As researchers working on industrial compostable packaging in India, we hear a version of this question regularly: if there are no industrial composting facilities to process these products, what exactly is the environmental benefit?

Firstly, I have to acknowledge that this is a fair question. So let’s understand how robust the objection is:

- Industrial composting infrastructure requires specific controlled conditions which do not exist at a meaningful scale in India.

- As of June 2025, India has only 3 registered industrial composting units, with 9 more in process. For a country of 1.4 billion people, that is a near-total absence of end-of-life infrastructure.

- So what is the point of investing in, innovating in, and being excited about industrially compostable packaging?

Nobody can attempt to analyze the need or potential of industrially compostable packaging without acknowledging this gap.

I also want to ask and attempt to answer a harder question: does the absence of infrastructure today tell us anything meaningful about tomorrow?

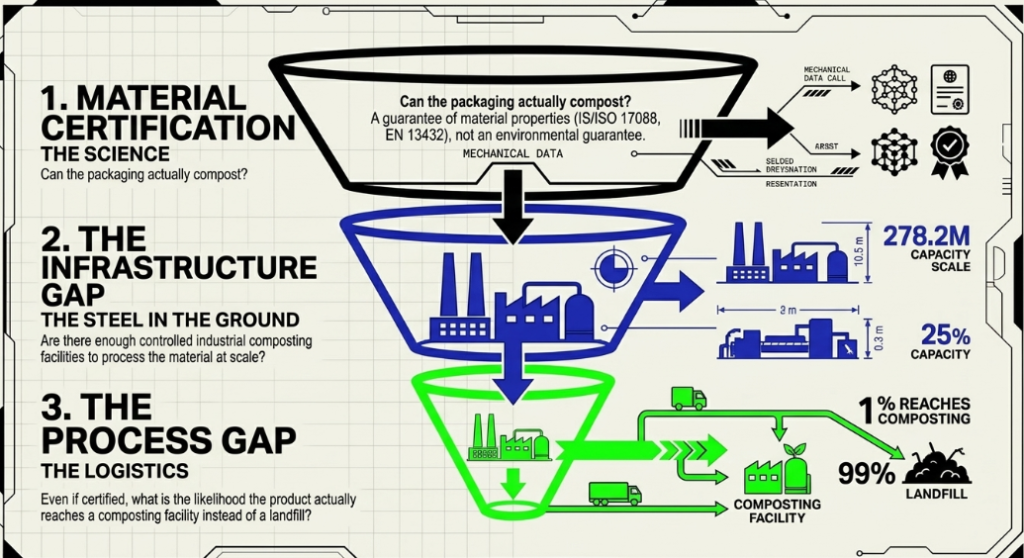

To answer it properly, we need to separate three distinct problems:

- Material certification — can the packaging actually compost? This is about material properties

- The infrastructure gap — are there enough industrial composting facilities to process it at scale?

- The process gap — even when a product is certified compostable, what is the likelihood it actually reaches a composting facility?

Definition: A product certified as industrially compostable must degrade into carbon dioxide, water, and biomass within 12 weeks under controlled facility conditions. In India, the governing standard is IS/ISO 17088. Internationally: EN 13432 (EU) and ASTM D6400 (US). The certification describes performance under specific facility conditions — it is not a general environmental guarantee.

The ‘Industrial Composting’ Infrastructure Gap — A Global Problem, Not India’s Alone

Before drawing conclusions about India’s position, it is worth looking at the global picture of industrial composting infrastructure.

Certified Compostable Packaging Processing Capacity by Region

| Region | Facilities Accepting Certified Compostable Packaging | Key Gap |

| United States | Fewer than 100 facilities out of ~5,000 composting sites | Only 11% of the US population has access to any composting program |

| United Kingdom | Infrastructure for certified packaging is not at scale, despite investment in anaerobic digestion for food waste | Only 1 in 400 compostable takeaway cups reaches an appropriate facility |

| European Union | ~5,800 biowaste treatment facilities, but coverage of certified compostable packaging is uneven | Germany, Netherlands, and Belgium — despite mandatory separate food waste collection — achieve only 15–25% food waste collection rates |

| Italy | 300+ composting facilities; 85% of population covered under Biorepack scheme | Closest to a functioning national system; detail below |

| India | 3 registered industrial composting units | 1.4 billion people; virtually no accessible end-of-life pathway for certified compostable products |

The conclusion is straightforward: industrial composting infrastructure for certified compostable packaging is underdeveloped everywhere. This is a global gap at different stages of development, not an Indian failure.

This is also where we must tip our hats to the Italians.

Italy’s National Biorepack Scheme: How Industrial Composting Infrastructure Gets Built

Italy is the most instructive case study in building nationwide industrial composting infrastructure for bioplastics.

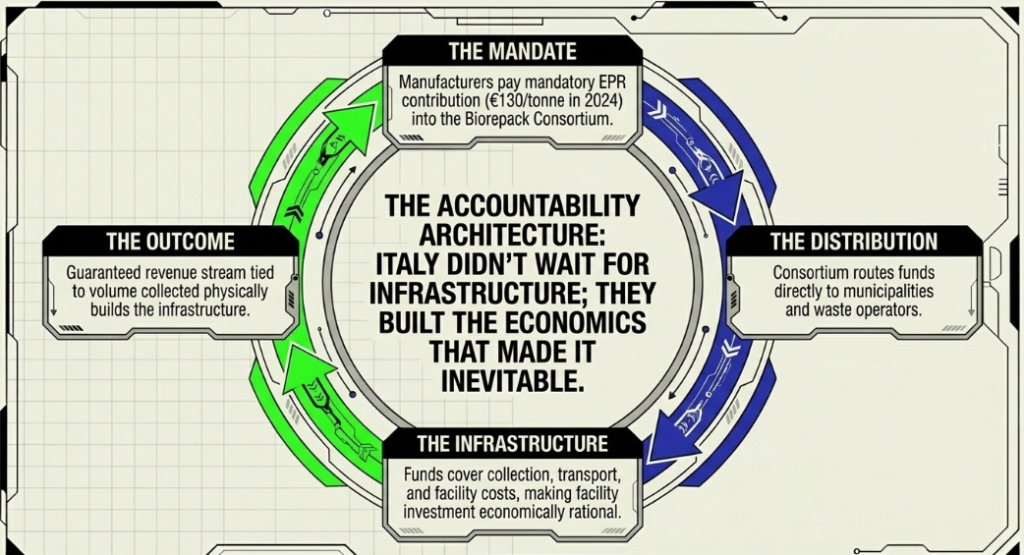

In 2020, it launched Biorepack — the world’s first EPR scheme dedicated exclusively to compostable bioplastics.

The mechanism works as follows:

- Manufacturers pay a mandatory EPR contribution (€130 per tonne in 2024) into the Biorepack consortium

- The consortium distributes funds to municipalities and waste operators to cover collection, transport, and composting facility costs

- This makes facility investment economically rational by guaranteeing a revenue stream tied to volume collected

The results within four years:

- 57.8% recycling rate for compostable packaging placed on the Italian market, surpassing the EU’s 2025 target (50%) and 2030 target (55%) ahead of schedule

- 85% of the Italian population now covered by compostable bioplastics collection and treatment systems, up 11 percentage points in a single year

- €12.7 million paid out to municipalities in 2024 to cover collection and composting costs

- 5.6 million tonnes of CO₂ equivalent avoided annually compared to landfill disposal; 1.9 million tonnes of compost produced per year

Italy did not wait for infrastructure before building the market.

It built the accountability architecture that made infrastructure investment economically rational. The infrastructure followed the policy design

How Infrastructure Has Always Followed the Product: Three Precedents

Italy’s pattern is not unusual. It is consistent with how every major infrastructure-dependent technology transition has unfolded.

Electric Vehicles and Charging The first mass-market EVs launched with almost no public charging network. The EV charging rollout was described at the time as an unsolvable chicken-and-egg problem: no infrastructure meant no buyers; no buyers meant no economic case for infrastructure. By 2024, the US had surpassed 180,000 public charging ports and the global figure exceeded 3 million. The infrastructure did not precede adoption, it was pulled into existence by it.

Solar and Wind Before Grid Storage Renewable energy was deployed at scale globally before adequate battery storage or transmission infrastructure existed for it. Solar and wind costs have since dropped over 80% in a decade; battery costs by almost 90% since 2010. In 2024, over 90% of all new power generation capacity worldwide came from renewables. Deployment created the economic incentive that made storage worth investing in, not the other way around.

UPI Before Smartphones Were Universal in India

This is the most directly relevant analogy. UPI launched in 2016 as a digital payments protocol before smartphone penetration and internet access were guaranteed across India’s rural and lower-income populations. The infrastructure it needed (affordable data, merchant terminals, feature phone compatibility) followed because the system was worth building toward. Today, India’s UPI processes 50% of the world’s digital transaction volume: over 250 billion transactions annually worth $3.4 trillion. India then exported the technology to 25 countries.

Across all three: the infrastructure gap was the starting condition, and when the product kicked off, the infrastructure gaps were filled.

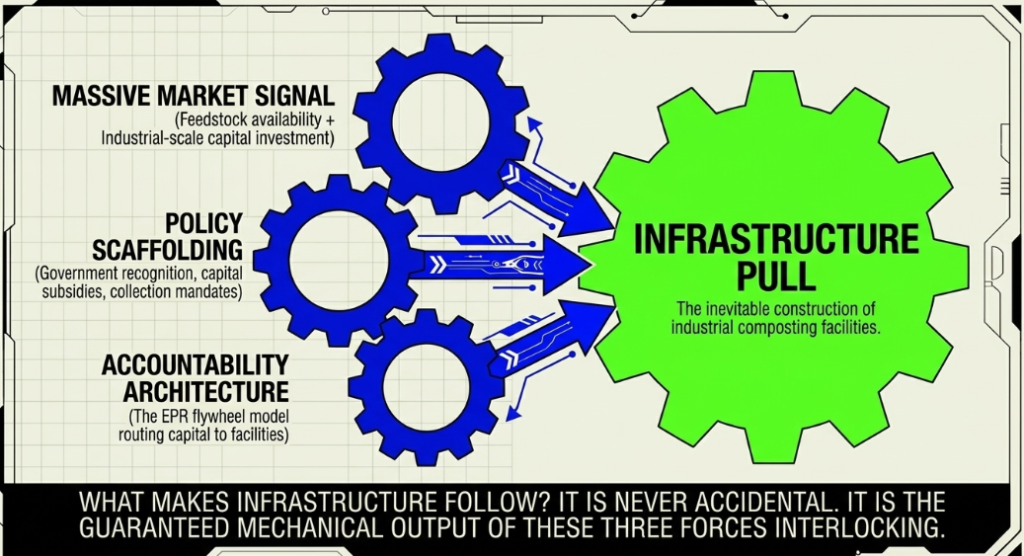

Why India’s Push on Compostable Bioplastics Is Structurally Sound And Not Speculative

India’s current momentum on compostable bioplastics is grounded in three realities:

- India’s feedstock position for domestic PLA production

- India is the world’s second-largest sugarcane producer and fourth in corn cultivation; both these crops are the primary feedstocks for PLA packaging India needs domestically.

- Over 80% of bioplastics currently used in India are imported, meaning domestic production at scale will materially reduce the cost of certified compostable materials and make local composting infrastructure economically viable at lower volume thresholds.

- Major leaps in domestic bioplastics production

The most significant market signal is Balrampur Chini Mills’ Bioyug plant, announced in 2025 with a ₹2,850 crore investment. It will be the world’s first facility to convert sugarcane to PLA at a single integrated site, powered entirely by renewables, with 80,000 tonnes per year production capacity commissioning in 2026. This is an industrial-scale commitment that changes the domestic supply economics of PLA packaging India entirely.

3. The regulatory and policy frameworks

- The EY-ASSOCHAM report recommends capital subsidies of up to 50% on eligible bioplastics investments and a National Bioplastics Policy including composting infrastructure provisions.

- India’s BioE3 Policy (2024) formally recognises biopolymers as a strategic sector for achieving net-zero by 2070.

- India’s bioplastics market is growing at over 20% annually, and is projected to reach $2.3 billion by 2033

When the domestic market signal is large enough and the supply chain local enough, composting infrastructure investment has a rational economic case.

India is approaching that threshold.

The Process Gap — Why “Compostable” Must Not Become the New “Recyclable”

Stat: Globally, only 9% of all plastic ever produced has been recycled. In the United States, the recycling rate has fallen by half since 2014; from 9.5% to roughly 5–6% today.

The “recyclable” label was placed on plastic products for decades, but the infrastructure to fulfil that promise was never built at scale. The label became a permission slip for continued production and not a system for environmental responsibility. Public trust has not recovered.

Industrial compostable packaging faces the same structural risk.

- A certified compostable product that ends up in a landfill because there is no collection system, no composting facility nearby, and no consumer education is functionally equivalent to a conventional plastic product.

- The certification itself and the presence of industrial composting infrastructure mean nothing without the process that gives it meaning.

The difference between industrial composting and recycling’s failure is that accountability can be designed into the system from the start.

Italy’s Biorepack model demonstrates exactly how.

What Could Close the Industrial Composting Process Gap in India: The Four Levers

1. Strict certification enforcement

Only CPCB-certified compostable products should be permitted in the market. Counterfeit and mislabelled products contaminate compost streams, degrade compost quality, and undermine the investment case for facilities.

India has issued 267 e-certificates to manufacturers as of mid-2025. So, the framework exists; enforcement at market scale is the next step.

2. Redirecting bioplastic EPR India collections toward composting infrastructure

India’s EPR framework already mandates a 100% collection target for compostable plastics (Category IV) from 2023–24. This is the strictest target in the entire plastic packaging regime.

The missing mechanism is the Italy model: bioplastic EPR India contributions should flow directly to municipalities and composting operators to cover facility and collection costs. Biorepack’s structure is a ready template.

3. Using concentrated corporate waste streams as anchor feedstock

India’s food delivery platforms, retail chains, and large FMCG operations already use certified compostable packaging at significant volume. These are geographically concentrated, predictable waste streams — the kind that make a composting facility economically viable because feedstock supply is not uncertain. This mirrors Australia’s FOGO model, where mandated organic waste programs created the feedstock certainty that justified facility investment.

4. Channeling existing program funding toward composting infrastructure

Swachh Bharat Mission and Smart Cities Mission already fund urban waste management infrastructure. Directing a portion of that funding specifically toward industrial composting facilities for certified compostable packaging does not require new legislation; only directed allocation within existing frameworks.

The Infrastructure Gap Is the Starting Point, Not the Final Word

Three registered industrial composting units in a country of 1.4 billion is a baseline, not a verdict.

Italy had a fragmented, underfunded composting system before Biorepack.

The US had fewer than 100 plants capable of processing certified compostable packaging before policy intervention.

UPI launched into a country where cash dominated nearly every transaction.

None of those systems waited for infrastructure to be complete before committing to the product. They committed to the product, built the accountability architecture, and the infrastructure followed.

India has a ₹2,850 crore PLA packaging plant under construction.

It has an EPR framework with a 100% collection mandate already in force for compostable plastics.

Its compostable bioplastics market is growing at 20% annually.

This trajectory is what matters.

So, the right question is not what is the point of industrial compostable packaging without infrastructure. It is: what will make the infrastructure follow?

The mechanisms are known.

- Italy has shown what they produce when applied consistently.

- India has the feedstock, the policy scaffolding, and the industrial investment to make the same case.

The commitment to execute is what determines whether “premature” becomes “pioneering.”

Ukhi researches and develops industrial compostable packaging from agricultural inputs, producing biopolymer solutions designed for existing packaging lines and certified to industrial composting standards. Research published on this site is independent.