The next major climate infrastructure category is circular materials manufacturing — and it is significantly underfunded.

The energy transition has, by now, attracted serious institutional capital.

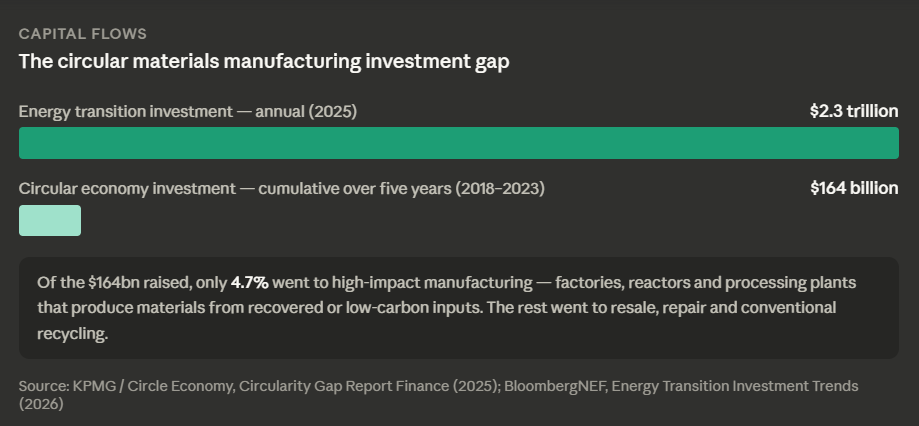

Global energy transition investment hit a record $2.3 trillion in 2025, according to BloombergNEF, covering solar, wind, EVs, batteries and grids. So that category is no longer early-stage.

The question sophisticated investors should now be asking is: which climate infrastructure category is at an early stage today?

The answer is circular materials manufacturing.

What is circular materials manufacturing?

Circular materials manufacturing is the industrial infrastructure that produces materials such as steel, cement, plastics and fibres using recovered waste, captured CO₂, bio-based feedstocks and renewable energy, rather than virgin raw materials.

CMM requires gigafactory-scale capital expenditure, project finance and long-term offtake contracts — the same financial architecture that was used to build the renewable energy industry.

CMM operates across four feedstock pathways:

- Captured CO₂ reformed into hydrocarbons, fuels, polymers and cement-grade carbonates

- Post-consumer and industrial waste chemically broken down and reconstituted into monomers and pure metals

- Bio-based feedstocks — sugars, agricultural residues, engineered microbes — fermented or grown into fibres, proteins and chemicals

- Renewable electricity and green hydrogen used as chemical reductants to replace coal in steelmaking and natural gas in chemicals

CMM can address roughly half of all global greenhouse gas emissions, and this is the half that clean energy cannot fix.

It has binding corporate demand already in place.

It is supported by a hardening regulatory floor.

Yet, it has received a fraction of the capital that energy has attracted. That gap is the opportunity this thesis sets out.

The Circular Materials Manufacturing Investment Gap: Where Capital Has — and Has Not — Gone

Between 2018 and 2023, businesses engaged in the circular economy raised approximately $164 billion globally, according to a KPMG and Circle Economy study.

Investment surged 87% in 2021–2023 versus the prior three years. On the surface, that looks like momentum.

The problem is where the money went.

- Only 4.7% of that capital flowed to high-impact Design and Production models — meaning the physical factories, reactors and processing plants that manufacture materials from recovered or low-carbon inputs at industrial scale.

- The overwhelming majority went to resale platforms, repair services, and conventional recycling operations: lower-impact, more familiar, easier to fund.

Stat: CMM addresses a share of global emissions roughly equivalent to the energy sector — yet, at $164 billion cumulative over five years, receives around one-fourteenth of the capital flowing into energy transition investment annually ($2.3 trillion invested in 2025).

This is a structural mismatch between where emissions come from and where capital goes and it represents a clear entry point for investors with a medium-to-long horizon.

Why Circular Materials Manufacturing Is The Next Big Opportunity

Circular materials manufacturing does not occupy the same space as most climate investments. It is not a bet on policy generosity or consumer behaviour change. It is a response to a set of physical and economic constraints that are independent of any political cycle. This section sets out the drivers that underpin the investment case.

Why Clean Energy Investment Does Not Reach Materials-Manufacturing Emissions

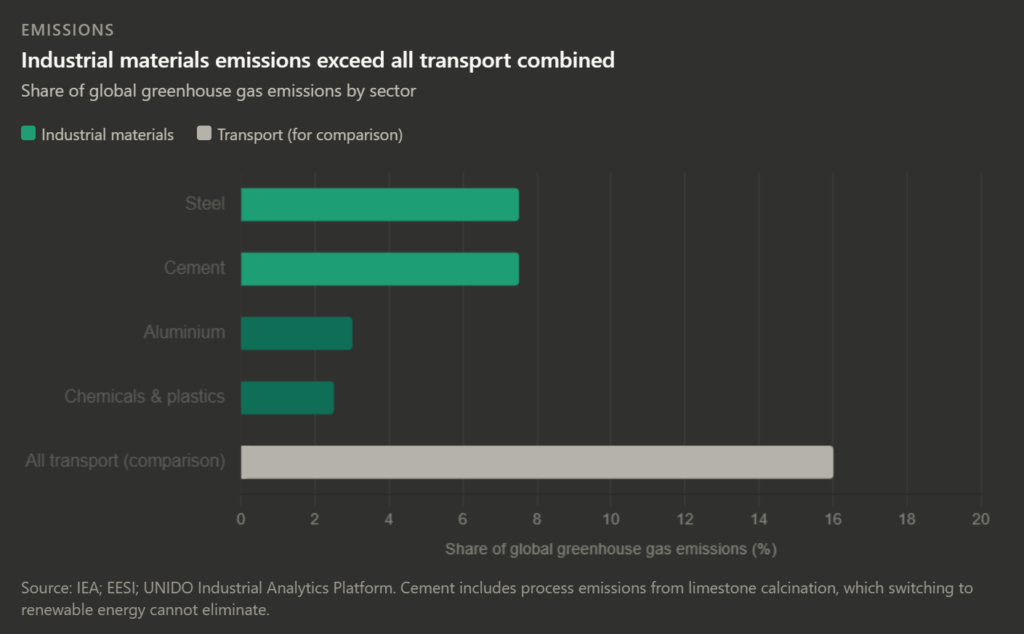

Energy decarbonisation (however necessary) does not solve the emissions embedded in the physical materials the world makes and uses. The industrial processes that produce steel, cement, plastics, chemicals and aluminium account for over a quarter of global greenhouse gas emissions on their own, more than all forms of transportation combined.

The Emissions Footprint of Key Industrial Materials

- Steel produces approximately 7–8% of global CO₂ emissions. Around 1.9 billion tonnes are produced each year.

- Cement is responsible for another 7–8%, with roughly half of those emissions coming from the chemistry of limestone calcination, a process that cannot be fixed by switching to renewable energy alone.

- Plastics and chemicals contribute a further 880+ million tonnes of CO₂ annually, with petrochemical demand projected to grow through 2050.

- Aluminium accounts for around 3% of direct industrial emissions, with smelting and anode production as the dominant sources.

Global Material Extraction Is Accelerating, Not Slowing

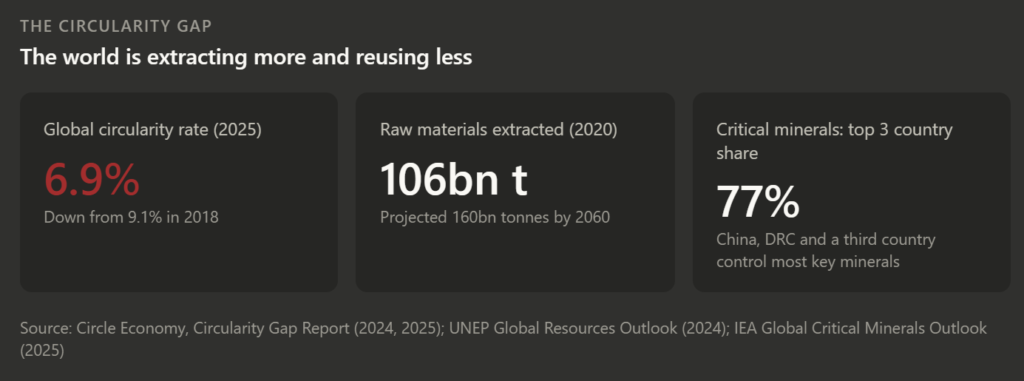

The world extracted 106 billion tonnes of raw materials in 2020, up from 30 billion tonnes in 1970. This is a tripling in five decades. By 2060, that figure is projected to reach 160 billion tonnes.

Meanwhile, the Circularity Gap Report 2024 recorded a global circularity rate of just 7.2%, down from 9.1% in 2018 — a measure that fell further to 6.9% in 2025. The world is extracting more and reusing less.

Critical Mineral Concentration Makes Circular Materials a Supply-Chain Security Play

The IEA’s Global Critical Minerals Outlook 2025 finds the top three mining countries control 77% of supply across key energy minerals.

- China alone refines 50–70% of global lithium and cobalt, and over 90% of battery-grade graphite.

- In late 2024, China began restricting exports of gallium, germanium, antimony and heavy rare-earth elements.

- Over half of energy-related minerals are now subject to some form of export control.

Circular materials manufacturing is, as a result, not only a climate investment but also a supply-chain security investment.

The Investor Framing

The investment logic here is what practitioners call the picks-and-shovels logic: rather than betting on which specific material or technology wins, the investment case rests on the infrastructure layer that all of these sectors need. Steel, cement, plastics and textiles each require purpose-built industrial plants capable of producing at scale from recovered or low-carbon inputs. CMM is that shared industrial layer.

The Circular Materials Manufacturing Company Landscape

The category is no longer pre-commercial. Below is a map of the most significant operators by archetype, with verified funding figures.

Green steel

- Stegra (Sweden, formerly H2 Green Steel):

- Hydrogen-DRI plant under construction in Boden, Sweden

- Secured approximately €6.5 billion in combined equity, senior debt and EU Innovation Fund grants

- Customer offtakes with Porsche, Volvo, IKEA and Mercedes-Benz already signed

- Boston Metal (USA):

- Molten oxide electrolysis for zero-carbon primary steel

- $282 million Series C, backed by ArcelorMittal, Microsoft Climate Innovation Fund and Breakthrough Energy Ventures.

CO₂-to-materials

- Twelve (USA)

- Electrochemical carbon transformation into fuels and chemicals

- $645 million raised in 2024, led by TPG Rise Climate, with Amazon, Coca-Cola and Mitsui as strategic investors.

- LanzaTech (USA, Nasdaq-listed):

- Gas fermentation converting industrial emissions into ethanol and chemicals

- Approximately $869 million raised cumulatively

Circular plastics

- Eastman Chemical (USA):

- Methanolysis facility operational in Tennessee

- Up to $375 million in US DOE funding for a second US plant

- €1 billion France facility under development

- Total recycling investment approximately $2.25 billion

- PureCycle Technologies (Nasdaq: PCT):

- Solvent-based polypropylene purification

- $300 million raised in 2025 to fund a $2 billion three-continent expansion targeting 450,000 tonnes per year capacity by 2030

Low-carbon cement

- Sublime Systems (USA):

- Electrochemical zero-emission cement

- $140 million+ raised

- Signed a binding 622,500-tonne offtake with Microsoft.

- Fortera (USA):

- CO₂-to-cement reactive carbonates

- $85 million Series C with Microsoft as a strategic investor

Battery and critical mineral recycling

- Redwood Materials (USA):

- Closed-loop battery recycler and cathode/anode materials producer

- Approximately $2.3 billion in private equity raised, plus a $2 billion DOE loan

- Partners include Panasonic, Ford, GM, Volkswagen, Toyota and BMW

- Holds approximately 70% of the US battery recycling market

Textile circularity

- Ambercycle (USA):

- Polyester regeneration into recycled fibre

- $21.6 million Series A

- Multi-year offtakes with Inditex and MAS Holdings

- First commercial plant targeted for 2026.

- Syre (Sweden, H&M Group spin-out):

- circular polyester backed by a $600 million H&M offtake commitment

How Regulation Is Building a Demand Floor for Circular Materials

The policy case for circular materials manufacturing is more durable than for many climate-tech categories because the primary regulations are already enacted and phasing into force.

| Regulation | Geography | What It Does | Timeline |

| CBAM | EU | Carbon tariff on cement, steel, aluminium imports | Definitive phase: Jan 2026 |

| EU Battery Regulation | EU | Minimum recycled-content mandates for cobalt, lithium, nickel | Thresholds from 2027–2031 |

| IRA §45X | USA | Production tax credit for recycled critical minerals | Finalised Oct 2024 |

| IDDI | Global | Green public procurement of low-carbon steel and cement | Covers 25–40% of global construction-materials markets |

CBAM is the most consequential of these for near-term investment. Importers of steel, cement and aluminium into the EU must now purchase certificates priced against the EU Emissions Trading System. This implies there is effectively a carbon cost imposed on high-emission production wherever it occurs. Clean producers, including CMM operators, are exempt from this cost.

The practical result is a growing price advantage for green steel, low-carbon cement and circular aluminium in Europe’s market. This mirrors the role that feed-in tariffs and renewable portfolio standards played in making solar and wind economically viable before cost curves fell far enough to stand alone.

Why the Circular Materials Manufacturing Investment Window Is Open Now

Three conditions are converging at the same time, which is what defines a category inflection point in infrastructure investing.

- Technology is reaching commercial scale across multiple archetypes simultaneously. Stegra, Boston Metal, Sublime, Twelve, Redwood and PureCycle are all in active build-out as of 2026.

- Corporate offtake de-risking capital: Microsoft, Apple, IKEA, H&M, Amazon, Mercedes-Benz and others have signed binding multi-year supply agreements. These contracts reduce off-take risk and improve the bankability of project finance.

- Mainstream capital has not yet arrived: Pension funds, infrastructure allocators and sovereign wealth funds — the capital pools that drove the final scaling phase of renewable energy — have not yet moved into CMM in volume. Returns in infrastructure investing compress as large pools of capital enter. The entry window is before that happens.

Insight: Northvolt’s bankruptcy, Ascend Elements’ Chapter 11 filing in 2025, and the rescission of several US DOE grants are read by some investors as signals that the category is too risky. History tells otherwise. In 2011, Solyndra — a US solar manufacturer — collapsed after receiving $535 million in federal loan guarantees. That failure was followed by a decade in which solar module costs fell 90% and global installed capacity grew 25-fold. Early-stage industrial categories go through a shakeout phase in which weaker operators fail and the underlying technology continues to advance. CMM is in that phase now.

Risks that require active diligence:

- CapEx and execution risk is high at gigafactory scale — Stegra required an additional €1.4 billion in emergency financing in 2025 after cost overruns.

- US policy instability is a real variable — DOE grant rescissions in May 2025 removed federal co-funding from several cement projects. European policy, anchored in legislation, is more stable.

- Feedstock economics in chemical recycling depend on the quality, consistency and price of waste-stream inputs — which vary by market.

- Greenwashing risk in chemical recycling is documented; rigorous techno-economic and lifecycle analysis is non-negotiable in diligence.

These are manageable risks with proper structuring. They are also the reason the category remains accessible to early and growth-stage investors before compression sets in.

The Investment Case

Circular materials manufacturing addresses the half of global emissions that clean energy investment does not reach. The category has verified capital demand, named companies in commercial build-out, binding corporate offtake already contracted, and regulation creating a durable demand floor across the EU and US.

The entry points most relevant to investors are Series B and C equity rounds, where technology risk has been substantially de-risked but mainstream infrastructure capital has not yet entered. The conditions that defined the renewable energy entry point are present in circular materials manufacturing today. The difference is that most institutional capital has not yet arrived. That is precisely what makes this moment the entry point.