Europe’s plastic waste problem can no longer be pushed aside.

If things don’t change, plastic packaging waste in the EU could grow by almost 46% by 2030. Much of that comes from heavy reliance on single-use plastics. Uneven recycling practices across member states are also to blame.

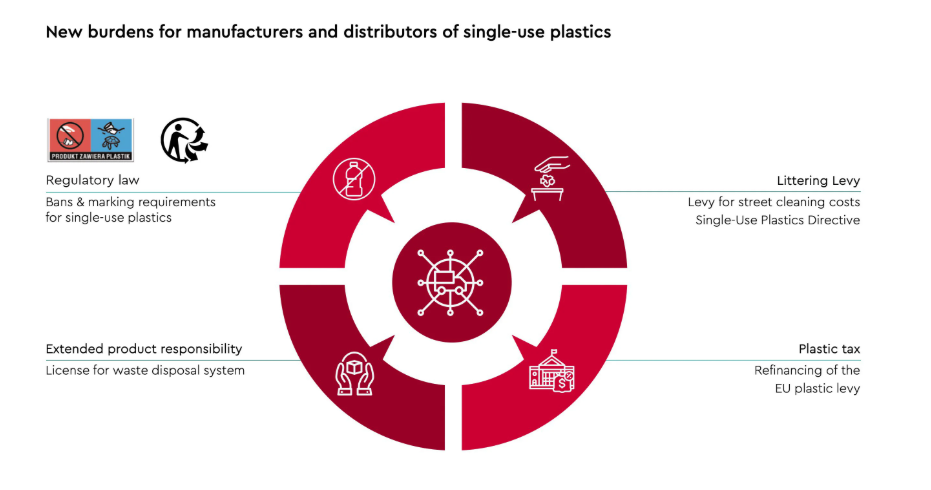

To combat this, the EU introduced a price on waste itself. The EU plastic tax, officially known as the EU plastics levy, puts a direct cost on every kilogram of plastic packaging that is produced but not recycled.

Since 2021, this cost has been flowing quietly through national budgets, supply chains, and packaging decisions across Europe.

In this article, I’ll break down what the EU plastic tax regulation really does and how it works in practice.

I’ll also discuss how this regulatory change is creating a very real, multi‑billion‑dollar opportunity for bio‑based plastics and next‑generation packaging materials.

A complete overview of the EU plastic tax

The EU plastic tax targets the point where plastic packaging waste is generated but not recycled. The amount each country pays is linked directly to its performance on recycling.

This measure stands out because it directly connects environmental outcomes with financial responsibility.

By putting a tangible cost on waste, the EU plastics levy aims to make every kilo of non-recycled plastic packaging a real business consideration and not merely a regulatory statistic.

Why Did the EU Introduce a Plastic Tax?

The EU wasn’t just looking to reduce plastic waste; it also needed a reliable way to support its post-COVID recovery.

In 2020, EU leaders agreed to create a new revenue stream for the EU budget: a plastics levy on non-recycled packaging waste.

This helped fill the funding gap left by Brexit and enabled the launch of the €750 billion NextGenerationEU recovery plan.

At the same time, this new regulation fits seamlessly into Europe’s bigger sustainability roadmap.

For instance, it reinforces the EU Green Deal vision for a climate‑neutral, circular economy. It supports tighter packaging and waste rules to reduce pollution and conserve resources.

It also gives national governments a clear financial incentive to invest in recycling and reduce dependence on virgin plastics.

How Does the EU Plastic Tax Work?

The logic is straightforward. Each year, countries pay €0.80 for every kilogram of plastic packaging waste that goes unrecycled. To push change further, the EU has proposed to increase this to €1.00 per kilogram.

Each member state is responsible for paying the levy, but they can independently decide how to recover this cost.

Spain and Italy, for example, have introduced national plastic taxes, surcharges, or higher Extended Producer Responsibility (EPR) fees. Others simply fund it through general taxation.

This financial pressure doesn’t stop at the national level. Producers, packaging suppliers, brands, and eventually, even consumers may all feel the effects. That’s because these new costs will ripple through the supply chain.

By tying payments directly to recycling rates, the EU plastic tax makes a country’s performance on waste management a matter of fiscal responsibility.

What Counts as “Non-Recycled Plastic Packaging Waste?”

Each country will have to look at how much plastic packaging is placed on the market in a year and then subtract what is actually recycled.

What remains is classified as non‑recycled plastic packaging waste, and that is what the EU packaging levy is calculated on.

To make this work across 27 member states, the EU relies on a shared reporting framework. Countries collect data from manufacturers, waste operators, and recycling systems, and submit their final figures to Eurostat.

The idea behind this system is that everyone measures plastic waste the same way, using the same rules. This way, no country gains an advantage by reporting loosely.

In practice, though, this has proven harder than it sounds. The European Court of Auditors has pointed out several early challenges.

Differences in how countries interpret what qualifies as “plastic packaging,” variations in how recycling is measured, and delays in reporting complete data are just some of them.

These gaps don’t invalidate the system. But they do show why accurate waste tracking has suddenly become a high‑stakes issue for governments.

What Has the EU Plastic Tax Achieved So Far?

Despite a rocky start, the EU plastics levy is already reshaping the conversation around waste.

In 2021, it generated about €5.9 billion for the EU budget. In 2023, this figure climbed to around €7.2 billion, which is roughly 4% of the EU’s total revenue that year.

Early evidence suggests that, for the first time in years, plastic packaging waste in the EU dropped slightly in 2023, to 79.7 million tonnes.

More companies and governments are searching for ways to minimize the amount of non-recycled plastic packaging. They obviously want to lower their future liabilities and signal progress to stakeholders.

How is the EU Plastic Tax Creating a $10B Opportunity for Bio-Based Alternatives?

For years, bioplastic packaging was seen as a “nice-to-have” option. That’s especially true for businesses that want to appear eco-friendly. But it wasn’t treated as a core business decision.

Now that the EU plastic tax is raising the cost of non-recycled and fossil-based packaging, businesses have started to seriously consider the potential of bio-based alternatives.

Why Are Bio-Based Alternatives Becoming More Attractive?

With every kilogram of non-recycled fossil plastic now facing a hefty penalty, traditional materials are simply getting more expensive to use and justify.

Pressure is growing on brands and manufacturers to show real progress on sustainability. Investors are asking for Environmental, Social, and Governance (ESG) proof, not just promises.

Furthermore, Europe’s new Bioeconomy Strategy even includes €10 billion in corporate commitments to buy bio-based materials by 2030. It shows just how serious the demand has become.

In this environment, bio-based plastic alternatives are becoming essential tools for risk management and growth.

If you can cut your exposure to future plastic taxes, meet customer expectations, and future-proof your business, why wouldn’t you move quickly?

How Big Is the European Bio-Based Plastics Market?

The numbers now tell a very different story than they did just a few years ago.

In 2023, the European bioplastics market was valued at roughly $5.8 billion. Analysts predicted that it will surpass $29 billion by 2033 as new policies are introduced and consumer demand increases.

Packaging dominates bioplastic demand in the EU, with more than half of all bioplastic demand coming from this segment. Food wrappers, trays, shopping bags, and e-commerce packs are seeing the fastest growth.

The $10 billion figure that’s often quoted for bio-based plastics isn’t just marketing talk. The number comes from modest shifts toward alternative packaging, alongside price premiums and fresh demand triggered by the EU plastics levy.

What’s Driving Investment and Innovation?

Major chemical companies like BASF and Corbion are investing in new facilities for next-generation bioplastic materials.

Startups across Europe are securing millions in funding to develop everything from medical-grade biopolymers to plant-based film coatings.

EU grants, national incentives, and big private investments are all supporting new ideas.

For example, the EU’s updated Bioeconomy Strategy is building a clear pipeline for “bankable” projects and encouraging public-private partnerships.

One of the most exciting trends is the move toward using agricultural waste as a feedstock for high-performance biopolymers.

Here at UKHI, we develop compostable polymers like our EcoGran™ range. It’s made from crop residues such as hemp, nettle, and flax.

Our materials are designed to run on existing manufacturing lines. They also meet food-grade standards and help brands lower their carbon footprint without sacrificing performance or cost-efficiency.

What Are the Real-World Challenges?

None of this growth comes without challenges. First, cost remains a real hurdle. Many bioplastic options are still three to four times more expensive than conventional plastics.

Until technology advances or production scales up further, this price gap will limit how quickly businesses can make the switch.

Then there’s the question of infrastructure. Industrial composting facilities, for example, aren’t available everywhere in Europe. That means a compostable coffee cup in Berlin might just end up as landfill in Madrid or Paris.

Sorting, collection, and recycling systems are all in a period of catch-up as these new materials come to market.

Greenwashing is also a real risk. Products labeled “bio-based” aren’t always as sustainable as they sound. And clear standards are still taking shape.

So, businesses need to keep an eye on both regulatory changes and changing consumer expectations.

Final Words

For bio-based plastic alternatives to go mainstream, a few things need to fall into place. Europe needs clearer, harmonised policies and incentives. Investment in recycling and composting infrastructure also needs to pick up speed.

Finally, collaboration is key. Companies, governments, and research groups need to work together. As these pieces fall into place, the move away from fossil plastics becomes both practical and profitable.