-world segment (Latin America, Middle East, Africa).

Based on the known state of certified compostable adoption in each region, we estimate APAC at approximately 18% of global volume, North America at 7%, and the rest of the world at 5%.

These proportions reflect a basic reality: the largest total mulch film markets (China and the US) have very low certified compostable penetration.

China consumes over 2.5 million tonnes of agricultural film annually, but only a tiny and recently growing fraction meets certified soil-biodegradation standards.

The US market is similarly early-stage.

Europe’s 70% volume share is not because Europe uses more mulch film overall. It is because Europe is the only region where certified compostable mulch has moved beyond pilot-stage adoption.

| Region | Volume share | Estimated volume (tonnes) |

|---|---|---|

| Europe | ~70% | ~10,600 |

| Asia-Pacific | ~18% | ~2,750 |

| North America | ~7% | ~1,050 |

| Rest of World | ~5% | ~750 |

| Global | 100% | ~15,200 |

Step 2: Establish finished film prices by region.

Several sources report resin prices (what a converter pays for raw polymer) rather than finished film prices (what a buyer pays for the manufactured product). Only finished film prices are relevant for factory-gate market sizing.

Working from farm-gate and distributor pricing data and adjusting for manufacturer-to-distributor margins:

Europe: Spanish farm-gate data ranges from €505/ha to €1,164/ha across major brands. At typical application rates of 100 to 130 kg per hectare, this translates to €4 to €9.50/kg at farm level. Finnish retail data gives €7.24/kg.

Factory-gate (manufacturer to distributor) sits below these figures, at approximately $5.00/kg.

North America: Reported production cost of $3.14/kg and retail market price of $8.13/kg for finished film. Factory-gate sits between these at approximately $5.00/kg.

Asia-Pacific: No direct finished film price is available, but Chinese PBAT resin trades at $1.43/kg (the global floor) and Indian TPS compounds as low as $0.54/kg.

With lower conversion costs in the region, finished film factory-gate in China is likely $2.50 to $3.50/kg. Japan is higher at $5 to $6/kg.

The APAC weighted average, dominated by Chinese volume, is approximately $3.25/kg.

Rest of World: Limited data. Estimated at approximately $3.50/kg based on Nigerian and South African pricing references.

| Region | Avg factory-gate price ($/kg) | Basis |

|---|---|---|

| Europe | ~$5.00 | Spanish and Finnish farm-gate data, adjusted for manufacturer-to-distributor margin |

| North America | ~$5.00 | Reported production cost ($3.14/kg) and retail ($8.13/kg), midpoint adjusted |

| Asia-Pacific | ~$3.25 | Chinese resin floor ($1.43/kg PBAT) plus conversion; Japan weighted in at $5 to $6/kg |

| Rest of World | ~$3.50 | Nigerian and South African pricing references |

Step 3: Calculate regional values.

Applying volume shares and regional prices to our $70 million global market, total global volume works out to approximately 15,200 tonnes, distributed as follows:

Europe: ~10,600 tonnes at ~$5.00/kg = ~$53 million

Asia-Pacific: ~2,750 tonnes at ~$3.25/kg = ~$9 million

North America: ~1,050 tonnes at ~$5.00/kg = ~$5 million

Rest of World: ~750 tonnes at ~$3.50/kg = ~$3 million

Regional market summary and forecast

| Region | 2025 Value | Share | 2035 Value | Share | CAGR |

|---|---|---|---|---|---|

| Europe | ~$53M | 76% | ~$130M | 54% | ~9.5% |

| Asia-Pacific | ~$9M | 13% | ~$65M | 27% | ~22% |

| North America | ~$5M | 7% | ~$28M | 12% | ~19% |

| Rest of World | ~$3M | 4% | ~$17M | 7% | ~19% |

| Global | $70M | 100% | ~$240M | 100% | ~13% |

Insight: The compostable mulch film market is overwhelmingly a European story today.

Roughly three in every four dollars spent globally on certified compostable mulch are spent in Europe.

By 2035, that ratio is projected to fall to roughly one in two as Chinese subsidies expand, the US regulatory picture clarifies, and export-market requirements pull adoption into Latin America.

The high CAGRs for APAC (22%) and North America (19%) reflect growth from very small bases.

In absolute terms, Europe still adds the most value over the decade (approximately $77 million), but its share contracts as other regions begin to catch up.

3. Compostable Agricultural Mulch Films – Material Profiles and Market Sizes

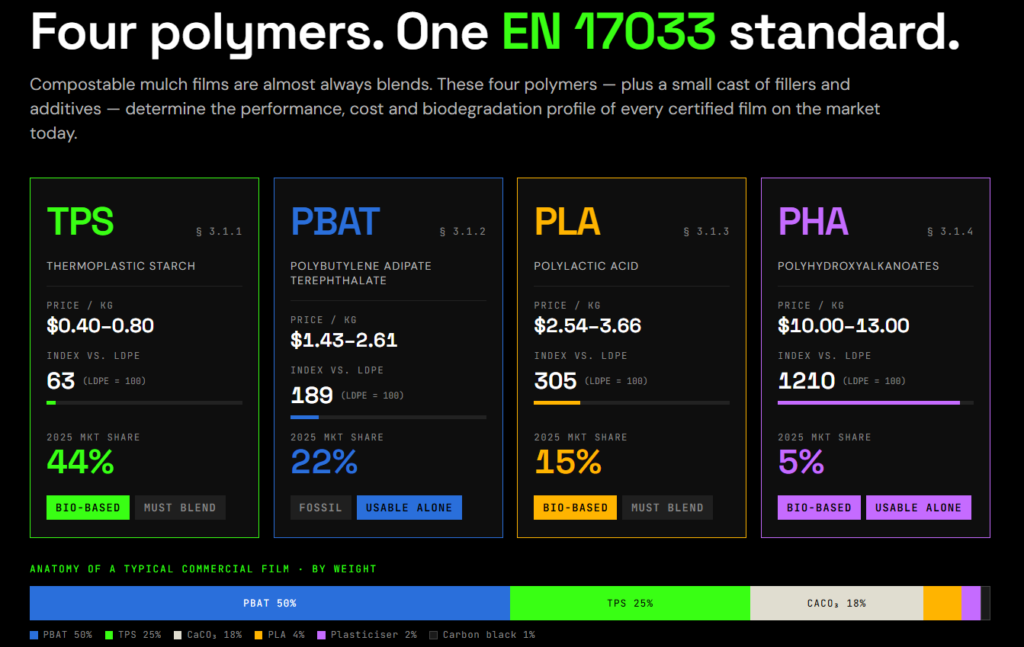

The performance, cost, and biodegradation profile of a compostable mulch film is determined by the materials it is made from.

This chapter profiles the four primary polymers used in certified compostable mulch, the fillers and additives that make them commercially viable, and the market share each of them commands.

3.1 Polymer Profiles: Properties, Processing, and Pricing

3.1.1 TPS (Thermoplastic Starch) and Starch-Based Blends

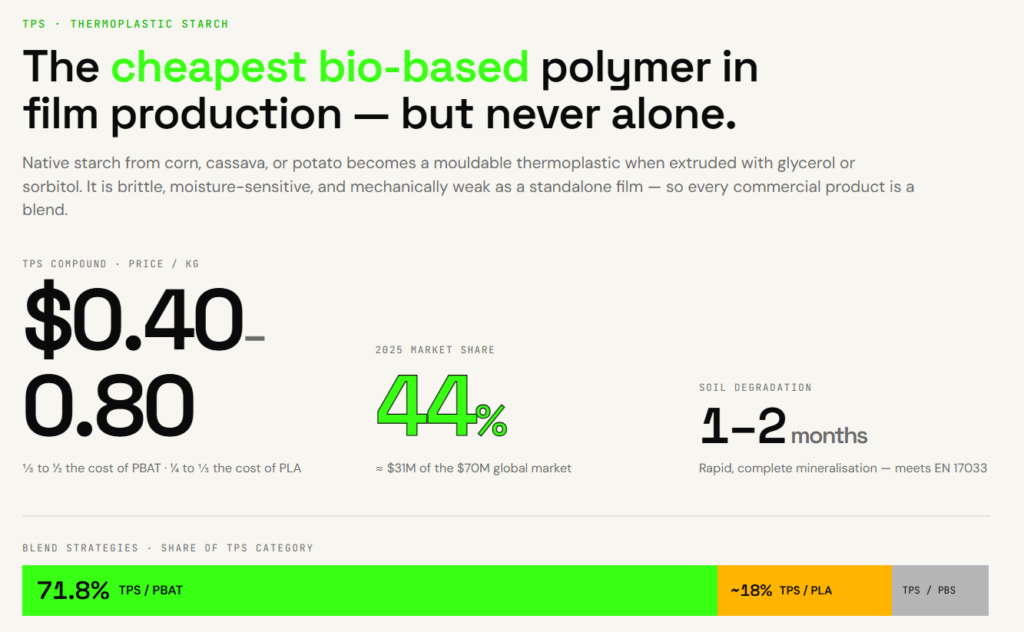

What Is Thermoplastic Starch

Thermoplastic starch (TPS) is produced by processing native starch (from corn, cassava, potato, or other crops) with heat and plasticisers such as glycerol or sorbitol in a twin-screw extruder.

This converts granular starch into a mouldable, extrudable thermoplastic.

TPS is the cheapest bio-based polymer available for film production, which is the primary reason it dominates the compostable mulch film market by volume.

TPS Properties and Processing Behaviour

TPS offers two significant advantages for mulch applications:

it is a low-cost renewable carbon source, and

it degrades rapidly and completely in soil, producing only water, CO₂, and biomass.

Its biodegradation profile comfortably meets EN 17033 requirements.

Its limitations are equally significant.

Pure TPS films are brittle, moisture-sensitive, and mechanically weak.

They absorb water from soil and humid air, losing structural integrity.

They lack the tensile strength and elongation needed to survive tractor-mounted installation.

These properties make TPS unusable as a standalone mulch film material. It must be blended.

Tensile strength: Too low for mechanical laying when unblended.

Water sensitivity: TPS swells and softens on contact with moisture, which accelerates degradation but compromises in-season performance.

Processing: TPS is compounded into pellets before film extrusion. The compounding step (starch + glycerol + water in a twin-screw extruder) is critical for achieving consistent melt flow in downstream blown film lines.

TPS Blend Strategies

Because pure TPS cannot function as a mulch film, the commercially relevant products are all blends.

The blend partner determines the film’s mechanical performance, degradation timing, and price.

TPS/PBAT blends are the market standard, projected to hold a 71.81% share of the material category.

PBAT provides the flexibility, tear resistance, and water resistance that TPS lacks.

Typical ratios range from 40 to 60% PBAT with 25 to 40% TPS and the balance in fillers.

The PBAT acts as a hydrophobic shield around starch domains: microbes colonise the starch first, then the PBAT matrix degrades in a controlled sequence.

TPS/PLA blends use PLA to add stiffness and improve the film’s Young’s modulus.

These are less common than TPS/PBAT but appear in formulations targeting higher mechanical performance.

TPS/PBS blends are emerging, with PBS offering a middle ground between PBAT’s flexibility and PLA’s rigidity.

Insight: The blend ratio is not just a technical decision. It is the primary cost lever in compostable mulch film economics.

Every percentage point of TPS replacing PBAT in a formulation reduces material cost, because TPS feedstock runs $0.40 to $0.80 per kg compared with $1.50 to $2.50 for PBAT.

This is why TPS-heavy formulations dominate in price-sensitive Mediterranean and APAC markets.

TPS Pricing and Feedstock Economics

TPS is the cheapest material in the compostable mulch film supply chain.

Feedstock costs (raw starch from corn, cassava, or potato) are low and relatively stable compared with petrochemical-derived monomers.

TPS compound price: Approximately $0.40 to $0.80 per kg, depending on starch source, plasticiser type, and regional feedstock availability.

Feedstock geography: Asia-Pacific leads in low-cost TPS production due to vertical integration with cassava and potato starch supply chains in Thailand, Indonesia, and Vietnam.

European TPS production draws primarily on corn and potato starch, at moderately higher cost.

Comparative position: TPS is roughly one-third to one-half the cost of PBAT per kilogram and one-quarter to one-third the cost of PLA.

This cost gap is the fundamental reason starch-based blends hold the largest market share and are projected to grow it.

TPS and starch-based films market size in the compostable mulch segment is estimated at approximately $31 million in 2025, representing roughly 44% of the global market.

This share is expected to grow as feedstock economics continue to favour starch over synthetic polyesters.

3.1.2 PBAT (Polybutylene Adipate Terephthalate)

What Is PBAT

PBAT is a fully biodegradable aliphatic-aromatic copolyester.

Its molecular structure combines four monomers: 1,4-butanediol, adipic acid, terephthalic acid, and dimethyl terephthalate.

The aliphatic segments (butanediol and adipic acid) provide flexibility and biodegradability.

The aromatic segments (terephthalic acid) provide the mechanical strength that makes PBAT processable into tough, flexible films.

PBAT is petroleum-derived but certified soil-biodegradable, which places it in a distinct category from bio-based materials like PLA or TPS.

PBAT Properties and Film Processing Behaviour

PBAT is valued in mulch film applications for its high elongation at break (over 400%), good tear resistance, and flexibility at low temperatures.

These properties make it the closest biodegradable equivalent to conventional LDPE in terms of how the film handles during installation and performs in the field.

Processing PBAT into film requires careful control of two variables:

Moisture: PBAT is highly sensitive to residual water.

At processing temperatures, water molecules trigger hydrolytic chain scission, weakening the polymer. Resin must be dried at 65 to 80°C for 4 to 6 hours to reach moisture levels below 0.02% before extrusion.

Temperature: Blown film extrusion uses a progressive temperature profile, typically 140°C at the feed zone rising to 165 to 175°C at the die.

PBAT should not be left sitting in a heated barrel during shutdowns because it decomposes into acidic residues that corrode equipment.

Blow-up ratio: A BUR of 2.5 to 4.0 is recommended for optimal mechanical orientation and film uniformity.

Why PBAT Is Rarely Used Alone

Despite its strong mechanical profile, PBAT is almost never used as a standalone mulch film resin.

The reasons are economic and functional.

Cost: Pure PBAT film is too expensive to compete with PE mulch at farm-gate prices.

Blending with TPS reduces material cost by 20 to 40%.

Mechanical tuning: Standalone PBAT can be too flexible for some applications.

Blending with PLA increases stiffness. Blending with TPS can improve hydrophobicity and thermal stability.

Degradation control: In blends, PBAT acts as a hydrophobic matrix that protects starch domains from premature moisture breakdown.

Once tilled into soil, microbes colonise the starch first, then the exposed PBAT degrades.

This creates a “programmed degradation” sequence where the film holds together during the growing season and breaks down afterward.

Multilayer use: In co-extruded films, a core layer of 100% PBAT provides mechanical strength while outer layers of PBAT/TPS/CaCO₃ blends offer easier microbial access for biodegradation.

PBAT Pricing

PBAT pricing fluctuates with petrochemical feedstock costs (adipic acid and butanediol) and varies significantly by region.

Global range: Commercial estimates span $1.40 to $4.00 per kg depending on market, grade, and date.

China: The lowest-cost producer region, with domestic prices around $1.43 per kg in 2025 periods.

Europe: Assessed between $1.82 and $2.48 per kg, reflecting higher compliance costs and logistics.

Japan: Approximately $2.61 per kg, reflecting a premium-specification market.

United States: Rose to approximately $1.80 per kg following supply disruptions in early 2026.

Stat: At an average of $1.65 to $2.50 per kg, PBAT costs two to four times more than conventional LDPE (approximately $0.95 per kg).

This price gap is the single largest reason that blending with cheaper starch is commercially necessary.

3.1.3 PLA (Polylactic Acid)

3.1.3 PLA (Polylactic Acid)

What Is PLA

Polylactic acid (PLA) is a bio-based thermoplastic polyester derived from renewable feedstocks, most commonly corn starch, sugarcane, or cassava.

It is produced by fermenting plant sugars into lactic acid, which is then polymerised.

PLA is the most widely produced bio-based plastic globally, with total production exceeding 620,000 metric tonnes in 2024, led by China at over 186,000 metric tonnes.

PLA Properties and Film Processing Behaviour

PLA offers high tensile strength (50 to 70 MPa) and excellent stiffness, comparable to petroleum-based polystyrene.

It is naturally transparent, resistant to grease and oil, and provides good barrier properties.

For mulch film applications, however, PLA has some significant weaknesses.

Brittleness: PLA has an elongation at break of only about 5%, far below the 200 to 500% range required for tractor-mounted installation.

A pure PLA mulch film would tear during laying.

Melt processing difficulty: PLA has insufficient melt strength for stable blown film extrusion.

The polymer tends to sag near the die exit (“melt sag”) and produces unstable bubbles.

Processors use melt strength enhancers or carefully control processing speed and air pressure to compensate.

Moisture sensitivity: Like PBAT, PLA pellets must be thoroughly dried before processing (40 to 50°C for 24 hours) to prevent hydrolytic chain scission during extrusion.

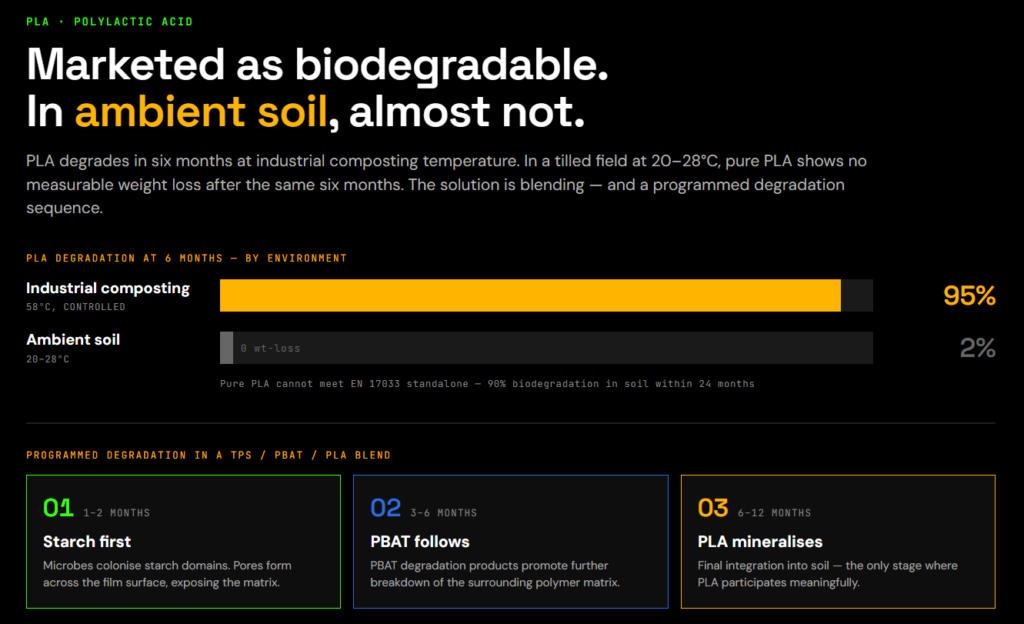

The Soil-Biodegradation Paradox

This is the most important technical nuance about PLA in the mulch context.

PLA is widely marketed as biodegradable, and under industrial composting conditions (58°C and above), it degrades rapidly within six months.

But in ambient soil at 20 to 28°C, pure PLA shows no measurable weight loss after six months and can persist for years.

This means pure PLA film cannot meet the EN 17033 requirement of 90% biodegradation within 24 months in soil.

The solution is blending.

When PLA is combined with PBAT and TPS, the blend degrades in a stepwise sequence:

Starch degrades first (1 to 2 months), creating pores and surface area for microbial colonisation.

PBAT follows (3 to 6 months), with its degradation products promoting further breakdown of the surrounding matrix.

PLA undergoes final mineralisation (6 to 12 months), completing the film’s integration into the soil.

This stepwise mechanism allows PLA-containing blends to meet EN 17033 certification while benefiting from PLA’s mechanical contribution to the film.

PLA Pricing

PLA sits between TPS (cheapest) and PBAT (more expensive) in the cost hierarchy, though regional variation is significant.

Europe: $3.66 per kg (April 2026 spot price), the highest among major regions.

Southeast Asia: $2.98 per kg.

Northeast Asia: $2.67 per kg.

North America: $2.54 per kg.

Comparative position: On a price index where conventional polypropylene equals 100, PLA sits at 170 to 200.

It is roughly twice the cost of LDPE but generally cheaper than PBAT outside of China.

Blending PLA with TPS ($0.40 to $0.80 per kg) reduces overall film cost by 20 to 40%.

3.1.4 PHA (Polyhydroxyalkanoates)

What Are Polyhydroxyalkanoates

Polyhydroxyalkanoates (PHA) are a family of bio-based polyesters produced naturally by microorganisms.

Bacteria synthesise PHA as intracellular energy storage granules when fed carbon-rich feedstocks such as sugars, plant oils, or even waste streams like molasses.

Unlike every other material in this chapter, PHA is fully bio-based, fully soil-biodegradable, and fully marine-biodegradable without requiring blending or special conditions.

This combination of properties makes it the most environmentally complete polymer available for mulch film applications.

It is also, by a wide margin, the most expensive.

PHA Properties and Film Processing Behaviour

PHA degrades through complete microbial mineralisation in soil and marine environments at ambient temperatures.

It comfortably meets EN 17033 requirements without the blending workarounds that PLA needs.

PHA resins are naturally UV-resistant and moisture-resistant, which are useful properties for outdoor agricultural exposure.

The processing challenges for PHA are significant.

PHA resins have narrow melt-processing windows, with some variants melting very close to their thermal degradation point.

Crystallisation is slow, which causes bubble instability in blown film extrusion and longer production cycles.

Pure PHB (the most common homopolymer) is highly crystalline and extremely brittle, which makes it unsuitable for standalone film production.

To overcome these limitations, PHA is typically blended with PLA, PBAT, or PCL.

Higher-performance copolymers such as PHBHHx offer a wider processing window and can support standard blown film and multilayer extrusion without blending, but they are produced in limited volumes.

PHA Variants: PHB, PHBV, and PHBH

The PHA family contains several variants with meaningfully different performance profiles.

PHB (poly-3-hydroxybutyrate): The most common and cheapest PHA variant.

Stiffer than polypropylene but extremely brittle, with very low elongation at break. Not viable as a standalone film material.

PHBV (polyhydroxybutyrate-co-valerate): A copolymer with improved toughness and a lower melting point (~137°C) that makes it easier to process.

Elongation at break of 10 to 50% is better than PHB but still well below PBAT or PE levels. Used in blends to balance rigidity and flexibility.

PHBH / PHBHHx (polyhydroxybutyrate-co-hexanoate): The most advanced variant.

The hexanoate units reduce crystallinity and increase flexibility, giving it the broadest processing window and the closest mechanical profile to conventional HDPE.

Currently produced in small quantities at premium pricing.

PHA Pricing

PHA is the most expensive compostable resin in commercial use.

Price range: Industrial estimates for PHA resins run $10 to $13 per kg, roughly three times the cost of PLA/PBAT blends and more than ten times the cost of conventional LDPE.

Cost drivers: Microbial fermentation is complex and energy-intensive.

Downstream purification (extracting PHA granules from bacterial cells) adds further cost. Supply stability is low compared with starch-based or petrochemical-derived polymers.

Cost reduction trajectory: Some manufacturers project that scale-up could eventually bring PHA prices toward $2.50 per kg, but current global production capacity (expected to surpass 50,000 tonnes by 2025) remains far too small to achieve this.

Stat: On a price index where conventional polypropylene equals 100, PHA sits above 300.

This is why PHA is used primarily as a strategic blend component to meet soil-biodegradation requirements, rather than as a standalone film resin.

3.2 Fillers, Additives, and Cost Modifiers In Compostable Agricultural Mulch Films

The polymers covered above receive most of the attention in market reports and investor presentations.

But the materials that make compostable mulch films commercially viable at farm-gate prices are the ones that receive the least coverage: mineral fillers, plasticisers, and pigments.

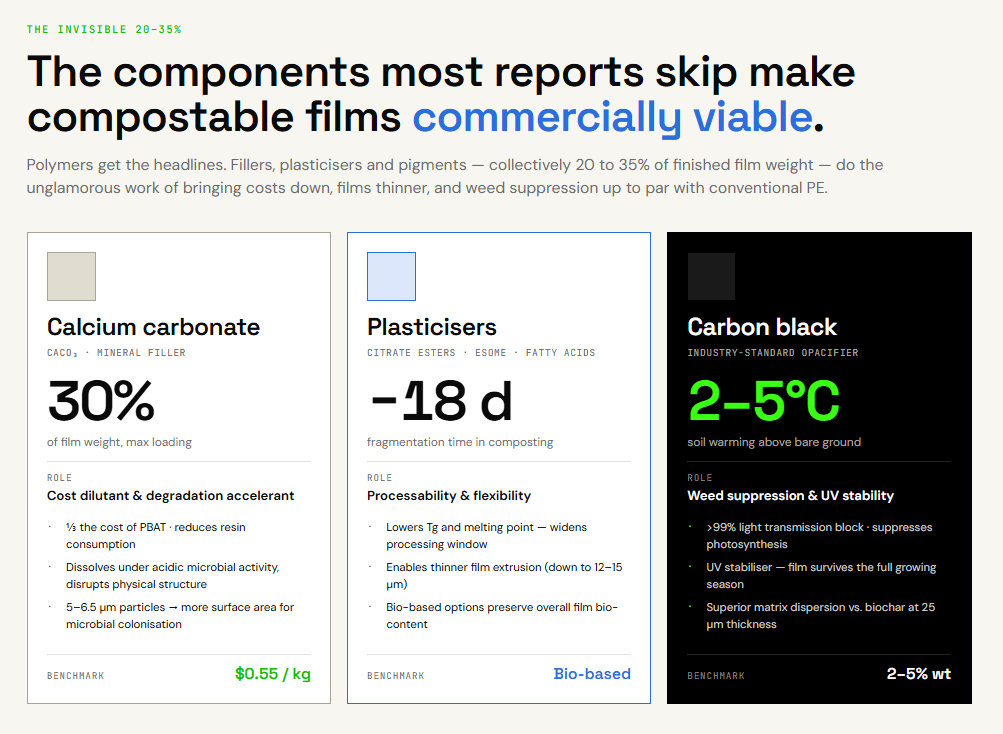

These components can constitute 20 to 35% of a finished film by weight and have an outsized effect on both cost and field performance.

Calcium Carbonate: Cost Reduction and Degradation Management

Calcium carbonate (CaCO₃) is the most widely used inorganic filler in compostable mulch film production.

At approximately $0.55 per kg, it costs roughly one-third the price of PBAT.

By loading CaCO₃ at up to 30% of film weight, manufacturers dilute resin consumption and reduce overall material cost significantly while maintaining acceptable mechanical properties.

CaCO₃ also plays an active role in biodegradation.

In acidic soil conditions (created by microbial activity from organisms such as Clostridium perfringens), the calcium carbonate particles dissolve, disrupt the film’s physical structure and accelerate total breakdown.

This makes CaCO₃ a dual-purpose additive: it reduces cost and helps programme degradation timing.

Two technical details matter for formulators:

Particle size: Smaller particles (5 to 6.5 µm) provide greater surface area for microbial colonisation and water diffusion, accelerating hydrolysis and mineralisation compared with larger particles.

Surface treatment: CaCO₃ is naturally incompatible with some polymer matrices. Coating agents such as polyethylene glycol or silanes improve dispersion within the blend, which in turn improves both mechanical performance and water diffusivity.

Plasticisers, Lubricants, and Carbon Black

Plasticisers solve a specific problem: biopolymers like PLA and PHA are inherently brittle, and without plasticisation many blends cannot be processed into thin, flexible films.

Plasticisers work by lowering the glass transition temperature and melting point of the polymer, which widens the processing window and enables thinner film production.

Common compounds: Bio-based options include citrate esters and epoxidised soybean oil methyl ester (ESOME), which are preferred because they maintain the film’s overall bio-based content.

Degradation impact: Effective plasticisers increase polymer chain mobility, which can reduce film fragmentation time by up to 18 days in composting conditions.

Lubricants: Fatty acids and their salts are added as processing aids to stabilise the melt during extrusion.

Carbon black is the industry-standard opacifier that makes weed suppression possible.

Effective weed control requires blocking at least 75% of photosynthetically active radiation (PAR).

Carbon black achieves near-total opacity (light transmission below 1%) at concentrations of just 2 to 5% by weight.

Beyond opacity, carbon black contributes two additional functions:

UV stabilisation: It absorbs ultraviolet radiation that would otherwise accelerate polymer degradation during the growing season, helping the film maintain integrity until it is tilled into soil.

Soil warming: Black-pigmented films absorb ultraviolet, visible, and infrared wavelengths, raising soil temperature by 2 to 5°C above bare-ground levels.

This thermal effect is critical for early-season growth of high-value crops such as melons and strawberries.

Insight: Carbon black offers superior matrix dispersion compared with alternative opacifiers like biochar.

This allows manufacturers to produce functional films at standard thicknesses of 25 µm without sacrificing mechanical strength.

This processing advantage is why carbon black remains dominant despite growing interest in bio-based pigment alternatives.

3.3 Compostable Agricultural Mulch Film Market Size by Material

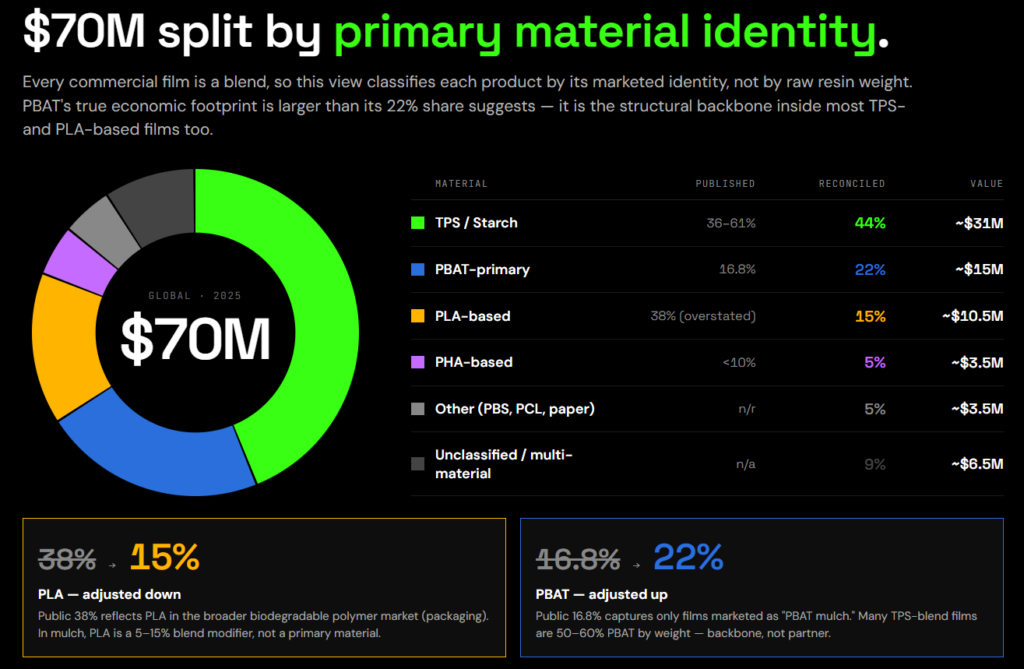

Understanding how the $70 million global compostable mulch film market breaks down by material is essential for two audiences.

For investors, it reveals which polymer platforms command the most revenue and where share is shifting.

For procurement teams, it shows which material categories offer the most competitive pricing and where supply concentration creates risk.

Why material-level sizing is difficult in this market

Every published market report on compostable mulch films attempts to size the market by material.

Every one of them faces the same structural limitation, and most do not acknowledge it.

Compostable mulch films are almost never made from a single polymer. They are blends.

A typical commercial product might contain PBAT for flexibility, thermoplastic starch for cost reduction and biodegradation, a small percentage of PLA for rigidity, calcium carbonate as a filler, and carbon black for opacity.

When a film contains four or five materials, assigning its full market value to one of them requires a classification decision that is inherently imperfect.

The standard approach, which published research uses and which we follow here, is to classify each finished film product under its primary material identity.

This means:

A film sold as a “starch-based biodegradable mulch” is counted under TPS, even if it contains 50 to 60% PBAT by weight.

A film marketed as a “PBAT compostable mulch” counts under PBAT, even if 20% of its weight is starch and 15% is calcium carbonate.

Each dollar of the $70 million global market is therefore assigned to the material category that defines the product as marketed, not to the individual resins inside it.

This is a market share by product category (value), not a breakdown of raw material consumption by weight.

Readers should keep this distinction in mind when interpreting the figures below: PBAT’s true economic importance, for example, is larger than its product-category share suggests, because PBAT is also the structural backbone inside most TPS-based and PLA-based films.

Reconciling conflicting public data

To size the market by material, we need dependable estimates of each material’s share of the compostable agricultural mulch film market by value.

Published figures from multiple research firms exist, but they conflict in ways that must be resolved before they can be applied to our $70 million global figure.

TPS / Starch-based blends

Published share estimates range from 36% to 61%.

The lower figures (36 to 47%) represent current market share by revenue from firms including Mordor Intelligence and Precedence Research.

The higher figures (57 to 61%) are forward-looking projections that assume TPS cost advantages will continue pulling share from synthetic polyesters over the next decade.

For 2025, we use approximately 44%, which sits at the upper end of the current-year estimates and reflects TPS’s established dominance in cost-sensitive European and APAC markets.

PBAT-primary blends

Published at 16.8% of the market.

This captures only films where PBAT is the primary marketed material identity.

It understates PBAT’s presence because many PBAT-heavy formulations (containing 50 to 60% PBAT by weight) are classified under “starch blend” by reports that lead with the starch component.

We adjust upward to approximately 22%.

PLA-based blends

Published at 38%.

This figure requires the most significant correction.

In mulch film formulations, PLA typically appears at only 5 to 15% of blend weight.

It is a performance modifier, not the primary material.

The 38% almost certainly originates from sources sizing PLA’s share across the broader biodegradable polymer market, where PLA dominates packaging applications.

For compostable mulch specifically, we adjust to approximately 15%.

PHA-based films

Published at under 10%.

PHA is genuinely small in current mulch applications.

It is the fastest-growing segment by CAGR (9 to 11%), but the installed base is minimal.

We use approximately 5%.

Other materials (PBS, PBSA, paper, PCL)

No single published figure.

These are collectively minor.

We estimate approximately 5%.

Unclassified / multi-material

The remaining approximately 9% represents films where primary material classification is ambiguous, multi-material co-extrusions that do not fit neatly into one category, or products from smaller manufacturers whose blend compositions are not publicly documented.

Compostable mulch film market size by material (2025)

| Material category | Published range | Reconciled share | Estimated market value (2025) |

|---|---|---|---|

| TPS / Starch-based blends | 36% to 61% | ~44% | ~$31M |

| PBAT-primary blends | ~16.8% | ~22% | ~$15M |

| PLA-based blends | ~38% (overstated) | ~15% | ~$10.5M |

| PHA-based films | <10% | ~5% | ~$3.5M |

| Other (PBS, PBSA, paper, PCL) | Not reported | ~5% | ~$3.5M |

| Unclassified / multi-material | N/A | ~9% | ~$6.5M |

| Total | 100% | $70M |

Reading this table:

The “Published range” column shows what research firms report.

The “Reconciled share” column shows the figure we use after adjusting for scope errors and classification inconsistencies.

The gap between the two is widest for PLA (adjusted from 38% down to 15%) and PBAT (adjusted from 16.8% up to 22%).

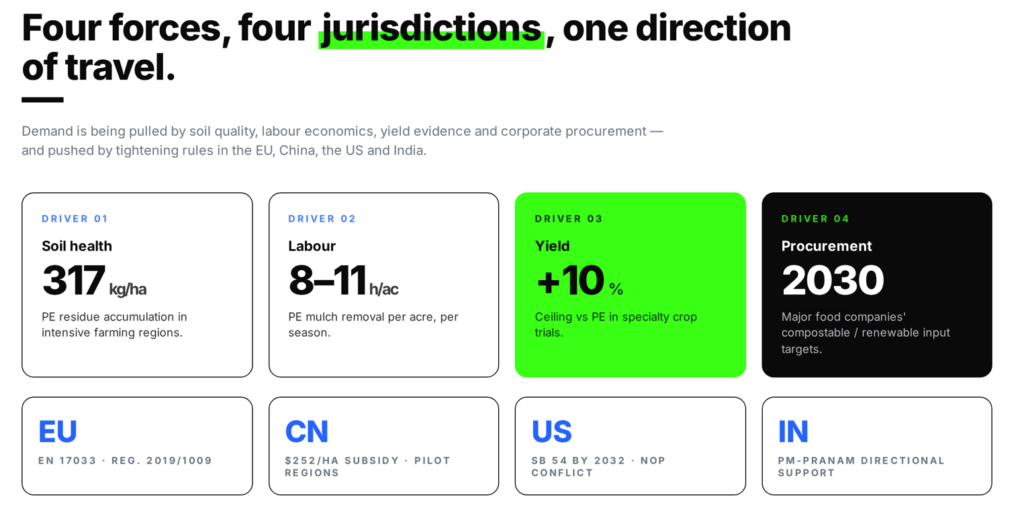

4.1 Compostable Agricultural Mulch Films – Demand Drivers

The shift toward compostable and soil-biodegradable mulch films is the result of several forces converging at once:

deteriorating soil quality from plastic accumulation,

rising labour costs for conventional film removal,

tightening regulation across major agricultural economies (explained in detail in section 4.2), and

growing supply-chain pressure from food companies with sustainability commitments.

Each of these operates on a different timescale and affects different buyer segments, but together they are moving the market from niche to structural.

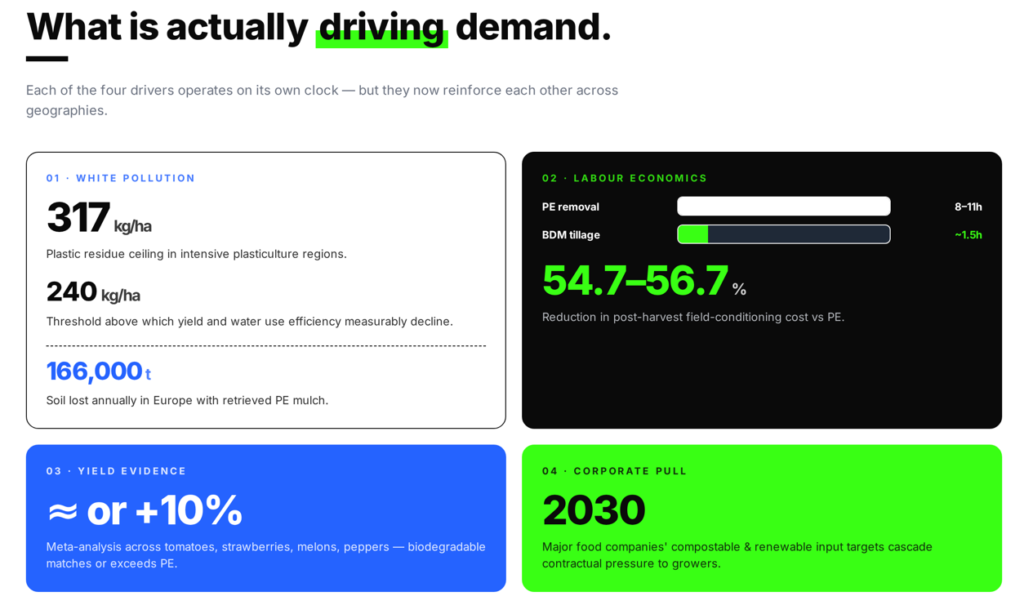

Soil health and the problem of white pollution

The most fundamental driver is agronomic.

Conventional polyethylene mulch film does not biodegrade.

When it is removed from the field after harvest, fragments are inevitably left behind.

Over years of repeated mulching, these fragments accumulate.

In intensive farming regions, plastic residues in soil can reach levels as high as 317 kg per hectare.

At concentrations above 240 kg/ha, research shows measurable reductions in crop yield and water use efficiency.

The fragments also disrupt soil structure, block root penetration, interfere with water transport, and reduce aeration.

This problem is known as “white pollution” and is most acute in China, where over 20 million hectares are mulched annually, but it is present wherever PE mulch is used repeatedly without complete removal.

Compostable films address this directly: they undergo microbial mineralisation in the soil, convert into CO₂, water, and biomass rather than persisting as microplastic fragments.

Stat: An estimated 166,000 tonnes of soil is lost annually in Europe, carried away attached to retrieved PE mulch films during post-harvest removal.

Soil-biodegradable films that are tilled in place eliminate this loss entirely.

Labour economics and total cost of ownership

The second driver is operational.

Removing PE mulch from the field after harvest is labour-intensive, requiring 8 to 11 man-hours per acre.

On a 100-acre vegetable operation, that represents over 1,000 labour hours per season dedicated solely to pulling plastic off the ground.

Add to that the cost of transporting heavily soiled film to landfill and paying disposal fees, and the post-harvest cost of conventional mulch becomes substantial.

Compostable mulch films eliminate this step.

The film is tilled directly into the soil after harvest.

While the material itself costs 2 to 3 times more per roll than PE, it reduces post-harvest field conditioning costs by 54.7 to 56.7%.

For operations where labour is expensive or scarce (across North America and Western Europe), the total cost of ownership calculation can favour compostable films even at today’s price premium.

Yield performance

A persistent concern among growers is whether compostable films perform as well as PE in the field.

The evidence is now substantial.

Meta-analyses across specialty crops (tomatoes, strawberries, mel

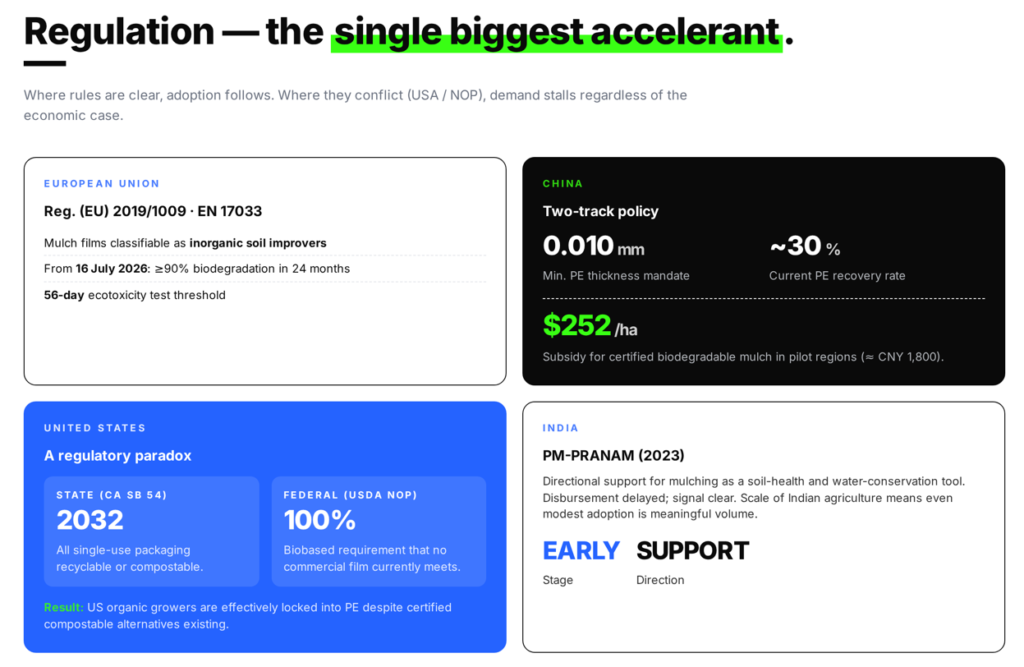

European Union

Europe operates the most developed regulatory framework for agricultural film biodegradability.

The Fertilising Products Regulation (EU) 2019/1009 is the pivotal piece of legislation.

It allows mulch films to be classified as “inorganic soil improvers”, which means they can legally be tilled into soil rather than collected as waste.

From July 16, 2026, polymers used in these films must demonstrate at least 90% biodegradation in soil within 24 months and pass 56-day ecotoxicity tests.

As of November 2025, starch-based films (such as Mater-Bi formulations) have already received certification under this framework.

The EU Single-Use Plastics Directive and the broader Circular Economy Action Plan add further pressure by restricting conventional plastic use in agriculture and compelling the shift toward certified biodegradable alternatives.

EN 17033 remains the defining technical standard for soil-biodegradable mulch films across the EU.

China

China is the world’s largest consumer of agricultural film and faces the most severe white pollution problem.

Its policy response operates on two tracks simultaneously.

Track one: improving PE recovery.

China mandates a minimum PE film thickness of 0.010 mm to make films more durable and easier to collect after use.

Current recovery rates for conventional mulch sit at approximately 30%, meaning the majority of PE film laid each season remains in or on the soil.

Track two: subsidising biodegradable substitution.

The national Plastic Pollution Control Action Plan provides subsidies of approximately CNY 1,800 per hectare ($252) for farmers who switch to certified biodegradable mulch in designated pilot regions.

These subsidies have driven rapid uptake in provinces such as Xinjiang, Shandong, and Yunnan, making China the fastest-growing national market for compostable mulch film by volume.

Insight: China’s two-track approach reflects a pragmatic reality.

Full substitution of PE mulch across 20 million hectares is not feasible at current biodegradable film production capacity or pricing.

The near-term strategy is to improve PE recovery where possible and introduce biodegradable alternatives where subsidies make them cost-competitive, particularly for high-value crops and in regions where soil contamination is most advanced.

United States

The US regulatory environment for compostable agricultural film is shaped by a significant conflict between two policy goals.

At the state level, legislation like California SB 54 mandates that all single-use packaging and food service ware be recyclable or compostable by 2032, creating broader momentum toward compostable materials in agriculture as well.

At the federal level, the USDA National Organic Program (NOP) creates a paradox.

The NOP permits “biodegradable biobased mulch film” in organic farming, but requires 100% biobased content.

The problem is that no commercially functional mulch film currently meets this requirement.

The most widely used biodegradable resin, PBAT, is fully soil-biodegradable but petroleum-derived.

Until either the NOP adjusts its biobased threshold or a fully biobased alternative achieves commercial viability, organic farmers in the US are effectively forced to continue using and removing PE mulch, despite the availability of certified compostable alternatives.

Insight: The US organic mulch conflict is one of the clearest examples of regulation lagging behind material science in this market.

A resolution, whether through revised NOP standards, scaled PHA production (which is fully biobased), or new bio-based PBAT synthesis routes, would unlock a significant segment of North American demand.

India

India’s policy approach is earlier-stage but directionally supportive.

The PM-PRANAM scheme (2023) aims to reduce chemical fertiliser use and promotes mulching as a resource conservation technology.

Financial disbursement under the programme has faced delays, but the policy signal is clear: the Indian government views mulch adoption (including biodegradable options) as part of its broader soil health and water conservation strategy.

Given the scale of Indian agriculture, even modest adoption rates would represent meaningful volume.

5. Compostable Agricultural Mulch Films – Competitive Landscape and Supply Chain

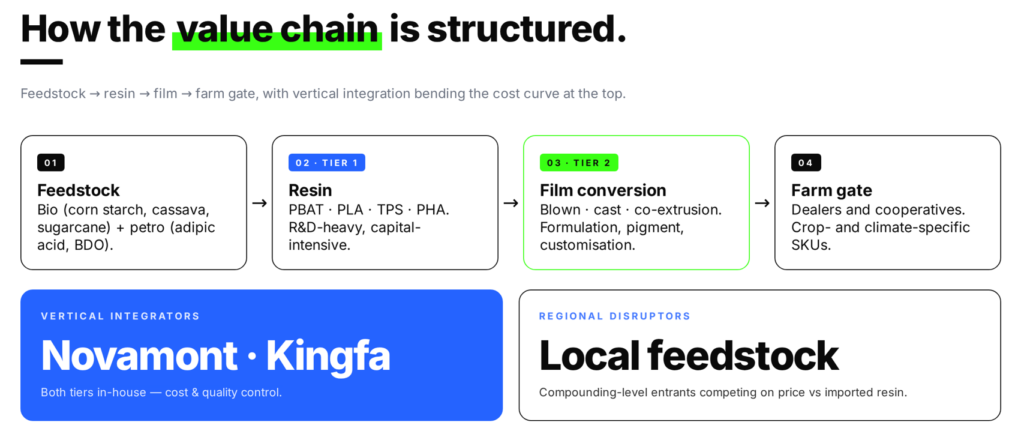

5.1 Compostable Agricultural Mulch Films – Value Chain

The compostable agricultural mulch film supply chain runs from raw feedstock through polymer synthesis, film conversion, and distribution to the farm gate.

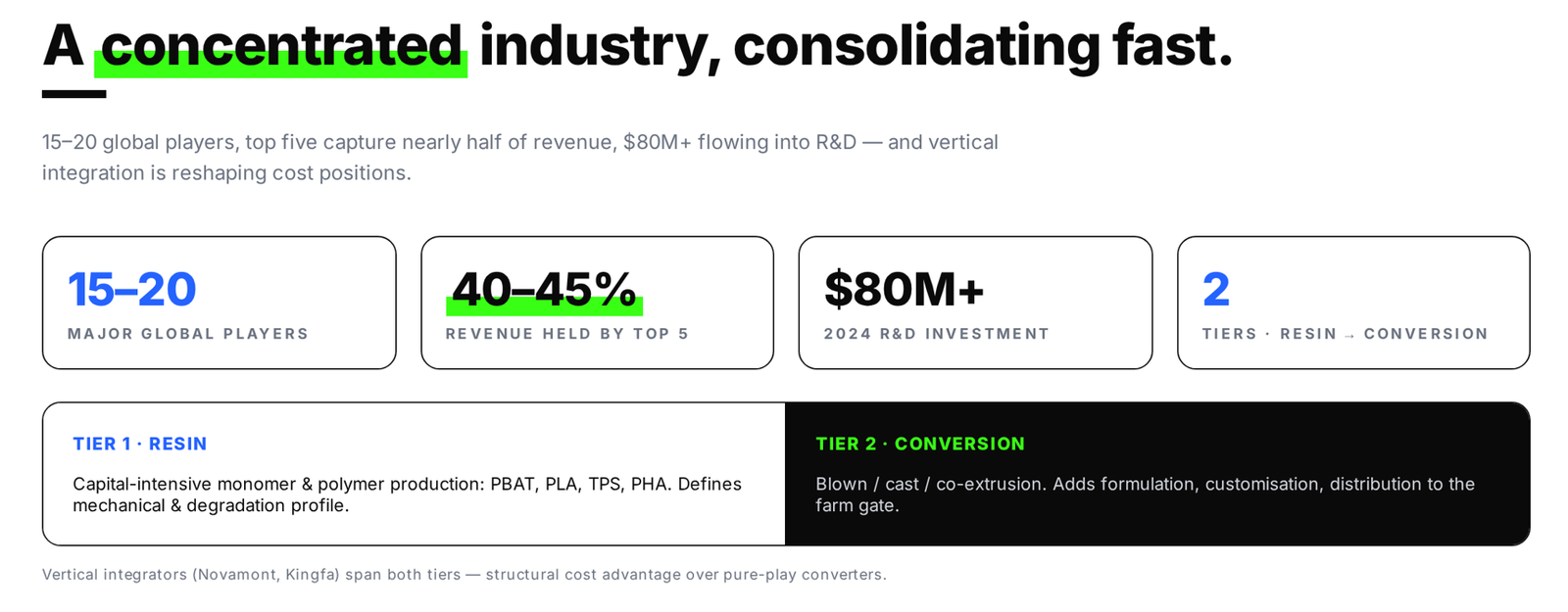

It is a relatively concentrated industry: approximately 15 to 20 major players operate globally, and the top five companies control roughly 40 to 45% of market revenue.

The value chain divides into two primary tiers, with a growing number of companies operating across both.

Tier 1: Biopolymer resin producers

Tier 1 companies produce the biopolymer resins (PBAT, PLA, TPS compounds, PHA) that define a film’s mechanical properties, degradation profile, and cost.

These are typically large chemical or biotechnology companies with significant R&D capacity and capital-intensive production infrastructure.

Tier 2: Film manufacturers and converters

Tier 2 companies are film manufacturers and converters.

They purchase resin from Tier 1 suppliers and process it into finished mulch film products using blown film extrusion, cast film, or co-extrusion lines.

Converters add value through:

formulation (blending resins with fillers, plasticisers, and pigments),

product customisation for specific crops and climates, and

distribution to agricultural dealers and cooperatives.

Vertical integration trend

A notable structural trend in this industry is vertical integration.

Several leading companies, most prominently Novamont and Kingfa, span both tiers, controlling resin production and film conversion.

This gives them cost advantages and tighter quality control over the final product.

At the other end of the spectrum, a growing number of regional startups are entering at the compounding or conversion level, using locally sourced feedstocks to compete on cost with imported resins.

5.2 Compostable Agricultural Mulch Films – Key Players by Tier

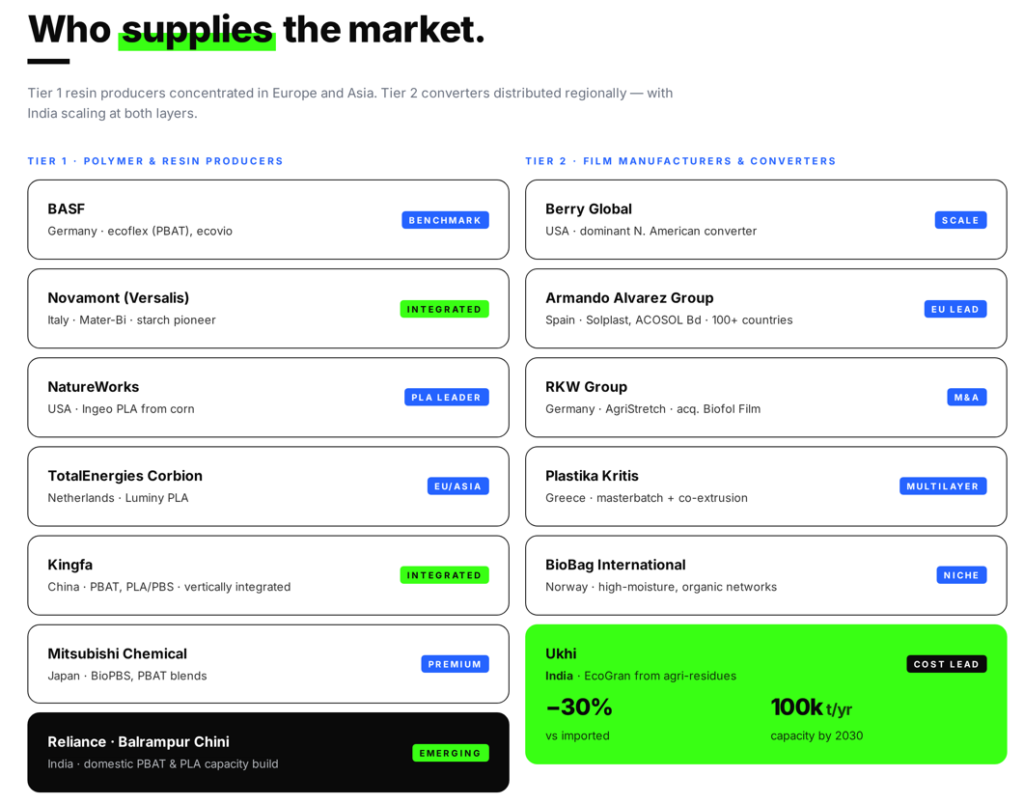

Tier 1: Polymer and Resin Producers

BASF SE (Germany) is the global benchmark in biodegradable polyester production.

Its ecoflex (PBAT) and ecovio (PLA/PBAT blend) product lines are the most widely referenced formulations in the compostable mulch market.

BASF’s scale in monomer production (adipic acid, butanediol) gives it a structural cost advantage in PBAT.

Novamont S.p.A. (Italy), now part of Versalis, is the pioneer of starch-based bioplastics.

Its Mater-Bi range is the dominant compostable mulch film material in European agriculture, particularly in Italy and Spain.

Novamont opened a new compounding facility in 2025 to expand global supply.

NatureWorks LLC (USA) is the primary global supplier of PLA resin under the Ingeo brand, produced from renewable corn starch.

NatureWorks supplies PLA to converters across packaging and agriculture.

TotalEnergies Corbion (Netherlands) produces Luminy PLA resins and is a significant supplier to the European and Asian markets.

Kingfa Sci. & Tech. Co. (China) has rapidly scaled PBAT and PLA/PBS production capacity, making it a major Asian supplier and global exporter.

Kingfa’s vertical integration into film conversion gives it a cost position that is difficult for pure-play converters to match.

Mitsubishi Chemical Corporation (Japan) produces advanced biodegradable resins including BioPBS and PBAT blends, serving the premium Japanese agricultural market.

Emerging producers:

Reliance Industries (India) is developing domestic PBAT manufacturing, and

Balrampur Chini (India) is constructing large-scale PLA facilities, both signalling that India is building upstream capacity to reduce dependence on imported resins.

Tier 2: Film Manufacturers and Converters

Berry Global Inc. (USA) is the dominant North American converter, offering both conventional PE and sustainable mulch film products across a broad crop portfolio.

Armando Alvarez Group (Spain) is one of Europe’s largest plastic film processors, serving over 100 countries through brands including Solplast and ACOSOL Bd.

In 2024, the company launched Solar Shrink, a thinner film structure that contracts under solar radiation for improved soil contact.

RKW Group (Germany) specialises in technical agricultural films including the AgriStretch line, and acquired Biofol Film GmbH to strengthen its biodegradable product portfolio.

Plastika Kritis S.A. (Greece) is a major Mediterranean converter with integrated masterbatch production and co-extrusion capability, specialising in multilayer films.

BioBag International AS (Norway) focuses on compostable film products for high-moisture soil applications and organic grower networks.

Ukhi (India) is an IP-led startup using agricultural waste residues to produce EcoGran, a biopolymer compound reported to be 30% less expensive than imported equivalents.

Ukhi’s model targets the cost barrier that limits adoption in price-sensitive markets, with projected production capacity of 100,000 tonnes annually by 2030.

5.3 Compostable Agricultural Mulch Films – Recent Investment and Partnership Activity

Capital is flowing into this sector at an accelerating rate, with R&D investment in biodegradable mulch films exceeding $80 million in 2024.

The activity falls into three categories.

Corporate R&D and product launches

BASF launched a specialised tropical-grade ecovio mulch film and expanded R&D partnerships in India during 2024/2025.

Novamont opened a new compounding capacity.

Dow developed DOWSIL 5-1050, a fluoropolymer-free processing aid designed to improve extrusion efficiency for agricultural film lines.

These moves indicate that established players are investing in both geographic expansion and manufacturing cost reduction.

Mergers and acquisitions

The market is consolidating as large packaging and chemical groups acquire specialised bioplastics firms.

RKW Group’s acquisition of Biofol Film GmbH added biodegradable capability to its agricultural film portfolio.

Kuraray acquired Plantic Technologies, a leader in high-starch-content materials, securing access to starch-based polymer IP.

This consolidation pattern is typical of a market transitioning from niche to mainstream: incumbents are buying capability rather than building it from scratch.

Cross-border research collaborations

Several government-funded programmes are working to extend compostable mulch film technology to new geographies and crop systems.

The UK-India Newton Fund supports collaboration between British and Indian researchers to develop degradable bioplastic film from tapioca starch waste from the cassava industry.

The UK-funded SMEP Programme (Sustainable Manufacturing and Environmental Pollution) is working with CSIR (South Africa) and Elizade University (Nigeria) to develop biodegradable mulch films tailored for Sub-Saharan African agriculture.

The HiBarFilm Project, led by Haydale under Innovate UK funding, is coating monolayer compostable films with functionalised graphene to enhance barrier performance, a technology that could allow single-layer compostable films to match the performance of non-recyclable multilayer structures.

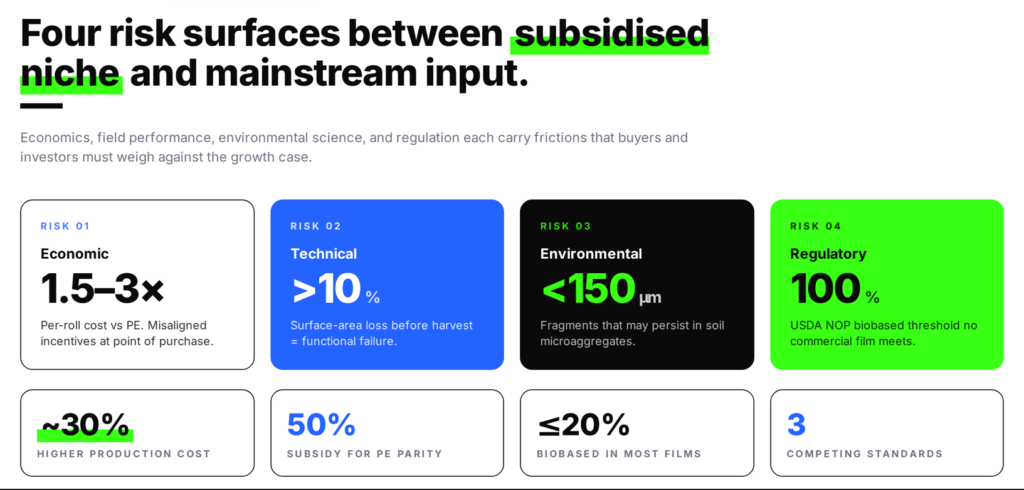

6. Compostable Agricultural Mulch Films – Risks and Challenges

The compostable mulch film market faces genuine obstacles that will determine whether it transitions from a subsidised niche to a mainstream agricultural input.

These risks span economics, field performance, environmental science, and regulation.

Investors and buyers should weigh them against the growth drivers outlined in Chapter 4.

Economic Risks

Upfront cost remains the single largest barrier to adoption.

Biodegradable mulch film costs 1.5 to 3 times more per roll than conventional PE, and production costs run approximately 30% higher than traditional plastic films.

While total cost of ownership can favour compostable film when labour and disposal savings are factored in (as discussed in Chapter 1), many growers evaluate cost at the point of purchase, not across the full season.

This creates an incentive misalignment.

Large-scale specialty crop operations (strawberries, tomatoes, peppers) can absorb the premium because their per-hectare revenues are high and their PE removal labour costs are substantial.

But lower-margin field crop growers (maize, cotton, grains) often cannot justify the upfront expense, even where the agronomic case is sound.

In several markets, adoption currently depends on government subsidies.

Research suggests that a subsidy rate of approximately 50% of the market price would be needed to equalise the cost of biodegradable mulch with PE across all crop categories.

Where subsidies exist (notably China at CNY 1,800/ha), adoption accelerates.

Where they do not, penetration remains confined to high-value crops.

Technical and Field Performance Risks

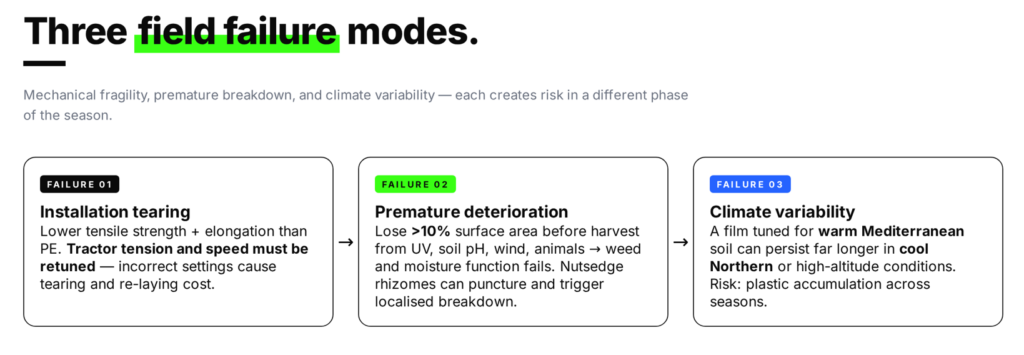

Mechanical fragility during installation is a persistent operational concern.

Compostable films generally have lower tensile strength and elongation at break than PE.

This makes them sensitive to the tension settings on tractor-mounted laying equipment.

Incorrect settings or excessive speed can cause tearing, which wastes material and requires costly re-laying.

Premature deterioration is another problem.

It is the inverse of the degradation-timing problem described in Chapter 1.

If a film loses more than 10% of its surface area before harvest, due to UV exposure, soil pH variation, wind stress, or animal damage, it fails its core function of weed suppression and moisture retention.

Aggressive perennial weeds such as nutsedge pose a particular challenge: their sharp rhizomes can puncture the film and trigger rapid localised breakdown.

Performance variability across climates and soil types remains significant.

Biodegradation rates depend on soil temperature, moisture, and microbial activity.

A film that degrades on schedule in a warm, humid Mediterranean climate may persist far longer in cooler Northern European or high-altitude conditions.

This raises concerns about plastic accumulation over successive seasons.

Environmental and Ecological Risks

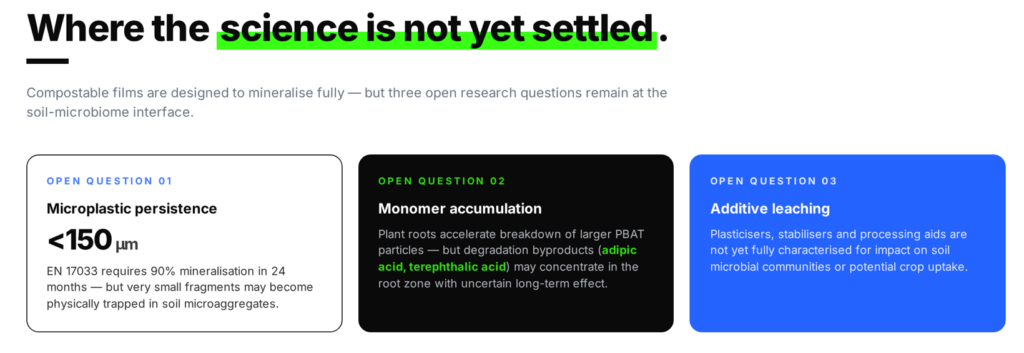

Compostable films are designed to mineralise fully in soil, but emerging research identifies areas where the science is not yet settled.

Microplastic persistence: While certified films must achieve 90% mineralisation within 24 months under EN 17033, very small fragments (below 150 µm) can become physically trapped within soil microaggregates.

Monomer accumulation in the root zone: Studies have found that plant roots can accelerate the breakdown of larger film particles, but this process may concentrate degradation byproducts (such as adipic acid and terephthalic acid from PBAT) directly around the roots, with uncertain long-term effects on plant health.

Additive leaching: The plasticisers, stabilisers, and processing aids used in compostable films have not been fully characterised for their long-term impact on soil microbial communities or potential uptake by crops.

Regulatory and Certification Risks

Standards confusion between industrial compostability (ASTM D6400, EN 13432) and soil biodegradability (EN 17033) continues to create market friction.

A film certified only under ASTM D6400 may not degrade at acceptable rates in actual farm soil, but buyers do not always understand this distinction.

The USDA organic certification barrier discussed in Chapter 4 locks out the largest certified biodegradable resins (particularly PBAT) from organic farming in the United States.

Most commercial compostable films contain 20% or less bio-based content by weight, well below the NOP’s 100% biobased requirement.

More broadly, the absence of harmonised global standards for in-field biodegradability creates uncertainty for manufacturers serving multiple regions and for growers trying to calculate return on investment with confidence.

7. Compostable Agricultural Mulch Films – Investment Opportunities

The compostable agricultural mulch film market is moving from early adoption into a phase where the investment case is built on regulatory mandates, proven agronomic performance, and identifiable technology bottlenecks waiting to be solved.

This chapter outlines where capital is flowing, where it is likely to flow next, and which emerging revenue models could reshape the sector’s economics.

Compostable Agricultural Mulch Films – Capital Flow

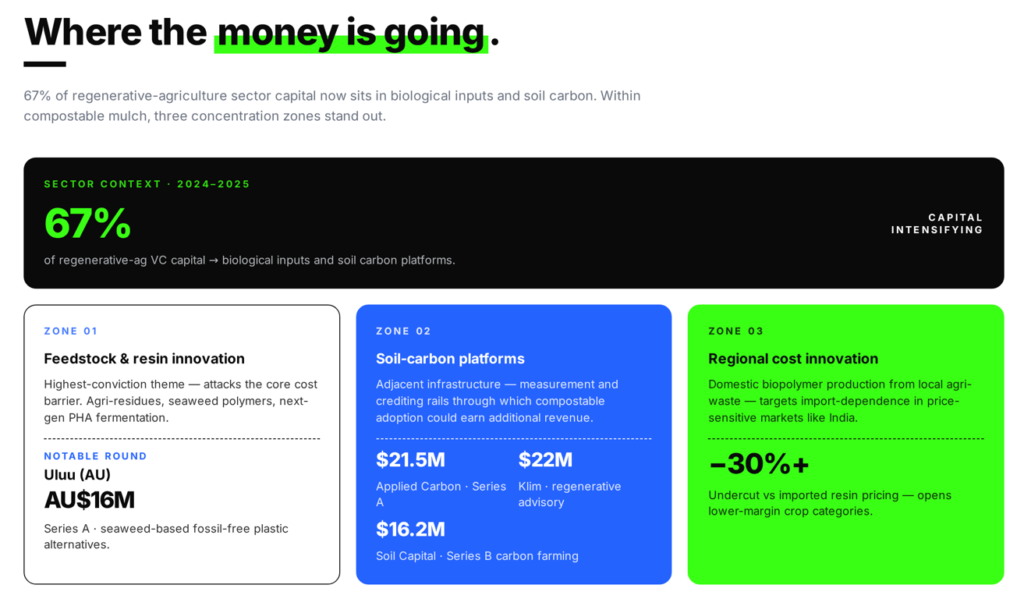

Venture capital activity in the broader regenerative agriculture space has intensified significantly in 2024 and 2025, with biological inputs and soil carbon platforms capturing 67% of total sector capital.

Within the compostable mulch segment specifically, funding is concentrated in three areas.

Feedstock and resin innovation

The highest-conviction investment theme is reducing the cost of biodegradable resins.