Home Compostable Packaging Navigator

Interactive companion to the State of Home Compostable Packaging: Global Report 2025

Is It Home Compostable?

Tap any material to see whether it genuinely qualifies for home composting, with key details from the report.

Compare Materials Side by Side

Select two or more materials to see how they compare on cost, compost timeline, certifications, and applications.

Certification Standards

Tap any standard to explore what it requires and where it applies. All require 90% biodegradation within 12 months at ambient temperatures.

Product Finder

Browse real home compostable products currently on the market, filtered by category.

Executive Summary

Home compostable packaging has moved from environmental experiment to commercial category.

It has certification standards, a growing material ecosystem, a tightening regulatory framework, and measurable consumer preference behind it.

It also has a persistent gap between what certified products are designed to do and what actually happens at end of life.

This report covers both sides of that picture honestly.

1. Home compostability is a defined, testable standard, not a general environmental claim.

The term is backed by certification frameworks including AS 5810, OK Compost HOME, NF T 51-800, and the newly launched BPI Home Compostability Standard, each of which requires verified biodegradation, disintegration, and ecotoxicity outcomes under ambient temperature conditions of 20°C to 30°C.

A product labeled “compostable” without further qualification is, in the vast majority of cases, industrially compostable only, meaning it requires a managed facility operating at 55°C to 70°C to break down.

These are fundamentally different claims with fundamentally different end-of-life outcomes for consumers.

2. Only a narrow set of materials genuinely qualifies for home compostability, and most of the market does not meet that bar.

Natural fiber formats (sugarcane bagasse, molded pulp, uncoated kraft paper) and starch-based blends are the commercially mature options.

PHA is the only mainstream bioplastic family certified for home, soil, and marine biodegradation, but it remains expensive at USD 4 to 7 per kilogram and is in the early stages of mass commercialization.

Standard PLA, the most widely used compostable bioplastic globally, is not home compostable.

It requires industrial heat above 58°C to degrade and will sit unchanged in a backyard bin for decades without it.

3. The market is growing significantly, driven by regulatory mandates and the absence of industrial composting infrastructure in most regions.

The global compostable packaging market was valued at approximately USD 85.43 billion in 2025 and is projected to reach USD 152.96 billion by 2034.

Home compostable formats within that total are growing at a CAGR of 20.43%, more than three times the rate of the broader compostable market.

The primary structural driver is not consumer preference alone.

It is the fact that fewer than 100 industrial composting facilities in the United States accept certified compostable packaging, making home compostable formats the only certified end-of-life pathway that does not depend on infrastructure most consumers cannot access.

4. The gap between certification and real-world outcome is the market’s most important unresolved problem.

Certification confirms performance under controlled conditions.

Real home compost heaps are variable.

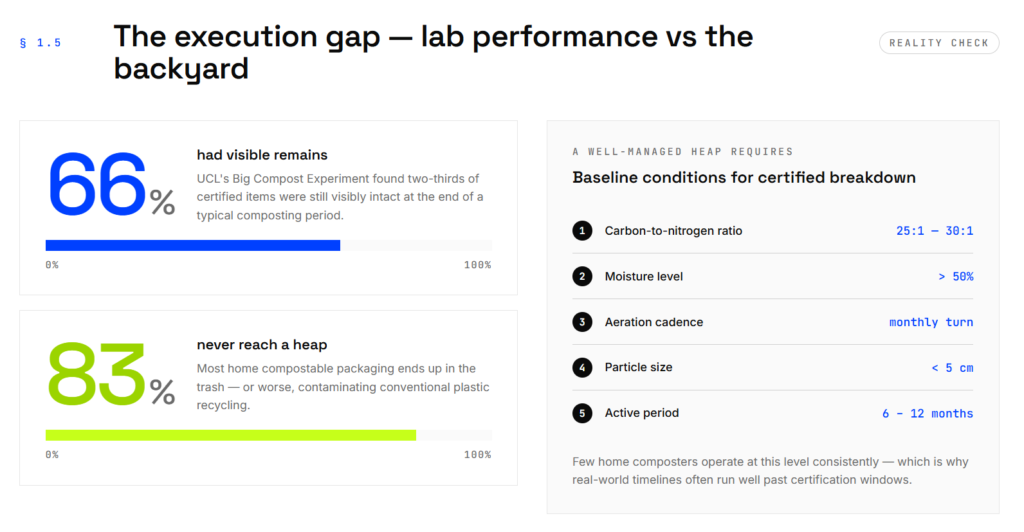

Research from University College London found that 66% of certified home compostable items still had visible remains at the end of a typical composting period, and an estimated 83% of home compostable packaging never reaches a compost system at all.

The label exists. The disposal behavior does not reliably follow.

Closing this gap requires clearer on-pack labeling, consumer education, and product design that makes correct disposal straightforward rather than instructional.

5. Investment and M&A activity confirm commercial confidence, but the Danimer Scientific bankruptcy is a direct warning about capital structure risk.

The sector has attracted multi-billion-dollar consolidation deals including Amcor’s USD 8.4 billion acquisition of Berry Global and CD&R’s USD 10.3 billion purchase of Sealed Air, alongside infrastructure-scale investments in PLA and PHA production across the UAE, Thailand, and India.

At the same time, Danimer Scientific, once valued at USD 890 million as a leading PHA producer, filed for Chapter 11 bankruptcy in March 2025 and sold its assets for USD 19 million.

Technical leadership does not guarantee commercial viability.

The path from certified material to revenue at scale is longer and more capital-intensive than early projections in this sector have consistently assumed, and investment theses need to account for that timeline explicitly.

Introduction and Framework

About This Report

The State of Home Compostable Packaging: Global Report 2025 is published by Ukhi, a biopolymer materials company focused on developing agricultural residue-based compounds for certified home compostable applications.

This report was produced to give brands, investors, procurement teams, and packaging developers a clear, technically grounded account of where the home compostable packaging market stands today.

The market is growing quickly and attracting significant capital and regulatory attention.

It is also generating a substantial volume of imprecise claims.

The purpose of this report is to cut through that noise: to define terms carefully, present the certification landscape accurately, assess which materials genuinely qualify, map the commercial landscape, and give an honest account of what the barriers to scale actually are.

This report does not advocate for any specific product, supplier, or certification body.

Where Ukhi’s own work is referenced, it is identified as such.

Scope and Boundaries

This report covers home compostable packaging specifically.

It does not cover industrial composting, recycling, or biodegradable materials that do not meet home compostability certification standards, except where those distinctions are necessary to clarify what home compostability is and is not.

The scope includes:

- Materials: Bio-resins (PHA, starch blends, PLA variants), natural fiber formats (bagasse, molded pulp, kraft paper), and emerging materials at the technical frontier

- Product categories: Foodservice disposables, flexible packaging, rigid formats, consumer goods, and personal care packaging

- Certification standards: AS 5810 (Australia and New Zealand), OK Compost HOME (TÜV Austria), NF T 51-800 (France), and the BPI Home Compostability Standard (North America)

- Geographies: Global coverage, with focused analysis on Europe, North America, Asia-Pacific, and Australia

- Value chain: Upstream resin producers, midstream converters, downstream brand owners, and enabling infrastructure

- Commercial and investment activity: M&A activity, venture capital, and infrastructure investment through 2025

The report does not cover home compostable packaging for agricultural or medical applications in depth, nor does it assess packaging formats where no certified home compostable alternative currently exists at commercial scale.

Methodology

This report is based on a structured review of publicly available technical literature, certification body documentation, regulatory texts, market data, and commercial disclosures published through the end of 2025.

Technical sources include test protocols and guidance published by TÜV Austria, the Australasian Bioplastics Association, DIN CERTCO, and BPI, as well as peer-reviewed research on biopolymer degradation kinetics and life cycle assessment data.

Regulatory sources include the full texts of the EU Packaging and Packaging Waste Regulation, France’s AGEC law, California SB 54, and India’s single-use plastic ban, alongside enforcement decisions published by the UK Advertising Standards Authority and the EU.

Market data is drawn from published forecasts by Fortune Business Insights, Mordor Intelligence, Grand View Research, and Towards Packaging, cross-referenced where multiple projections are available.

Company and product information is drawn from public disclosures, certification databases maintained by TÜV Austria and BPI, and announced investment and M&A activity reported in trade and financial press.

This report does not present primary survey data or proprietary market research.

It is an analytical synthesis of available information, structured to support informed decision-making rather than to replace primary due diligence.

Home Compostable Packaging — Overview

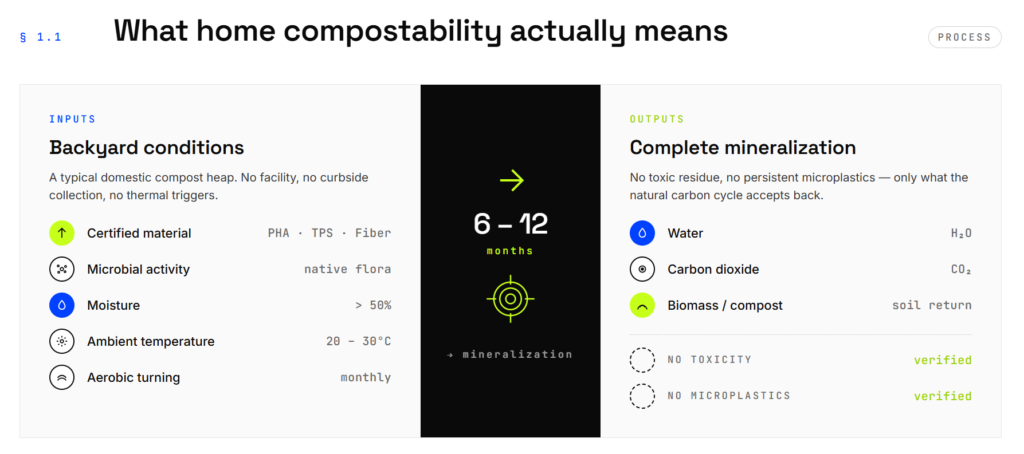

1.1 What Is Home Compostability?

Home compostability is the ability of a material to break down through microbial activity under the conditions of a typical domestic garden compost heap.

No industrial equipment, no controlled facility, and no municipal collection are required for home compostable packaging.

The process relies on naturally occurring microorganisms in a home compost environment, where temperatures typically remain between 20°C and 30°C and moisture levels and microbial communities vary.

The end products are water, carbon dioxide, and biomass (compost), and the timeframe for composting for certified materials is generally 6 to 12 months.

For a product to be genuinely home compostable, it must meet this outcome without leaving behind toxic residues or persistent microplastics.

The claim is specific, measurable, and testable, which is why certification standards exist to verify it.

Definition: Home compostability is not a general environmental claim.

It is a performance standard defined by temperature, time, biodegradation rate, and ecotoxicity outcomes, verified under standardized test protocols.

1.2 How Home Compostable Differs from Related Terms

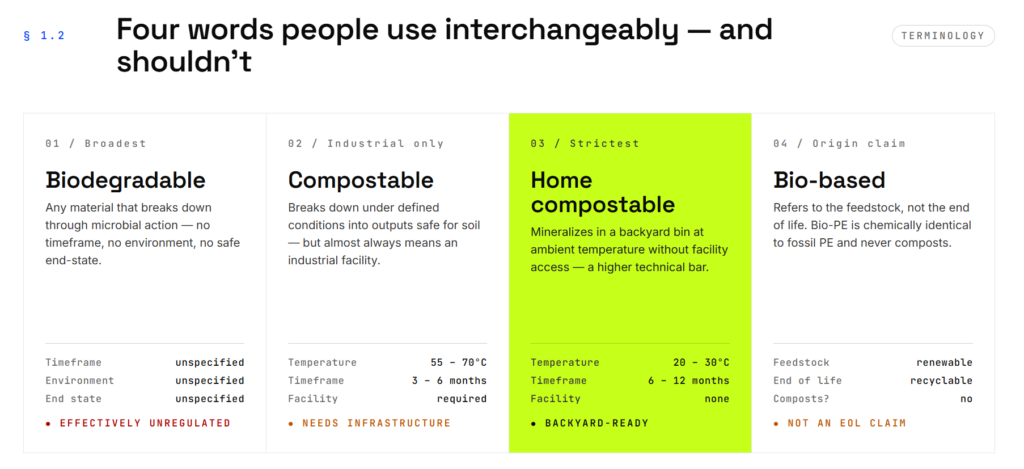

The language around sustainable packaging is crowded and imprecise.

Four terms are frequently confused: biodegradable, compostable, home compostable, and bio-based.

Each means something different, and conflating them creates real problems for consumers, brands, and regulators.

Biodegradable vs. Compostable

Biodegradable is a broad term describing any material capable of breaking down through microbial action.

It does not specify a timeframe, an environment, or a safe end state.

A conventional plastic bag, given enough time and conditions, is technically biodegradable.

The term is effectively unregulated in most markets, which is why it has become a vehicle for greenwashing.

Compostable is a more precise subcategory.

It requires a material to break down within a defined period, under defined conditions, and into outputs that are safe for soil.

Compostable claims are tied to measurable test standards.

Home Compostable vs. Industrially Compostable

This is the most consequential distinction for end-of-life outcomes.

Industrial composting takes place in managed facilities where temperatures are sustained at 55°C to 70°C.

These conditions allow materials like PLA (polylactic acid), the most widely used compostable bioplastic, to break down relatively quickly.

PLA will not meaningfully degrade in a home compost heap.

It requires industrial heat to do so.

Home compostable materials must function at ambient temperatures, without any infrastructure support.

This is a fundamentally harder technical bar to clear, and it is why far fewer materials currently qualify.

Insight: A product labeled “compostable” is not necessarily home compostable.

In most cases, it is industrially compostable only, meaning it requires a specialist facility to break down correctly.

Without that facility, it may sit intact in a home compost bin, or contaminate conventional plastic recycling if disposed of incorrectly.

Bio-based vs. Compostable

Bio-based describes the origin of a material, not its end-of-life behavior.

A material made from corn starch or sugarcane is bio-based, but bio-based does not mean biodegradable or compostable.

Bio-PE (bio-based polyethylene), for example, is chemically identical to fossil-based PE.

It is manufactured from renewable feedstocks, but it is not biodegradable and should be recycled, not composted.

The distinction matters because brands sometimes use bio-based language in ways that imply environmental end-of-life benefits that do not exist.

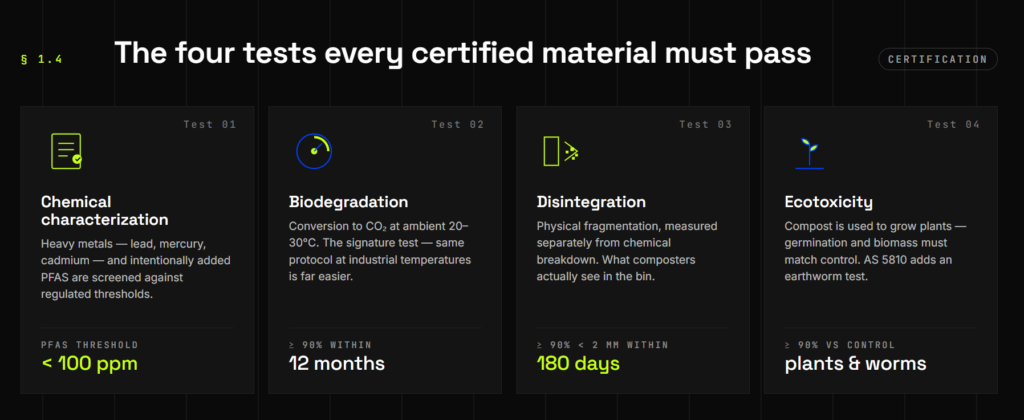

1.3 The Four Tests Every Home Compostable Product Must Pass

Certification as home compostable is not self-declared.

It is earned through a set of standardized laboratory tests that assess performance across four dimensions.

Passing all four is a prerequisite for certification under standards including OK Compost HOME (TÜV Austria), AS 5810 (Australia and New Zealand), and NF T 51-800 (France).

Test 1: Chemical Characterization

The product is screened for heavy metals including lead, mercury, and cadmium, which must remain below regulated thresholds.

Increasingly, standards also require testing for PFAS (per- and polyfluoroalkyl substances), a group of synthetic chemicals associated with persistence in soil and linked to health risks, to ensure they are not present above permitted levels.

Test 2: Biodegradation

This test measures the rate at which the material converts into carbon dioxide under home composting temperatures of 20°C to 30°C.

The threshold is 90% biodegradation within 12 months.

This is the core chemical breakdown test and the one that most sharply distinguishes home compostable materials from industrial-only alternatives, since the same test conducted at industrial temperatures is considerably easier to pass.

Test 3: Disintegration

Physical fragmentation is assessed separately from chemical breakdown.

The material must fragment into pieces smaller than 2mm, with at least 90% of the sample reaching this size within 180 days under home composting conditions.

This matters because a material can be chemically degrading while still appearing physically intact, which is what consumers and composters actually observe.

Test 4: Ecotoxicity

The compost produced during testing is used to grow plants.

Seed germination rates and plant biomass must reach at least 90% of a control sample to confirm the resulting compost is not phytotoxic.

The Australian AS 5810 standard goes further by including a mandatory earthworm toxicity test, verifying that the material does not harm soil macro-fauna as it breaks down.

Stat: Under AS 5810, materials must pass earthworm toxicity testing in addition to plant growth tests, making it one of the most ecologically rigorous home compostability standards currently operating at a national level.

1.4 The End-of-Life Reality of Home Composting Packaging

Certification confirms what a material can do under controlled conditions.

Real-world outcomes depend heavily on how composting is actually practiced at home.

What a Well-Managed Composting Heap Requires

For certified packaging to break down within its stated timeframe, a home compost system needs to meet certain baseline conditions:

- Carbon-to-Nitrogen ratio: 25:1 to 30:1 to sustain active microbial communities

- Moisture levels: consistently above 50%

- Aeration: turning the pile at least once a month to maintain aerobic conditions

- Particle size: packaging shredded or torn into pieces smaller than around 5cm to increase surface area available for microbial action

Most home composters do not operate at this level consistently.

Temperature varies with seasons.

Moisture is rarely monitored.

Aeration is often irregular.

These variables mean real-world breakdown times can extend well beyond the 6 to 12 months that certification standards are built around.

The Execution Gap

Laboratory performance and consumer reality diverge significantly.

A University College London study found that 66% of tested items still had visible remains at the end of a typical composting period.

The materials were certified; the conditions were simply not controlled enough to replicate laboratory performance.

The disposal routing problem compounds this further.

An estimated 83% of home compostable packaging does not reach a home compost system at all.

It ends up in the trash or, more problematically, in the conventional plastic recycling stream, where it can cause contamination and processing difficulties.

Insight: The execution gap is the central challenge for home compostable packaging as a system.

Certification is a necessary condition for a viable product, but it is not a sufficient one.

Consumer education, unambiguous labeling, and product design that actually supports home use are all part of what determines whether a certified product delivers its intended outcome.

1.5 Why Home Compostability Matters

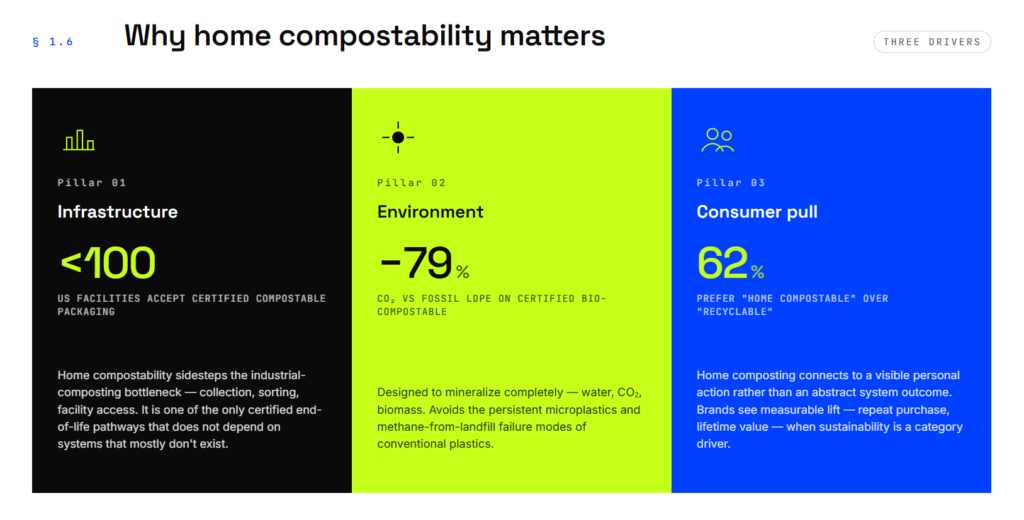

The Infrastructure Problem It Solves

Industrial composting infrastructure is limited in most markets.

In the United States, fewer than 100 facilities currently accept certified compostable packaging.

Many municipal programs exclude compostable plastics entirely because they are difficult to distinguish from conventional plastics on sorting lines and can contaminate recycling streams if misrouted.

Home compostability sidesteps this bottleneck.

It does not depend on curbside collection, specialist sorting equipment, or facility access.

For brands operating in regions without industrial composting infrastructure, which is most regions globally, home compostable formats represent one of the only certified end-of-life pathways currently available that does not rely on systems that largely do not exist.

This is a structural driver of category growth.

The home compostable packaging sector is expanding at a CAGR of approximately 20%, in part as a direct consequence of the inadequacy of industrial composting infrastructure.

The Environmental Case

Life cycle assessments indicate that certified compostable bioplastics can generate up to 79% lower carbon emissions than fossil-based LDPE on a per-unit basis.

Bio-based feedstocks such as corn and sugarcane act as temporary carbon sinks during growth, partially offsetting production emissions.

Certified home compostable materials are designed to mineralize completely into water, carbon dioxide, and biomass.

This prevents the accumulation of persistent microplastics in soil and waterways, a primary environmental failing of conventional plastics, many of which take over 450 years to degrade and shed microplastic particles throughout that process.

Aerobic decomposition in a compost heap also avoids the methane emissions produced when organic waste decomposes anaerobically in landfill.

Methane is a greenhouse gas significantly more potent than carbon dioxide over a 20-year period, making landfill diversion one of the clearest environmental arguments for compostable packaging done well.

What Consumer Behavior Tells Us

Around 62% of consumers say they prefer packaging labeled “home compostable” over “recyclable,” connecting it to a personal and visible environmental action rather than an abstract system outcome.

More than 54% of consumers report actively choosing products based on sustainable packaging, and 70% say clearer disposal labeling would improve how they handle packaging at end of life.

For brands, this translates into measurable commercial outcomes.

Verified home compostable packaging has been associated with a reported USD 20 increase in customer lifetime value and higher repeat purchase rates in categories where sustainability functions as a purchase driver.

Home Compostable Packaging – The Certification Landscape

A home compostable claim is only as credible as the standard behind it.

This chapter maps the four major certification frameworks operating globally, the regulations that now specifically name home compostability as a requirement, and the growing enforcement activity targeting brands that make compostable claims they cannot substantiate.

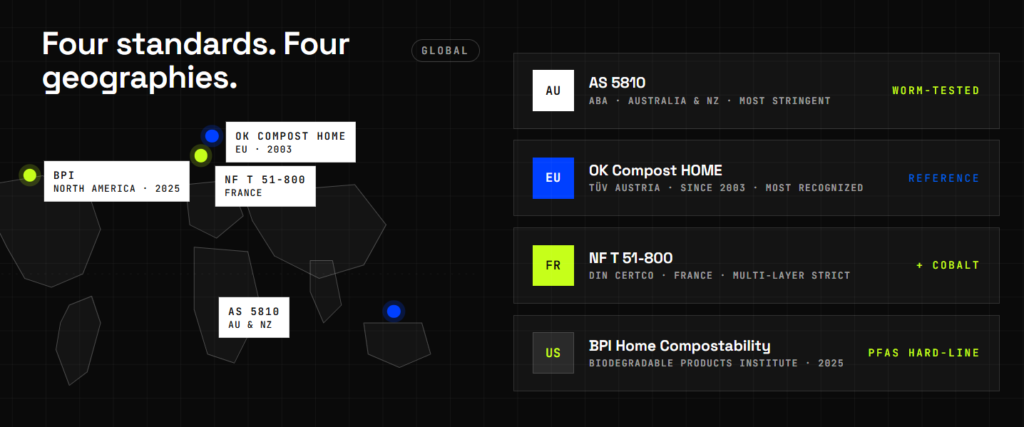

2.1 The Major Standards For Home Compostability

Home compostability certification requires a product to pass independently verified tests for biodegradation, disintegration, and ecotoxicity under ambient temperature conditions.

Four standards currently define what that means in practice, each covering a distinct geography and carrying its own technical specifications.

Definition: A certification standard is not the same as a certification mark.The standard sets the technical requirements.The mark (such as OK Compost HOME or the ABA seedling logo) is what appears on packaging once a product has passed those requirements through an accredited testing body.

AS 5810 (Australia and New Zealand)

AS 5810 is administered by the Australasian Bioplastics Association (ABA) and is widely considered the most stringent home compostability standard in operation globally.

Key requirements:

- Biodegradation: Minimum 90% conversion of carbon to CO2 within 12 months at 20°C to 30°C

- Disintegration: At least 90% of material must fragment into pieces smaller than 2mm within 6 months

- Organic content: Materials must contain more than 50% organic material by mass

- Earthworm toxicity: A mandatory test based on OECD Guideline 207 verifies that breakdown products do not harm soil macro-fauna. No other major home compostability standard currently requires this test.

- Heavy metals and hazardous substances: Must remain below strict permitted limits

The earthworm-safe ecotoxicity requirement is what sets AS 5810 apart.

Most standards verify that compost produced from a material does not harm plants.

AS 5810 also checks what happens to the organisms living in the soil, which is a meaningful additional layer of ecological protection.

OK Compost HOME (TÜV Austria)

Established in 2003 and administered by TÜV Austria, OK Compost HOME was the world’s first certification specifically designed for home compostable packaging.

It remains the most widely recognized home compostability mark in Europe and has served as the technical basis for several standards that followed, including AS 5810 and NF T 51-800.

Key requirements:

- Biodegradation: 90% within 12 months at ambient temperatures of 20°C to 30°C

- Disintegration: 90% of material into fragments smaller than 2mm within 6 months

- Scope: Certification covers not just the primary material but all components including inks, adhesives, additives, and labels. A packaging item cannot carry the mark if any single component fails the test.

The comprehensive component scope is an important detail for brands.

A film that passes may still lose certification if the printing ink on it contains substances that fail ecotoxicity thresholds.

NF T 51-800 (France)

NF T 51-800 is a French national standard that defines specifications for plastics suitable for household composting.

It functions as a primary European household composting standard and forms the technical foundation for the DIN-Geprüft Home Compostable mark managed by DIN CERTCO.

Key requirements:

- Biodegradation: 90% within 12 months at 25°C plus or minus 5°C

- Disintegration: 90% physical fragmentation within 180 days

- Heavy metals: Includes cobalt as a regulated substance, which OK Compost HOME does not. This makes NF T 51-800 more protective in certain chemical categories.

- Multilayer structures: Offers fewer testing concessions for complex multilayer materials compared to OK Compost HOME, meaning composite packaging formats face a stricter path to certification under this standard.

The French regulatory environment has given NF T 51-800 particular commercial relevance.

France’s AGEC law (Anti-Waste for a Circular Economy) actively encourages the adoption of home compostable alternatives for retail and takeaway packaging, and NF T 51-800 certified products are well positioned to meet those requirements.

BPI Home Compostability Standard (North America)

Launched in September 2025 and administered by the Biodegradable Products Institute (BPI), the BPI Home Compostability Standard is the first formal home compostability certification designed specifically for the North American market.

Applications opened on December 1, 2025.

Key requirements:

- Technical basis: Built primarily on the NF T 51-800 framework, with adaptations for the North American regulatory context

- Biodegradation and disintegration: 90% biodegradation within 12 months and physical disintegration within 180 days, consistent with NF T 51-800

- PFAS: Zero tolerance for intentionally added PFAS (per- and polyfluoroalkyl substances), with a strict threshold of 100 ppm total fluorine for the finished product

Insight: The BPI standard was created in direct response to the infrastructure gap.

Only 36% of U.S. residents have access to curbside composting.

By creating a credible home compostability certification for North America, BPI is giving brands and consumers a viable certified end-of-life route that does not depend on industrial composting facilities that most Americans cannot access.

Standards Comparison

| Requirement | AS 5810 (AU/NZ) | OK Compost HOME | NF T 51-800 / BPI |

|---|---|---|---|

| Administering Body | ABA | TÜV Austria | DIN CERTCO / BPI |

| Biodegradation Time | 12 months | 12 months | 12 months |

| Disintegration Time | 6 months | 6 months | 180 days |

| Temperature Range | 20 to 30°C | 20 to 30°C | 25 plus or minus 5°C |

| Ecotoxicity Scope | Plants and earthworms | Plants | Plants |

| Additional Heavy Metal | Not specified | Not specified | Cobalt |

| PFAS Restrictions | Yes | Yes | Yes (strict 100 ppm limit for BPI) |

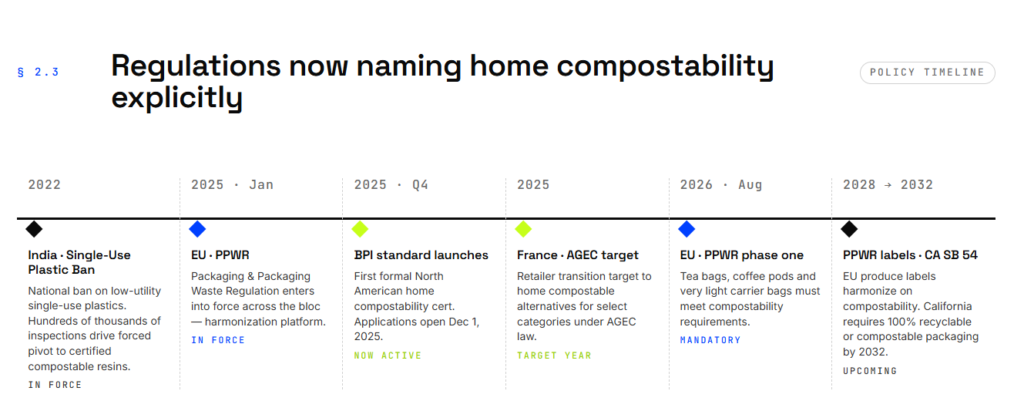

2.2 Global Regulations That Reference Home Composting

Legislation is moving beyond general composting mandates and beginning to distinguish explicitly between industrial and home compostability.

This shift has direct implications for which products can make which claims and in which markets.

European Union: Packaging and Packaging Waste Regulation (PPWR)

The EU Packaging and Packaging Waste Regulation (PPWR), which entered into force in early 2025, is the most significant harmonization effort underway.

Key timelines:

- From August 2026: Tea bags, coffee pods, and very lightweight plastic carrier bags must meet compostability requirements

- From 2028: Compostable labels for fresh produce must meet harmonized industrial composting standards, while individual member states retain the option to mandate home compostability for these labels depending on local waste infrastructure

The PPWR deliberately leaves the home versus industrial question partly to member states because waste infrastructure varies significantly across the EU.

Countries with limited industrial composting capacity are more likely to mandate home compostable formats.

France: AGEC Law

France’s AGEC law sets a target for retailers to transition to home compostable alternatives by 2025 for certain packaging categories, aligned with France’s decentralized biowaste management approach.

NF T 51-800 certified products are the natural solution for brands operating in this market.

Australia: FOGO and State-Level Policy

Australia has established the Food Organics and Garden Organics (FOGO) collection program alongside its rigorous AS 5810 standard.

However, there is real tension at the municipal level.

Several local councils and state EPAs have introduced caution or outright exclusions for compostable packaging in residential organics streams, citing the risk of contamination and the challenge of distinguishing certified compostable materials from conventional plastic in sorting.

This means that despite having one of the world’s toughest home compostability standards, the practical end-of-life pathway for home compostable packaging in Australia is not straightforward, and the regulatory picture varies by state and council.

United States: California SB 54 and State-Level Activity

California SB 54 requires all packaging sold in California to be 100% recyclable or compostable by 2032.

Critically, any product labeled “Home Compostable” in California must meet OK Compost HOME certification requirements.

This sets a specific certification bar for home compostability claims rather than leaving the term open to self-declaration.

India: Single-Use Plastic Ban

India’s 2022 national ban on low-utility single-use plastics has created a significant forced pivot toward certified compostable resins in the market.

Enforcement activity has included hundreds of thousands of inspections targeting non-compliant imports, which makes certification a practical commercial requirement for brands selling into India, not just a voluntary credential.

2.3 Home Compostable Packaging – Greenwashing and Enforcement

Regulators across multiple jurisdictions are tightening the rules around environmental claims, and compostability is one of the most actively scrutinized areas.

The shift is away from accepting self-declared claims and toward requiring specific, certified, same-medium substantiation.

The Scale of the Problem

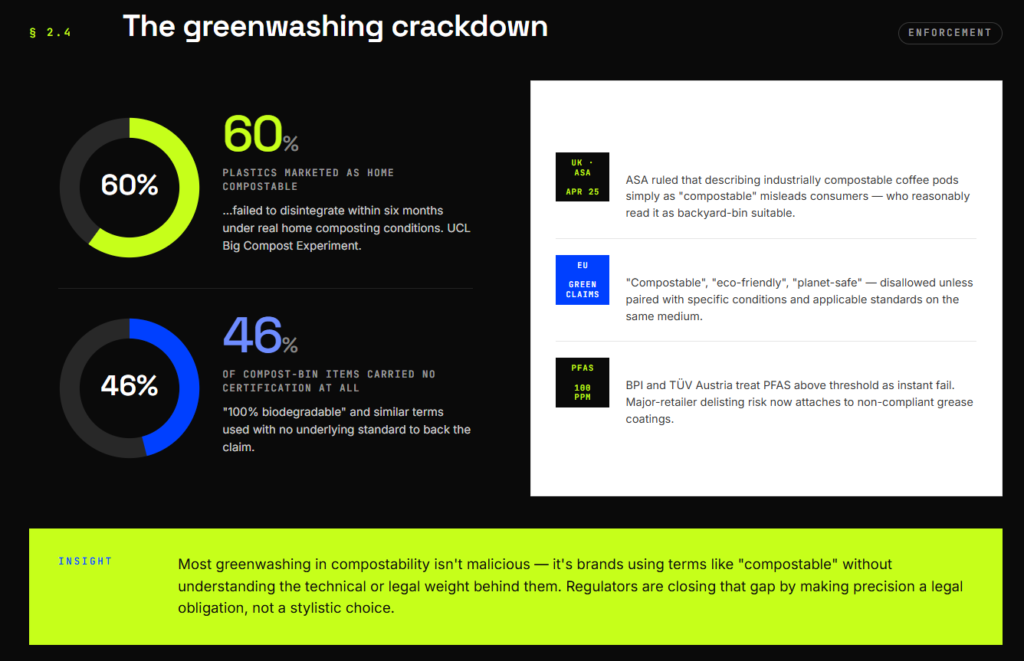

Research from University College London’s Big Compost Experiment found that 60% of plastics marketed as home compostable failed to disintegrate within a typical six-month period under real home composting conditions.

More significantly, 46% of items placed in home compost heaps during the study carried no actual compostability certification.

They used terms like “100% biodegradable” with no standard behind them.

Regulator and Watchdog Action

Enforcement in the home compostability packaging space is becoming concrete:

- UK ASA ruling (April 2025): The UK Advertising Standards Authority banned advertising for Lavazza and Dualit coffee products. Both brands had described their coffee pods as “compostable” without specifying that this required industrial composting. The ASA ruled that consumers reasonably interpret “compostable” to mean suitable for a home compost bin. Describing industrially compostable products simply as “compostable” was found to be misleading.

- EU Green Claims Directive: Generic terms such as “compostable,” “eco-friendly,” or “planet-safe” are now prohibited in the EU unless accompanied by specific conditions and applicable standards stated on the same medium as the claim. A compliant label must now read something like: “Industrially compostable per EN 13432, not suitable for home composting.”

Financial Consequences of Greenwashing

Under the EU Empowering Consumers Directive, non-compliance with green claims rules can result in administrative fines of at least 4% of annual EU turnover or EUR 2 million, whichever is higher.

In Italy, the national competition authority ceiling for violations reaches EUR 10 million.

Penalties can also include revenue confiscation and exclusion from public procurement.

The PFAS Threshold as a Disqualifier

Certification bodies including BPI and TÜV Austria now treat PFAS contamination as a hard disqualifier.

Any material exceeding the 100 ppm total fluorine threshold cannot be certified or marketed as compostable.

This is increasingly relevant for packaging formats that have historically used fluorinated coatings for grease resistance, including some paperboard and molded fiber products.

Brands that fail to validate compliance with evolving PFAS limits face delisting risk from major retailers alongside regulatory exposure.

Insight: The greenwashing enforcement trend is not primarily about bad actors making knowingly false claims.

A significant share of the problem comes from brands using terms like “compostable” or “biodegradable” without understanding the technical and legal requirements behind them.

The regulatory shift toward mandatory same-medium substantiation is designed to close that gap by making precision a legal obligation rather than a voluntary choice.

3. Home Compostable Packaging – Material Profiles

Not all materials that carry sustainability claims can break down in a home compost heap.

The conditions in a backyard bin are fundamentally different from those in an industrial facility, and most of the packaging formats currently marketed as compostable are designed for industrial processing, not home systems.

This chapter sets out which materials genuinely qualify as home compostable.

3.1 The Core Technical Constraint: Why Home Composting Is a Harder Bar to Clear

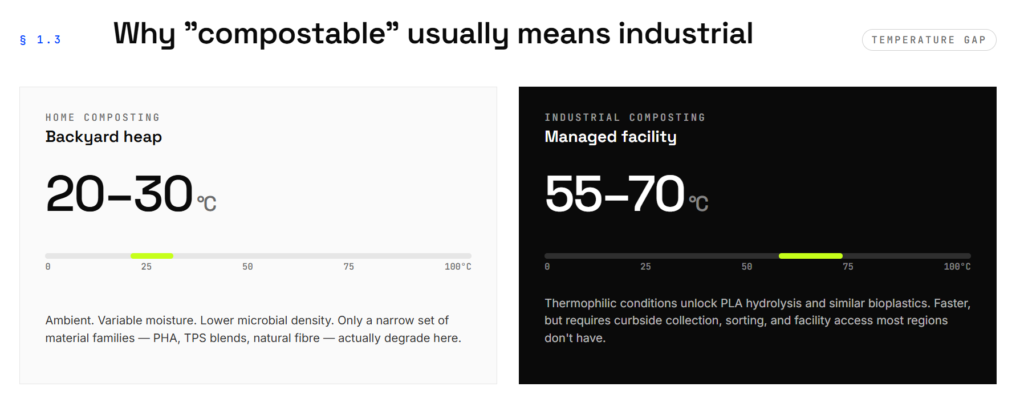

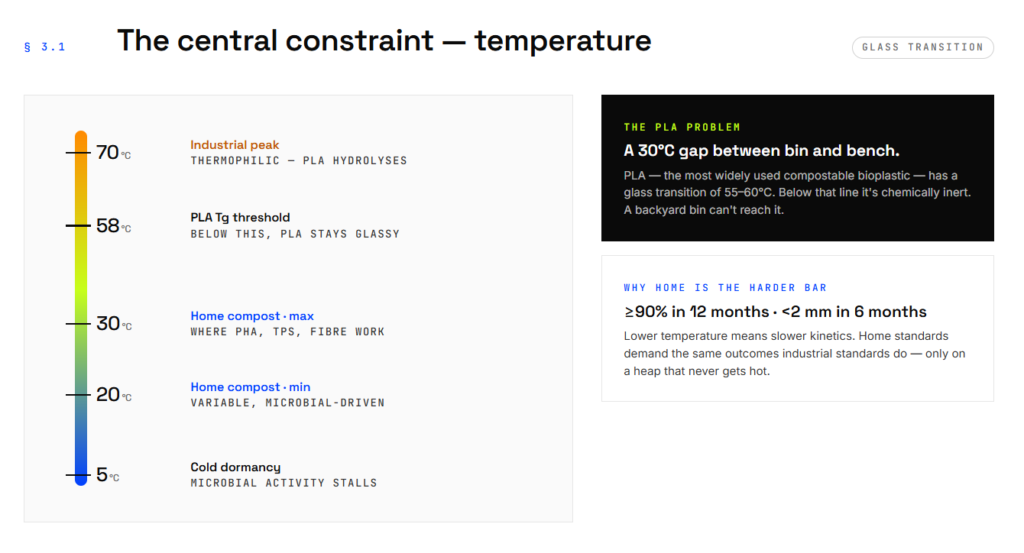

The central problem is temperature.

Home composting operates at ambient conditions, typically between 20°C and 30°C, with variable moisture and lower microbial density than a managed industrial facility.

Industrial composting sustains temperatures of 55°C to 70°C, driven by thermophilic bacteria that thrive only at high heat.

That temperature gap determines which materials can degrade and which cannot.

Most synthetic bioplastics are engineered to be chemically stable under ambient conditions to maintain product shelf life.

This stability is what makes them useful as packaging.

It is also what makes them inert in a home compost heap.

The Glass Transition Problem

Standard PLA (polylactic acid), the most widely used compostable bioplastic globally, has a glass transition temperature (Tg) of 55°C to 60°C.

Below this threshold, PLA remains rigid and chemically inactive.

The hydrolysis process that breaks PLA down into lactic acid requires sustained heat above this point, which a home bin cannot reliably provide.

At home composting temperatures, PLA does not degrade.

It sits unchanged.

Definition: Glass transition temperature (Tg) is the point at which a polymer shifts from a rigid, glassy state to a softer, more pliable state.

For PLA, this threshold is around 55°C to 60°C.

Home compost heaps do not reach this temperature, which is why standard PLA cannot break down in them.

Because biodegradation kinetics are slower at lower temperatures, certification standards for home compostability are stricter than industrial ones.

A material must achieve 90% biodegradation within 12 months and physical disintegration within 6 months at ambient temperatures.

The equivalent industrial thresholds are 6 months and 3 months respectively.

The practical implication is that only a narrow set of material families can meet this bar.

Each is covered below.

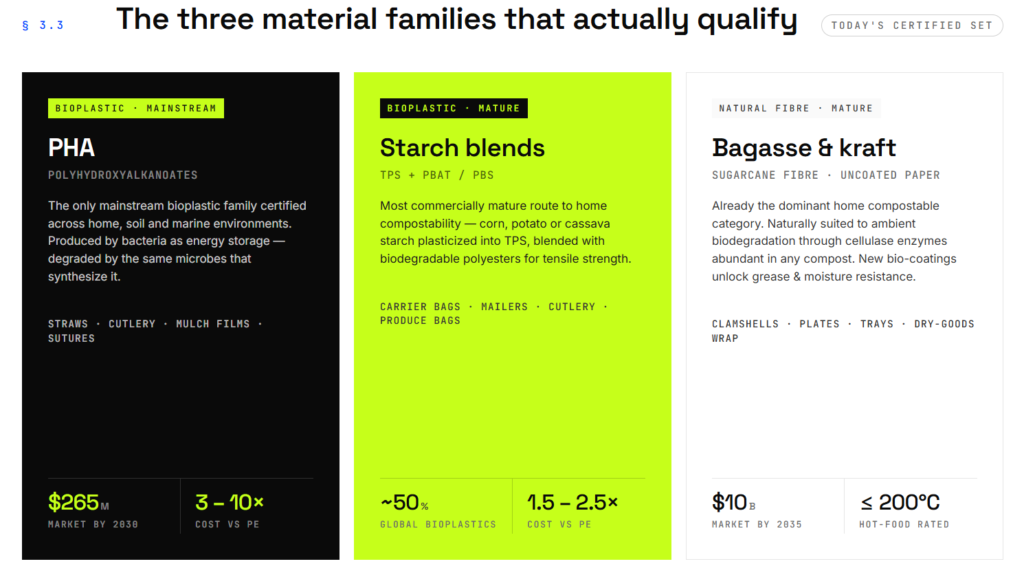

3.2 PHA (Polyhydroxyalkanoates): The Only Mainstream Bioplastic That Is Genuinely Home Compostable

PHA (polyhydroxyalkanoates) is a family of bio-polyesters produced naturally by bacteria as intracellular energy storage granules.

It is currently the only mainstream bioplastic family that is certified for home compostability, soil biodegradability, and marine biodegradability across virtually all biologically active environments.

Unlike synthetic bioplastics, PHA does not require an industrial thermal trigger to break down.

The same microorganisms that synthesize PHA in nature also produce the enzymes (PHA depolymerases) needed to degrade it, which is why it mineralizes effectively at ambient temperatures.

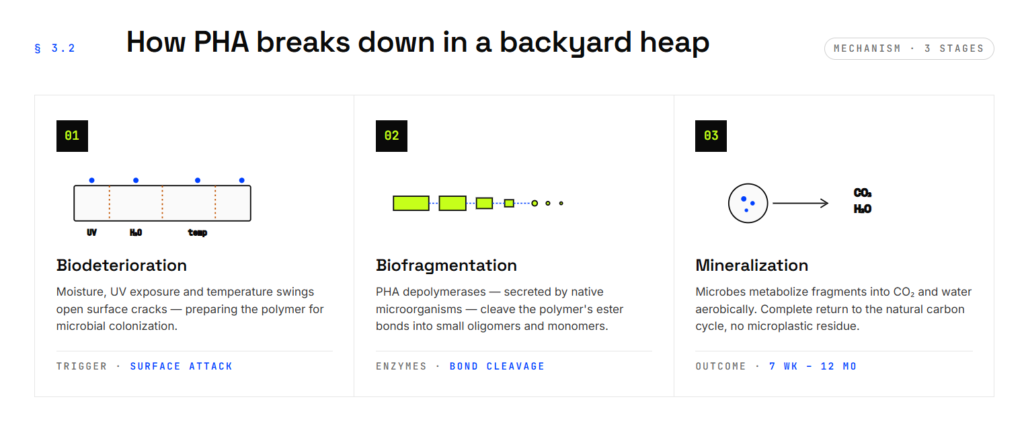

The Degradation Process

The degradation process moves through three stages:

- Biodeterioration: Moisture, UV exposure, and temperature fluctuation cause surface cracking, which enables microbial colonization

- Biofragmentation: Extracellular enzymes cleave the polymer’s ester bonds, reducing it to small oligomers and monomers

- Mineralization: Microorganisms metabolize these fragments into carbon dioxide and water under aerobic conditions

In a well-managed home compost heap at 20°C to 30°C, PHA typically fully biodegrades within 3 to 12 months.

Under favorable conditions, complete mineralization can occur in as little as 7 weeks.

The specific copolymer structure matters: PHBV (polyhydroxybutyrate-valerate) degrades faster than pure PHB (polyhydroxybutyrate) because lower crystallinity gives enzymes easier access to the polymer backbone.

Market Position and Commercial Constraints

PHA remains in the early stages of mass commercialization.

The global PHA market is projected to grow from USD 123.8 million in 2025 to USD 265.2 million by 2030, with production volumes expected to rise from around 59 kilotons in 2026 to over 170 kilotons by 2031.

The primary commercial barrier is cost.

PHA currently prices between USD 4 and USD 7 per kilogram, roughly 3 to 10 times the cost of conventional polyethylene.

Processing is also more demanding than for standard resins: PHA has a narrow thermal processing window and can degrade if held at elevated temperatures for too long during manufacturing, often requiring 9 to 15 months for customer onboarding and equipment calibration.

Stat: PHA costs 3 to 10 times the price of conventional PE.

Despite this, the market is growing at a CAGR of 16.5%, driven by brands seeking certified home and marine compostable formats that perform in real-world disposal conditions.

Current applications include food service items (straws, coffee lids, cutlery), agricultural mulch films that can be tilled directly into soil after harvest, and biomedical uses such as absorbable sutures and drug delivery systems.

3.3 Starch-Based Blends: The Most Cost-Effective Route to Home Compostability

Starch-based blends are the most commercially mature and widely produced home compostable bioplastic format.

They currently account for approximately 50% of global bioplastics production and represent the most economically accessible route to certified home compostability.

Pure starch is a natural polysaccharide derived from crops including corn, potato, and cassava.

In its unmodified form it is moisture-sensitive and brittle.

To make it processable as packaging, it is converted into thermoplastic starch (TPS) using plasticizers such as glycerol and sorbitol, then physically blended with biodegradable polyesters like PBAT (polybutylene adipate terephthalate) or PBS (polybutylene succinate) to provide the tensile strength and flexibility needed for practical use.

Specialized TPS blend grades, such as AGENACOMP and certain TPS-PBAT formulations, hold OK Compost HOME certification and are verified to degrade under ambient conditions.

Microorganisms treat starch as a primary energy source, and use amylase enzymes to break down its glycosidic bonds.

Thin-film starch-based products (around 15 micrometers) can visibly degrade within 2 weeks and fully compost within 4 weeks at temperatures at or below 28°C.

The starch-blended bioplastic market is estimated at USD 335.9 million in 2025 and is projected to reach USD 532.8 million by 2035.

Cost premium is moderate at 1.5 to 2.5 times conventional resin pricing, substantially lower than PHA.

Primary applications are high-volume, short-life flexible formats: supermarket carrier bags, produce bags, courier mailers, and disposable cutlery.

3.4 Natural Fiber Formats: The Most Commercially Mature Home Compostable Packaging

Natural fiber formats are the most established category of home compostable packaging and the most straightforward from a certification standpoint.

They are naturally suited to ambient biological degradation and do not require synthetic polymer engineering to achieve compostability.

The two primary formats are:

- Molded sugarcane bagasse: The fibrous residue left after sugarcane juice extraction, containing 32% to 45% cellulose and 20% to 32% hemicellulose.

- Uncoated kraft paper: High-strength paper derived from wood pulp, naturally suited to ambient biodegradation and widely certified for home composting.

Bagasse can withstand temperatures up to 200°C, which makes it suitable for hot food applications, while still breaking down naturally in home compost through the action of cellulase and wood-degrading enzymes that are abundant in standard compost environments.

It is the dominant format for food service clamshells, plates, bowls, and airline meal trays.

Used primarily for dry goods and retail packaging.

The global molded fiber market is projected to grow from USD 5.5 to 6.2 billion in 2025 to USD 10 billion by 2035, reflecting the scale at which these formats already operate.

A significant active development in this space is the integration of home compostable bio-coatings onto kraft paper and bagasse substrates.

Coatings such as BASF’s ecovio provide grease and moisture resistance, enabling these natural fiber formats to replace plastic-lined cups and trays without sacrificing compostability.

Insight: Natural fiber formats are frequently the first choice for food service operators making the switch to home compostable packaging, not only because they are well-certified and cost-effective, but because consumers recognize them as visibly natural and are more confident disposing of them correctly.

3.5 What Does Not Qualify as Home Compostable

A substantial portion of packaging sold as “compostable” does not qualify for home composting.

This gap between label and performance is one of the central issues in the market.

Standard PLA

Standard PLA is not home compostable.

As described in section 3.1, it requires industrial heat above 58°C to begin hydrolysis.

In a home compost heap, a PLA cup or fork can remain physically unchanged for decades.

In marine environments, PLA showed zero measurable degradation after 428 days submerged in seawater.

PLA is used extensively for rigid packaging, cups, cold drink lids, and 3D printing.

It is genuinely compostable, but only under industrial conditions.

Most consumers do not have access to the industrial composting facilities required.

PBAT Without Adequate Blending

PBAT is a fossil-based biodegradable polyester widely used to add flexibility to starch-based blends.

On its own, without specific modification or adequate blending ratios, it does not reliably pass home compostability certification requirements.

In some configurations, PBAT-heavy blends carry a risk of fragmentation into persistent particles if the biodegradation process is not fully managed.

The Infrastructure Mismatch

In the United States, fewer than 5% of households have access to industrial composting collection or drop-off.

For most consumers, an industrially compostable item ends in a landfill, where it behaves like conventional plastic and can take up to 1,000 years to decompose.

Many industrial composting facilities also actively reject PLA-based products on sorting lines because they are visually indistinguishable from conventional plastics, creating contamination risk.

Insight: The label “compostable” without further qualification means industrially compostable in the vast majority of cases.

Brands using that term without specifying the required conditions are now facing regulatory exposure under the EU Green Claims Directive, California AB 1201, and equivalent frameworks in multiple other markets.

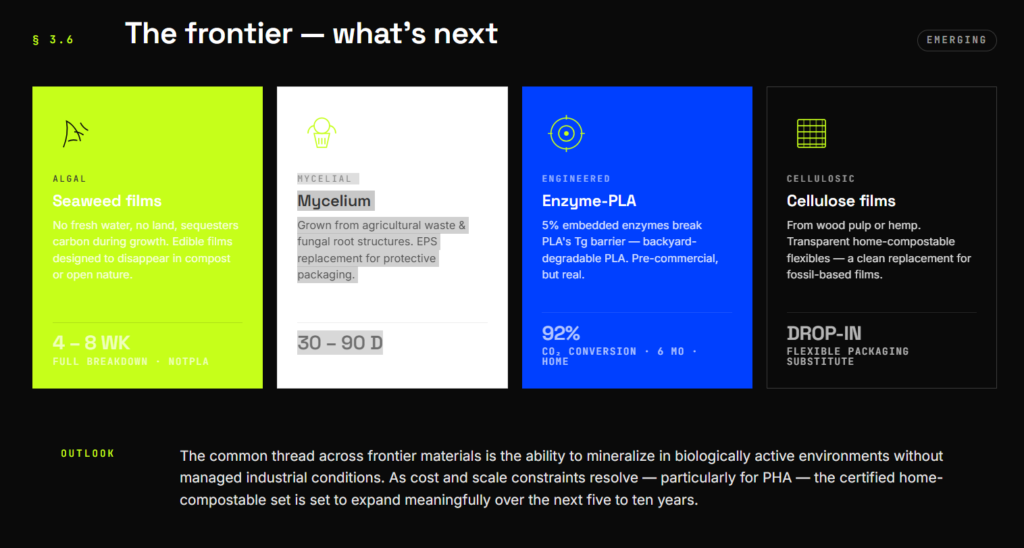

3.6 The Frontier: Emerging Home Compostable Materials

Beyond PHA and starch, a set of emerging materials is extending what is technically possible in home compostable formats.

- Seaweed-based biopolymers: Seaweed requires no fresh water, no arable land, and sequesters carbon during growth, making it a carbon-negative feedstock.

- Mycelium-based composites: Grown from agricultural waste and fungal root structures, mycelium composites are used as a sustainable alternative to expanded polystyrene (EPS) for cushioning and protective packaging.

- Enzyme-embedded PLA: Experimental formulations embed microbial enzymes directly into the PLA polymer matrix to overcome the Tg barrier at ambient temperatures.

- Cellulose-based films: Derived from wood pulp or hemp, these are available as home compostable transparent films and paperboard substrates, offering an alternative to fossil-based flexible film formats.

Companies including Notpla have commercialized seaweed films that are edible and designed to fully disappear in home compost or open nature within 4 to 8 weeks.

They are 100% home compostable and typically break down within 30 to 90 days.

In documented tests, PLA lids containing 5% enzyme concentration achieved 92% carbon conversion to CO2 within 6 months under backyard conditions.

Standard PLA in the same test showed zero measurable degradation.

This technology is not yet commercially scaled but represents a potential path to making PLA viable for home composting.

The common thread across frontier materials is the ability to mineralize in biologically active environments without requiring managed industrial conditions.

As cost and scale constraints are resolved, particularly for PHA, the range of certified home compostable formats available to brands is set to expand meaningfully over the next five to ten years.

4. Home Compostable Packaging – The Product Landscape

Home compostable packaging has moved well beyond simple fiber plates and paper bags.

Across foodservice, flexible packaging, and consumer goods, a commercially significant product ecosystem of compostable packaging exists now and spans certified high-barrier films, enzymatic biopolymers, and specialty coatings.

This chapter maps what is currently available, who is producing it, and where meaningful product gaps remain.

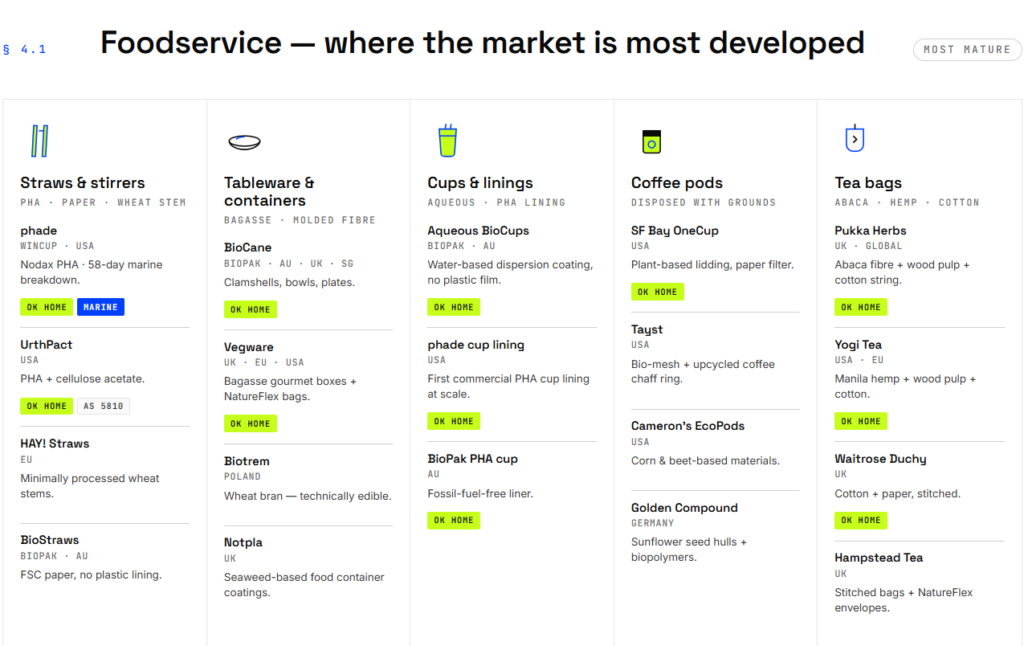

4.1 Home Compostable Foodservice Disposables: Where the Market Is Most Developed

Foodservice is the most mature and commercially active category in home compostable packaging.

Legislative bans on single-use plastics across the EU, UK, Australia, and multiple US states have accelerated adoption, and the product range now covers most standard disposable formats.

Straws and Stirrers

PHA-based straws represent the highest-performance option in this subcategory.

- phade straws (WinCup Inc., USA): Manufactured using Nodax PHA, certified for both home composting and marine biodegradation, with documented marine breakdown within 58 days.

- UrthPact straws (USA): Combine PHA and cellulose acetate and hold both OK Compost HOME and AS 5810 certifications.

Natural fiber alternatives include HAY! Straws, made from minimally processed wheat stems, and BioStraws from BioPak (Australia), made from FSC-certified paper without plastic linings.

These formats require no certification chemistry because their base materials are inherently suited to ambient biological degradation.

Tableware and Takeaway Containers

Sugarcane bagasse dominates this segment.

- BioCane (BioPak, available in Australia, UK, and Singapore): Covers the standard range of clamshells, bowls, and plates.

- Vegware (UK, EU, USA): Offers bagasse gourmet boxes and NatureFlex bags certified for home composting.

- Stealth Health (USA): Produces bamboo and sugarcane meal-prep containers designed for repeated reheating.

Less conventional formats exist at the category edge.

- Biotrem (Poland): Manufactures plates and cutlery from wheat bran that are technically edible.

- Notpla (UK): Applies seaweed-based coatings to food containers, designed to degrade as quickly as fruit peel in home compost.

Cups and Cup Linings

Traditional paper cups rely on thin plastic linings to prevent liquid absorption.

These linings disqualify the cup from home compostability, even when the paper itself is certified.

Two approaches have emerged to solve this:

- Aqueous (water-based) dispersion coatings: BioPak’s Aqueous BioCups eliminate the plastic film entirely, using a water-based coating that allows the full cup to be certified for home composting.

- PHA linings: BioPak (Australia) and phade (USA) have brought the first fossil-fuel-free cup linings to commercial scale in their respective markets.

Insight: The cup lining problem is a useful illustration of a pattern that recurs across home compostable packaging: the primary substrate is often straightforward to certify, but ancillary components including coatings, adhesives, and inks can disqualify an otherwise compliant product.

Full-product certification requires every component to pass, not just the main material.

Coffee Pods and Tea Bags

Home compostability matters particularly in this sector because pods and tea bags are routinely disposed of alongside wet organic waste such as grounds and leaves, which makes a home-compostable end-of-life path practically useful.

Coffee Pods

- San Francisco Bay (USA): OneCup technology uses plant-based lidding and paper filters, certified OK Compost HOME.

- Tayst Coffee (USA): Uses a bio-mesh cup body and a ring made from upcycled coffee chaff (the dried skin of the coffee bean).

- Cameron’s Coffee (USA): EcoPods made from corn and beet-based materials, 100% compostable.

- Golden Compound (Germany): Produces capsules from sunflower seed hulls combined with biopolymers.

Tea Bags

- Pukka Herbs (UK/Global): Abaca fiber, wood pulp, and organic cotton strings, replacing heat-sealed polypropylene.

- Yogi Tea (USA/Europe): Manila hemp and wood pulp bags with organic cotton strings, home compostable certified.

- Waitrose Duchy (UK): OK Compost HOME certified cotton and paper bags.

- Hampstead Tea (UK): Stitched (not heat-sealed) bags with NatureFlex (wood pulp) loose tea envelopes.

4.2 Home Compostable Flexible Packaging and High-Barrier Films: The Most Technically Demanding Format

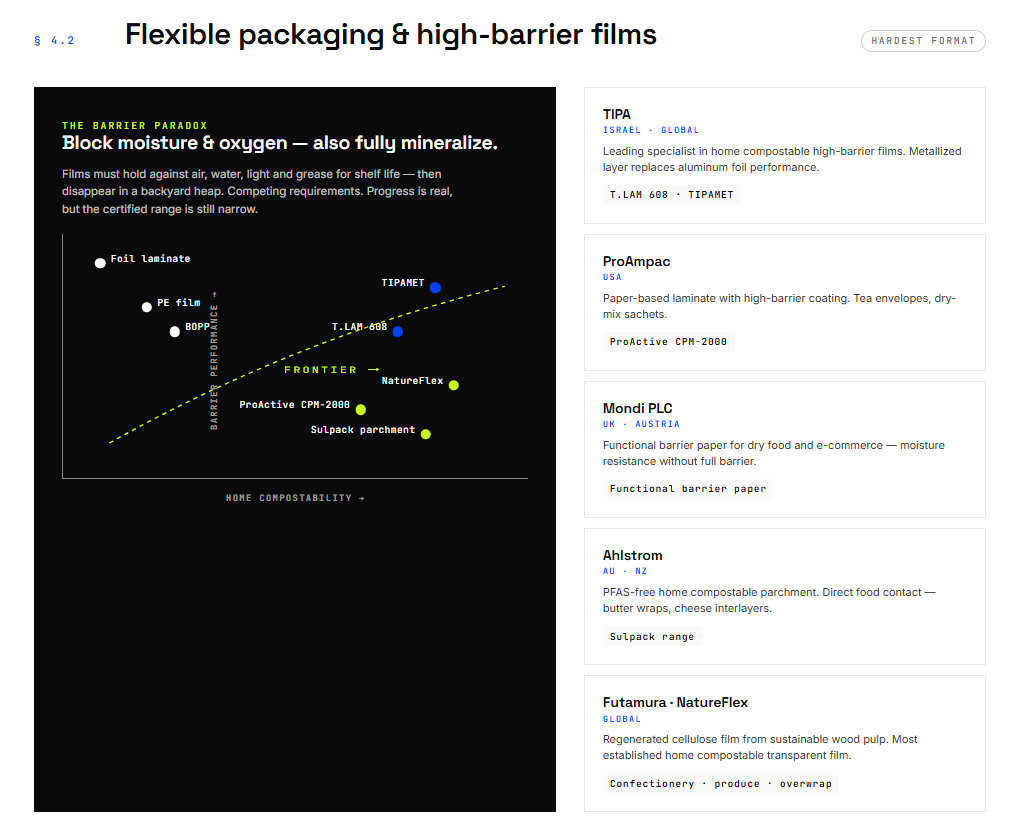

Flexible packaging is the hardest category to convert to home compostability.

Films must simultaneously maintain barrier properties against oxygen, moisture, and light to preserve product shelf life while being engineered to break down completely at ambient temperatures once disposed of.

These are, in many ways, competing requirements.

Progress is being made, but the product range remains narrower than in foodservice, and most formats are still early in commercial scaling.

High-Barrier Bio-Laminates

TIPA Ltd. (Israel, with global distribution) is the leading specialist in home compostable high-barrier films.

Their T.LAM 608 and TIPAMET products are multilayer bio-laminates designed to replace conventional plastic laminate films in snack, confectionery, and coffee packaging.

TIPAMET specifically incorporates a metallized layer that provides barrier performance comparable to aluminum foil while remaining certified for home composting.

These films are technically significant because metallized or foil-layer packaging has historically been one of the most difficult formats to make compostable.

The ability to replace it with a certified home compostable alternative opens up a substantial portion of the flexible packaging market that was previously inaccessible.

Paper-Based High-Barrier Laminates

ProAmpac (USA) offers ProActive CPM-2000, a paper-based laminate with a high-barrier coating suitable for dry food applications including tea envelopes and dry mix sachets.

This format prioritizes the paper substrate for rigidity and printability and relies on the barrier coating to provide functional shelf life protection.

Mondi PLC (UK/Austria) supplies functional barrier paper for dry food and e-commerce applications, covering formats where a degree of moisture resistance is required without the full barrier performance demanded by fats or oxygen-sensitive products.

Specialty Papers and Parchment

Ahlstrom’s Sulpack range is a PFAS-free, home compostable parchment paper used for direct food contact applications including butter wraps and cheese interlayers, primarily in Australian and New Zealand dairy markets.

This is a relevant development given regulatory pressure on PFAS in food contact materials across multiple markets.

Cellulose Films

NatureFlex (Futamura, available globally) is a regenerated cellulose film made from sustainably sourced wood pulp.

It is widely used for confectionery wrapping, fresh produce packaging, and snack overwraps, and is certified for home composting.

It is one of the most commercially established home compostable transparent film options currently available.

Stat: Over 110 million residents in Europe now have access to local or household compost bins, up 34% since 2018.

This expanding infrastructure base is a direct driver of demand for home compostable flexible packaging formats that consumers can actually dispose of correctly.

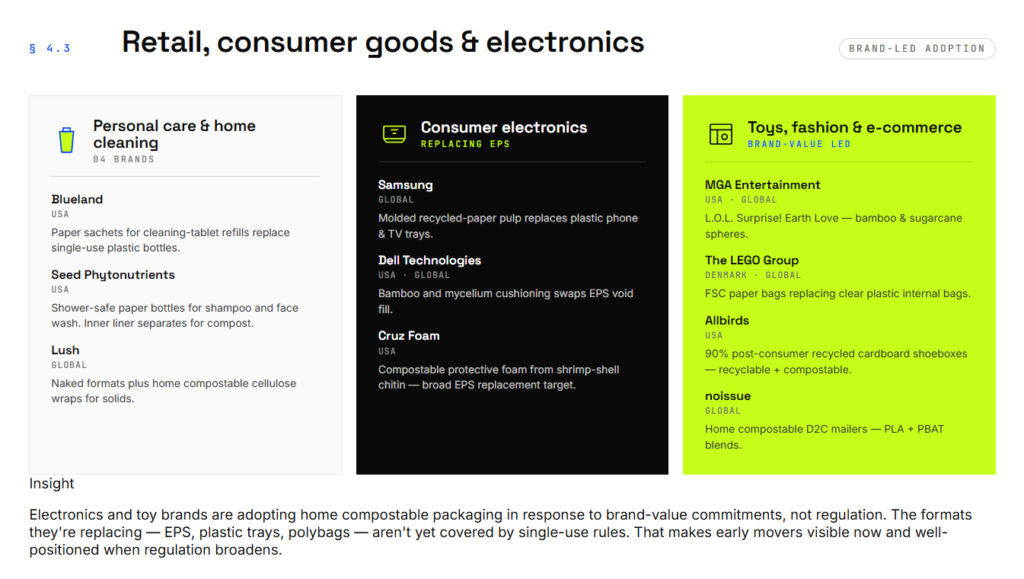

4.3 Home Compostable Retail, Consumer Goods, and Electronics Packaging

Beyond food and beverage, home compostable formats are being adopted across personal care, consumer electronics, toys, and fashion.

The scale and sophistication of these applications vary considerably, but the directional trend is consistent.

Personal Care and Home Cleaning

- Blueland (USA): Home compostable paper-based sachets for cleaning tablet refills, replacing single-use plastic bottles.

- Seed Phytonutrients (USA): A shower-safe paper bottle for liquid shampoo and face wash, with a paper shell that is compostable after the inner liner is separated.

- Lush (Global): Uses naked (unpackaged) formats alongside home compostable cellulose wraps for solid bath and beauty products.

Consumer Electronics

Electronics packaging has historically relied on expanded polystyrene (EPS) for cushioning and plastic trays for component organization.

Both are now being replaced at meaningful commercial scale.

- Samsung (Global): Replaces plastic phone and TV trays with molded pulp made from recycled paper across its mobile and large-format product lines.

- Dell Technologies (USA/Global): Uses bamboo and mycelium-based cushioning for notebook and desktop packaging, replacing EPS void fill.

- Cruz Foam (USA): Produces compostable protective foam from chitin derived from shrimp shells, targeting the broader EPS replacement market.

Toys and Fashion

- MGA Entertainment (USA/Global): Replaced plastic spheres in its L.O.L. Surprise! Earth Love line with packaging made from bamboo and sugarcane, home compostable certified.

- The LEGO Group (Denmark/Global): Transitioning from clear plastic internal bags to FSC-certified paper bags across its product range.

- Allbirds (USA): Uses 90% post-consumer recycled cardboard shoe boxes that are both recyclable and compostable.

- noissue (Global): Supplies home compostable shipping mailers made from PLA and PBAT blends, used primarily by direct-to-consumer and e-commerce brands.

Insight: Electronics and toy brands adopting home compostable packaging are largely responding to brand value commitments rather than regulatory mandates.

The formats they are replacing (EPS, plastic trays, polybags) are not yet subject to the same legislation as single-use foodservice items.

This makes early movers in these categories more visible to sustainability-oriented consumers, and it positions them favorably ahead of packaging regulations that are expected to broaden in scope.

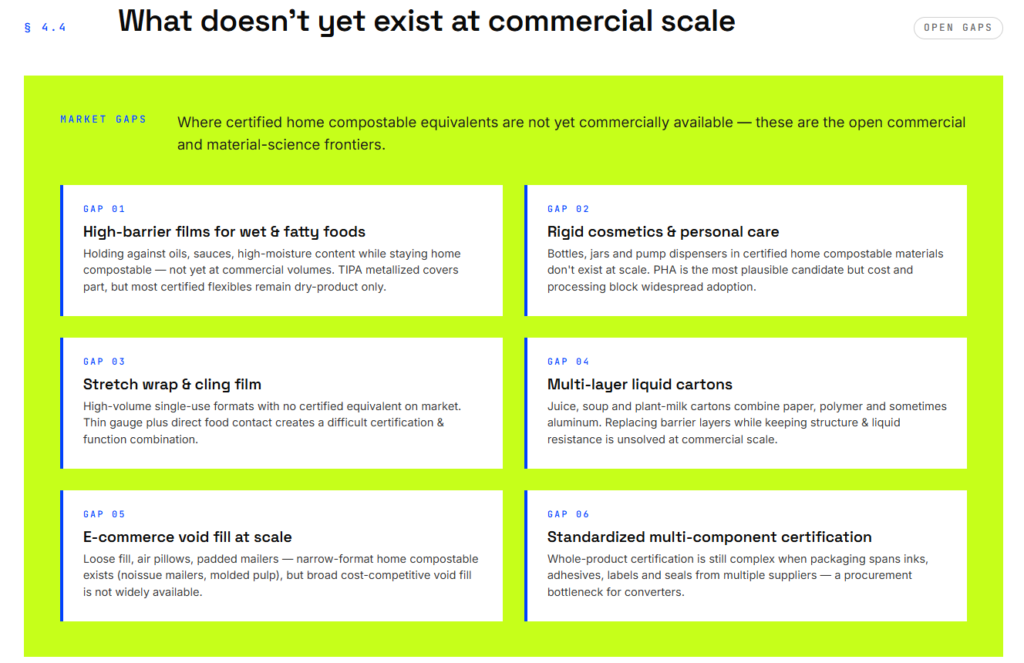

4.4 What Home Compostable Packaging Does Not Yet Exist at Commercial Scale

The current product landscape, while growing, leaves a number of significant format gaps.

These represent both the technical limits of the field and the commercial opportunities that remain open.

High-barrier flexible films for wet and fatty foods at scale. Films that must hold against oils, sauces, or high-moisture content while remaining certified for home composting are not yet available in commercial volumes.

TIPA’s metallized laminates address part of this, but the range of food applications covered remains limited.

Most home compostable flexible formats are currently restricted to dry or low-fat products.

Certified home compostable rigid cosmetics and personal care packaging. Bottles, jars, and pump dispensers made from home compostable materials do not yet exist at commercial scale.

The mechanical and moisture resistance requirements of these formats are not currently met by certified home compostable polymers.

PHA is the most plausible candidate material, but cost and processing constraints prevent widespread adoption.

Home compostable stretch wrap and cling film. These are high-volume, single-use formats with no certified home compostable equivalent currently on the market.

Their thin gauge and direct food contact requirements create a challenging combination of functional and certification demands.

Fully certified home compostable multi-layer structures for liquid packaging.

Carton-style packaging for liquids (juice, soup, plant-based milk) involves bonded layers of paper, polymer, and sometimes aluminum.

Replacing the polymer and barrier layers with home compostable alternatives while maintaining structural integrity and liquid resistance is an unsolved problem at commercial scale.

Standardized home compostable e-commerce void fill.

Loose fill, air pillows, and padded mailers represent a large volume of packaging waste generated by e-commerce.

Home compostable alternatives exist in narrow formats (noissue mailers, molded pulp inserts) but broad-format, cost-competitive void fill certified for home composting is not yet widely available.

These gaps are not permanent, but they are real constraints that affect which brands and categories can credibly commit to fully home compostable packaging today.

Closing them will require continued material science development, investment in manufacturing scale, and certification frameworks that keep pace with new format types.

5. Home Compostable Packaging – The Commercial and Competitive Landscape

Home compostable packaging has crossed a threshold.

What began as a niche category driven by sustainability-focused brands and specialist manufacturers has entered a phase of large-scale consolidation, infrastructure investment, and mainstream adoption.

This chapter maps the value chain, identifies the key players at each level, and examines the investment and M&A activity that is reshaping the sector.

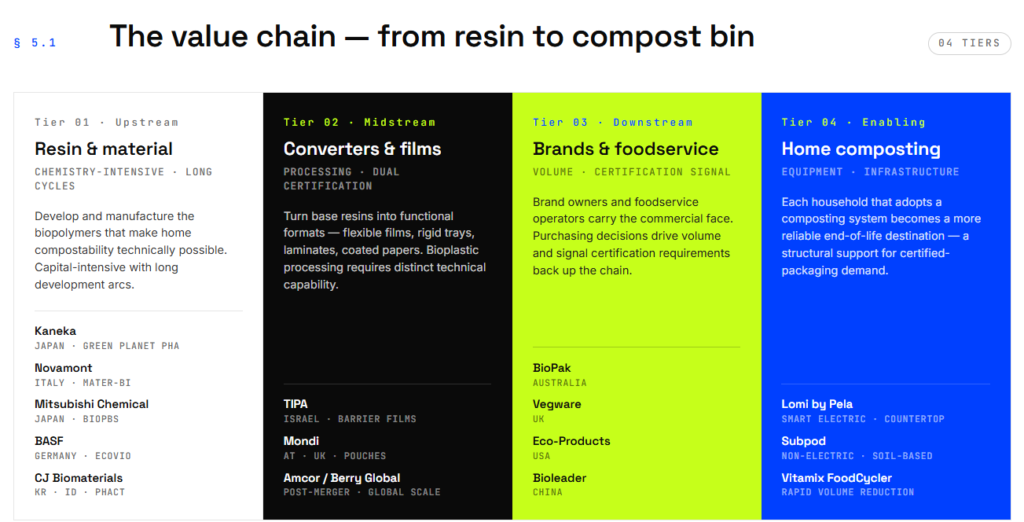

5.1 The Home Compostable Packaging Value Chain

The value chain runs from raw material science through to the consumer’s compost bin, and understanding where value is created and where constraints sit is essential for any brand or investor assessing this market.

Upstream: Resin and Material Producers

At the base of the chain are the companies that develop and manufacture the biopolymers that make home compostability possible.

These are chemistry-intensive businesses with significant capital requirements and long development cycles.

- Kaneka Corporation (Japan): Produces Green Planet PHA, one of the few commercially scaled PHA resins certified for home, soil, and marine biodegradation.

- Novamont (Italy): A founding company of starch-based bioplastics, producing the Mater-Bi family of blends widely used in carrier bags and cutlery.

- Mitsubishi Chemical (Japan): Produces BioPBS, a bio-based polybutylene succinate resin offering high heat resistance while remaining home compostable.

- BASF (Germany): Manufactures the ecovio range, blending its proprietary PBAT with PLA and starch components for film and injection-moulding applications.

- CJ Biomaterials (South Korea/Indonesia): A growing PHA producer supplying PHACT resins as both primary materials and performance modifiers for home compostable formats.

Midstream: Converters and Film Specialists

Converters take base resins and transform them into functional packaging formats, including flexible films, rigid trays, laminates, and coated papers.

This layer requires technical capability in processing biopolymers, which behave differently from conventional resins, and increasingly requires dual certification (home and industrial) as a baseline B2B requirement.

Key midstream players include TIPA (Israel, high-barrier films), Mondi (Austria/UK, barrier papers and pouches), and Amcor/Berry Global (post-merger, sustainable rigid and flexible formats at global scale).

Downstream: Brand Owners, Foodservice Specialists, and Retailers

Brand owners and foodservice operators are the commercial face of home compostable packaging.

Their purchasing decisions drive volume and signal certification requirements back up the chain.

BioPak (Australia), Vegware (UK), Eco-Products (USA), and Bioleader (China) are the dominant specialists in the foodservice and tableware segment, collectively supplying certified bagasse and PLA-lined products to operators across multiple geographies.

Enabling Infrastructure: Home Composting Equipment

A distinct but commercially relevant segment of the value chain is the equipment that supports home composting itself.

- Lomi (by Pela): Leads the smart electric countertop composter market.

- Subpod: Occupies the non-electric, soil-based niche.

- Vitamix FoodCycler: Offers rapid volume reduction for urban households.

As home composting adoption grows, this enabling layer becomes a structural support for demand in certified packaging materials.

Insight: The growth of the home composting equipment market is not incidental to the packaging market.

Each household that adopts a composting system becomes a more reliable end-of-life destination for home compostable packaging.

5.2 Home Compostable Packaging – Investment and M&A Activity

The investment picture from 2023 to 2025 reflects a market in structural transition: large established players are consolidating to secure sustainable material platforms, venture capital continues to fund material science innovation, and significant infrastructure capital is being deployed to scale primary resin production.

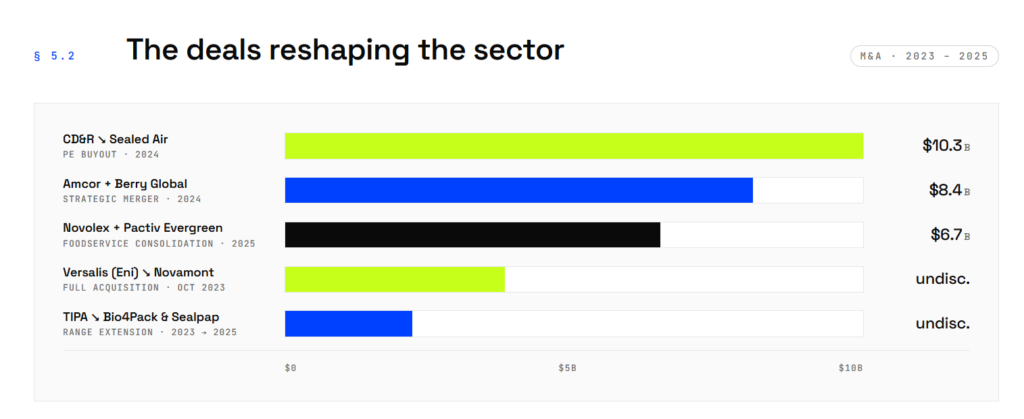

Major M&A Deals

- Amcor and Berry Global (USD 8.4 billion): The largest deal in sustainable packaging consolidation, tilting Amcor’s portfolio decisively toward fiber-based and certified sustainable flexible and rigid formats.

- CD&R and Sealed Air (USD 10.3 billion): Positions Sealed Air as a material-agnostic platform for sustainable packaging at industrial scale.

- Versalis (Eni) and Novamont: The full acquisition of Novamont by Eni’s chemicals subsidiary in October 2023 brought one of the foundational starch bioplastics businesses into the orbit of a major energy company.

- Novolex and Pactiv Evergreen (USD 6.7 billion): Consolidating North American foodservice packaging at a moment when home compostable demand in that market is accelerating following the launch of the BPI Home Compostability Standard.

- TIPA acquisitions: TIPA acquired Bio4Pack (May 2023) and Sealpap (November 2025), extending its range from flexible films into compostable closures and rigid formats.

The Cryovac brand has since entered bio-based compostable protein tray development in collaboration with Eastman.

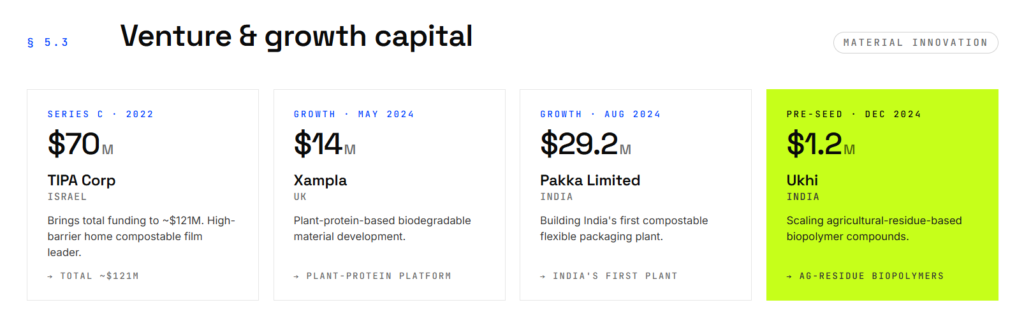

Venture and Growth Capital

- TIPA Corp: USD 70 million Series C in 2022, bringing total funding to approximately USD 121 million.

- Xampla (UK): USD 14 million secured in May 2024 for plant-protein-based biodegradable material development.

- Pakka Limited (India): USD 29.2 million in August 2024 to build India’s first compostable flexible packaging plant.

- Ukhi (India): USD 1.2 million pre-seed in December 2024 to scale agricultural residue-based biopolymer compounds.

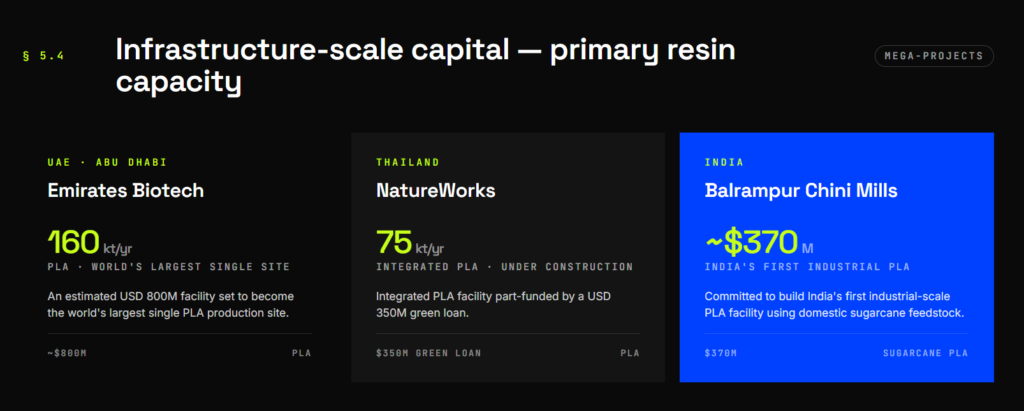

Infrastructure-Scale Investment

Three projects illustrate the scale of capital now targeting primary resin production:

- Emirates Biotech (UAE): An estimated USD 800 million investment for a 160,000 tonne per year PLA facility in Abu Dhabi, which would become the world’s largest single PLA site.

- NatureWorks (Thailand): A 75,000 tonne per year integrated PLA facility under construction, partly funded by a USD 350 million green loan.

- Balrampur Chini Mills (India): Approximately USD 370 million committed to build India’s first industrial-scale PLA facility using domestic sugarcane feedstock.

Distressed M&A: A Cautionary Signal

Not all capital deployments have succeeded.

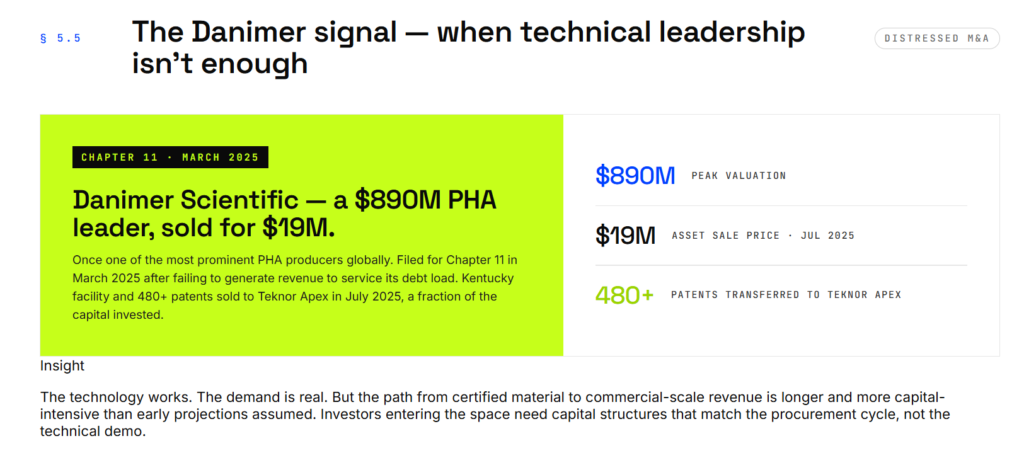

Danimer Scientific, once valued at USD 890 million as one of the most prominent PHA producers globally, filed for Chapter 11 bankruptcy in March 2025 after failing to generate sufficient revenue to service its debt load.

Its Kentucky production facility and over 480 patents were sold to Teknor Apex for USD 19 million in July 2025, a fraction of the capital invested.

Insight: The Danimer case illustrates the central tension in this market: the technology works, and the demand is real, but the path from certified material to commercial-scale revenue is longer and more capital-intensive than early projections assumed.

Investors entering the space need to account for the gap between technical validation and the pace of commercial adoption, particularly in markets where procurement cycles are long and certification requirements create additional lead time before products reach shelves.

Looking ahead, analysts project USD 8 to 12 billion in global investment in sustainable coating capacity by 2030, with M&A activity expected to concentrate on securing marine-safe IP, particularly PHA, ahead of the EU’s 2028 regulatory enforcement cycle.

6. Home Compostable Packaging – Outlook

6.1 The State of Home Compostable Packaging

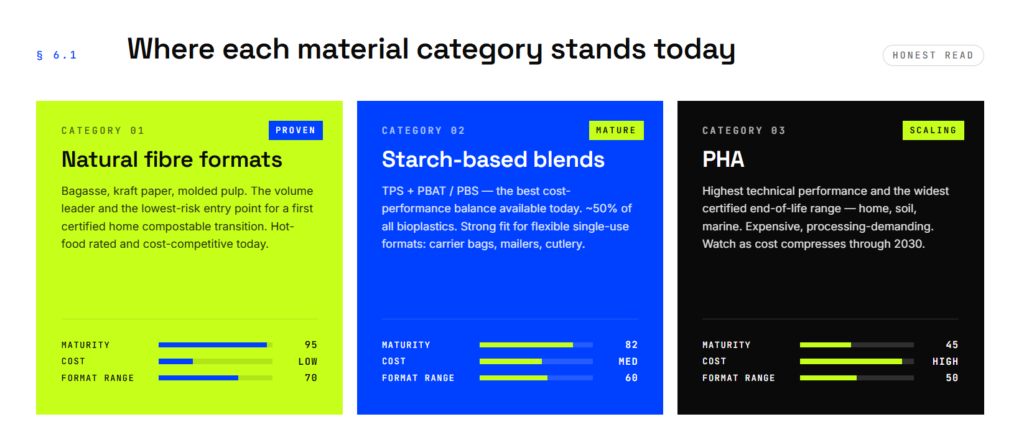

Home compostable packaging is commercially real, technically constrained, and growing faster than most adjacent sustainability categories.

Natural fiber formats (bagasse, kraft paper, molded pulp) and starch-based blends are proven at scale.

PHA is scaling, expensive, and technically superior.

High-barrier home compostable flexible films are early in commercial availability but exist.

However, a significant portion of what is sold as compostable today is neither home compostable nor reaching a composting facility of any kind.

The honest picture is a market that has cleared the proof-of-concept stage and is now navigating the harder problems: cost, consumer behavior, certification integrity, and the gap between what certified products can do in a laboratory and what actually happens in a backyard bin.

These are solvable problems, but they require specificity, not optimism.

6.2 Home Compostable Packaging – Market Drivers

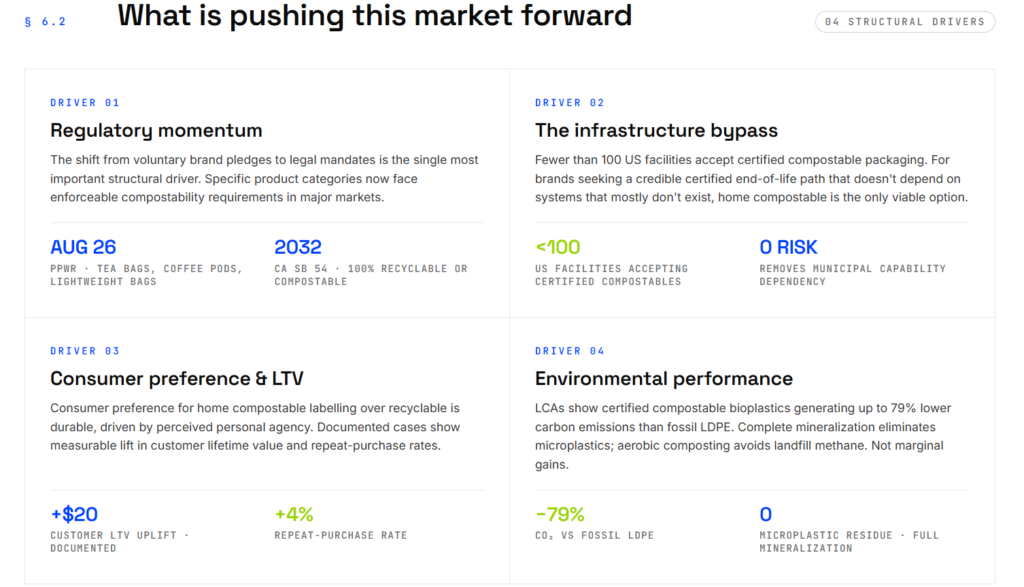

Regulatory Momentum

The shift from voluntary brand pledges to legal mandates is the single most important structural driver.

This is not a soft trend.

Specific product categories now face enforceable compostability requirements in major markets:

- The EU PPWR mandates compostability for tea bags, coffee pods, and lightweight plastic carrier bags from August 2026.

- France’s AGEC law targets retail and takeaway packaging conversion to home compostable formats.

- California SB 54 requires all packaging sold in California to be recyclable or compostable by 2032.

- India’s 2022 ban on low-utility single-use plastics has driven large-scale adoption of certified compostable resins across South and Southeast Asian supply chains.

The Infrastructure Bypass Effect

In the United States, fewer than 100 facilities currently accept certified compostable packaging.

For brands seeking a credible certified end-of-life path that does not depend on infrastructure that does not exist for most consumers, home compostable formats are the only viable option.

This is a practical supply chain decision.

Brands that choose home compostable formats remove their dependency on municipal composting capability, which reduces long-term regulatory and reputational risk.

Consumer Preference and Commercial Return

Consumer preference data consistently favors home compostable labeling over recyclable labeling, with the gap driven by the perceived personal agency of composting at home.

Beyond preference, commercial outcomes are measurable: home compostable e-commerce packaging has been associated with a USD 20 increase in customer lifetime value and a 4% increase in repeat purchase rates in documented cases.

Environmental Performance

Life cycle assessments show that certified compostable bioplastics can generate up to 79% lower carbon emissions than fossil-based LDPE.

Complete mineralization eliminates microplastic generation, and aerobic composting avoids the methane emissions produced by landfill decomposition.

These are not marginal gains.

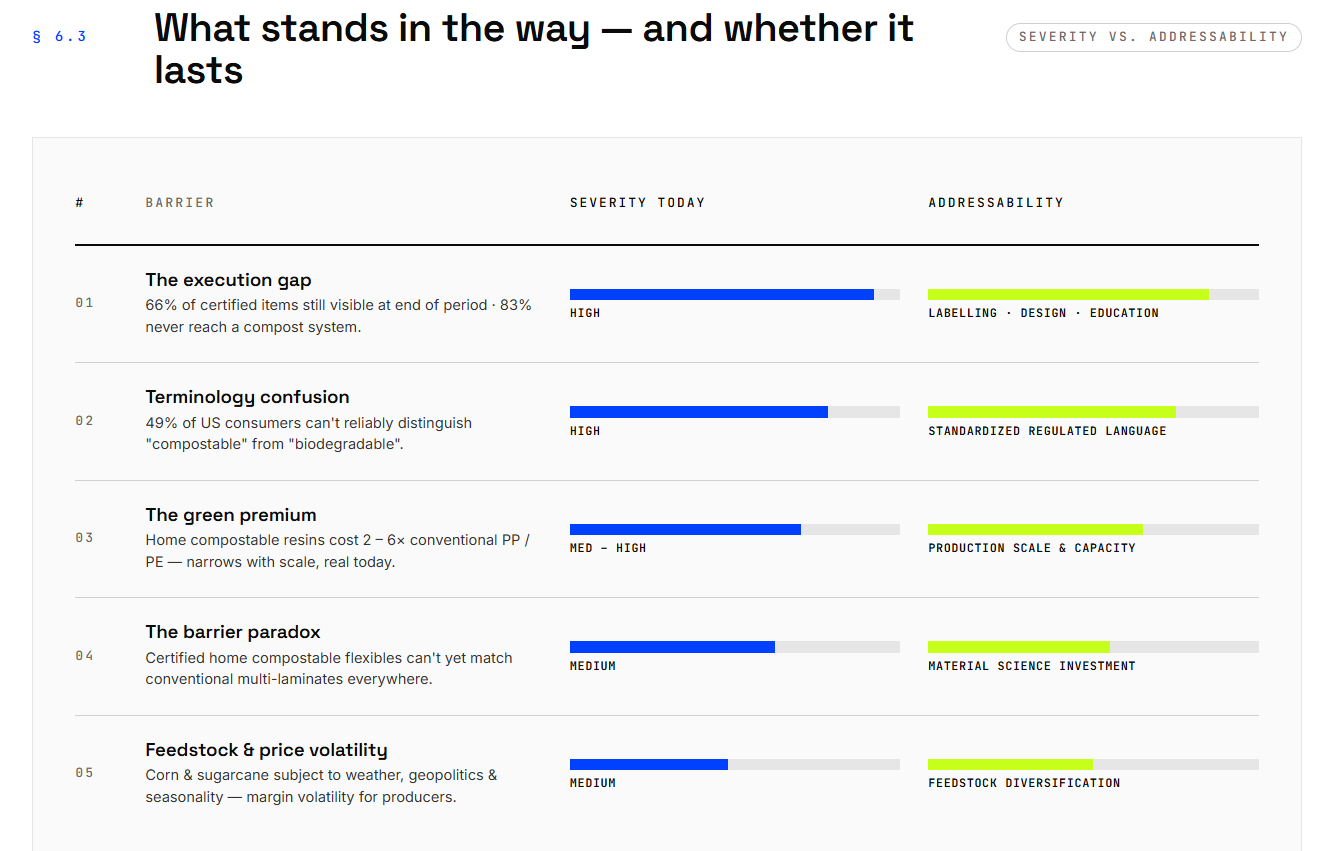

6.3 Home Compostable Packaging – Market Barriers

The Execution Gap

The most stubborn barrier is not technical.

It is behavioral.

Certification standards are built around controlled laboratory conditions.

However, real home compost heaps are variable in temperature, moisture, and aeration.

One major study found that 66% of certified home compostable items still had visible remains at the end of a typical composting period.

A separately documented figure shows that 83% of home compostable packaging does not reach a home compost system at all, ending up in general waste or, more problematically, in conventional plastic recycling where it acts as a contaminant.

Closing this gap requires clearer on-pack disposal instructions, better consumer education, and product design that makes correct disposal intuitive rather than effortful.

Consumer Confusion About Terminology

49% of US consumers cannot reliably distinguish between “compostable” and “biodegradable.”

Many expect certified products to break down within weeks, when certification timelines allow up to 12 months.

This confusion reflects years of inconsistent and often misleading labeling across the industry.

Fixing it requires precise, standardized, regulation-backed language, which the EU Green Claims Directive is beginning to enforce.

The Green Premium

Home compostable resins currently cost 2 to 6 times more than the conventional polypropylene or PE they replace.

This premium narrows as production volumes increase, but it remains a real barrier in price-sensitive categories and markets.

For most brands, the business case depends on either regulatory obligation, a customer base that actively values sustainability and pays a corresponding premium, or a sufficiently high customer lifetime value to absorb the packaging cost difference.

The Barrier Paradox in Flexible Packaging

For products that require moisture and oxygen protection, certified home compostable flexible films cannot yet match the barrier performance of conventional multi-laminates across all applications.

Progress is being made, as TIPA’s metallized films demonstrate, but the available range of barrier-certified home compostable flexible formats remains narrower than what the overall packaging market requires.

This limits which product categories can fully transition today.

Feedstock and Price Volatility

Agricultural commodity prices for corn and sugarcane, the primary feedstocks for starch-based bioplastics and PLA, are subject to weather shocks, geopolitical disruption, and seasonal variability.

This introduces margin volatility for resin producers and cost unpredictability for brands, particularly those operating at high volume.

Insight: The barriers listed above are not equally weighted.

The execution gap and consumer confusion are addressable through labeling, design, and education.

The green premium is addressable through scale.

The barrier paradox is addressable through material science investment.

None of them represent a structural ceiling on the market.

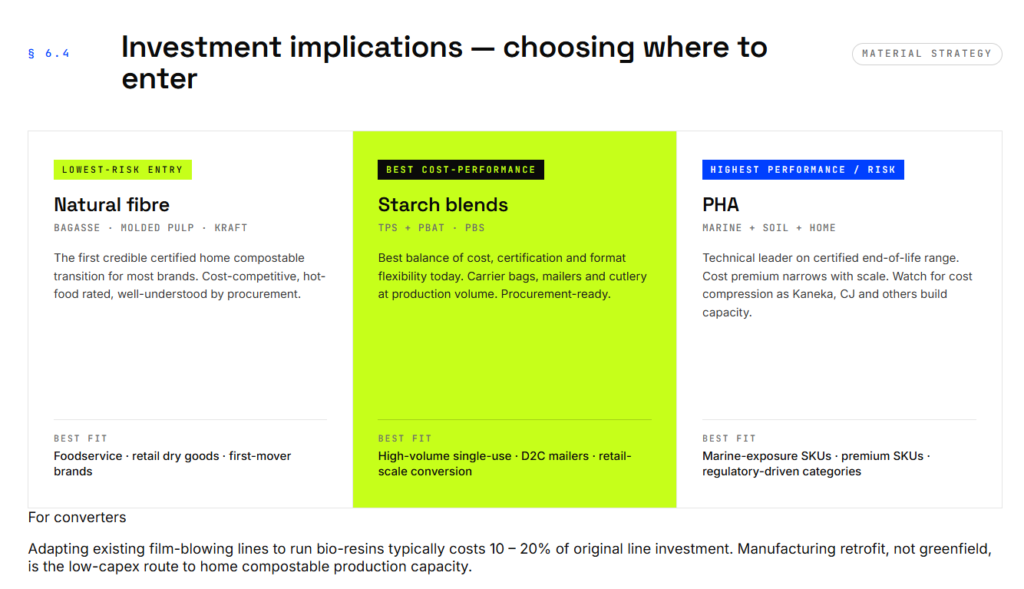

6.4 Home Compostable Packaging – Investment Outlook

The clearest investment signal in this market is the divergence between material categories.

PHA offers the highest technical performance and the widest certified end-of-life range (home, soil, marine), but carries significant cost and processing risk.

Starch-based blends offer the best cost-performance balance today.

Natural fiber formats are the lowest-risk entry point for brands making their first certified home compostable transition.

For converters, manufacturing retrofits represent a low-capex opportunity.

Adapting existing film-blowing lines to run bio-resins typically costs 10 to 20% of the original line investment, which allows for material grade transitions without greenfield capital expenditure.

For investors, the Danimer Scientific bankruptcy (filed March 2025, assets sold for USD 19 million against significantly higher funded debt) is a direct reminder that technical leadership does not guarantee commercial viability.

The path from certified material to commercial-scale revenue is longer than early projections in this sector have typically assumed, and capital structures need to reflect that.

Industry analysts project USD 8 to 12 billion in global investment in sustainable coating capacity by 2030.

M&A activity is expected to concentrate on securing marine-safe intellectual property, particularly PHA assets, ahead of the EU’s 2028 regulatory enforcement cycle.

Conclusion

Home compostable packaging is not a speculative category.

The materials exist, the certifications are rigorous, the regulations are tightening, and consumer preference is measurable and durable.

What the market has not yet fully resolved is the distance between a certified product and a reliable real-world outcome, the cost of home compostable materials relative to conventional alternatives, and the availability of certified formats across all packaging types that brands need.

The next five years will be defined by whether the market closes those gaps or whether it allows them to persist, creating continued space for greenwashing, consumer confusion, and certified products that never reach a compost heap.

The technical and commercial foundations are in place.

What remains is execution, at every level of the value chain.

© 2026 Ukhi Bioplastics Private Limited. All rights reserved.

References

1. Atlantic Packaging. (2026, January). Compostability certifications reference guide.

2. Australasian Bioplastics Association. (2025). ABA home compost certification. Bags and Pouches Singapore.

3. BASF. (2025, May 6). Metpack and BASF cooperate to demonstrate certified home-compostable, coated paper for food packaging.

4. Biodegradable Products Institute. (2025, November 4). BPI’s new home compostability certification. BioCycle.

5. Biodegradable Products Institute. (2025). Home compostable certification.

6. CalRecycle. (2026). Truth-in-labeling laws: Protecting California consumers from false marketing claims. State of California.

7. EcoClaim. (2026). Greenwashing in food & beverage: What’s banned under EU law (2026).

8. GOV.UK. (2026, January 22). Making green claims: Getting it right, across the supply chain.

9. Good Start Packaging. (2026). Home compostable vs industrial composting: what’s the difference?.

10. Latham & Watkins. (2025). European packaging and packaging waste regulation summary of provisions and new guidance.

11. Mordor Intelligence. (2026). Biodegradable plastic packaging market size & growth 2031.

12. Murray, W. (2025, August). Navigating the compostable landscape: Regulation, innovation, and responsibility. Sinclair Intl.

13. Notpla. (2025). Home compostable vs industrial compostable packaging: what’s the difference?.

14. Packaging Europe. (2025, April 18). ‘Misleading’ compostability claims lead to ban of coffee product search ads.

15. Solinatra. (2025). Global plastic regulations 2025: Updated bans & worldwide policy overview.

16. Standards Australia. (2010). Biodegradable plastics—Biodegradable plastics suitable for home composting (AS 5810-2010).

17. The global state of home compostability in packaging: A decadal strategic analysis (2025–2035). (2025).

18. Torise Biomaterials. (2025). 2025 compostable packaging trends: How top companies are embracing biodegradable solutions.

19. TÜV AUSTRIA Belgium. (2012, March 1). Program OK 2: Home compostability of products (Edition D).

20. Weston, P. (2022, November 3). ‘It’s greenwash’: most home compostable plastics don’t work, says study. The Guardian.

21. Sander, M., Weber, M., Lott, C., Zumstein, M., Künkel, A., & Battagliarin, G. (2024). Polymer Biodegradability 2.0: A Holistic View on Polymer Biodegradation in Natural and Engineered Environments. Advances in Polymer Science, 293, 65–110. https://doi.org/10.1007/12_2023_163,.

22. Fogašová, M., Figalla, S., Danišová, L., Medlenová, E., Hlaváčiková, S., Vanovčanová, Z., Omaníková, L., Baco, A., Horváth, V., Mikolajová, M., Feranc, J., Bočkaj, J., Plavec, R., Alexy, P., Repiská, M., Přikryl, R., Kontárová, S., Báreková, A., Sláviková, S., Koutný, M., Fayyazbakhsh, A., & Kadlečková, M. (2022). PLA/PHB-Based Materials Fully Biodegradable under Both Industrial and Home-Composting Conditions. Polymers, 14(19), 4113. https://doi.org/10.3390/polym14194113.

23. Hubbe, M. A., Lavoine, N., Lucia, L. A., & Dou, C. (2021). Formulating Bioplastic Composites for Biodegradability, Recycling, and Performance: A Review. BioResources, 16(1), 2022-2083,.

24. Debnath, M., Sarder, R., Pal, L., & Hubbe, M. A. (2022). Molded pulp products for sustainable packaging: Production rate challenges and product opportunities. BioResources, 17(2), 3810-3870. https://doi.org/10.15376/biores.17.2.Debnath,.

25. Baxter, D. (2026, March 17). What Is PHA? The Complete Guide to Polyhydroxyalkanoate Bioplastics. PlantSwitch. https://www.plantswitch.com/blog/what-is-pha-polyhydroxyalkanoate-bioplastics-guide,.

26. Baxter, D. (2026, March 2). Why PLA Isn’t Actually Compostable (And What Is). PlantSwitch. https://www.plantswitch.com/blog/why-pla-isnt-actually-compostable,.