Executive Summary

Packaging is changing, and it is changing because it has to.

Governments across Europe, North America, and Asia are restricting or banning conventional single-use plastics.

Brands are under growing pressure from regulators, retailers, and consumers to switch to alternatives that can be composted rather than landfilled.

Compostable plastics processed via thermoforming sit at the centre of this shift.

Thermoforming is the manufacturing process behind the trays, clamshells, lids, and cups that make up a large share of rigid food packaging globally.

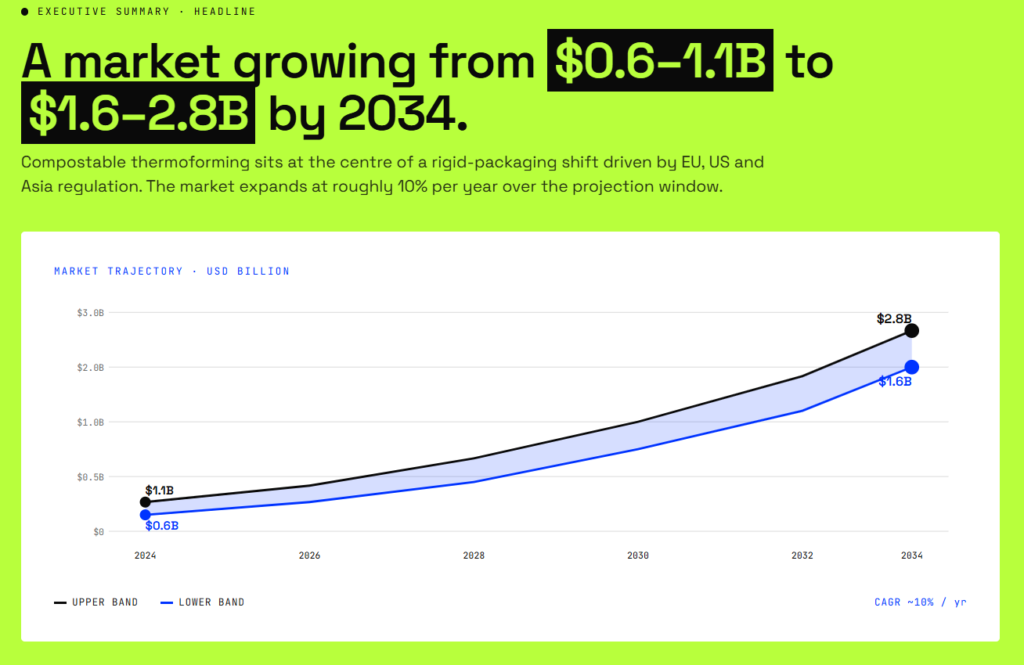

This report estimates that the market for compostable plastics in this application is currently worth USD 0.6 to 1.1 billion and is on track to reach USD 1.6 to 2.8 billion by 2034, growing at approximately 10% per year.

Key Findings

The five points below summarise what the analysis found.

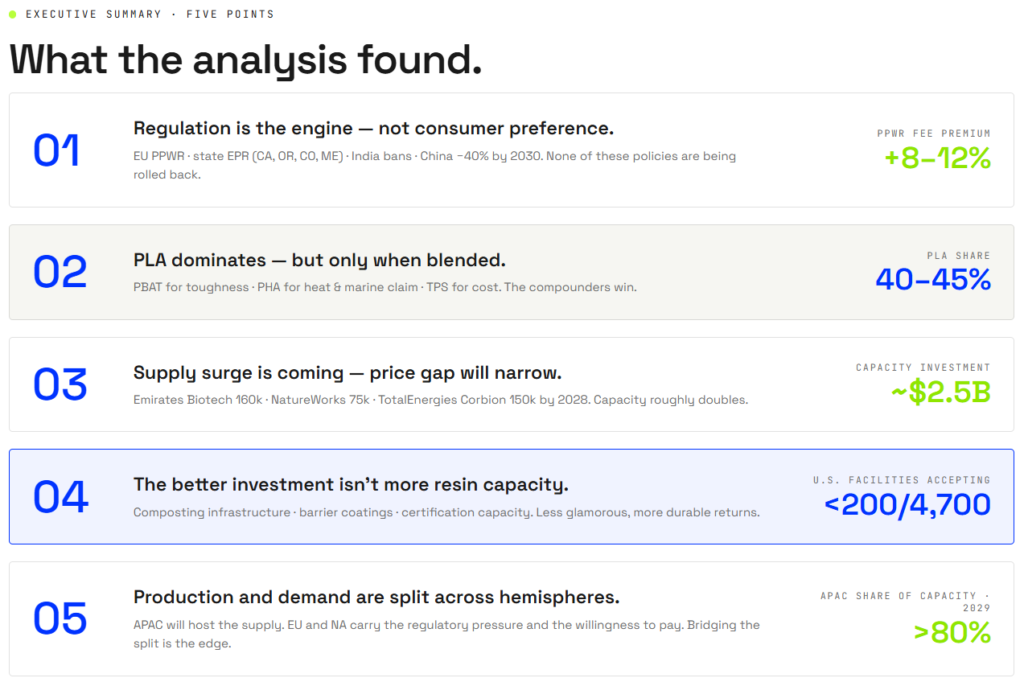

1. Regulation is the engine of the thermoforming-relevant compostable plastics market, and it is propelling the industry forward.

The clearest finding in this report is that policy, not consumer preference, is what is actually moving this market.

The EU’s Packaging and Packaging Waste Regulation (PPWR) requires all packaging sold in Europe to be recyclable or compostable by 2030.

It has already introduced fees that has made non-compostable plastics 8 to 12% more expensive, effective since January 2025.

In the United States, California, Oregon, Colorado, and Maine have each passed Extended Producer Responsibility laws that penalise packaging which contaminates recycling streams.

India has banned a growing list of single-use plastic formats.

China is targeting a 40% reduction in single-use plastics by 2030.

None of these policies are being rolled back. For any manufacturer still using conventional thermoformed plastics, the cost of staying put is rising every year.

For compostable thermoforming suppliers, this is a massive commercial tailwind.

2. PLA is the dominant material today, but requires blending of additives to be functional.

Polylactic Acid (PLA) is the most widely used resin in thermoforming-relevant compostable plastics market, accounting for roughly 40 to 45% of the segment by value.

It is clear, stiff, and compatible with existing thermoforming equipment, which makes it the natural starting point for brands converting from conventional PET or polystyrene.

The problem is that PLA on its own is brittle, loses shape above 55°C, and absorbs moisture during storage. In practice, it works best when blended with other materials.

- PBAT adds toughness and flexibility.

- PHA improves heat resistance and carries marine biodegradability credentials that PLA cannot match.

- Thermoplastic starch reduces cost.

The companies that understand how to formulate these blends for specific applications, whether that is a hot-fill ready-meal tray, a cold-chain produce clamshell, or a peel-seal deli lid, are the ones with the most defensible market positions.

3. A supply surge is coming, and it will change the economics.

More than USD 2.5 billion is currently being invested in new PLA production capacity.

- Emirates Biotech is building a 160,000 tonne per year plant in Abu Dhabi.

- NatureWorks is adding 75,000 tonnes per year in Thailand.

- TotalEnergies Corbion plans to double its Thai facility to 150,000 tonnes per year by 2028.

If these projects complete on schedule, global PLA supply will roughly double within four years.

More supply means lower prices. At the same time, EU carbon pricing is forecast to reach €126 to €150 per tonne by 2030, which raises the cost of producing conventional plastics.

These two forces are moving toward each other. The price gap between compostable and conventional thermoforming resins, currently 2 to 6 times, will narrow.

When it does, brands that have been holding off on switching for cost reasons will have one fewer reason to wait.

4. The better investment is not in building more resin capacity.

Resin production is where most of the capital in this sector has gone.

It is also where the most competition and pricing pressure will become obvious as new capacity comes online.

The underserved parts of the value chain are further downstream.

- Composting infrastructure is the most critical gap: fewer than 200 of roughly 4,700 U.S. composting facilities currently accept certified compostable plastics.

- Barrier coating technology remains an open gap, particularly for moisture and oxygen resistance in food packaging applications.

- Certification and testing capacity is another constraint, with lead times of 6 to 18 months slowing commercial rollout.

These are less glamorous investment targets than a new resin plant, but they offer more durable returns.

5. Production and demand are concentrated in different geographies, and that gap is an opportunity.

Asia-Pacific will host over 80% of global bioplastic production capacity by 2029.

Europe and North America are where the regulatory pressure, the brand commitments, and the willingness to pay a premium for certified compostable packaging exist.

This geographic split between where materials are made and where they are needed creates a real advantage for companies that can bridge it, whether through integrated supply chains, regional conversion assets, or direct relationships with brand owners in high-compliance markets.

About This Report

This report is produced by Ukhi, a company developing compostable biopolymer compounds from agricultural residues.

Our position in the value chain gives us a direct operational view of the market: its material performance requirements, its supply chain dynamics, and the gap between what regulatory timelines demand and what the industry can currently deliver.

The report covers compostable plastics for thermoforming as a defined commercial sub-market.

It is structured to serve two audiences.

- For investors and venture capital firms, it provides market sizing, competitive landscape analysis, and investment opportunity mapping.

- For industry professionals and brand owners, it provides regulatory context, material performance comparisons, and supply chain reference.

Scope and Boundaries

What this report covers:

- Compostable plastic materials processed via thermoforming, including sheet extrusion as a prerequisite step

- The four primary resin families used in this application: PLA, PHA, thermoplastic starch blends, and PBAT

- The full supply chain from resin producers through sheet extruders and converters to brand owners

- Four primary geographies: the European Union, the United States, India, and China

- Market data covering 2024/2025 as the base period, with forward projections to 2030 and 2034

Methodology

The compostable plastics for thermoforming sub-market is not tracked as a discrete category by any major research firm.

Published reports cover either:

- the global thermoforming plastics market (all materials, all applications) or

- the global compostable or biodegradable plastics market (all processing routes).

Neither analysis is able to isolate the overlap.

A further complication is definitional inconsistency.

The terms bioplastics, biodegradable plastics, and compostable plastics describe nested categories that are frequently conflated in market reports, which can inflate the apparent market size by seven to eight times.

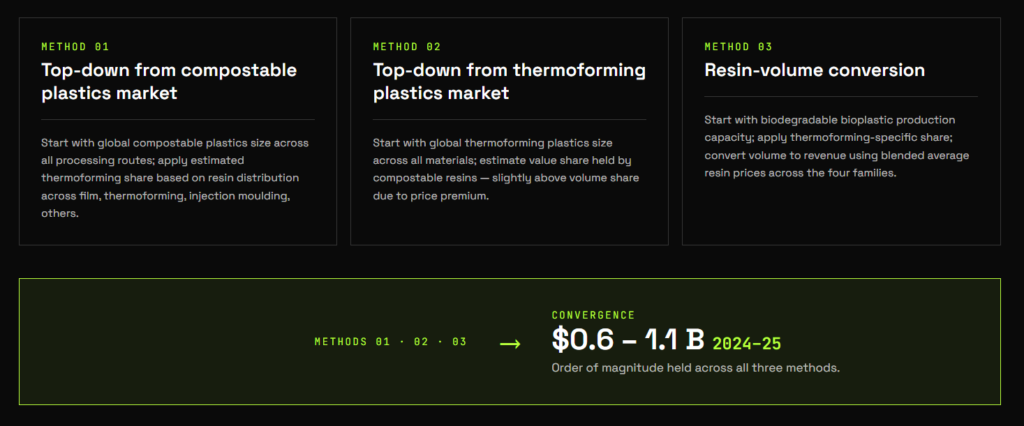

Triangulation across three methods

To arrive at a market size estimate for compostable thermoforming, we apply three independent methods and look for convergence.

Method 1: Top-down from the compostable plastics market.

We start with the published global market size for compostable plastics across all processing routes, drawing on consistent estimates from multiple research firms.

We then apply an estimated thermoforming share based on the known distribution of compostable resin demand across the main processing routes:

- film extrusion,

- thermoforming,

- injection moulding, and

- others.

Because thermoforming accounts for a meaningful but not dominant share of total compostable resin consumption, this produces a sub-market estimate that is a fraction of the parent figure.

Method 2: Top-down from the thermoforming plastics market.

We start from the other direction, using the published global market size for thermoforming plastics across all materials.

We then estimate the current value share held by compostable resins within that total.

This share is estimated slightly above the equivalent volume share because compostable resins carry a price premium over conventional alternatives, which means their revenue contribution is proportionally larger than their tonnage contribution.

Method 3: Resin-volume conversion.

Rather than starting from market value, this method starts from physical production capacity.

We take published estimates of total biodegradable bioplastic production capacity, apply a thermoforming-specific share based on the known dominance of film extrusion in compostable resin consumption, and then convert the resulting volume estimate into a revenue figure using blended average resin prices across the four material families covered in this report.

All three methods produce overlapping estimates, and it is this convergence across different starting assumptions that gives us reasonable confidence in the order of magnitude of the result.

1. What Are Compostable Plastics for Thermoforming?

Understanding what thermoforming is, what makes a plastic genuinely compostable, and which materials are commercially viable for this application is essential context for evaluating the market opportunity.

1.1 What Is Thermoforming?

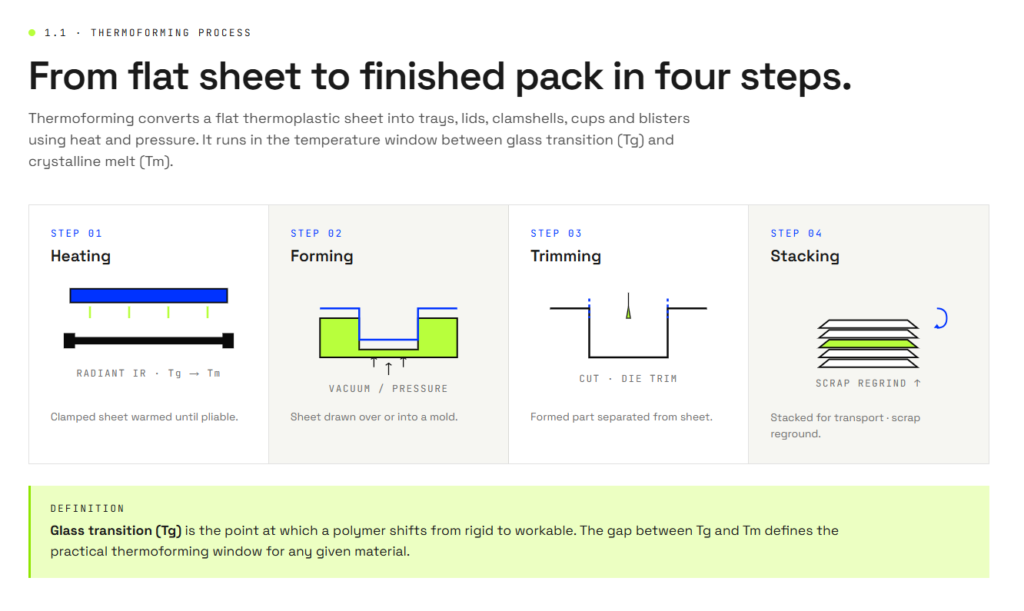

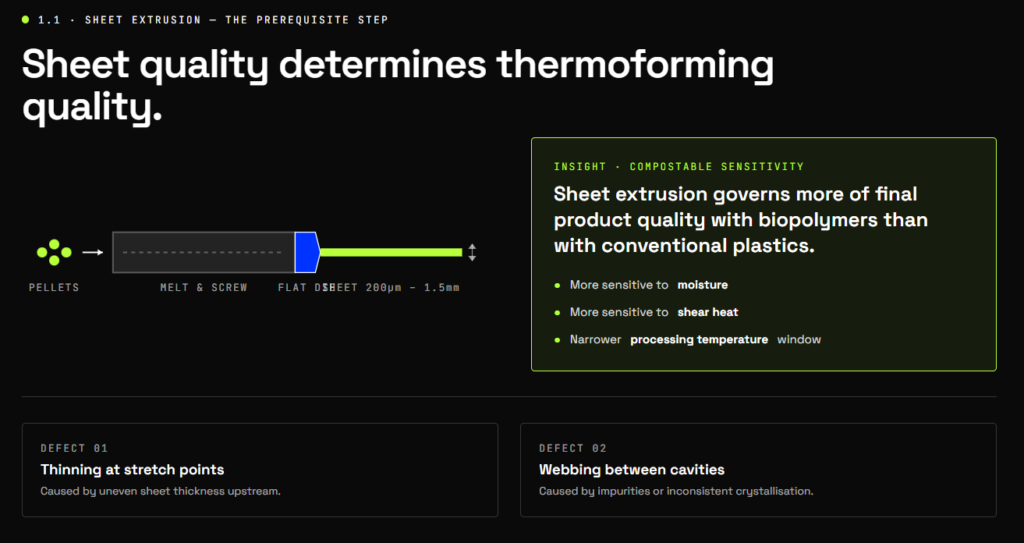

Thermoforming is a manufacturing process that converts a flat thermoplastic sheet into a three-dimensional shape using heat and pressure.

It is one of the most widely used processes in rigid packaging production, and covers formats including trays, lids, clamshells, cups, and blisters.

How the Thermoforming Process Works

Thermoforming works in the temperature range between a material’s glass transition temperature (Tg) and its crystalline melting point (Tm).

In this range, the plastic becomes pliable enough to stretch and conform to a mold without tearing or losing structural integrity.

Definition: Glass transition temperature (Tg) is the point at which a polymer shifts from a rigid, brittle state to a softer, workable one.

The gap between Tg and Tm defines the practical thermoforming window for any given material.

The industrial thermoforming-based production cycle follows four steps:

- Heating: A clamped plastic sheet is heated, typically via radiant infrared heaters, until it reaches the required level of pliability.

- Forming: The softened sheet is shaped over or into a mold. Vacuum forming uses atmospheric pressure to draw the sheet against the mold surface. Pressure forming uses compressed air, which delivers higher precision and sharper detail.

- Trimming: The formed part is cut away from the surrounding sheet.

- Stacking: Finished products are organized for transport, and excess trim material is typically ground down and reprocessed.

The Role of Sheet Extrusion in the Thermoforming Process

Before thermoforming can take place, raw resin pellets must be converted into a continuous flat sheet through sheet extrusion.

In this process, resin is melted and pushed through a flat die to produce a roll or flat sheet at a specified thickness, typically between 200 micrometres and 1.5 mm for packaging applications.

Sheet extrusion is a critical quality control point.

Uneven thickness or impurities introduced at this stage lead directly to defects during forming, including thinning at stretch points and webbing between mold cavities.

Insight: In compostable thermoforming, the sheet extrusion step governs more of the final product quality than it does with conventional plastics.

Biopolymers are more sensitive to moisture, shear heat, and processing temperature than conventional plastics, which means that the extrusion parameters must be tightly controlled to preserve material integrity before thermoforming begins.

1.2 What Are Compostable Plastics?

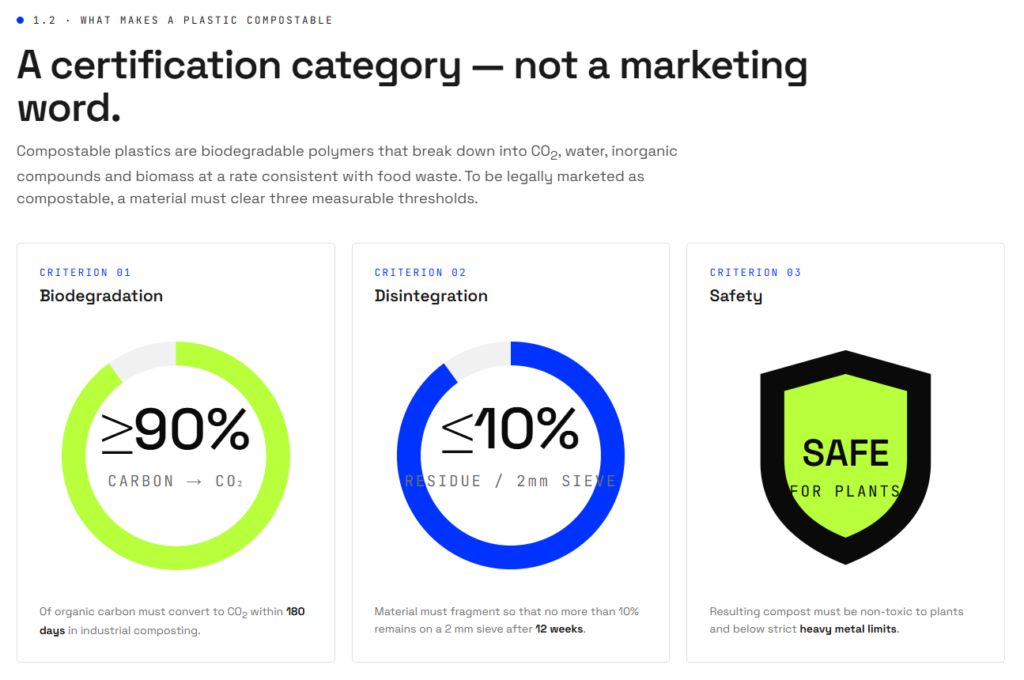

Compostable plastics are a defined subset of biodegradable polymers that break down into carbon dioxide, water, inorganic compounds, and biomass at a rate consistent with organic materials such as food waste.

The term is not a general marketing descriptor.

It is a technical certification category with specific, measurable criteria.

To be legally marketed as compostable, a material must meet international standards including EN 13432 in Europe and ASTM D6400 in North America.

The core requirements under these standards are:

- Biodegradation: A minimum of 90% of organic carbon must convert to CO2 within 180 days in an industrial composting environment.

- Disintegration: The material must physically fragment so that no more than 10% remains on a 2mm sieve after 12 weeks.

- Safety: The resulting compost must be non-toxic to plants and remain within strict heavy metal concentration limits.

1.3 Types of Compostable Plastics Suitable for Thermoforming

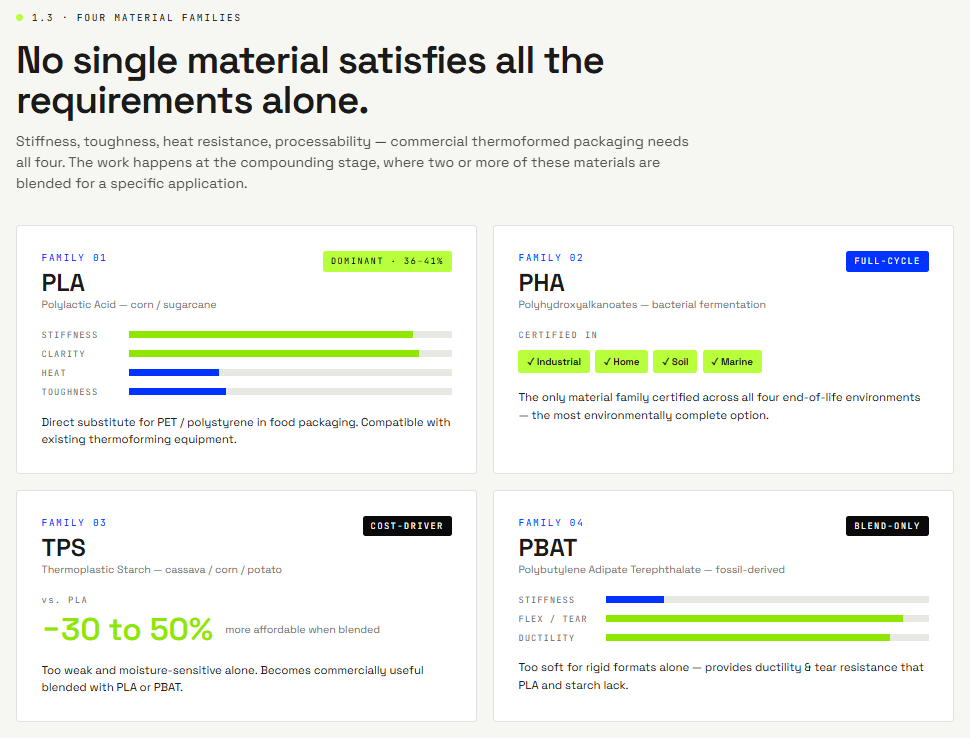

Four material families dominate the landscape of commercial compostable plastics for thermoforming: PLA, PHA, thermoplastic starch blends, and PBAT.

They are rarely used in isolation.

The commercial reality of this sector is that blending two or more of these materials is typically required to achieve the combination of stiffness, toughness, heat resistance, and processability that a finished thermoformed product demands.

1. Polylactic Acid (PLA)

PLA is the dominant material in compostable thermoforming, holding approximately 36 to 41% of the market.

Derived from fermented corn starch or sugarcane, it offers high stiffness, clarity, and gloss, making it a direct substitute for PET and polystyrene in food packaging applications.

2. Polyhydroxyalkanoates (PHA)

PHAs are produced through bacterial fermentation and are the only material family certified for composting across all four environments: industrial, home, soil, and marine.

This makes them the most environmentally complete option available.

3. Thermoplastic Starch Blends (TPS)

Thermoplastic starch is produced by plasticizing native starch from crops including cassava, corn, and potato.

On its own, starch is too weak and moisture-sensitive for most packaging applications.

When blended with PLA or PBAT, however, it becomes commercially useful and is consistently 30 to 50% more affordable than PLA.

4. Polybutylene Adipate Terephthalate (PBAT)

PBAT is a fossil-derived but certified compostable polyester.

It is rarely used alone in thermoforming because its high flexibility makes it too soft for rigid formats.

Its commercial importance lies entirely in its role as a blend component.

PBAT provides the ductility and tear resistance that stiffer biopolymers like PLA and starch lack, which makes it essential for producing compostable thermoformed packaging that can withstand the mechanical stresses of filling lines, transport, and consumer handling.

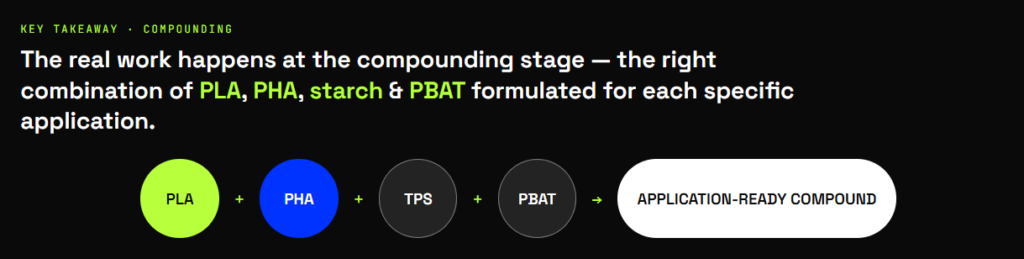

Key Takeaway: No single compostable material satisfies all the performance requirements of thermoformed packaging on its own.

The real work in this sector happens at the compounding stage, where the right combination of PLA, PHA, starch, and PBAT is formulated for each specific application.

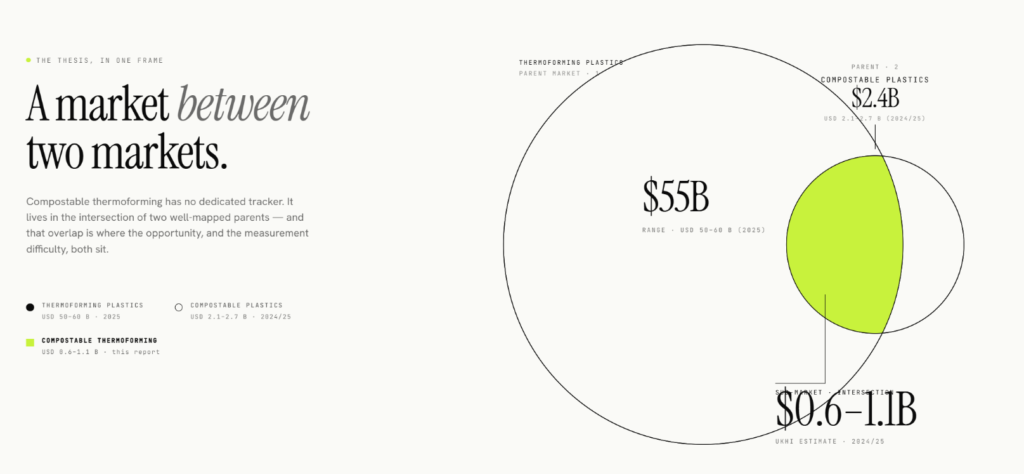

2. Compostable Plastics for Thermoforming: Market Definition and Sizing

The market of compostable plastics for thermoforming market exists at the intersection of two larger, well-documented industries:

- the global thermoforming plastics market and

- the global compostable plastics market.

Both are tracked individually by multiple research firms.

However, no single market report isolates their overlap.

Sizing this sub-market therefore requires working inward from both parent markets and cross-checking against resin volumes.

This chapter sets out how we arrive at a market size estimate, presents the headline figures, and breaks down the opportunity by region.

2.1 Approaches to Sizing the Compostable Thermoforming Market

Before applying any sizing method, there is an important data quality issue to address.

The published estimates for the thermoforming plastics market vary dramatically across research firms, and the reason is definitional scope.

Thermoforming plastics market size estimates for 2025 range from roughly $12 billion to $60 billion depending on the source:

-

Fortune Business Insights: Values the global market at USD 60.51 billion in 2025, projecting USD 120.05 billion by 2034 at a CAGR of 7.91%.

This appears to capture the full value of thermoformed packaging goods across all materials and end uses. - Polaris Market Research: Estimated the market at USD 52.16 billion in 2023, forecasting USD 77.78 billion by 2032 at a CAGR of 4.6%.

- Mordor Intelligence: Projects a 2026 market size of USD 49.55 billion, growing to USD 61.77 billion by 2031 at a CAGR of 4.51%.

- Research and Markets (via GlobeNewswire): Focuses on “thermoformed plastics” rather than thermoformed packaging, estimating growth from USD 15.98 billion in 2024 to USD 24.61 billion by 2030 at a CAGR of 7.39%.

- Coherent Market Insights: Provides a lower estimate of USD 12.5 billion in 2026, reaching USD 23.2 billion by 2033 at a CAGR of 9.2%.

Insight: The roughly fivefold gap between the highest and lowest figures is not an error.

The $50 to $60 billion estimates capture the full converted-goods value of thermoformed packaging (the finished tray on the shelf).

The $12 to $16 billion estimates likely capture only the plastics material or resin value, or a narrower product sub-segment.

When we estimate what share of the thermoforming market has converted to compostable materials below, we use the broader $50 to $60 billion bracket as the denominator, because it is more comparable to how the compostable plastics market is reported (at converted-goods value, not raw resin value).

The compostable plastics market size data is more internally consistent, but a different problem arises: the terms “compostable,” “biodegradable,” and “bioplastics” end up being used loosely, although they are not interchangeable.

- Grand View Research: Global compostable plastics market valued at USD 2.74 billion in 2024, forecast to reach USD 5.12 billion by 2030 at a CAGR of 10.3%.

- Spherical Insights: Valued at USD 2.17 billion in 2024, forecasting USD 6.32 billion by 2035 at a CAGR of 10.2%.

- Future Market Insights: Projects growth from USD 2.1 billion in 2025 to USD 3.5 billion by 2035 at a CAGR of 5.2%.

- Towards Packaging: Projects the broader biodegradable plastics market at USD 16 billion in 2025, rising to USD 107.3 billion by 2035.

- Towards Chemical and Materials Consulting: Reports on the broadest category, bioplastics, at USD 18.4 billion in 2025, growing to USD 44.8 billion by 2034.

Definition: Compostable vs. biodegradable vs. bioplastics.

These three terms describe nested categories, not synonyms.

- Bioplastics is the broadest label, covering any plastic that is bio-based, biodegradable, or both.

- Biodegradable plastics is a subset: plastics that will eventually break down biologically, though this may require specific conditions and timescales that vary widely.

- Compostable plastics is the narrowest and most regulated category: plastics that are certified to break down within a defined timeframe under industrial or home composting conditions, meeting standards such as EN 13432 in Europe or ASTM D6400 in the United States.

For this report, we use the compostable plastics figures specifically, not the broader biodegradable or bioplastics numbers.

Three sources, Grand View Research, Spherical Insights, and Future Market Insights, converge on a 2024/2025 market size of USD 2.1 to 2.7 billion.

This is our base for all sizing calculations that follow.

Three methods for estimating the compostable thermoforming sub-market

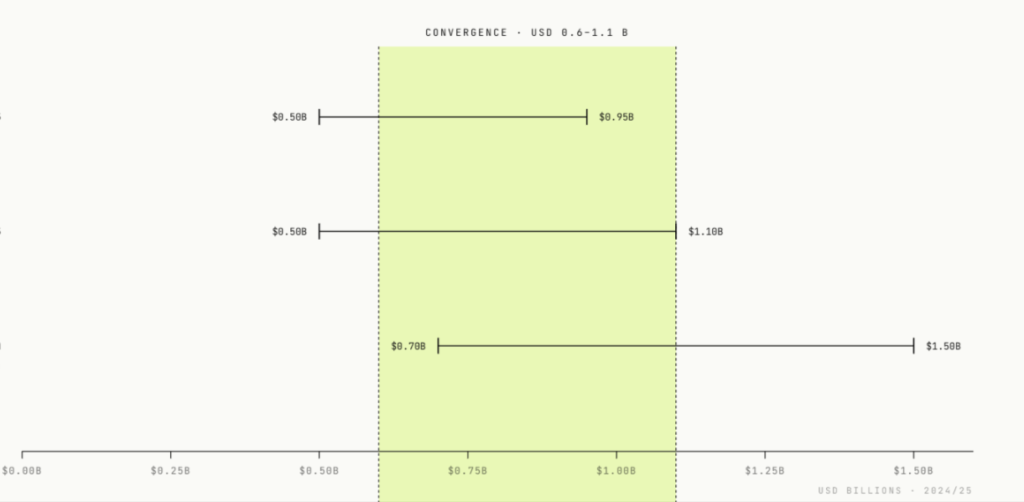

Method 1: Top-down from the compostable plastics market

We start with the global compostable plastics market at USD 2.1 to 2.7 billion (2024/2025) and estimate what share is processed via thermoforming.

Compostable resins reach finished products through four main processing routes:

- film extrusion (bags, wraps, agricultural mulch),

- thermoforming (trays, clamshells, cups, lids),

- injection moulding (cutlery, capsules, closures), and

- fibre spinning or other methods.

Thermoforming accounts for an estimated 25 to 35% of compostable plastics by value.

This share is lower than injection moulding’s (which we estimated at 35 to 45%) because a large volume of compostable resin goes into film applications (particularly PBAT-based compostable bags and starch-blend films), which do not pass through thermoforming.

However, thermoforming is the primary processing route for PLA, the leading compostable resin, in its highest-volume application: rigid food packaging.

Result: approximately USD 0.5 to 0.95 billion (2024/2025).

Method 2: Top-down from the thermoforming market

Starting from the other parent, the thermoforming plastics market is roughly USD 50 to 60 billion in 2025.

What share is compostable?

According to Mordor Intelligence, polypropylene alone held 35.67% of the thermoformed plastics market in 2025.

However, compostable resins still represent a small fraction of total thermoforming.

We estimate their current value share at 1.0 to 1.8%, which is slightly above their volume share because compostable resins carry a price premium of roughly 35% over conventional alternatives like polypropylene.

Result: approximately USD 0.5 to 1.1 billion (2025).

Method 3: Resin-volume conversion

European Bioplastics and nova-Institute reported total biodegradable bioplastics production capacity at approximately 1.4 million tonnes in 2025.

We estimate that 20 to 30% of that volume is processed through thermoforming (a lower share than by value, because film extrusion dominates on a tonnage basis and thermoforming generates significant trim scrap).

This gives a usable volume of roughly 280,000 to 420,000 tonnes.

Multiplying by a blended average resin price of USD 2.50 to 3.50 per kilogram (PLA forms the bulk at around USD 2.00 to 2.50/kg, while PHA pulls the average upward at USD 5 to 8/kg) produces a revenue estimate.

Result: approximately USD 0.7 to 1.5 billion.

Convergence range

All three methods produce overlapping estimates centred on USD 0.6 to 1.1 billion for 2024/2025.

This convergence across different starting assumptions gives reasonable confidence in the order of magnitude, even though a precise point estimate is not possible.

2.2 Compostable Plastics for Thermoforming: Market Size and Forecast

Based on the triangulation above, we estimate the global compostable thermoforming market at USD 0.6 to 1.1 billion in 2024/2025.

For the compostable thermoforming market forecast, we apply the compostable plastics growth rate (CAGR of approximately 10%, the consensus across Grand View Research and Spherical Insights) rather than the general thermoforming growth rate (CAGR of 5 to 7%).

The rationale is that growth in this sub-market is driven primarily by material substitution (compostable replacing conventional) rather than by expansion of thermoforming as a process.

- 2030 projection: USD 1.1 to 1.8 billion (at 10% CAGR from the range midpoint).

- 2034 projection: USD 1.4 to 2.6 billion.

There is a reasonable case that the compostable thermoforming segment will outpace even the broader compostable plastics CAGR.

Single-use plastic bans disproportionately target thermoformed products: expanded polystyrene food containers, thin-gauge trays, and non-recyclable clamshells are among the first items regulators restrict.

2.3 Compostable Thermoforming Market: Regional Analysis

Europe: Compostable Plastics Market Share Leader

Europe is the most mature market for compostable thermoformed packaging, and the global leader in adoption by revenue share.

The region accounted for 43.57% of the global compostable plastics market in 2023 (Grand View Research).

Within Europe, Germany leads the thermoform packaging segment with approximately 15% of the European share, supported by the highest municipal waste processing rate in the EU at 66%.

Italy has pioneered integrated models that link biorefineries directly to agricultural and municipal composting networks, thereby providing the end-of-life infrastructure that makes compostable packaging viable at scale.

Applying Europe’s 43% share of the global compostable plastics market to our overall sub-market estimate gives an implied regional figure for compostable thermoforming.

Compostable plastics for thermoforming — Market Size (Europe): Roughly USD 0.26 to 0.47 billion (2024/2025)

North America: Fastest-Growing Compostable Plastics Market

North America held 34.35% of the global thermoform packaging market in 2025, valued at USD 20.78 billion (Fortune Business Insights).

The U.S. rigid thermoform plastic packaging segment alone is valued at USD 13.35 billion in 2025.

However, compostable penetration remains lower than in Europe.

The U.S. compostable plastics market is expected to reach USD 811.7 million by 2030 at a CAGR of 10.5% (Grand View Research), making it the fastest-growing national market by rate.

This figure covers all compostable plastics, not only the ones used in thermoforming.

So, applying our estimated thermoforming share suggests a sub-market of roughly USD 0.15 to 0.33 billion (2024/2025).

Compostable plastics for thermoforming — Market Size (North America): USD 0.15 to 0.33 billion (2024/2025).

Asia-Pacific: Global Bioplastics Production Hub

Asia-Pacific held 39.96% of the global thermoformed plastics market in 2025 (Mordor Intelligence), growing at the fastest regional CAGR of 5.94%.

In production capacity for compostable resins, the region is dominant: it is projected to host over 80% of global bioplastics capacity by 2029.

However, there is an important distinction between production and consumption.

Asia-Pacific manufactures compostable resin at scale:

- China’s installed PLA and PBAT capacity reached 1.5 million metric tonnes by 2023.

- Thailand hosts NatureWorks’ 75,000-tonne integrated PLA facility.

However, much of this output is exported to Europe and North America, where the demand premium exists.

Regional consumption of compostable thermoformed products is currently lower, placing Asia-Pacific’s share of the demand-side market at an estimated 15 to 20%, or roughly USD 0.09 to 0.22 billion (2024/2025).

Compostable plastics for thermoforming — Market Size (Asia-Pacific): USD 0.09 to 0.22 billion (2024/2025)

3. Compostable Plastics for Thermoforming: Market by Material

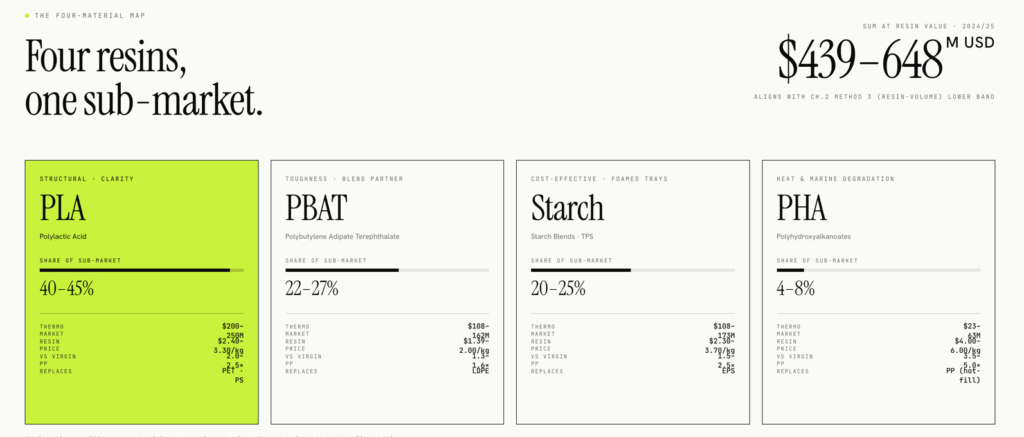

Four compostable resins account for the vast majority of thermoformed compostable packaging produced today: PLA, PBAT, starch blends, and PHA.

This chapter profiles each material’s thermoforming behaviour, cost position, and estimated market size within the thermoforming segment.

A note on how we size each material

No published source isolates compostable resin revenues specifically for thermoforming.

To arrive at per-material estimates, we start from each material’s total global market value (all applications), then apply a thermoforming share based on what proportion of that material’s demand flows through sheet extrusion and thermoforming rather than film, injection moulding, or other routes.

Note: For PLA, industry data indicates that sheet-grade PLA for thermoforming exceeds 100,000 tonnes annually, representing roughly 12% of total PLA demand.

For the remaining materials, we estimate thermoforming shares from their known end-use profiles.

All figures are at resin or compound value, not finished-goods value.

3.1 PLA (Polylactic Acid) for Thermoforming: Properties, Cost, and Market Size

3.1.1 PLA Properties and Thermoforming Behaviour

Polylactic acid (PLA) is the dominant resin in compostable thermoforming because it offers high stiffness and optical clarity comparable to conventional PET and polystyrene (PS).

In practical terms, a PLA clamshell looks and feels similar to the petroleum-based version it replaces.

However, PLA thermoforming demands tighter process control than conventional plastics:

-

Narrow forming window: PLA requires temperature control within a band of just 5 to 10°C.

If the sheet is too cold, it fractures during stretching.

If too hot, it becomes overly soft and sticks to the mold.

By comparison, PET and PP are far more forgiving. -

Low melt strength: During heating, PLA sags more than polypropylene or high-impact polystyrene.

This causes localized thinning and uneven wall thickness in the finished part.

Processors have to add chain-extending additives to counteract this. -

Deep-draw limitations: For products like cups and deep trays, plug-assist thermoforming is nearly universal.

A mechanical plug pre-stretches the material into the mold cavity before vacuum is applied, to distribute it more evenly. -

Low heat resistance: Standard PLA has a glass transition temperature of just 55 to 65°C, meaning it softens and deforms in warm conditions.

This limits it to cold-fill applications unless processors use “heat-setting,” which involves forming in a hot mold (90 to 110°C) to induce crystallinity and raise the usable temperature.

Stat: Pure PLA has an elongation at break of just 2% to 10%, making it inherently brittle.

This is the primary reason it is frequently blended with PBAT (see Section 3.4).

PLA also requires strict pre-drying (60 to 80°C for 4 to 6 hours, to reduce moisture below 250 ppm) before processing, because it absorbs moisture from the air that causes molecular degradation during sheet extrusion.

On end-of-life, PLA is certified for industrial composting under standards such as EN 13432 and ASTM D6400, biodegrading within 90 to 180 days under controlled thermophilic conditions (above 58°C).

It does not break down readily in landfill or marine environments.

3.1.2 PLA Cost

PLA cost remains the principal barrier to broader adoption.

In 2025, standard-grade PLA traded at roughly USD 2.40 to 3.30 per kg, which is approximately 2.0 to 2.5 times the price of virgin polypropylene (USD 1.00 to 1.50/kg).

High-heat nucleated compounds, required for hot-fill applications, are more expensive at USD 2.70 to 3.80/kg.

Regional pricing varies a lot.

- Northeast Asia offers the lowest spot prices at approximately USD 2.42/kg, which is a result of proximity to large-scale production in China and Thailand.

- European delivered prices (CFR Hamburg) are at around USD 2.72/kg.

Insight: The cost gap between PLA and conventional thermoforming resins like PET (USD 1.00 to 1.40/kg) and PS (USD 1.10 to 1.60/kg) runs to roughly 70 to 130%.

This is narrower than it was five years ago, but still material enough to make compostable thermoforming a regulation-driven market rather than a cost-driven one.

Brands switch to PLA because they must, not because it saves money.

3.1.3 PLA Market Size for Thermoforming

The total PLA market size was valued at approximately USD 1.2 billion in 2025 across all applications and processing routes.

PLA holds a 65.92% share of the biodegradable plastic packaging market.

Within this, sheet-grade PLA used specifically for thermoformed products (trays, lids, clamshells, blister packs) accounts for an estimated 12% of total global PLA demand by volume, exceeding 100,000 tonnes annually.

At prevailing prices, this translates to an estimated PLA thermoforming market of roughly USD 200 to 250 million at resin value (2024/2025).

This makes PLA the largest single material in compostable thermoforming, representing an estimated 40 to 45% of the segment.

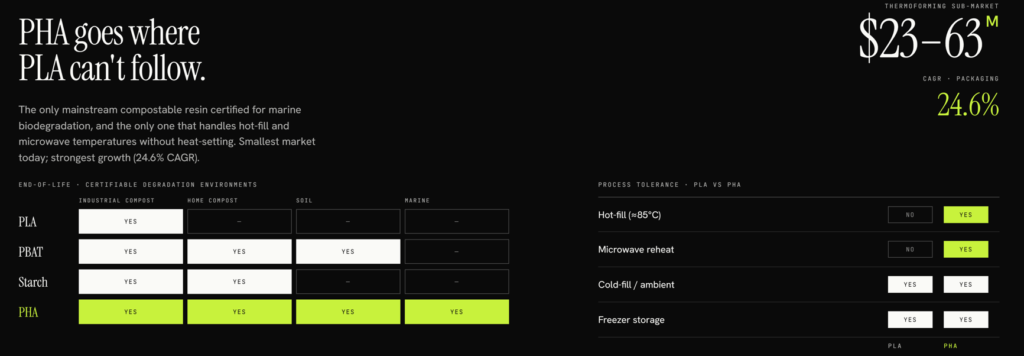

3.2 PHA (Polyhydroxyalkanoates) for Thermoforming: Properties, Cost, and Market Size

3.2.1 PHA Properties and Thermoforming Behaviour

Unlike PLA and PBAT, PHA is genuinely biosynthesised by microorganisms, not chemically polymerised from bio-derived monomers.

This gives it a unique environmental credential: certain PHA grades biodegrade in soil, home compost, and marine environments, making PHA one of the few plastics to pass marine biodegradation tests (such as TUV Austria “OK biodegradable MARINE”).

PHA’s thermoforming behaviour is technically demanding:

-

Thermal sensitivity: PHAs, especially PHB (the most common short-chain variant), degrade rapidly at temperatures near their melting point.

Overheating by even a few degrees causes molecular weight loss and visible yellowing of the part. -

Slow crystallisation: After forming, PHA remains soft and tacky for longer than PLA or PP.

Processors must add nucleating agents to speed solidification and prevent deformation during part ejection.

Without these, cycle times are unacceptably long for high-volume production. -

Blending is essential: Pure PHBV (a common PHA variant) has low melt strength and sags during heating.

Blending it with more ductile PHA types such as PHBH extends the processing window by up to 7 seconds and improves mold reproduction.

Definition: PHAs are classified by chain length.

- Short-chain-length (SCL) types like PHB are stiff and crystalline with high melting points (175 to 180°C).

- Medium-chain-length (MCL) types like PHBH are more flexible and tough.

Commercial thermoforming compounds typically blend both to balance rigidity with processability.

PHA’s key advantage over PLA in thermoforming is heat resistance.

Certain PHA grades can handle hot-fill temperatures and microwave use without the heat-setting step that PLA requires, which makes them suitable for ready-meal trays and coffee pods.

3.2.2 PHA Cost

PHA cost is the highest of any compostable resin in common use.

Packaging and industrial grades trade at roughly USD 4.00 to 6.00/kg in 2025, which is 3.5 to 5 times the price of virgin polypropylene.

Medical-grade specialty PHA compounds sit dramatically higher at USD 20 to 50/kg, though these are irrelevant to the packaging market.

The cost premium reflects low production volumes and the complexity of the fermentation process compared to chemical synthesis.

As capacity scales, prices are projected to fall, but PHA will remain the most expensive mainstream compostable thermoforming resin for the foreseeable future.

3.2.3 PHA Market Size for Thermoforming

The total PHA market remains small, estimated at roughly USD 150 to 250 million in 2024/2025 across all applications.

However, PHA market growth is the strongest in the segment at a reported 24.62% CAGR in packaging applications.

PHA’s thermoforming applications (rigid trays, coffee pods, pharmaceutical blisters) account for an estimated 15 to 25% of total PHA demand.

The remainder goes to coatings, films, injection moulding, and specialty applications.

This places the PHA thermoforming market at roughly USD 23 to 63 million (2024/2025), which represents approximately 4 to 8% of total compostable thermoforming.

Insight: PHA’s small absolute size understates its strategic importance.

It is the only compostable resin that credibly addresses hot-fill and marine-degradation requirements, two gaps that PLA cannot fill.

For investors, PHA capacity investments represent a bet on tightening end-of-life regulations rather than near-term volume.

Cross-Material Comparison

Table 1: Material Properties, Thermoforming Processing Parameters, and Comparison

| Parameter | PLA | PHA | Starch Blends | PBAT |

|---|---|---|---|---|

| Primary role in thermoforming | Structural resin (rigidity and clarity) | High-performance alternative (heat and marine degradation) | Cost-effective substitute (foamed trays and dishes) | Toughness modifier (blend component) |

| Standalone or blend | Both; often blended with PBAT | Blended (SCL + MCL types, or with PLA) | Always blended (with PLA, PBAT, or PHA) | Almost always a blend component |

| Glass transition temperature (Tg) | 55 to 65°C | Varies by grade; SCL types: high crystallinity, Tm 175 to 180°C | Not applicable (governed by blend partner) | Approximately minus 30°C |

| Thermoforming temperature range | Narrow; 5 to 10°C control band required | Narrow; degrades rapidly if overheated by even a few degrees | 100 to 170°C; carbonisation above 180°C | Broad; high melt strength allows wider processing window |

| Melt strength | Low; sagging in oven is common; chain extenders often added | Low for pure PHBV; improved significantly by blending with PHBH | Low to moderate; improved by adding PBAT | High; resists sagging and maintains even wall thickness |

| Elongation at break | 2 to 10% (brittle) | Varies by grade; SCL types are brittle, MCL types are ductile | Dependent on blend ratio and moisture content | 500 to 800% (extremely ductile) |

| Deep-draw capability | Limited; plug-assist forming nearly universal for cups and deep trays | Moderate; blending extends forming window by up to 7 seconds | Limited; requires thicker starting gauge to prevent blowouts | Strong; enables snap-fit lids and living hinges |

| Heat resistance of finished part | Low (softens above 55 to 65°C) unless heat-set in hot mould at 90 to 110°C | Good; certain grades handle hot-fill and microwave temperatures without heat-setting | Low to moderate; governed by blend partner | Low; not used standalone for rigid heat-resistant parts |

| Moisture sensitivity during processing | High; requires pre-drying to below 250 ppm (60 to 80°C, 4 to 6 hours) | Moderate | Critical; too wet causes bubbles, too dry causes cracking | Low |

| Mould shrinkage | Low | Moderate; slow crystallisation requires nucleating agents | Moderate to high | Higher than PLA (1.0 to 1.5%); requires precise cooling |

| Cold-temperature performance | Becomes more brittle | Varies by grade | Poor; becomes brittle | Excellent; remains flexible in freezer environments |

| Optical clarity | High (comparable to PET) | Lower; can yellow if overprocessed | Low (typically opaque) | Moderate; translucent |

| Energy requirement vs conventional plastics | Comparable to PET/PS processing | Higher (slower cycles, nucleating agents needed) | 10 to 15% lower per cycle than PET/PP | Comparable |

| Key processing challenge | Narrow thermal window and brittleness | Thermal degradation sensitivity and slow crystallisation | Moisture management and sheet thinning at high draw ratios | Cannot be used alone; must be compounded with rigid resin |

| Composting certification | Industrial only (EN 13432, ASTM D6400); 90 to 180 days | Industrial, home, soil, and marine (grade-dependent) | Industrial; 90% biodegradation within 180 days | Industrial and soil; higher soil degradation activity than PLA |

| Conventional plastic it most directly replaces | PET and PS (clear rigid packaging) | PP (hot-fill trays, microwaveable containers) | Expanded PS / EPS (foamed trays and dishes) | LDPE (as a flexibility component in blends) |

Table 2: Global Market Size Summary by Material (2024/2025)

| Metric | PLA | PHA | Starch Blends | PBAT | Total |

|---|---|---|---|---|---|

| Total market size (all applications) | USD 1,210M (2025) | USD 150 to 250M (est.) | USD 2,160M (2024) | USD 1,350M (2024) | USD 4,870 to 4,970M |

| Share of global bioplastic production capacity | 17.9% | Small but expanding (capacity +166.7% by 2026) | 20.7% (largest single share) | 4.5% | — |

| Estimated thermoforming share of material demand | ~12% (direct data: sheet-grade PLA volume) | ~15 to 25% (rigid trays, pods, blisters) | ~5 to 8% (foamed trays and pressed dishes) | ~8 to 12% (as blend component in PBAT/PLA and PBAT/starch compounds) | — |

| Basis for thermoforming share estimate | Direct industry data point: >100,000 tonnes/year of sheet-grade PLA for thermoforming | Estimated from end-use profile; rigid formats are a significant share of PHA’s small total market | Estimated from end-use profile; film dominates, thermoforming is secondary | Estimated from end-use profile; film is primary, thermoforming via blends is secondary | — |

| Thermoforming market size (resin value) | USD 200 to 250M | USD 23 to 63M | USD 108 to 173M | USD 108 to 162M | USD 439 to 648M |

| Share of compostable thermoforming segment | ~40 to 45% | ~4 to 8% | ~20 to 25% | ~22 to 27% | 100% |

| Spot price 2025 (USD/kg) | 2.40 to 3.30 (standard); 2.70 to 3.80 (high-heat) | 4.00 to 6.00 (packaging grade) | 2.30 to 3.70 | 1.39 to 1.44 (China FOB); 1.83 to 2.00 (European CFR) | — |

| Cost multiplier vs virgin PP | 2.0 to 2.5x | 3.5 to 5.0x | 1.5 to 2.5x | 1.3x (China); 1.5 to 1.6x (Europe) | — |

| Growth outlook | Steady; anchored by regulation-driven PET/PS substitution | Fastest-growing (24.62% CAGR in packaging) | Moderate (packaging segment at 9.88% CAGR) | Strong volume growth; Chinese overcapacity depressing prices | — |

4. Compostable Plastics for Thermoforming: Demand Drivers and Regulatory Landscape

The demand for compostable plastics in thermoforming is accelerating across all major markets.

This chapter maps the forces behind that growth and the regulatory frameworks shaping how manufacturers, brands, and investors need to respond.

The single most important structural feature of this market is the regulatory divide between Europe and the rest of the world.

In North America, Asia-Pacific, and Emerging Markets, PLA is unrestricted and accounts for 88% or more of polymer straw sales.

In Europe, PLA is banned in both the EU and the UK, making PHA the largest polymer straw material and creating a uniquely diversified material mix.

This regulatory divide shapes every aspect of the material landscape covered in this chapter: pricing, demand, supply chain development, and investment flows.

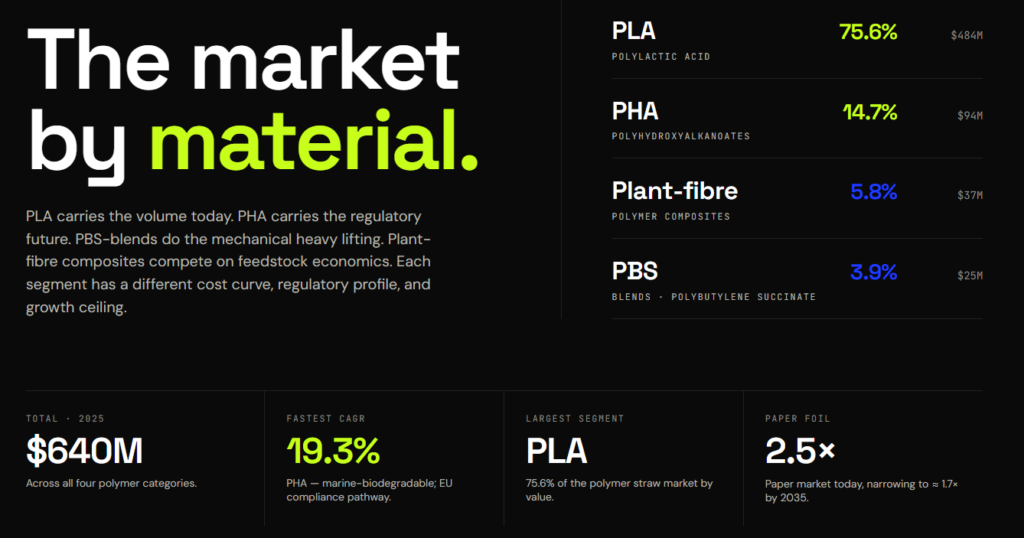

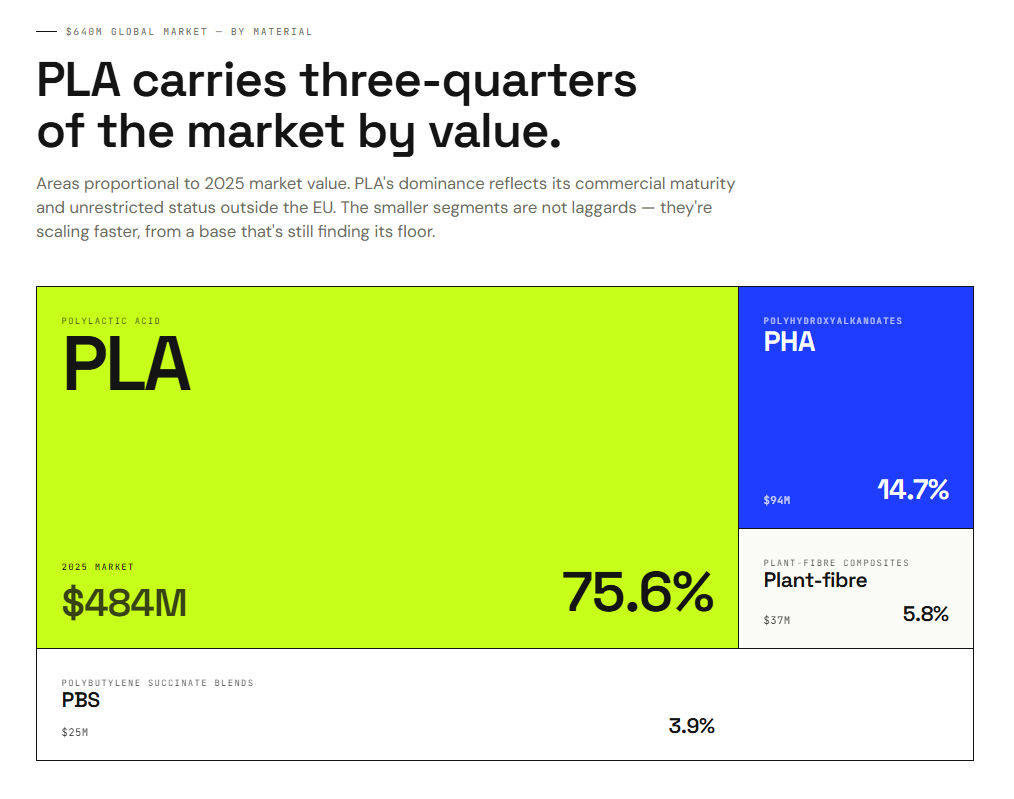

| Material | Global Market (2025) | Share | CAGR (2025 to 2035) | Defining Characteristic |

|---|---|---|---|---|

| PLA | $484M | 75.6% | 11.0% | Lowest cost, largest scale, banned in EU and UK |

| PHA | $94M | 14.7% | 19.3% | Marine-biodegradable, home-compostable, EU compliance potential |

| PBS/blends | $25M | 3.9% | 19.0% | Blend modifier for flexibility and processability |

| Plant-fibre composites | $37M | 5.8% | 15.0% | Agricultural waste feedstock, home-compostable |

| Total | $640M | 100% | 13.0% |

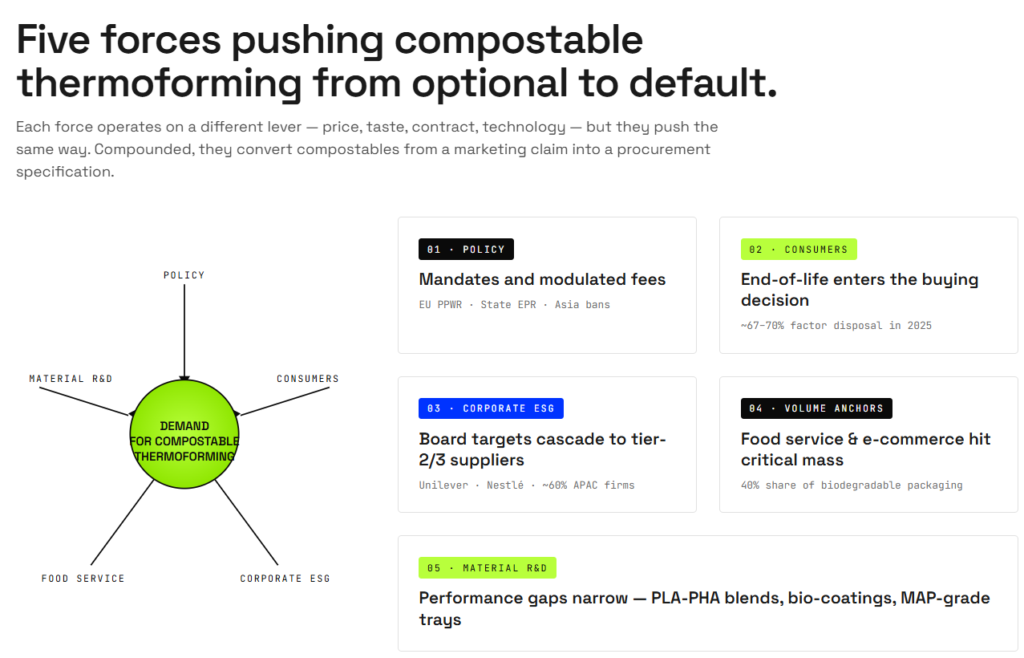

4.1 Compostable Plastics for Thermoforming – Demand Drivers

4.1.1 Policy-Led Market Creation

Governments are no longer issuing voluntary guidance on plastic waste.

They are legislating it.

This shift is the single most powerful demand driver for compostable thermoforming materials today.

In Europe, the Packaging and Packaging Waste Regulation (PPWR) imposes modulated fees that raise the effective cost of non-compostable plastics by 8 to 12%, effective January 2025.

In the United States, a patchwork of state-level Extended Producer Responsibility (EPR) laws in California, Oregon, Colorado, and Maine is forcing brand owners to rethink their packaging choices.

New Jersey has gone further, mandating that all packaging be recyclable or compostable by 2034.

In Asia-Pacific, China has set national targets for a 40% reduction in single-use plastics by 2030, while India’s Plastic Waste Management (Amendment) Rules have banned specific single-use formats outright.

4.1.2 Consumer Preference and Purchasing Behavior

Consumer awareness of packaging end-of-life has moved from niche to mainstream.

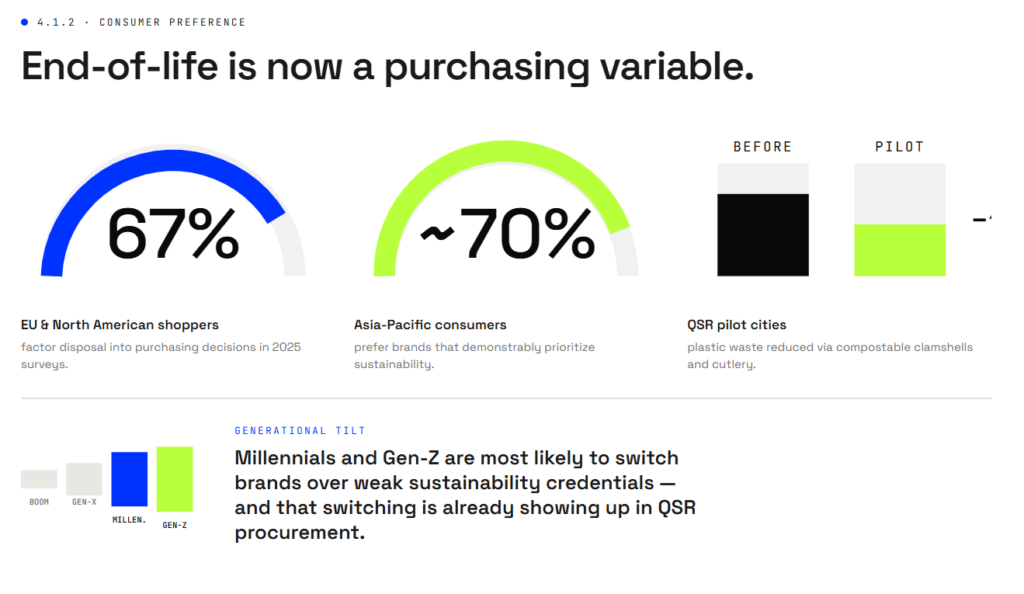

Surveys from 2025 show that 67% of shoppers in Europe and North America factor disposal into purchasing decisions.

In Asia-Pacific, approximately 70% of consumers prefer brands that demonstrably prioritize sustainability.

The generational shift is significant.

Millennials and Gen Z are more likely to switch brands over weak sustainability credentials, and this behavior is already influencing procurement in quick-service restaurants.

Pilots of compostable thermoformed clamshells and cutlery have reduced plastic waste by 15 to 20% in trial cities.

4.1.3 Corporate ESG Commitments Driving Procurement Change

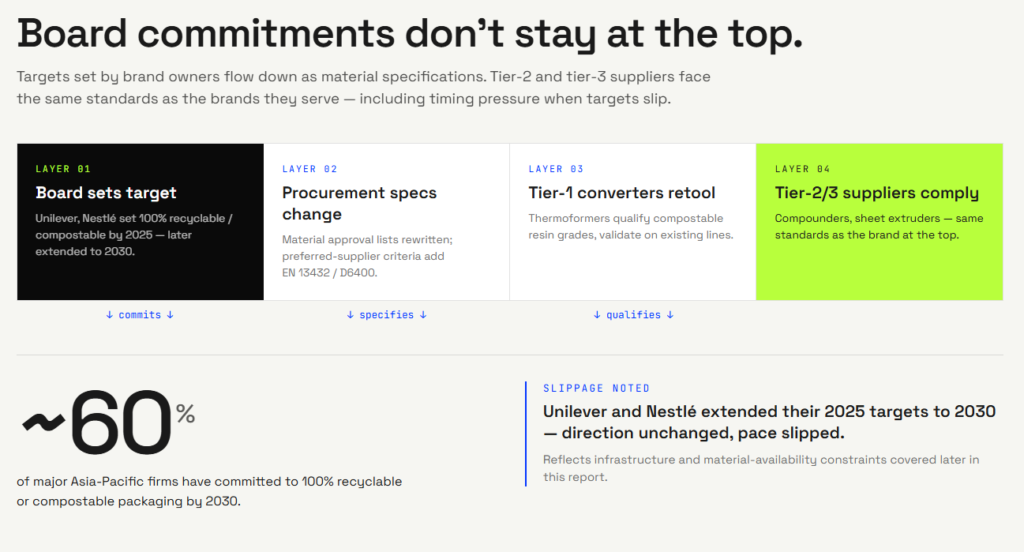

Sustainability targets set at board level are filtering into purchasing specifications.

Around 60% of major Asia-Pacific firms have committed to 100% recyclable or compostable packaging by 2030.

Unilever and Nestlé both set public targets to make all packaging recyclable or compostable by 2025.

Both have since acknowledged those targets will not be fully met on that timeline and have extended their commitments to 2030.

The direction of travel is unchanged, but the pace has slipped, which reflects the infrastructure and material availability constraints that this report covers throughout.

These commitments create cascading requirements across supply chains, meaning tier-two and tier-three suppliers increasingly face the same material standards as the brands they supply.

4.1.4 Food Service and E-commerce as Volume Anchors

Compostable thermoformed packaging has found its largest commercial application in food service and online food delivery.

Food packaging accounts for a 40% share of the total biodegradable packaging market globally.

The Thai food delivery market, as one regional indicator, grew from 7 billion to 105 billion Thai baht between 2018 and 2021, illustrating the volume that this sector alone can generate.

Thermoforming is increasingly preferred over injection molding in food packaging because it offers faster production speeds and lower tooling costs.

This gives brands a practical route to switching materials without lengthy retooling cycles, which matters when sustainability timelines are tightening.

4.1.5 Advances in Material Performance

Early bioplastics for thermoforming had real performance limitations, particularly around heat resistance and moisture barriers.

These gaps have narrowed significantly.

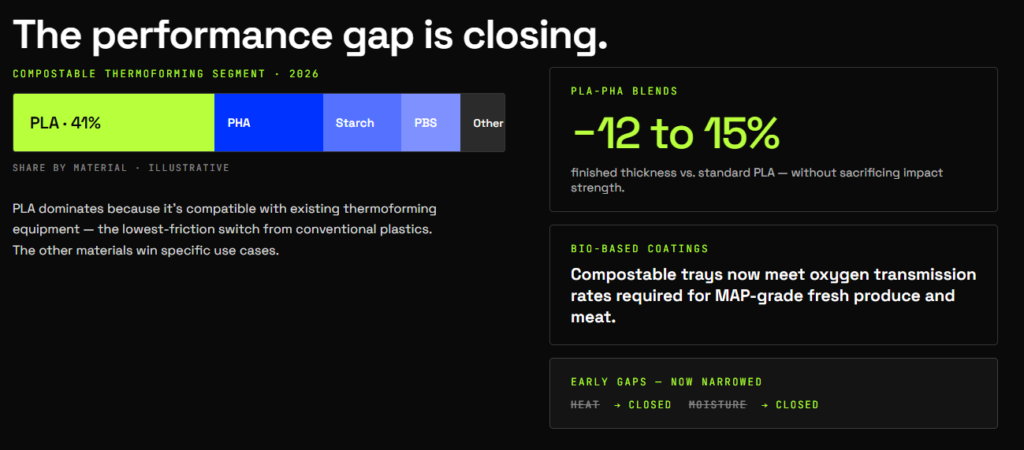

Polylactic Acid (PLA) holds a 41% share of the compostable thermoforming materials segment in 2026, largely because it is compatible with existing equipment.

Newer blends, such as PLA-PHA compounds, reduce finished product thickness by 12 to 15% compared to standard PLA without sacrificing impact strength.

Advances in bio-based coatings are enabling compostable trays to meet the oxygen transmission rates required for modified-atmosphere packaging of fresh produce and meat.

4.2 Compostable Plastics for Thermoforming – Regulatory Landscape

Regulations for compostable plastics in thermoforming are tightening across every major market: mandatory compostability requirements, rising costs for non-compliant materials, and strengthening certification standards.

The pace and approach differ by region.

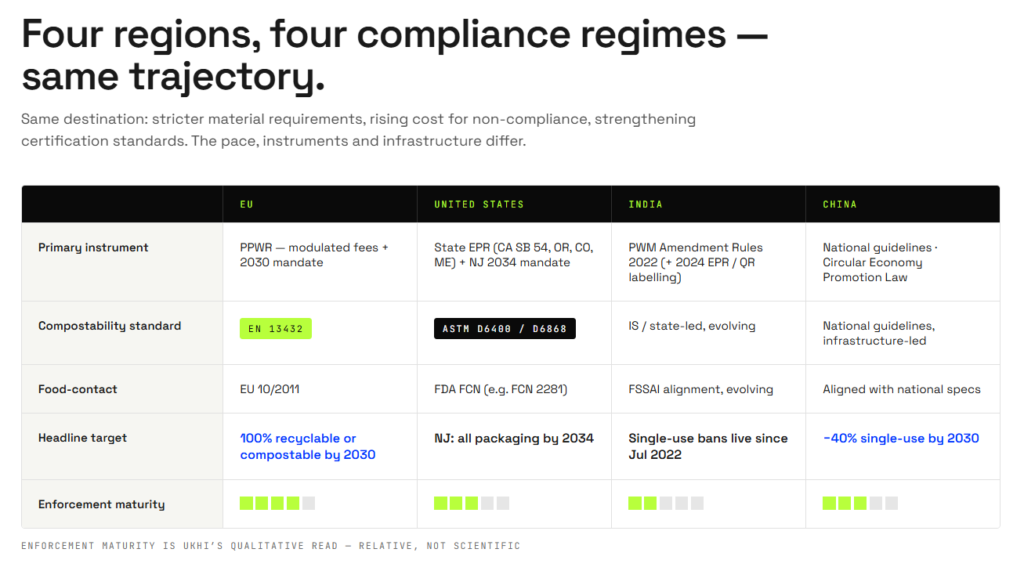

4.2.1 European Union

The EU is the most advanced policy environment for compostable packaging regulation.

The PPWR entered into force in February 2025 and will be broadly applicable from August 2026.

By 2030, all packaging placed on the EU market must be either recyclable or compostable.

Key compliance requirements for thermoforming manufacturers:

-

Industrial compostability certification: The EN 13432 standard is the de facto market-entry requirement.

Any material marketed as compostable must carry this certification. - Food-contact compliance: Thermoformed products intended for food use must comply with Commission Regulation (EU) No. 10/2011 on plastic materials and articles in contact with food.

- Country-level acceleration: France extended its ban on single-use plastics to cover fresh produce packaging in 2025, ahead of the broader PPWR timeline.

- Cost incentives: Modulated fees effective from January 2025 make certified compostable substrates a direct cost-avoidance strategy for manufacturers still using conventional plastics.

4.2.2 United States

The U.S. lacks federal harmonization on compostable plastics regulation, which has resulted in a state-by-state compliance environment that adds complexity for national brands and their thermoforming suppliers.

- EPR frameworks: California’s SB 54, alongside EPR laws in Oregon, Colorado, and Maine, is reshaping how packaging is specified and procured across the supply chain.

- Material mandates: New Jersey requires all packaging to be recyclable or compostable by 2034.

- Compostability standards: ASTM D6400 for plastics and ASTM D6868 for coatings on paper or board are the primary certification benchmarks.

-

Food-contact requirements: Thermoformed products must meet FDA Food Contact Substance Notification requirements.

Specific material blends, such as PHA-PLA combinations, require individual notifications (for example, FCN 2281).

4.2.3 India

India is a high-growth market where regulation of compostable plastics is at an earlier stage but accelerating.

India’s single-use plastic bans came into effect under the Plastic Waste Management (Amendment) Rules, 2022, which prohibited a defined list of items including polystyrene food containers, plastic cutlery, stirrers, and thin-gauge carry bags from July 2022.

The 2024 amendment extended the compliance framework by introducing Extended Producer Responsibility tracking requirements, including QR code labelling on plastic packaging, to improve accountability across the supply chain.

Together, these rules are pushing food-service operators and packaging manufacturers toward certified compostable alternatives.

The primary challenge is enforcement, which currently varies by state.

This makes India a market where early movers can establish supplier relationships and compliance frameworks before regulatory tightening intensifies.

4.2.4 China

China is the largest compostable packaging market in Asia-Pacific, accounting for 65% of the regional share.

National guidelines released in 2024 target a 40% reduction in single-use plastics by 2030.

The Circular Economy Promotion Law underpins government investment in biodegradable material innovation and composting infrastructure.

The Ministry of Housing and Urban-Rural Development is piloting food-waste separation and composting programmes across 46 major cities, which is critical to ensuring functional end-of-life pathways for compostable thermoformed packaging at scale.

Key Takeaway: Across all regions, the trajectory is toward stricter material requirements and rising compliance costs for conventional plastics.

For compostable plastics in thermoforming, this represents a structural tailwind, not a cyclical one.

The markets best positioned for rapid adoption are those where regulatory timelines, composting infrastructure, and material innovation are converging simultaneously.

Europe leads on all three.

China and India are building fast.

5. Compostable Plastics for Thermoforming: Competitive Landscape and Investment Activity

The commercial ecosystem for compostable plastics in thermoforming is spread across four layers.

Understanding where value is created and where bottlenecks exist at each stage is essential for assessing any investment opportunity.

5.1 Compostable Plastics for Thermoforming – Supply Chain

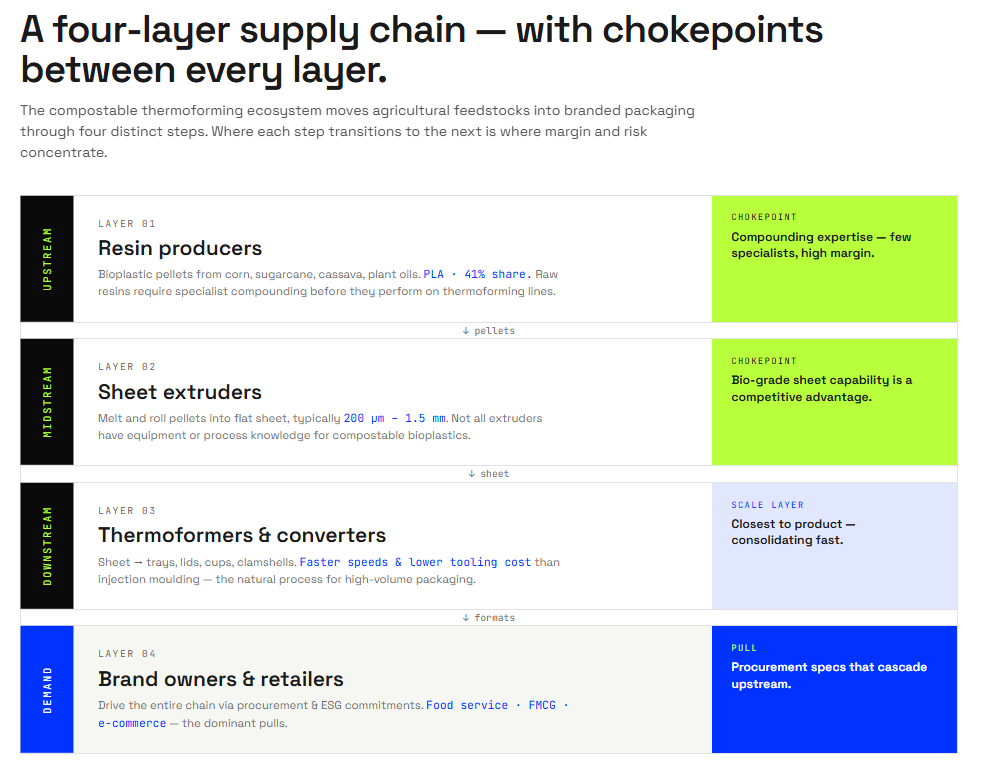

5.1.1 Resin Producers (Upstream)

The supply chain begins with bioplastic resin producers who manufacture raw material pellets from agricultural feedstocks such as corn, sugarcane, cassava, and plant oils.

These pellets are the input for all downstream processing.

Polylactic Acid (PLA) is the dominant resin in compostable thermoforming today, with approximately 41% of the material segment.

A critical nuance at this layer is that raw resins require specialist compounding before they perform reliably on thermoforming lines.

Definition: Compounding refers to the process of blending a base resin with additives to enhance specific performance properties.

For compostable thermoforming, this means improving heat deflection temperature, reducing brittleness, or accelerating crystallisation rates.

5.1.2 Sheet Extruders (Midstream)

Resin pellets are purchased by sheet extruders, who melt and process them into flat sheets suitable for thermoforming.

For packaging applications, sheets are typically produced in thicknesses ranging from 200 micrometres to 1.5 mm depending on the end use.

This layer is a technical chokepoint.

Not all extruders have equipment or process knowledge suited to compostable bioplastics, and those that do carry a competitive advantage.

5.1.3 Thermoformers and Converters (Downstream Manufacturing)

Converters heat the extruded sheets and shape them into finished packaging formats, including trays, lids, cups, and clamshells.

This is the layer closest to the product.

Thermoforming is preferred over injection moulding for high-volume packaging because it offers faster production speeds and lower tooling costs.

This makes it the natural process choice for brands that need to convert at scale without long capital cycles.

5.1.4 Brand Owners (End Users and Demand Drivers)

Brand owners and retailers drive the entire supply chain through procurement commitments and compliance requirements.

The major demand is in food service, fast-moving consumer goods (FMCG), and e-commerce.

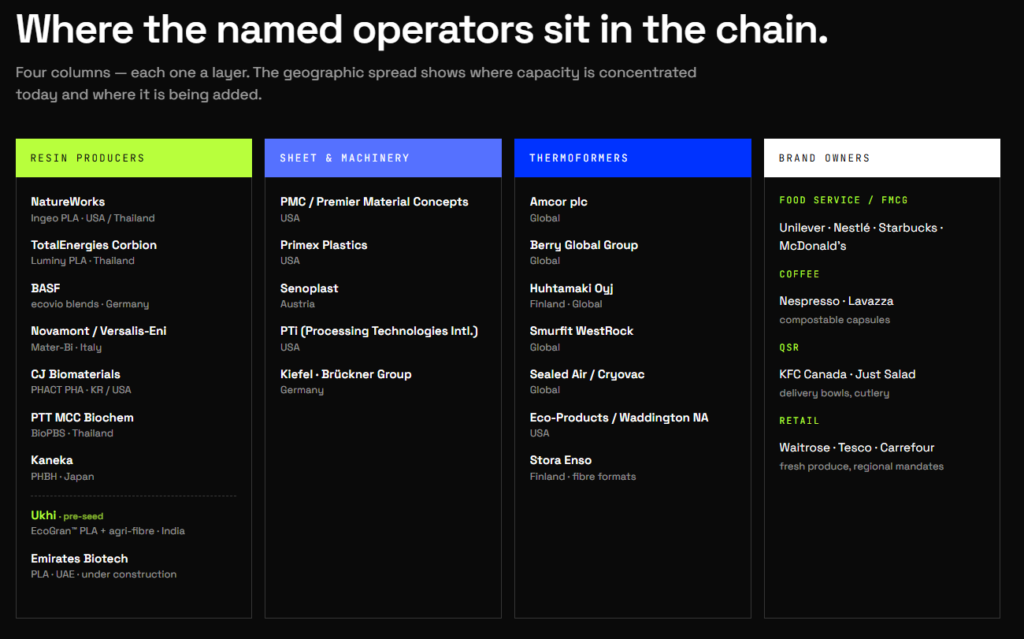

- Food service and FMCG: Unilever, Nestlé, Starbucks, and McDonald’s have all set targets to transition packaging to recyclable or compostable formats by 2025 to 2030.

- Coffee: Nespresso and Lavazza are primary drivers for compostable coffee capsules, a high-volume thermoformed format.

- Quick-service restaurants: KFC Canada and Just Salad have committed to compostable consumer-facing packaging including delivery bowls and cutlery.

- Retail: European retailers including Waitrose, Tesco, and Carrefour use compostable packaging for fresh produce to comply with regional mandates.

5.2 Compostable Plastics for Thermoforming – Key Players by Segment

Resin Producers

- NatureWorks (Ingeo PLA, USA/Thailand)

- TotalEnergies Corbion (Luminy PLA, Thailand)

- BASF (ecovio blends, Germany)

- Novamont/Versalis-Eni (Mater-Bi, Italy)

- CJ Biomaterials (PHACT PHA, South Korea/USA)

- PTT MCC Biochem (BioPBS, Thailand)

- Kaneka Corporation (PHBH, Japan)

- Ukhi (EcoGran™ PLA compounds and agri-fibre blends, India, pre-seed stage)

- Emirates Biotech (PLA, UAE, under construction)

Sheet Extruders and Machinery

- PMC/Premier Material Concepts (USA)

- Primex Plastics Corporation (USA)

- Senoplast (Austria)

- PTi Processing Technologies International (USA)

- Kiefel GmbH/Brückner Group (Germany)

Thermoformers and Converters

- Amcor plc (Global)

- Berry Global Group (Global)

- Huhtamaki Oyj (Finland/Global)

- Smurfit WestRock (Global)

- Sealed Air/Cryovac (Global)

- Eco-Products/Waddington North America (USA)

- Stora Enso (Finland, fibre-based formats)

5.3 Compostable Plastics for Thermoforming – Recent Funding, M&A, and Capacity Expansions

The compostable thermoforming sector is in an active phase of capital deployment.

Investment is flowing into three areas: consolidation through acquisition, large-scale production capacity, and early-stage material innovation.

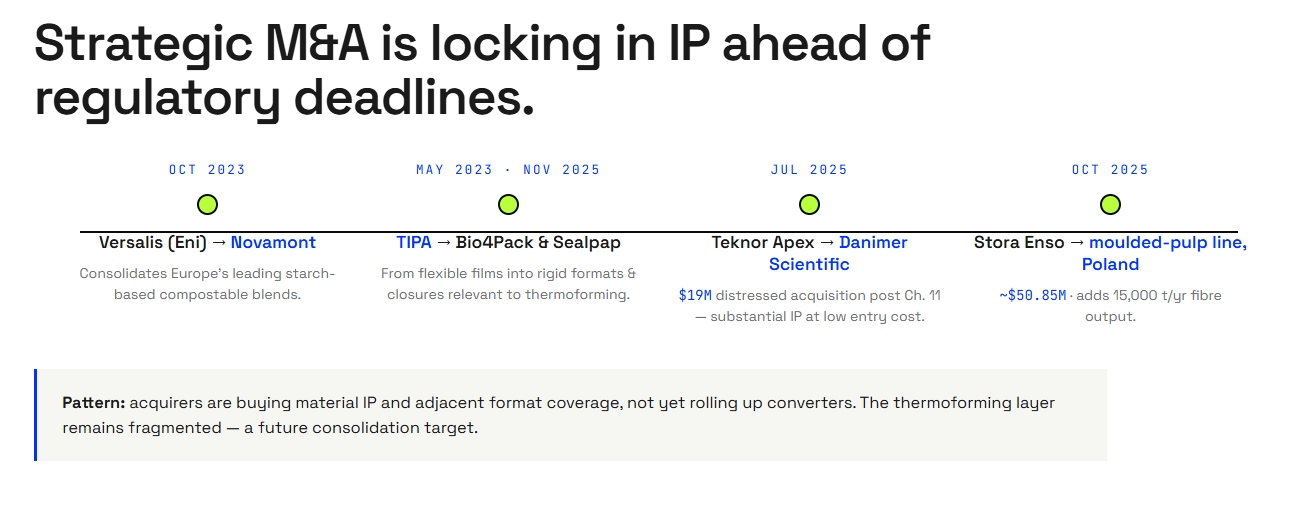

5.3.1 Mergers and Acquisitions

Strategic acquisitions are being used to secure material IP and market position ahead of regulatory deadlines.

Versalis (Eni) acquired Novamont in October 2023, consolidating control over Europe’s leading producer of starch-based compostable blends.

Teknor Apex acquired Danimer Scientific in July 2025 for $19 million in a distressed transaction following Danimer’s Chapter 11 filing.

The acquisition represented substantial IP value at a low entry cost.

TIPA acquired Bio4Pack in May 2023 and Sealpap in November 2025, extending its reach from flexible compostable films into rigid formats and closures relevant to thermoforming.

Stora Enso acquired a moulded-pulp line in Poland for approximately $50.85 million in October 2025, which added 15,000 tonnes of annual output in fibre-based packaging formats.

5.3.2 Capacity Expansions

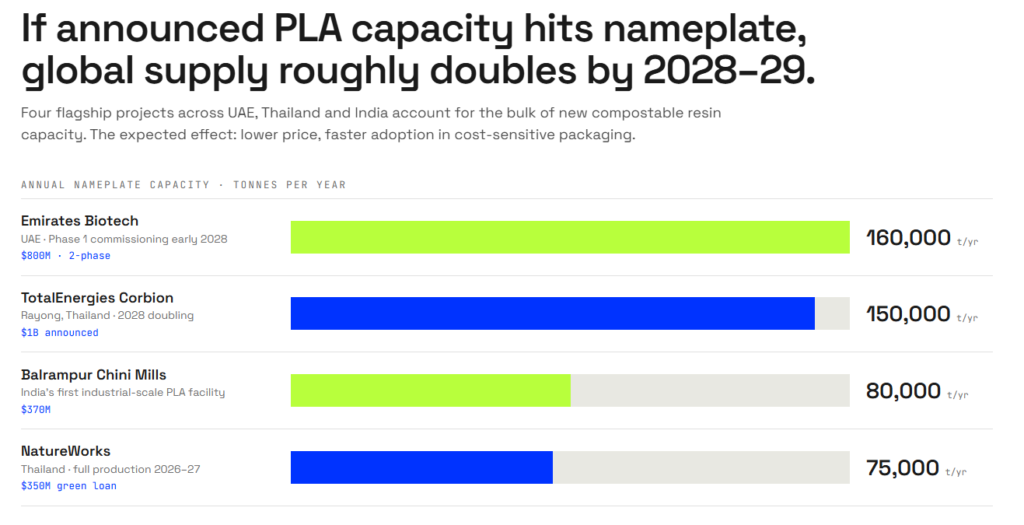

New production capacity for compostable bioplastic resins is being built primarily in Asia-Pacific and the Middle East.

Emirates Biotech (UAE): An $800 million, two-phase project to build the world’s largest single-site PLA plant in Abu Dhabi, targeting 160,000 tonnes per year with Phase 1 commissioning in early 2028.

NatureWorks (Thailand): A 75,000 tonne per year integrated PLA facility supported by a $350 million green loan, with full production targeted for 2026 to 2027.

TotalEnergies Corbion: A $1 billion plan announced in early 2025 to double its Rayong PLA plant capacity to 150,000 tonnes per year by 2028.

Balrampur Chini Mills (India): India’s first industrial-scale PLA facility, representing a $370 million investment targeting 80,000 tonnes per year.

Insight: If the announced projects reach nameplate capacity by 2028 to 2029, global PLA supply will roughly double.

This is expected to reduce price and accelerate adoption of compostable thermoforming materials in cost-sensitive packaging segments.

5.3.3 Startup and Venture Funding

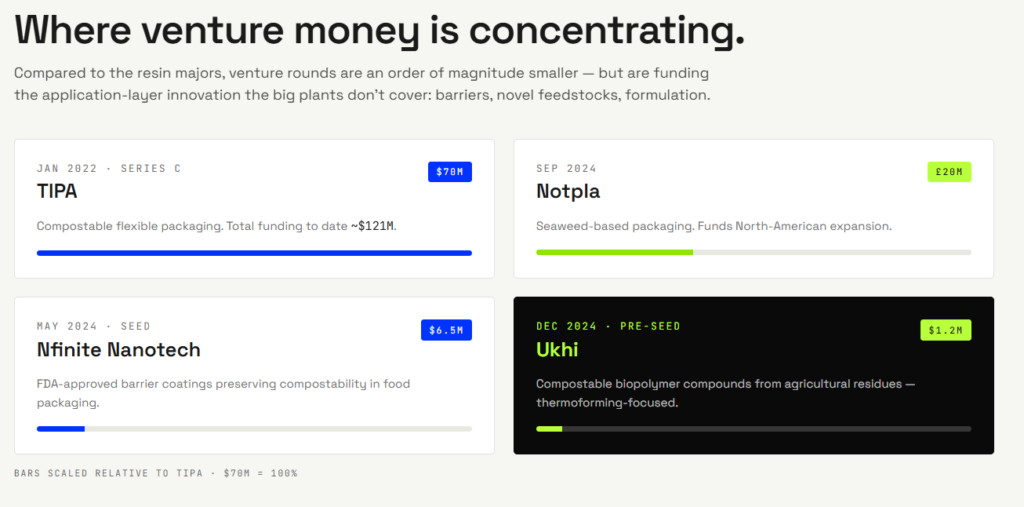

TIPA raised $70 million in a Series C round in January 2022, which brings its total funding to approximately $121 million for compostable flexible packaging.

Notpla raised £20 million in September 2024 to expand its seaweed-based packaging into North America.

Nfinite Nanotech secured $6.5 million in seed funding in May 2024 to scale FDA-approved barrier coatings that preserve compostability in food packaging.

Ukhi raised $1.2 million in pre-seed funding in December 2024 to scale compostable biopolymer compounds derived from agricultural residues, with a focus on thermoforming applications.

6. Compostable Plastics for Thermoforming: Risks and Outlook

The market for compostable plastics in thermoforming is growing with momentum behind it.

But growth at this stage of maturity comes with technical, systemic, and commercial risks.

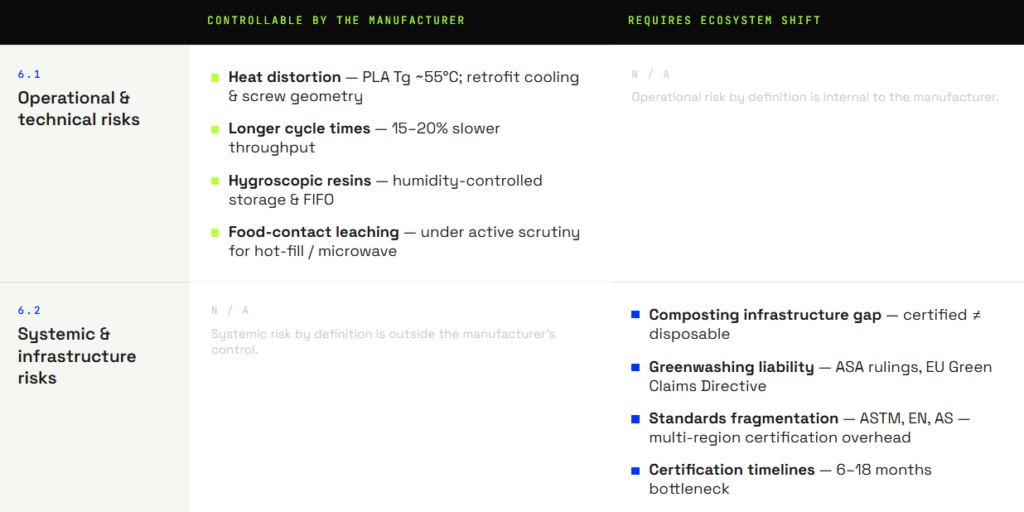

6.1 Compostable Plastics for Thermoforming – Operational and Technical Risks

Converting from conventional plastics to compostable thermoforming materials is not a drop-in substitution for most manufacturers.

The operational adjustments are significant.

Heat distortion and processing limitations

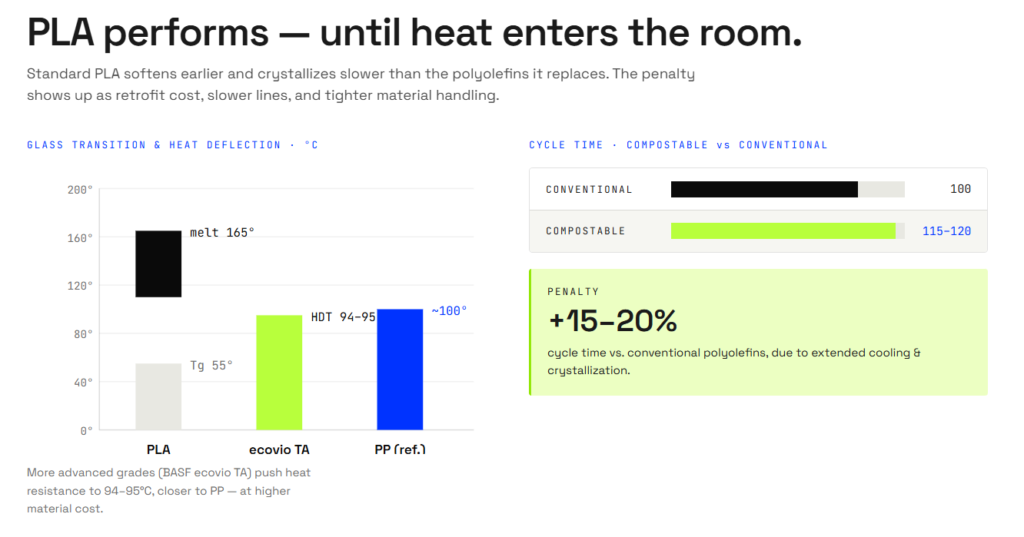

Standard Polylactic Acid (PLA) has a glass transition temperature of approximately 55°C and a melting temperature of around 165°C.

This is lower than that of polyethylene or polypropylene, which means that manufacturers need to retrofit cooling systems or adjust screw geometries to prevent polymer degradation from shear heat during processing.

More advanced grades, such as BASF’s ecovio TA, push heat resistance to 94 to 95°C, and performance closer to PP, but at higher material cost.

Longer cycle times

Production cycles for compostable bioplastics can run 15 to 20% longer than for conventional polyolefins, due to extended cooling and crystallization phases.

On high-volume lines, this translates into reduced throughput and higher per-unit cost.

Manufacturers investing in the transition need to account for this in their operational planning.

Material handling and storage

Unlike petrochemical plastics, many compostable resins are hygroscopic.

This means they absorb moisture from the air.

This can trigger premature degradation before the material has even been processed.

Manufacturers must implement humidity-controlled storage and strict FIFO (First-In, First-Out) inventory protocols to maintain material integrity throughout production.

Food-contact and leaching concerns

Critical assessment of PLA in food-contact applications has raised questions about plasticizer leaching when the material is exposed to heat.

The majority of commercial grades carry food-contact certification, including FDA and EU 10/2011 compliance, but this remains an area of active scrutiny, particularly for hot-fill or microwave applications.

6.2 Compostable Plastics for Thermoforming – Systemic and Infrastructure Risks

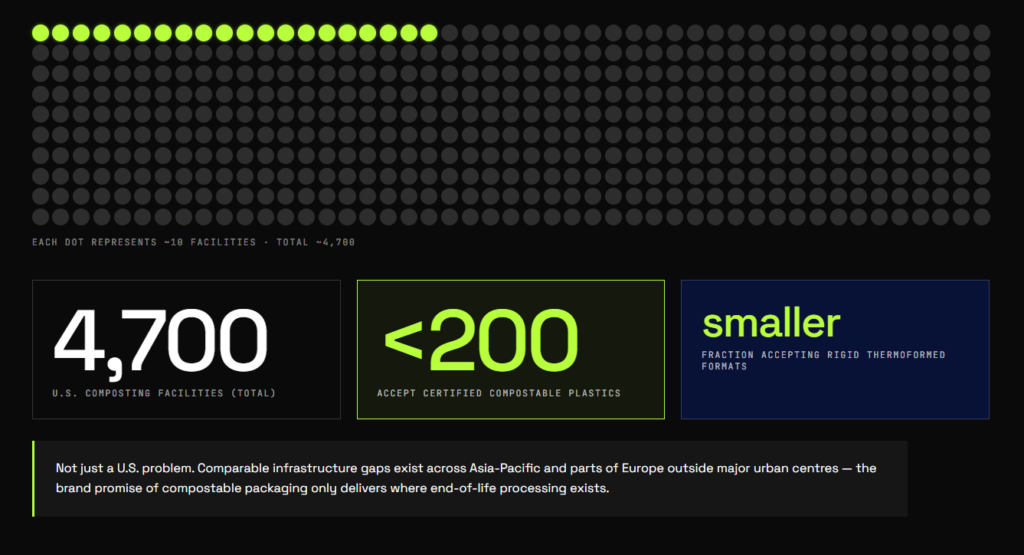

The composting infrastructure gap

The most consequential systemic risk is the mismatch between certified compostable packaging claims and actual end-of-life disposal capability.

In the United States, fewer than 200 of approximately 4,700 composting facilities accept certified compostable plastics.

The fraction accepting rigid thermoformed formats such as trays and lids is smaller still.

This is not solely a U.S. problem.

Infrastructure gaps exist across Asia-Pacific and in parts of Europe outside major urban centres.

Greenwashing liability

Regulatory scrutiny of sustainability claims is intensifying.

In April 2025, the UK’s Advertising Standards Authority upheld rulings against brands for marketing packaging as compostable without clearly distinguishing between home and industrial compostability requirements.

The EU’s Green Claims Directive, currently advancing through implementation, will require substantiated, third-party-verified environmental claims across member states.

Standards fragmentation

There is no single global standard for compostability.

ASTM D6400 governs certification in the United States, EN 13432 applies in Europe, and AS 4736 covers Australia.

Manufacturers selling across multiple markets must pursue multi-region certification strategies, which adds cost and lead time.

Current certification timelines range from 6 to 18 months, which slows innovation cycles and creates a bottleneck as demand for new home-compostable material grades accelerates.

7. Compostable Plastics for Thermoforming: Investment Opportunities

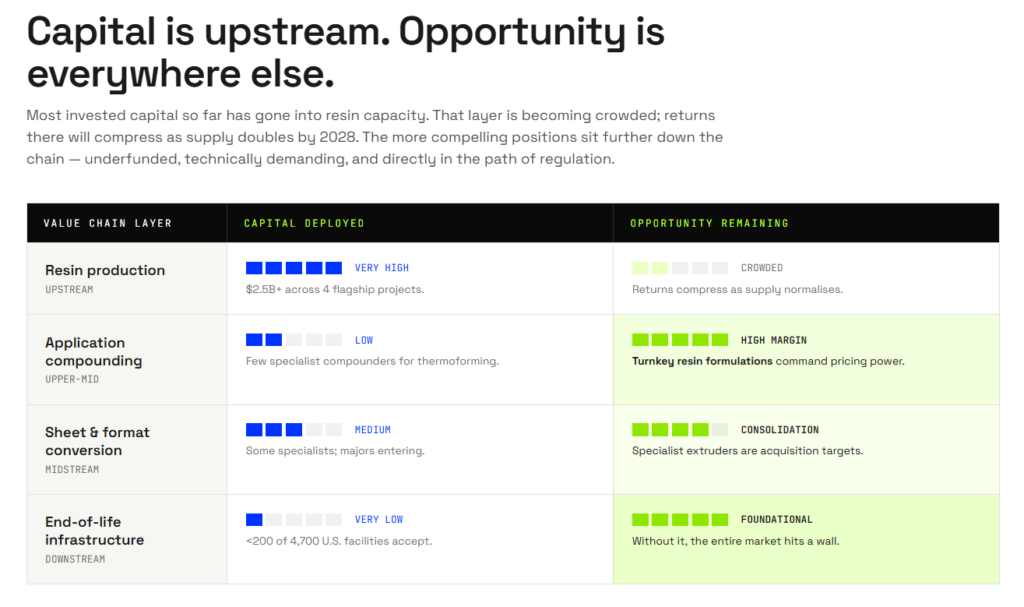

Most of the capital that has entered compostable plastics for thermoforming so far has gone into building resin production capacity.

That makes sense as a starting point, but it means the upstream layer is becoming crowded, and the returns there will compress as large-scale supply comes online by 2028.

The more compelling investment case is further down the value chain, in the parts of the market that remain underfunded, technically demanding, and directly in the path of regulatory-driven demand.

7.1 Compostable Plastics for Thermoforming – Underserved Gaps in the Value Chain

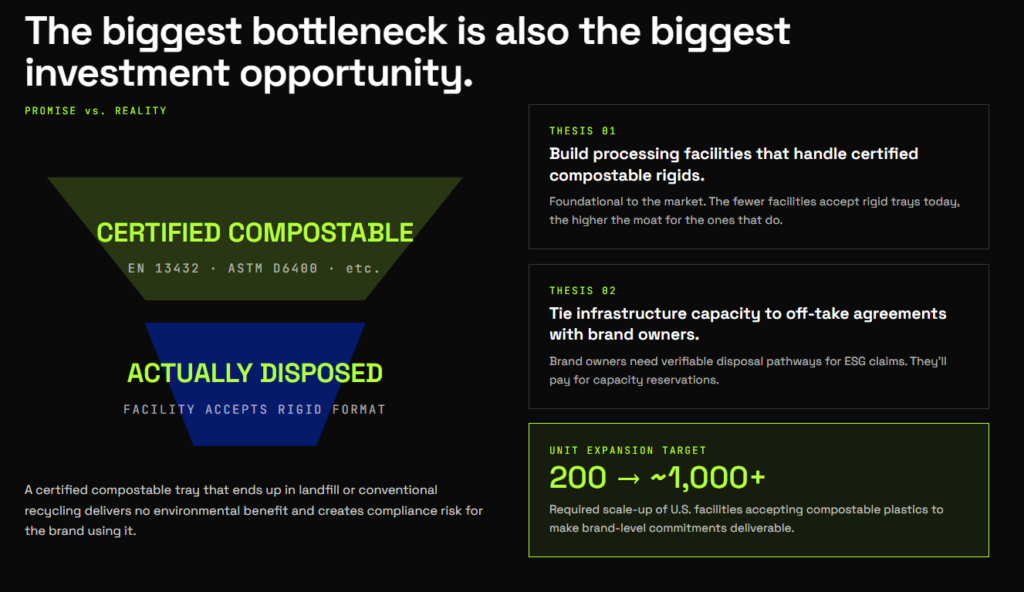

7.1.1 Composting Infrastructure

The most significant bottleneck in the entire compostable packaging ecosystem is end-of-life infrastructure.

In the United States, fewer than 200 of approximately 4,700 composting facilities currently accept compostable plastics.

The fraction accepting rigid thermoformed items such as trays and lids is smaller still.

This gap undermines the core value proposition of compostable packaging.

A certified compostable tray that ends up in landfill or a conventional recycling stream delivers no environmental benefit and creates compliance risk for the brands using it.

Investment in processing facilities that can handle certified compostable rigids is therefore foundational to the market.

7.1.2 Application-Specific Compounding

Raw bioplastic resins do not perform reliably on thermoforming lines without specialist formulation.

There is a shortage of compounders with the depth of expertise to develop turnkey resin formulations for specific end uses, such as high-heat trays for ready meals, optically clear lids for fresh produce, or flexible formats for peel-seal applications.

This is a high-margin, technically differentiated segment.

Companies that can deliver application-ready compostable thermoforming compounds with validated processing parameters reduce conversion risk for brand owners and command pricing power accordingly.

7.1.3 Certification and Testing Infrastructure

Current testing lead times for compostability certification range from 6 to 18 months.

As regulatory requirements expand and new standards for home compostability gain traction alongside industrial compostability, the demand for accredited testing capacity will increase substantially.

Investment in testing and certification infrastructure is not high-profile, but it is commercially durable.

It is a toll-road position: every new material, blend, or format that enters the market must pass through it.

7.2 Compostable Plastics for Thermoforming – High-Performance Material Innovations

7.2.1 Next-Generation Barrier Coatings

Achieving moisture and oxygen barriers comparable to conventional plastics remains the most significant technical barrier to widespread adoption of compostable thermoformed packaging in shelf-stable and chilled food categories.

Bio-based coatings that maintain certified compostability while delivering the barrier performance required for modified-atmosphere packaging represent a multi-billion-dollar addressable market.

The companies that solve this problem will become a critical input supplier to the entire converting industry.

Startups including Nfinite Nanotech and Ionkraft are actively developing in this space.

7.2.2 Marine and Home-Compostable Substrates

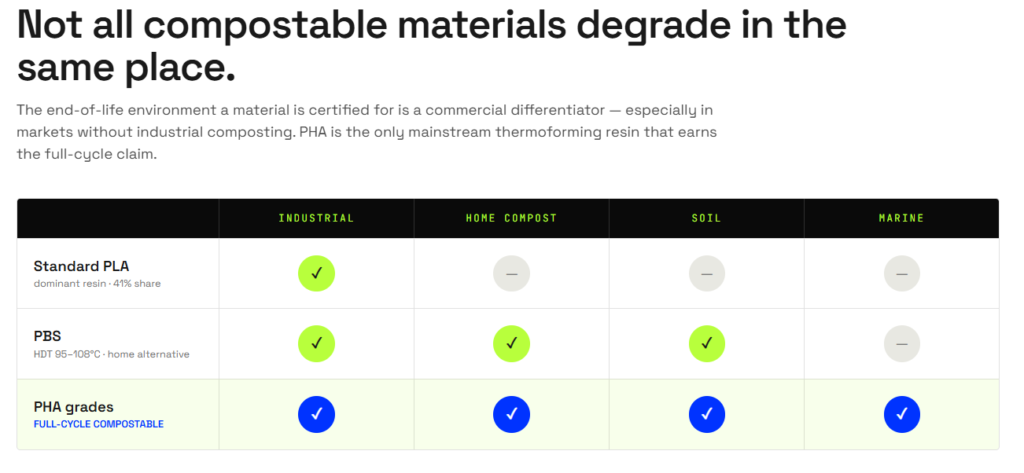

Not all compostable materials are equal at end-of-life.

Most certified compostable plastics, including standard PLA, require industrial composting conditions to break down within the certified timeframe.

They do not degrade in home compost bins, soil, or marine environments.

This is a meaningful limitation in markets where industrial composting infrastructure is absent or patchy, which currently describes most of Asia, Africa, and large parts of North America.

Polyhydroxyalkanoates (PHAs) are the primary exception.

Certain PHA grades are certified for degradation across all four end-of-life environments: industrial composting, home composting, soil, and marine.

This makes PHA the only mainstream thermoforming resin that can substantiate a full-cycle compostability claim regardless of where the packaging ends up.

For food-service operators in coastal markets, seafood chains, or any application where packaging litter risk is high, this distinction is commercially significant.

Polybutylene Succinate (PBS) offers a different set of advantages.

It is home-compostable and soil-biodegradable in certified formulations, and it outperforms standard PLA on heat resistance, with a heat deflection temperature of 95 to 108°C.

It is not, however, marine-biodegradable, and should not be positioned as such.

Its value in this context is as a home-compostable alternative to PLA in markets where industrial composting is unavailable, not as a full-environment solution.

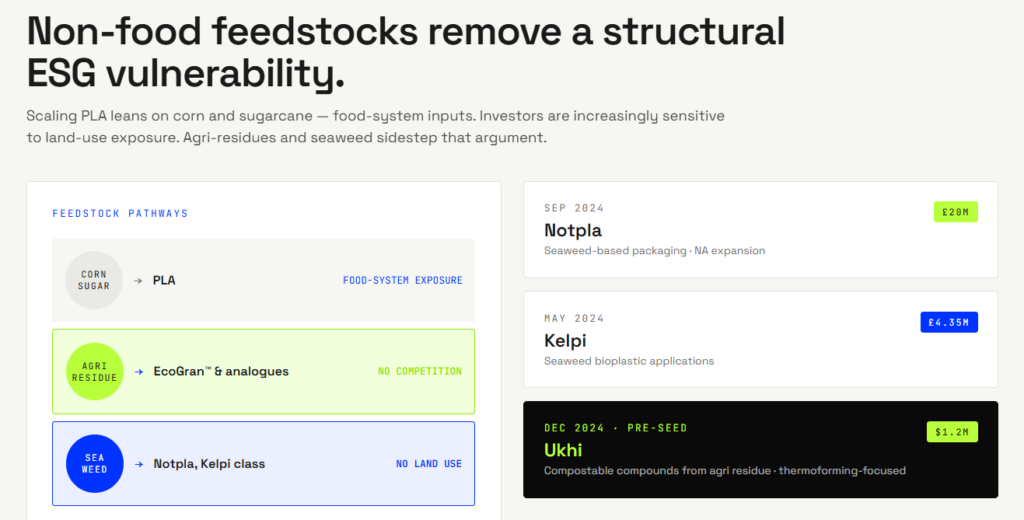

7.2.3 Agricultural Residues and Seaweed-Based Materials

A growing cohort of startups is developing thermoformable sheets from non-food feedstocks, including seaweed and agricultural waste.

Notpla raised £20 million in September 2024 to expand seaweed-based packaging into North America.

Kelpi secured £4.35 million in May 2024 for seaweed-based bioplastic applications.

These materials address a secondary but increasingly visible concern among investors: the land-use and food-system competition implications of scaling PLA, which relies on corn and sugarcane feedstocks.

Non-food feedstock pathways reduce this exposure and carry a stronger sustainability narrative.

Key Takeaway: The most attractive investment positions in compostable thermoforming are not in building more resin capacity.

They are in solving the problems that prevent existing capacity from being fully utilised: infrastructure deficits, formulation gaps, barrier performance limitations, and traceability.

These are the layers where defensible margins and durable competitive positions are being built.

© 2026 Ukhi Bioplastics Private Limited. All rights reserved.

References

- Bish, T. (2026, May 5). Plastic thermoforming explained: The complete guide for manufacturers. Vantage Plastics.

- Brentwood. (2025, August 14). A complete guide to thermoforming: A beginner’s guide to its process and applications. Brentwood Industries.

- CJ Biomaterials. (2024, May). Sustainable biopolymers for thermoforming. CJ Biomaterials.

- Chaban, M. (2026, March 12). Advantages and disadvantages of thermoforming: A comprehensive guide for manufacturing strategy. RapidMade.

- Chen, A. (2026). ASTM D6400 certification guide (2026 update): ASTM D6400 explained: Certification requirements for compostable plastics. Certified Compostable Bags Manufacturer.

- Ford, L. (2025, June 11). Driving compostable packaging solutions with PHA & PLA innovations. CJ Biomaterials; Packaging Technology Today.

- Formlabs. (2026). Guide to thermoforming. Formlabs.

- Jamestown Plastics. (2026). PLA in thermoforming: Practical uses and limitations. Jamestown Plastics.

- Mulan Group. (2026, January 7). Innovations in thermoforming plastic: Trends to watch. Mulan Manufacturing Group.

- Pan, A. (2025, May 17). Complete biodegradable plastics compared: PHA, PHB, PBAT, PLA, PBS, PCL, and TPS explained. specialty-polymer.com; Guangzhou Chozen Technology Co., Ltd.

- Samcome. (2026, April 24). Types of bioplastics: PLA, PBAT, PHA, PBS and TPS explained. Samcome.

- The Industrial Evolution of Sustainable Polymer Processing: A Comprehensive Analysis of Thermoforming and Compostable Materials. (2026). [Markdown Analysis Document].

- Tina. (2026, February 2). Bioplastics guide: PLA, PHA & starch-based types. Sales Plastics.

- Tina. (2026, March 4). What is thermoplastic starch (TPS)? Properties, processing, and uses. Sales Plastics.

- Tina. (2026, March 10). High-performance thermoplastic starch (TPS): A cost-effective bio-based solution for food packaging. Sales Plastics.

- Tyagi, P. (2025, March 22). PHA and its blends with different bioplastics: A sustainable revolution. Phantastic Bioplastics.

- Vivek, V. (2026, May). Bioplastic definitions and properties: PLA, PHA, PBAT, PBS, PHB and more. UKHI.

- Wylong Machinery. (2026, January 28). Common thermoforming defects: Prevent webbing & thinning. Wylong Machinery.

- Zhang, J. (2025, July 26). 2026 Global compostable packaging regulations: Prepare for EN13432, ASTM D6400 & EPR. Bioleader.

- Beasley, J. (2025, June 2). Staying ahead of the curve: A 2025 update on U.S. packaging EPR and packaging legislation. rePurpose Global.

- Bioleader. (2025, December 1). Canada compostable packaging certification guide 2025–2026: Standards, compliance & supplier requirements.

- Coherent Market Insights. (2026, April 2). Thermoform packaging market analysis & forecast: 2026-2033.

- European Bioplastics e.V. (2026, February 10). Bioplastics market development update 2025.

- Fortune Business Insights. (2026, April 20). Thermoform packaging market size, share & industry analysis.

- Future Market Insights. (2025, July 3). Compostable plastic packaging material market 2025-2035.

- G20 Implementation Framework for Actions on Marine Plastic Litter. (2025, October 9). China | Towards Osaka blue ocean vision: Actions and progress on marine plastic litter.

- Grand View Research. (2024). Compostable plastics market size & share report, 2030.

- IMARC Group. (2025). Saudi Arabia biodegradable packaging market size, share, trends and forecast by material type, application, and region, 2026-2034.

- MarketsandMarkets. (2026, May). Biodegradable plastics market.

- Molenveld, K., Borzacchiello, M. T., & Magnolfi, V. (2026). Bio-based plastics in a sustainable and circular bioeconomy. European Commission Knowledge Centre for Bioeconomy.

- Mordor Intelligence. (2026). Thermoform packaging market size & share analysis – growth trends and forecast (2026 – 2031).

- Polaris Market Research. (2024, March). Thermoform packaging market trends, global industry size 2024-2032.

- Research and Markets. (2025, April 14). Biodegradable plastics (PLA, starch blends, PBAT, PHA, PBS) market global forecast to 2029. Business Wire.

- Research and Markets. (2024, November 27). Thermoformed plastics market trends and business opportunities report 2025-2030. GlobeNewswire.

- Sharma, A. (2024, November). Biodegradable plastic market size, share & trends analysis report. Straits Research.

- Spherical Insights. (2026, January). Global compostable plastics market size, share, and COVID-19 impact analysis.

- Strategic Market Research. (2026, January). Thermoformed shallow trays market report 2030.

- Towards Chemical and Materials Consulting. (2025, August 7). Bioplastics market volume to hit 73,21,706.6 tons by 2034. GlobeNewswire.

- CBRHK. (n.d.). Biodegradable PP alternatives: Your guide to sustainable plastic solutions. https://cbrhkglobal.com/biodegradable-pp-alternatives-your-guide-to-sustainable-plastic-solutions/

- Chang, C.-J., Venkatesan, M., Cho, C.-J., Chung, P.-Y., Chandrasekar, J., Lee, C.-H., Wang, H.-T., Wong, C.-M., & Kuo, C.-C. (2022). Thermoplastic starch with poly(butylene adipate-co-terephthalate) blends foamed by supercritical carbon dioxide. Polymers, 14(10), 1952. https://doi.org/10.3390/polym14101952

- Chapleau, N., Huneault, M. A., & Li, H. (2006). Processing and properties of biaxially oriented poly(lactic acid)/thermoplastic starch blends. NRC Publications Archive. https://nrc-publications.canada.ca/eng/view/accepted/?id=6260c260-979a-4d60-bdc7-050bb4243b1c

- Chozen Technology. (2025, May 17). Complete biodegradable plastics compared: PHA, PHB, PBAT, PLA, PBS, PCL, and TPS explained. https://specialty-polymer.com/biodegradable-compared-pha-phb-pbat-pla-pbs-pcl-and-tps/

- Comprehensive engineering analysis of compostable polymers in thermoforming applications: Material science, processing mechanics, and industrial optimization. (n.d.).

- Feijoo, P., Samaniego-Aguilar, K., Sánchez-Safont, E., Torres-Giner, S., Lagaron, J. M., Gamez-Perez, J., & Cabedo, L. (2022). Development and characterization of fully renewable and biodegradable polyhydroxyalkanoate blends with improved thermoformability. Polymers, 14(13), 2527. https://doi.org/10.3390/polym14132527

- Hill, C. (2018, December). Biopolymers (bio-based plastics) – An overview. UK Climate Change Committee.

- Hong, J., Lee, J., Kim, S. K., Son, D., Kang, D., & Shim, J. K. (2025). Enhancing thermal insulation property and flexibility of starch/poly(butylene adipate terephthalate) (PBAT) blend foam by improving rheological properties. Polymers, 17(2), 138. https://doi.org/10.3390/polym17020138

- Jamestown Plastics. (n.d.). PLA in thermoforming: Practical uses and limitations. https://jamestownplastics.com/pla-in-thermoforming-practical-uses-and-limitations/

- Lee, R. E., Guo, Y., Tamber, H., Planeta, M., & Leung, S. N. S. (2016). Thermoforming of polylactic acid foam sheets: Crystallization behaviors and thermal stability. Industrial & Engineering Chemistry Research, 55(3), 560–567. https://doi.org/10.1021/acs.iecr.5b03473

- Li, J. (2025). Biodegradable PBAT plastics and composites. Springer Nature. https://doi.org/10.1007/978-981-96-2057-9

- Market Growth Reports. (2025, December 17). Biobased polylactic acid (PLA) market size, share, growth, and industry analysis. https://www.marketgrowthreports.com/biobased-polylactic-acid-pla-market-118705

- MarketsandMarkets. (2025, August). Polybutylene adipate terephthalate market report 2025-2030. https://www.marketsandmarkets.com/Market-Reports/polybutylene-adipate-terephthalate-market-184395122.html

- Morán, D., Velásquez, E., Calatayud, M. A., de la Fuente, B., Hernández-Muñoz, P., & López-de-Dicastillo, C. (2026). Sustainable upgrade of post-consumer PLA: The effect of adding a plasticizer and a chain extender on the functional properties and toxicity of this recycled bioplastic. ACS Omega, 11(1), 1690–1702. https://doi.org/10.1021/acsomega.5c09603

- Mordor Intelligence. (2026, February 9). Biodegradable plastic packaging – Market share analysis, industry trends & statistics, growth forecasts (2026 – 2031). GII Research. https://www.giiresearch.com/report/moi1939575-biodegradable-plastic-packaging-market-share.html

- PHA Sourcing. (2024, September 2). PHA market explosion by 2026: Biodegradable plastics take center stage. https://phasourcing.com/pha-market-explosion-by-2026-biodegradable-plastics-take-center-stage/

- Polaris Market Research. (2025, August). Biopolymer packaging market outlook and share 2034. https://www.polarismarketresearch.com/industry-analysis/biopolymer-packaging-market

- Sales Plastics. (2025, December 4). Polylactic acid (PLA) processing parameters guide. https://salesplastics.com/pla-processing-methods-and-production/

- Sales Plastics. (2026, April 27). PLA vs PBAT: Which biodegradable polymer is best for your application? https://salesplastics.com/pla-vs-pbat-which-biodegradable-polymer-is-best-for-your-application/

- Straits Research. (2025, August). Starch-based plastics market size, share & trends: Industry report, 2033. https://www.straitsresearch.com/report/starch-based-plastics-market

- BASF. (n.d.). Brochure ecovio® for sheet-line extrusion and thermoforming.

- Carlin, C. (Ed.). (2015). Quarterly – SPE Thermoforming Division, 34(3). Society of Plastics Engineers.

- ChemAnalyst. (2026). Polylactic acid market size, share, analysis and forecast 2036.

- CJ Biomaterials. (n.d.). Sustainable biopolymers for thermoforming.